Download as PDF, PPTX

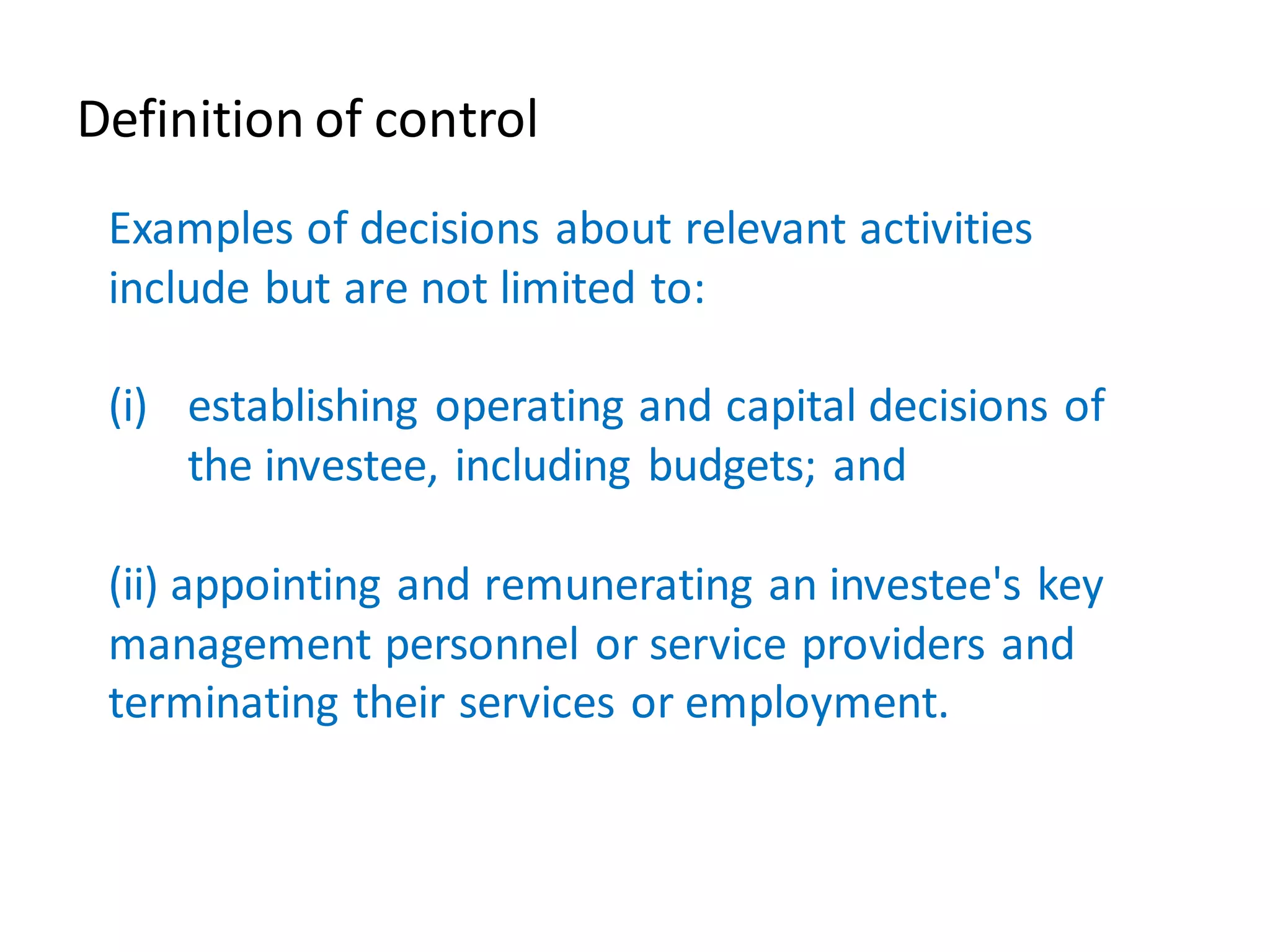

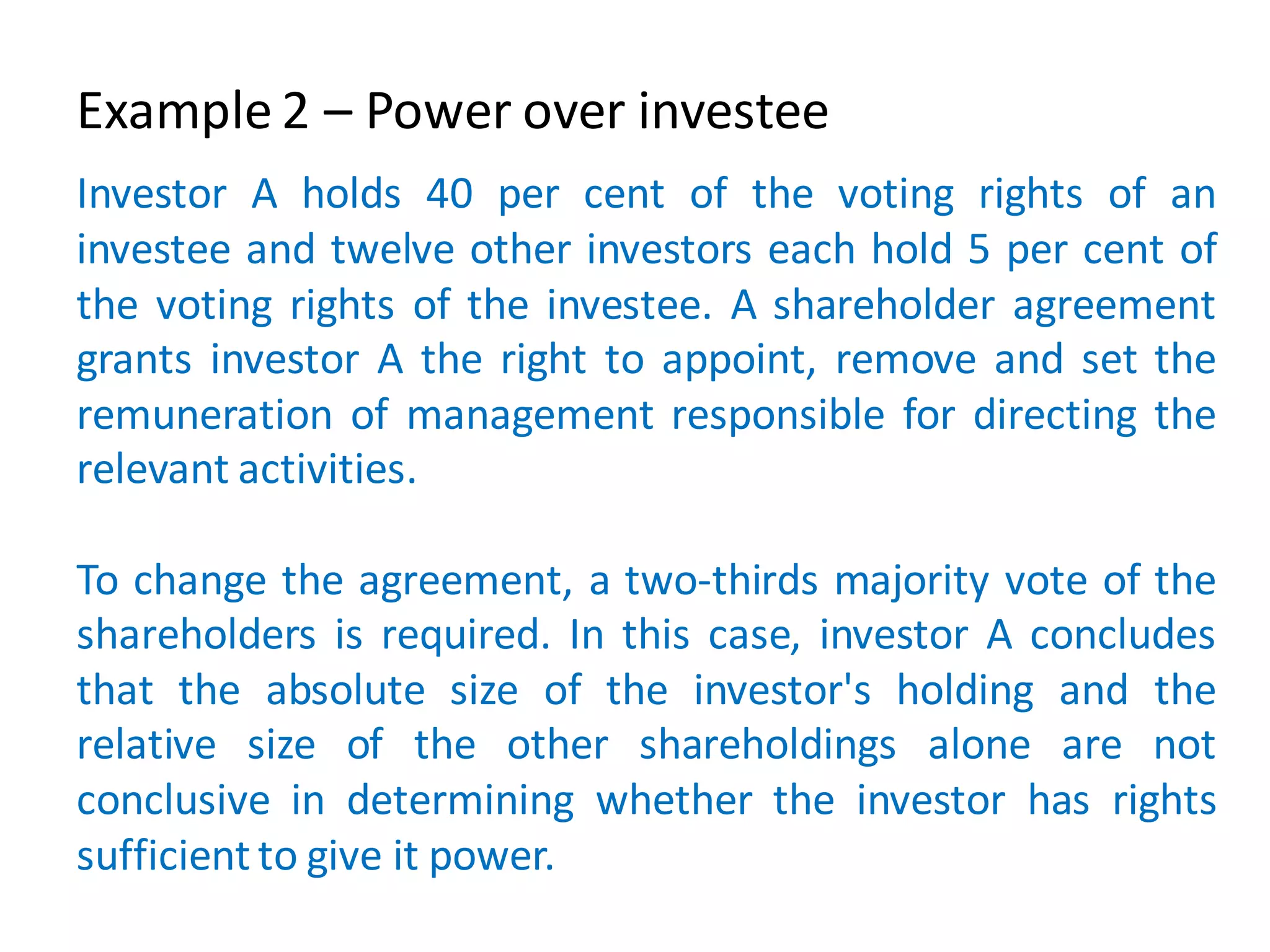

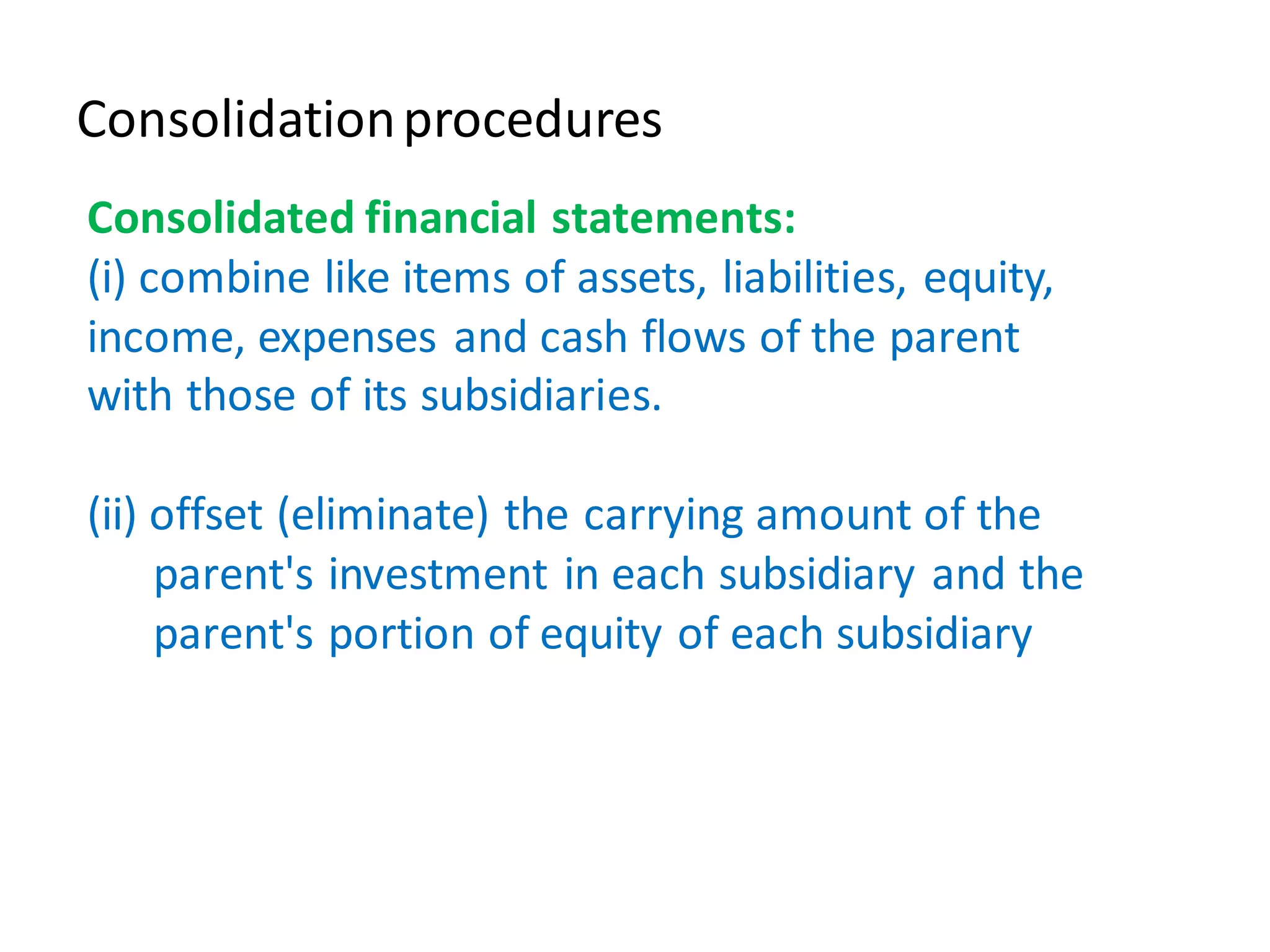

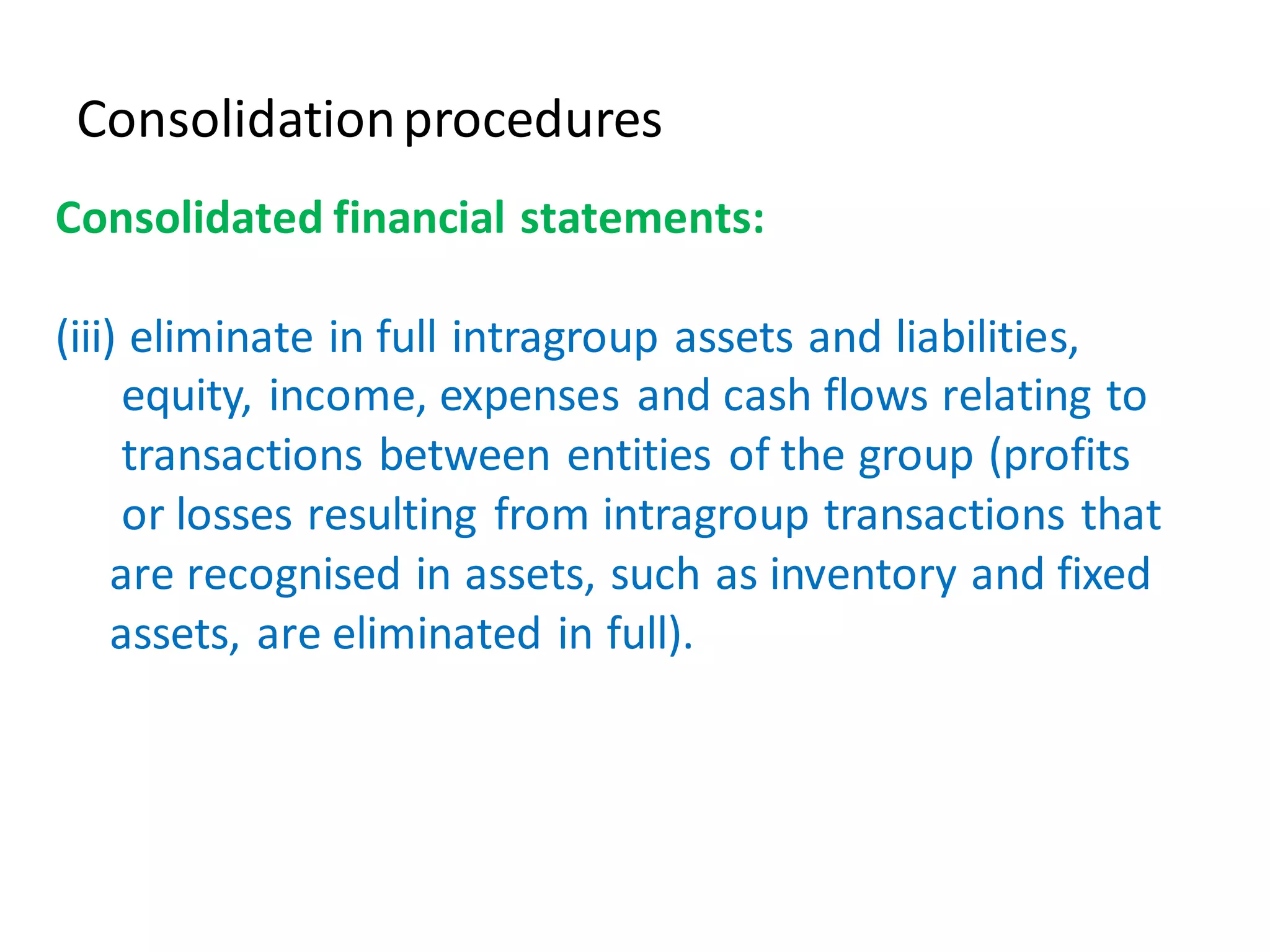

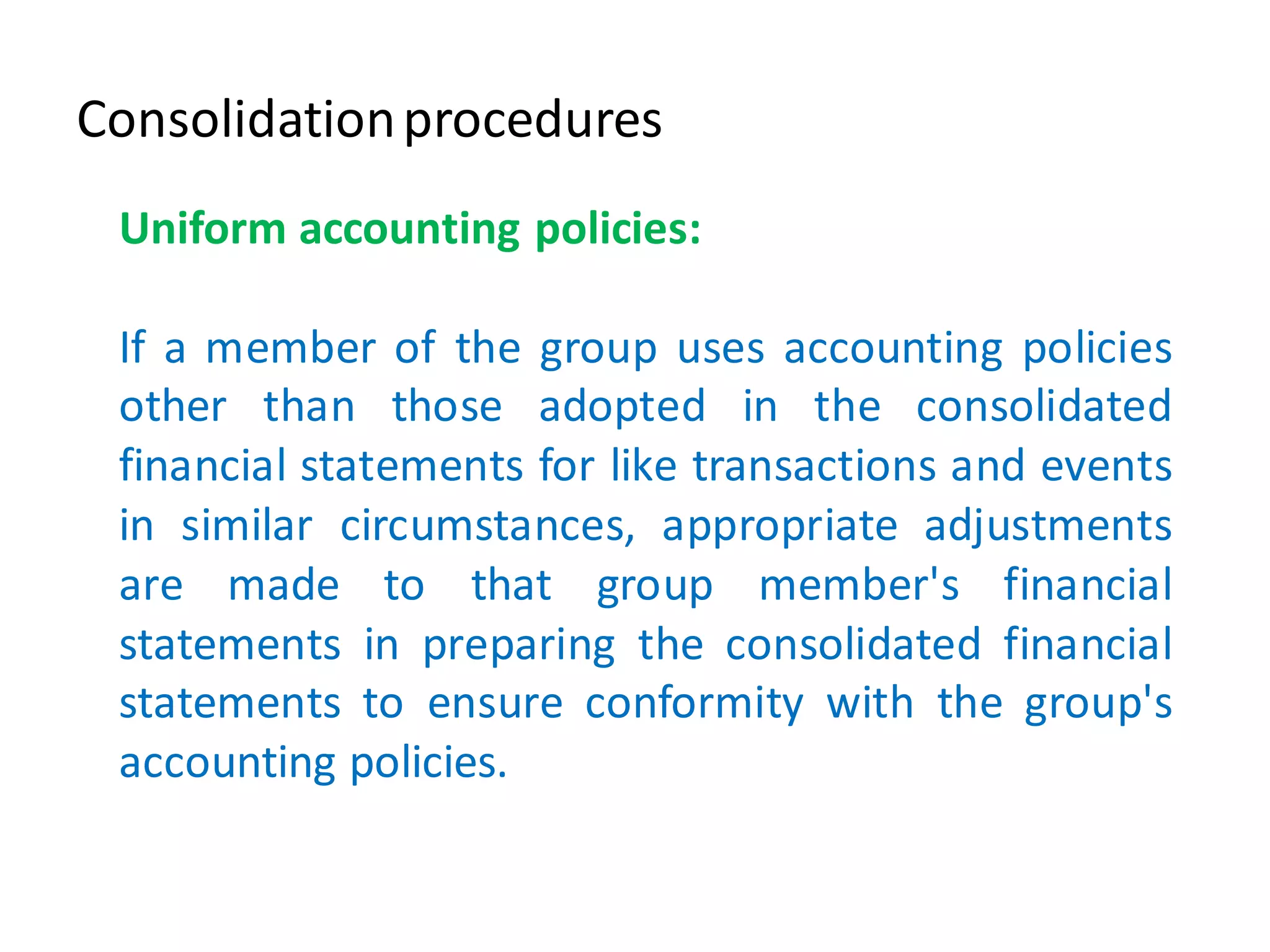

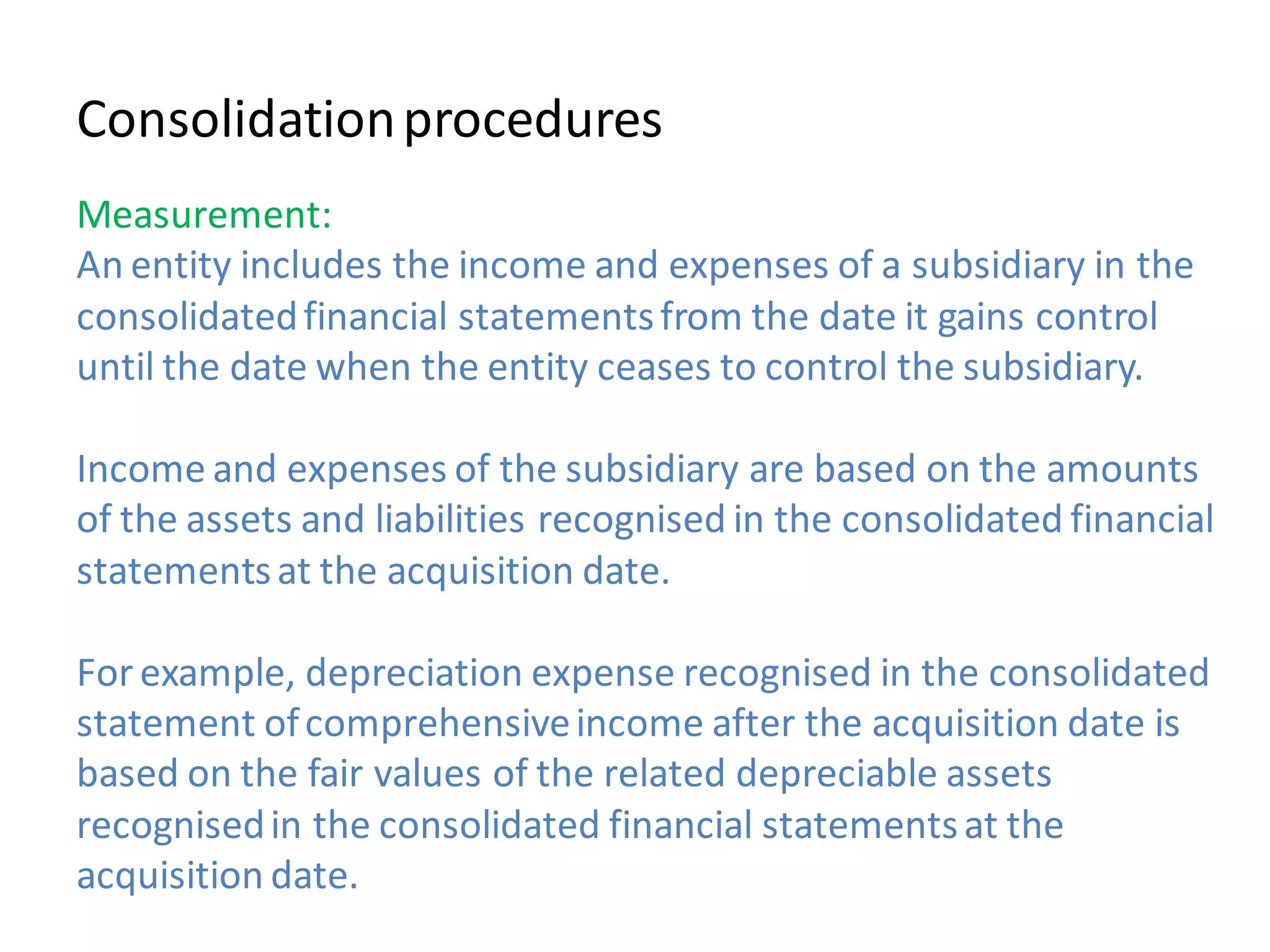

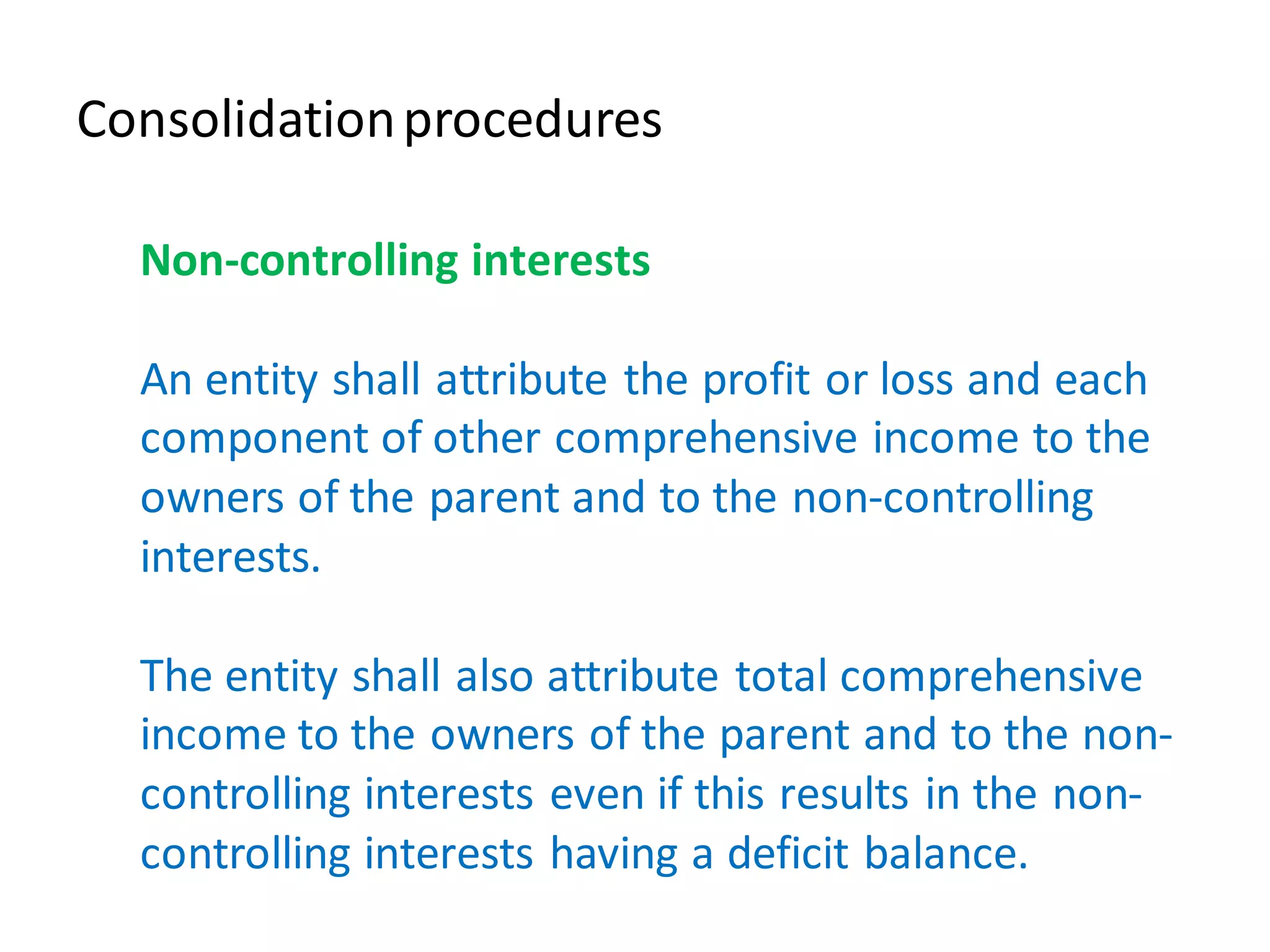

This document summarizes the key aspects of IFRS 10 regarding consolidated financial statements. IFRS 10 establishes the principles for determining when an entity controls another entity and requires their financial statements to be consolidated. Control is defined as having power over an investee, exposure or rights to variable returns, and the ability to use power to affect returns. Control is determined based on relevant activities like operating and financing decisions that significantly impact returns. The consolidated financial statements combine like items from the parent and subsidiaries, eliminate intragroup balances and transactions, and apply uniform accounting policies. Non-controlling interests are presented separately in equity and net income is attributed to the parent and non-controlling interests.

![2014 Annual Report - Separate financial statements February 18, 2015]](https://cdn.slidesharecdn.com/ss_thumbnails/3separate-financial-statements2014-150714153926-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![Indian Accounting Standard [AS] -22 Tax on Income](https://cdn.slidesharecdn.com/ss_thumbnails/as22-150525045409-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)