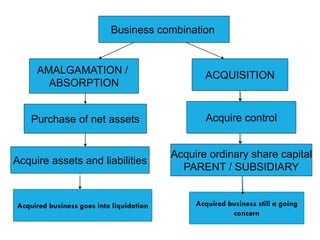

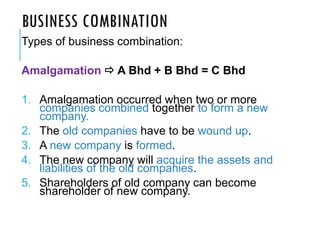

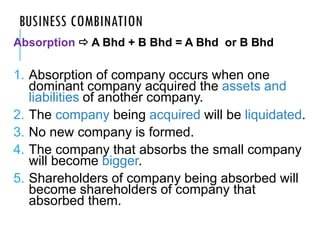

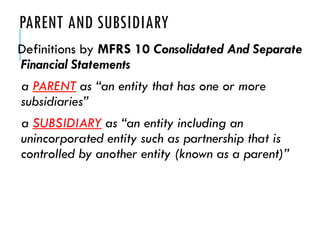

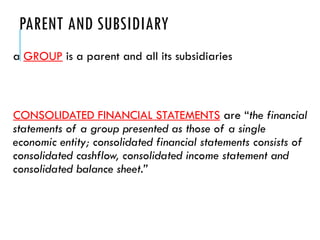

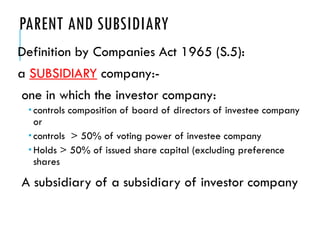

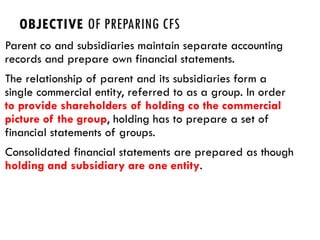

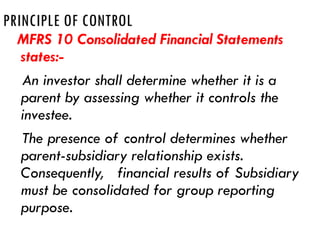

This document provides information on preparing consolidated financial statements. The key points are:

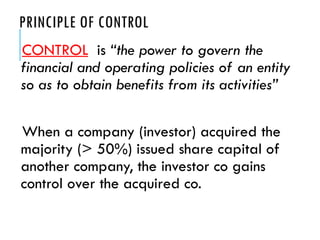

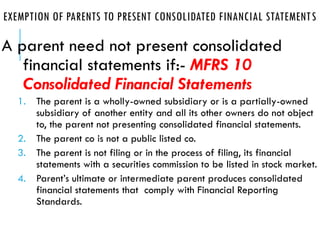

1) It outlines the objectives and principles of consolidated financial statements, including defining a parent/subsidiary relationship and the concept of control.

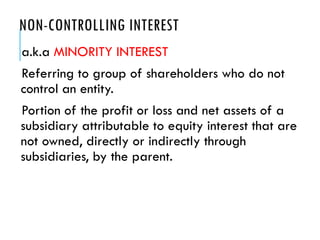

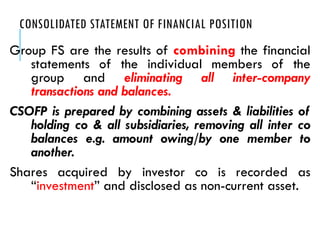

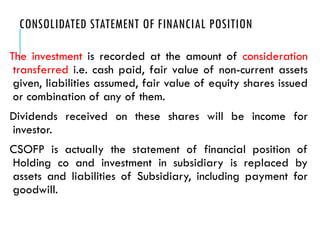

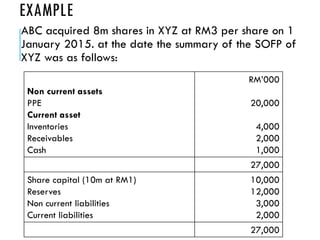

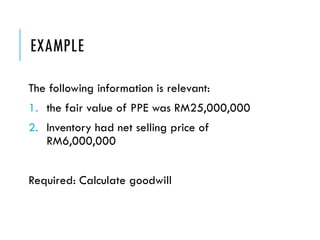

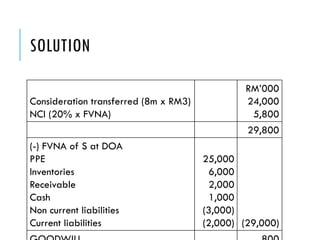

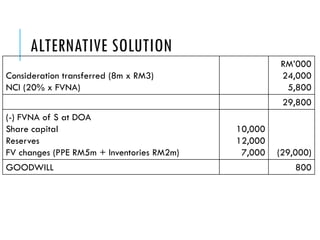

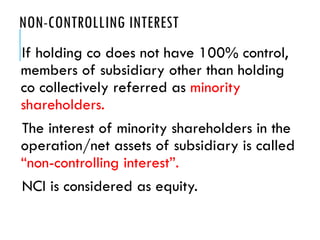

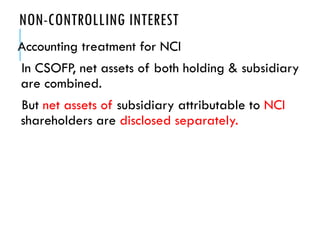

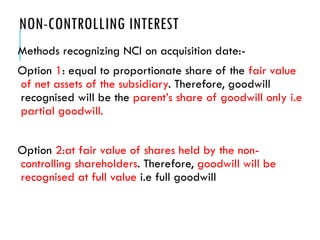

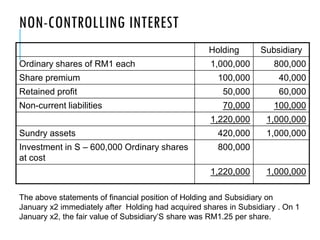

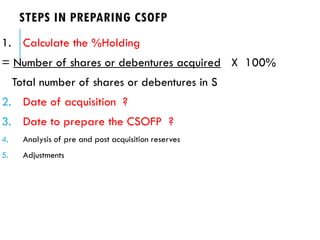

2) It describes the process of preparing a consolidated statement of financial position, including combining individual statements, eliminating inter-company balances, and accounting for non-controlling interests.

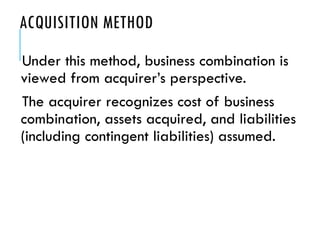

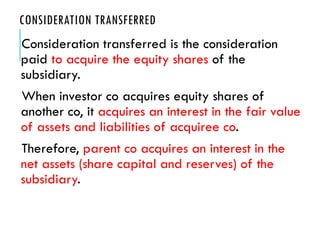

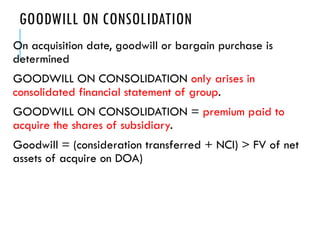

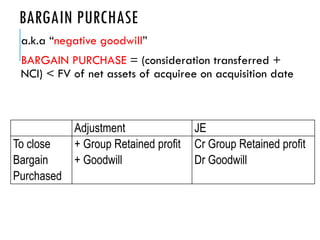

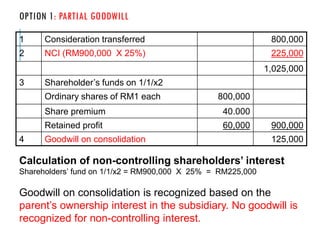

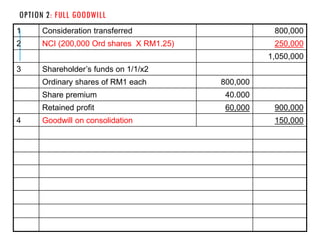

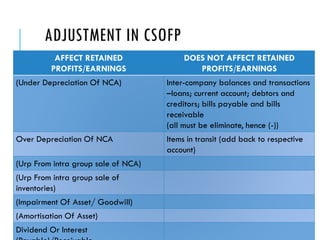

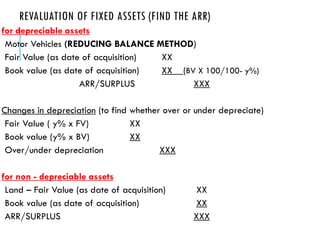

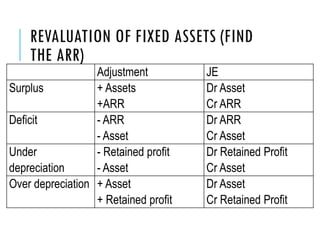

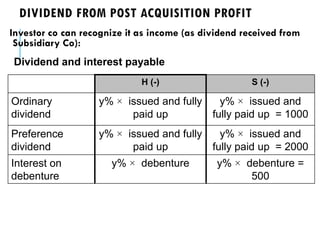

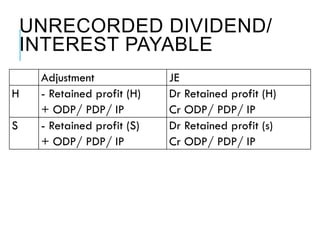

3) It discusses accounting treatments related to business combinations, such as the acquisition method, recognizing goodwill, and adjusting for pre-acquisition and post-acquisition reserves.

The document provides guidance on the technical procedures for preparing consolidated financial statements according to accounting standards.

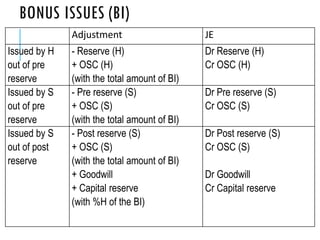

![BONUS ISSUES

Bonus Share/Issue [ a/b X issued and fully paid up]

a) If Holding company issue the bonus share =

+ OSC in the CSOFP

- Reserves of Holding company

If Subsidiary Co. issues the bonus share, identify whether the bonus

share will be taken from PRE or POST reserves a/c.

Out of PRE = + OSC in the schedule

- PRE and Y/E

Out of POST = + OSC in the schedule

- POST and Y/E

Capital Reserve (FROZEN) = %H X Bonus share](https://image.slidesharecdn.com/topic5csofp-230429150659-0f5bde5e/85/TOPIC5-CSOFP-pdf-43-320.jpg)