Downloaded 979 times

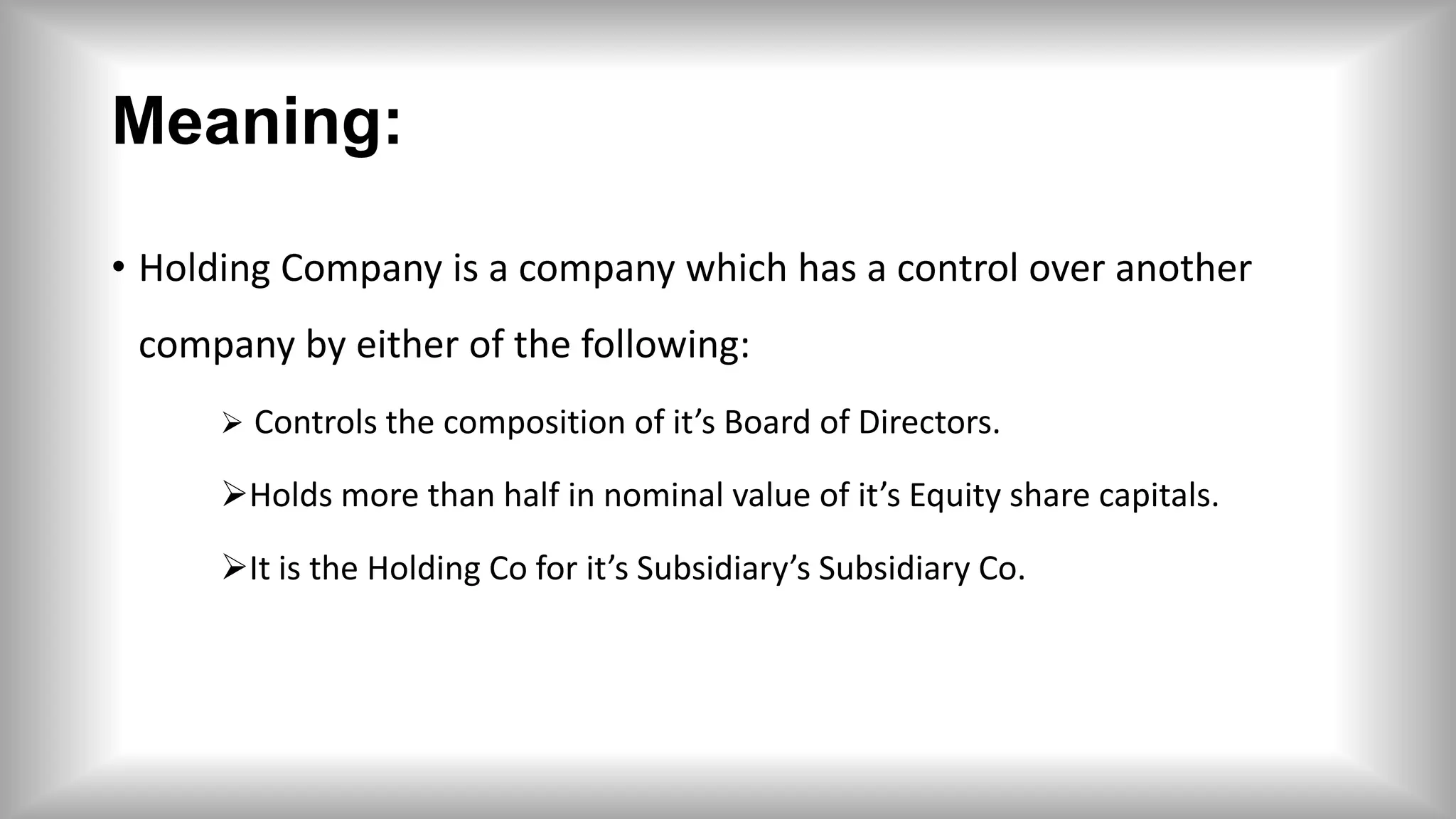

A holding company controls other companies by owning more than half of their equity shares or controlling their board of directors. When consolidating financial statements, the holding company combines its accounts with its subsidiaries' accounts by aggregating profit/loss figures, eliminating inter-company transactions, and merging asset and liability balances. This process eliminates the holding company's investment in shares of subsidiaries from the consolidated balance sheet. It also accounts for minority interests, unrealized inter-company profits, and other adjustments. The consolidated statements present the financial position and performance of the entire corporate group as a single economic entity.