Downloaded 38 times

![Chapter 4: Reporting financial performance

© Emile Woolf International Limited 89

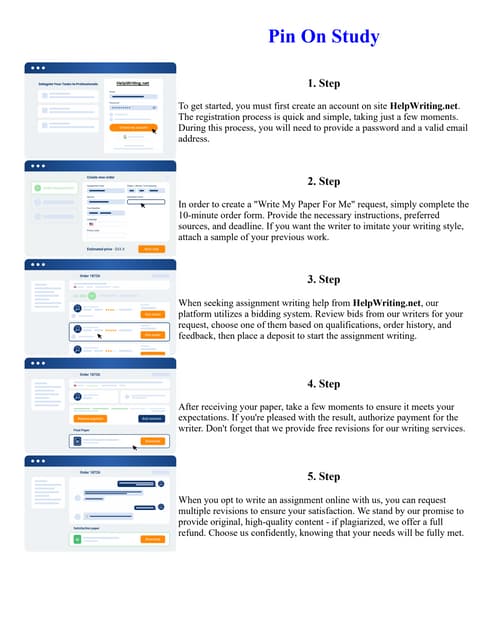

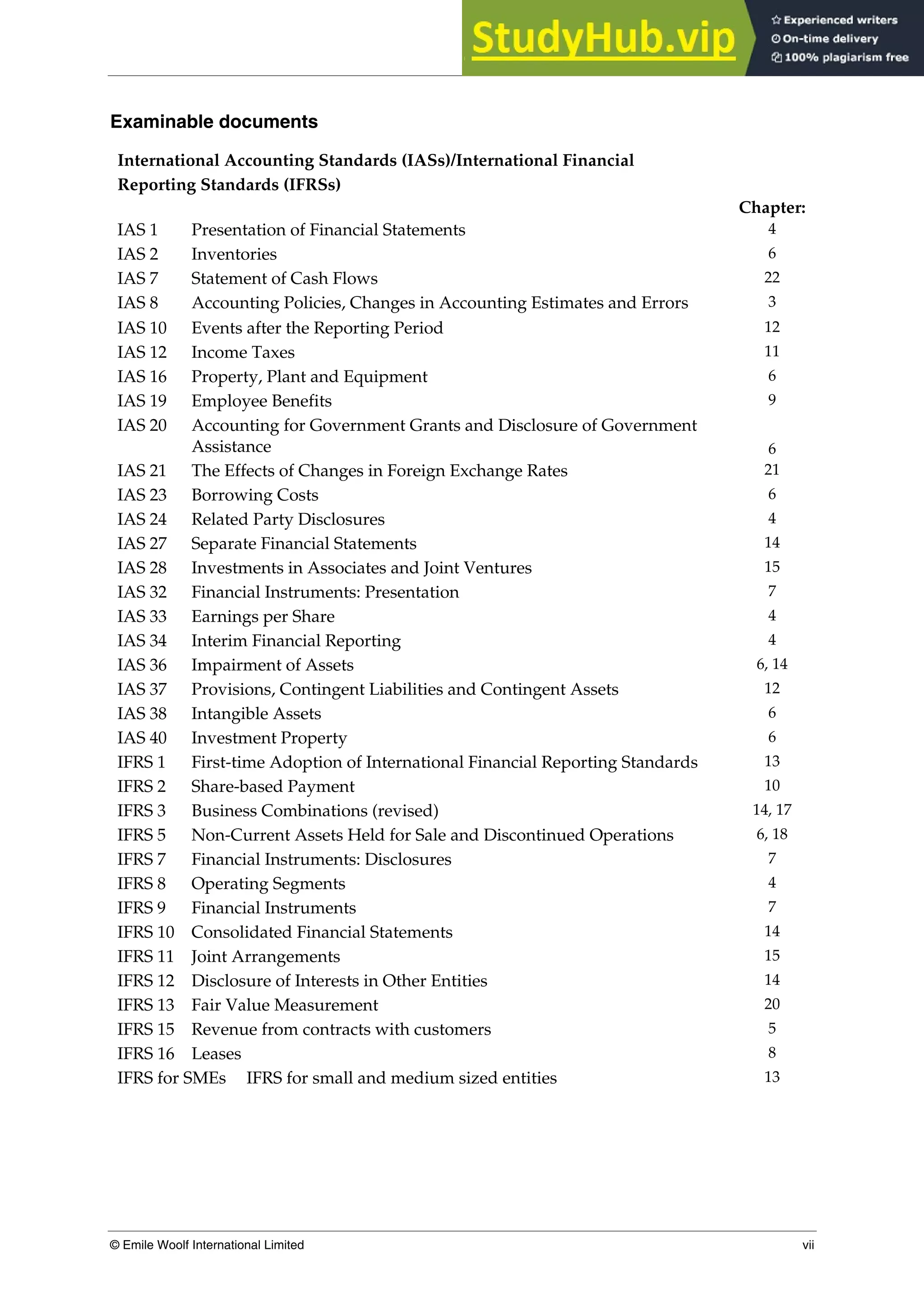

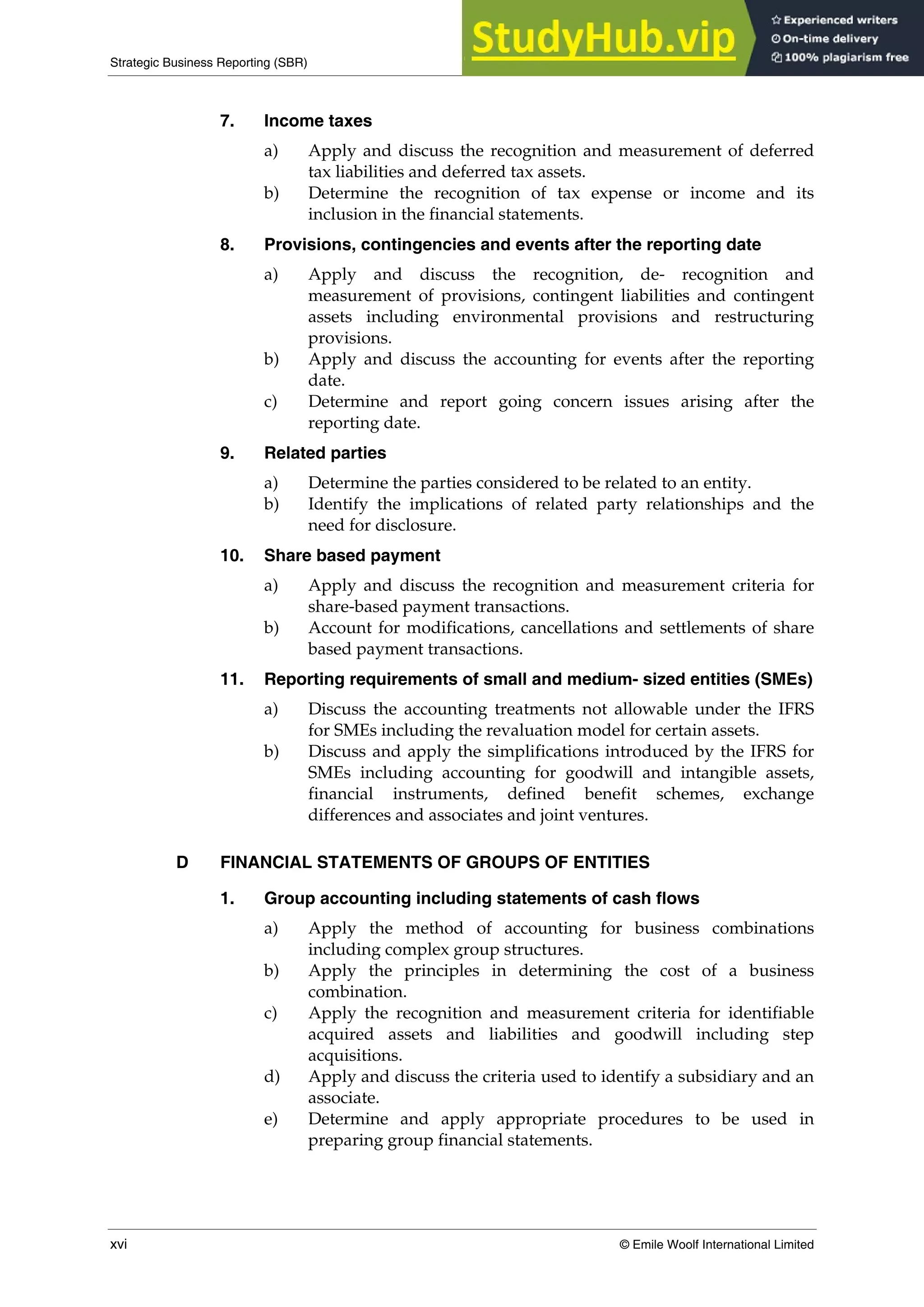

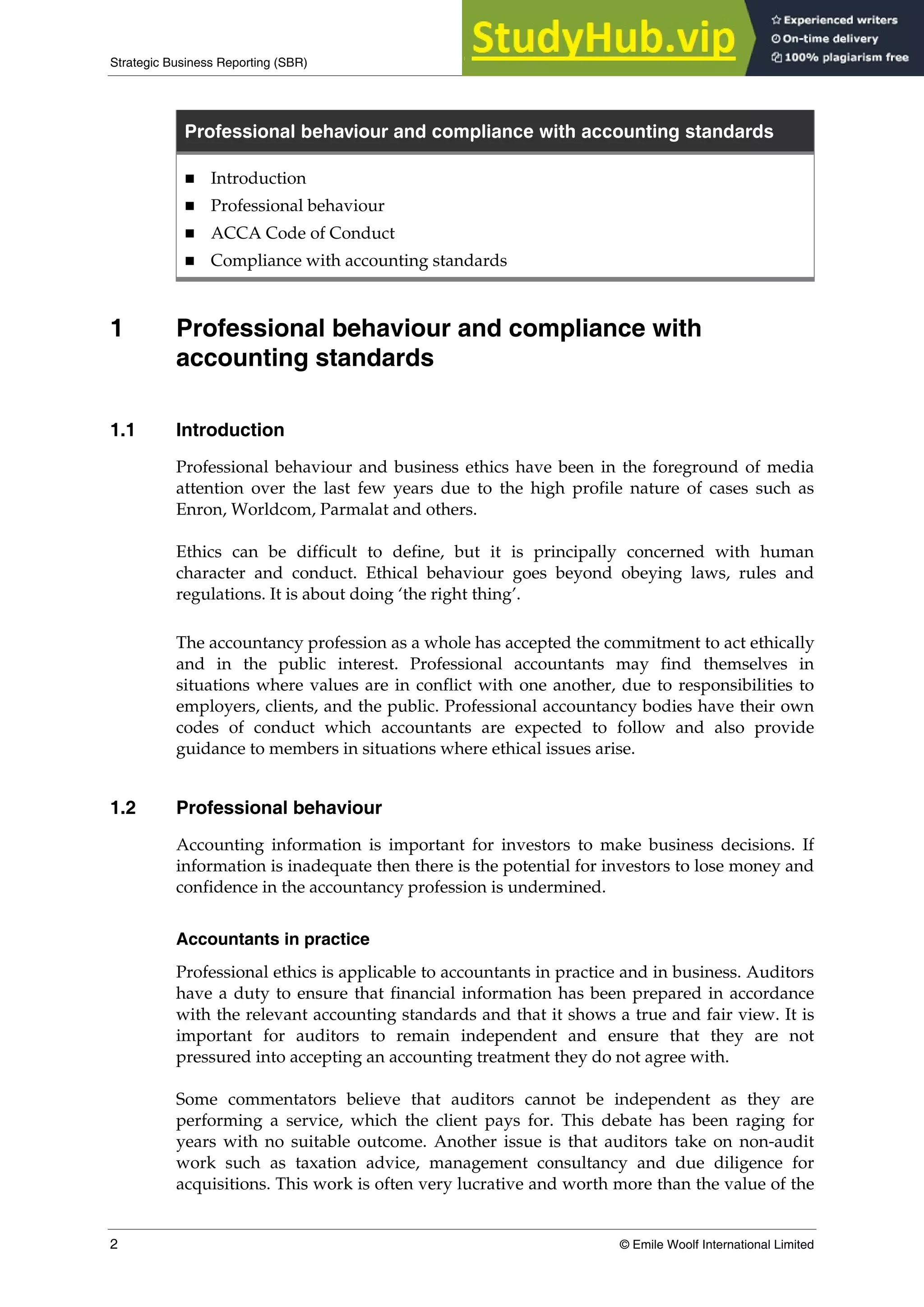

Earnings are the profit (or loss) after tax from continuing operations that are

attributable to the ordinary equity shareholders. With consolidated accounts,

earnings are the profits after tax from continuing operations that are attributable to

ordinary equity shareholders of the parent company (excluding the profit

attributable to non-controlling interests).

Preference dividends are deducted in arriving at the profit attributable to ordinary

equity shareholders. Preference dividends should normally only be deducted from

profit after tax to calculate a figure for earnings if they have already been declared

by the end of the financial year. This is because the company does not have an

obligation to pay the dividend unless it is declared. However, there is an exception

in the case of dividends on ‘cumulative preference shares’. When a company has

cumulative preference shares, the dividend that should be paid must be deducted

from profit after tax to calculate earnings, even if it has not yet been formally

declared. This is because if no dividend is declared, the entitlement of the

shareholders to their dividend remains. There is an obligation on the company to

pay the dividend, and this carries forward to the next financial year, until the

dividend is eventually paid.

Number of ordinary shares in issue. This is the weighted average number of

ordinary shares during the period. Calculating the number of shares in issue can be

fairly complicated.

When shares are issued during the financial year at a full market price, the number

of shares is a weighted average number of shares in issue during the year. This can

be calculated as follows:

Number of shares at the beginning of the year, plus A

Number of shares issued at full market price during the year

× [Number of months in the year after the share issue /12]

B

Weighted average number of shares in the year A + B

Example

A company issued 20,000 ordinary shares at their market price of $5 per share on 1

July 20X7. Its share capital prior to the issue was 200,000 and its profits after tax

were $50,000 for the year to December 20X6 and $70,000 for the year to 31 December

20X7.

The shares were issued at full market price.

The earnings per share in each year are calculated as follows:

20X6: EPS = $50,000/200,000 shares = $0.25

20X7: Weighted average number of shares = 200,000 + (20,000 × 6/12) = 210,000

EPS = $70,000/210,000 shares = $0.33.](https://image.slidesharecdn.com/accastrategicbusinessreportingstudytext-230807154039-3fc63967/75/ACCA-Strategic-Business-Reporting-Study-Text-pdf-111-2048.jpg)

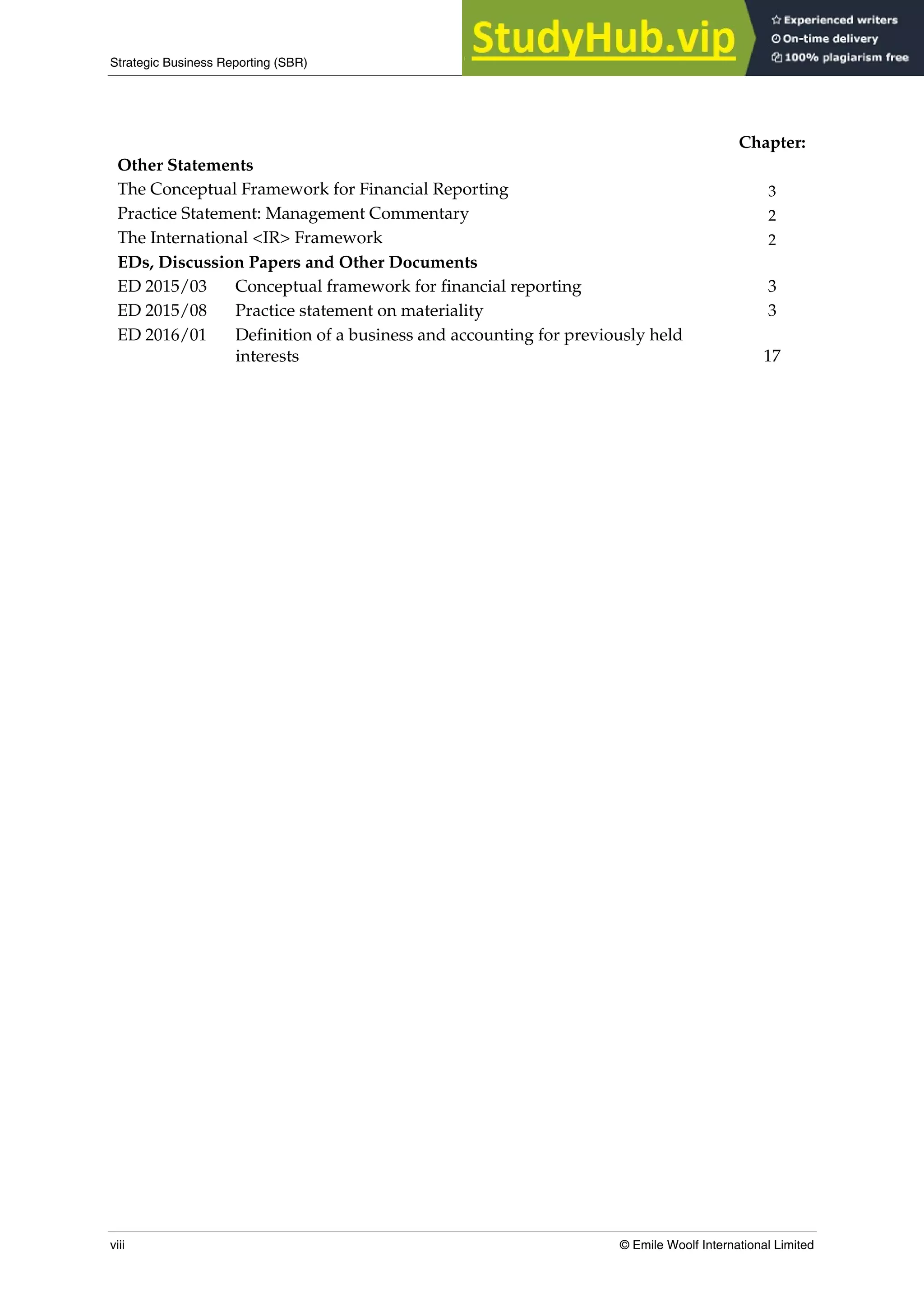

![Chapter 12: Provisions and events after the reporting date

© Emile Woolf International Limited 415

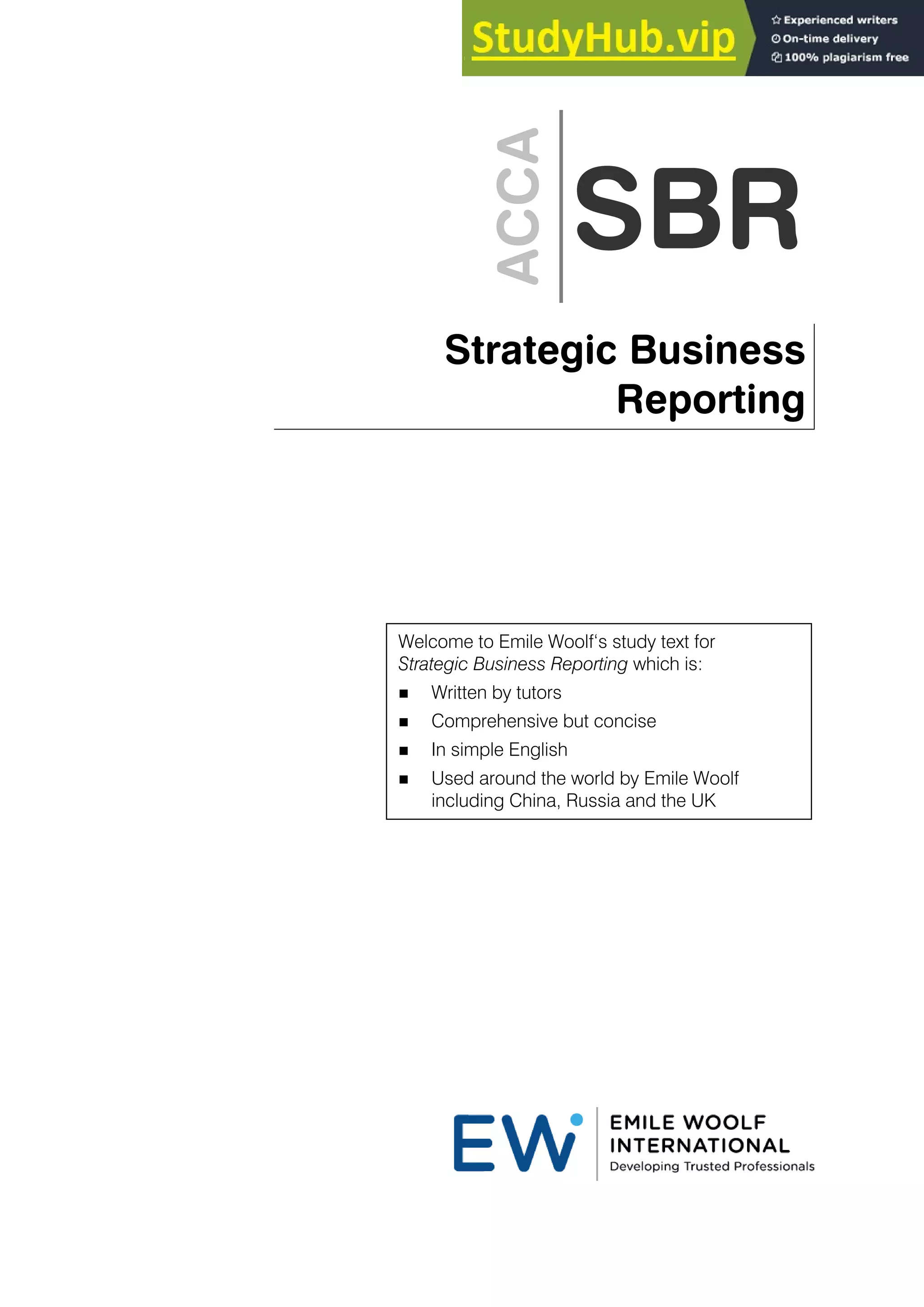

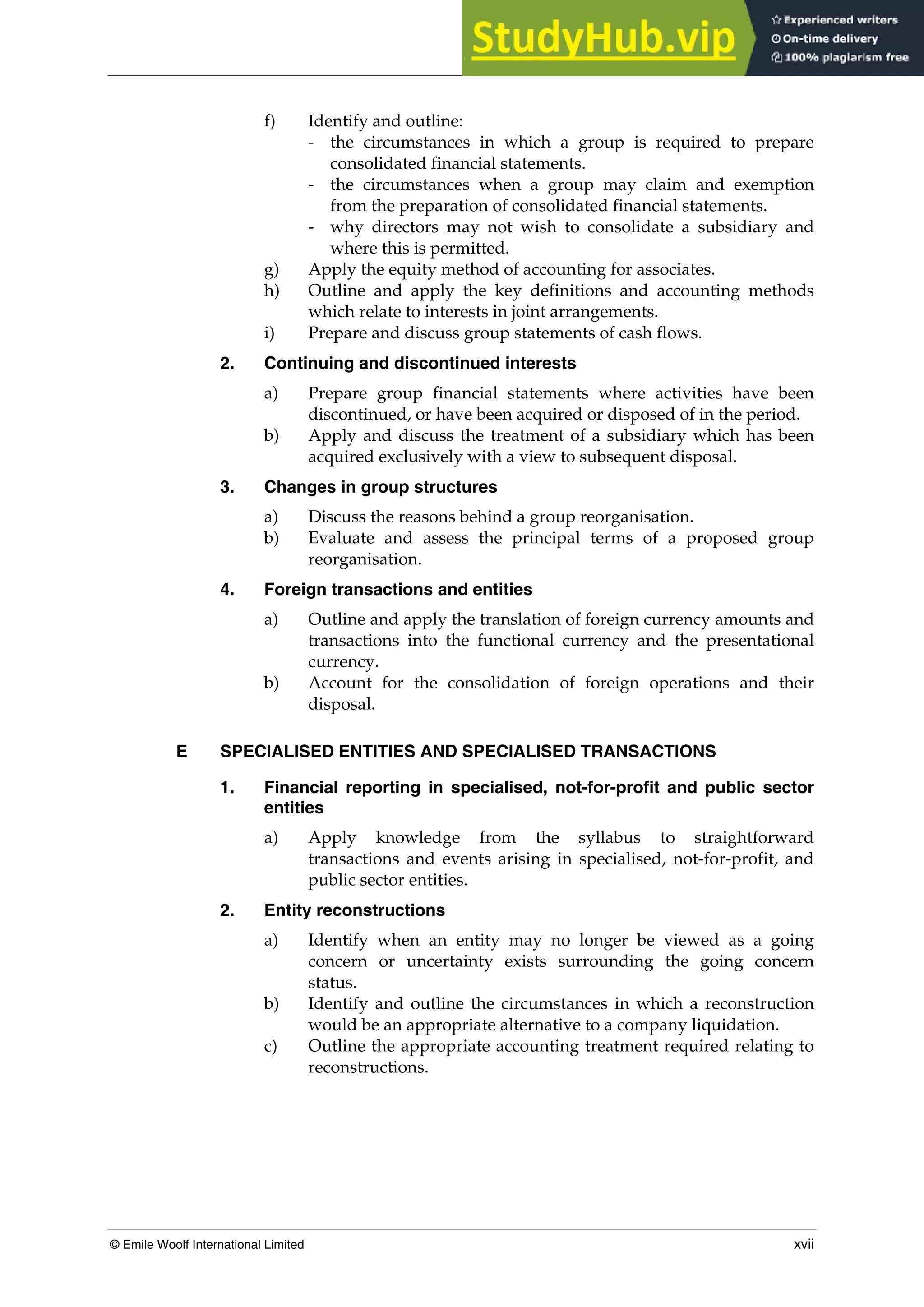

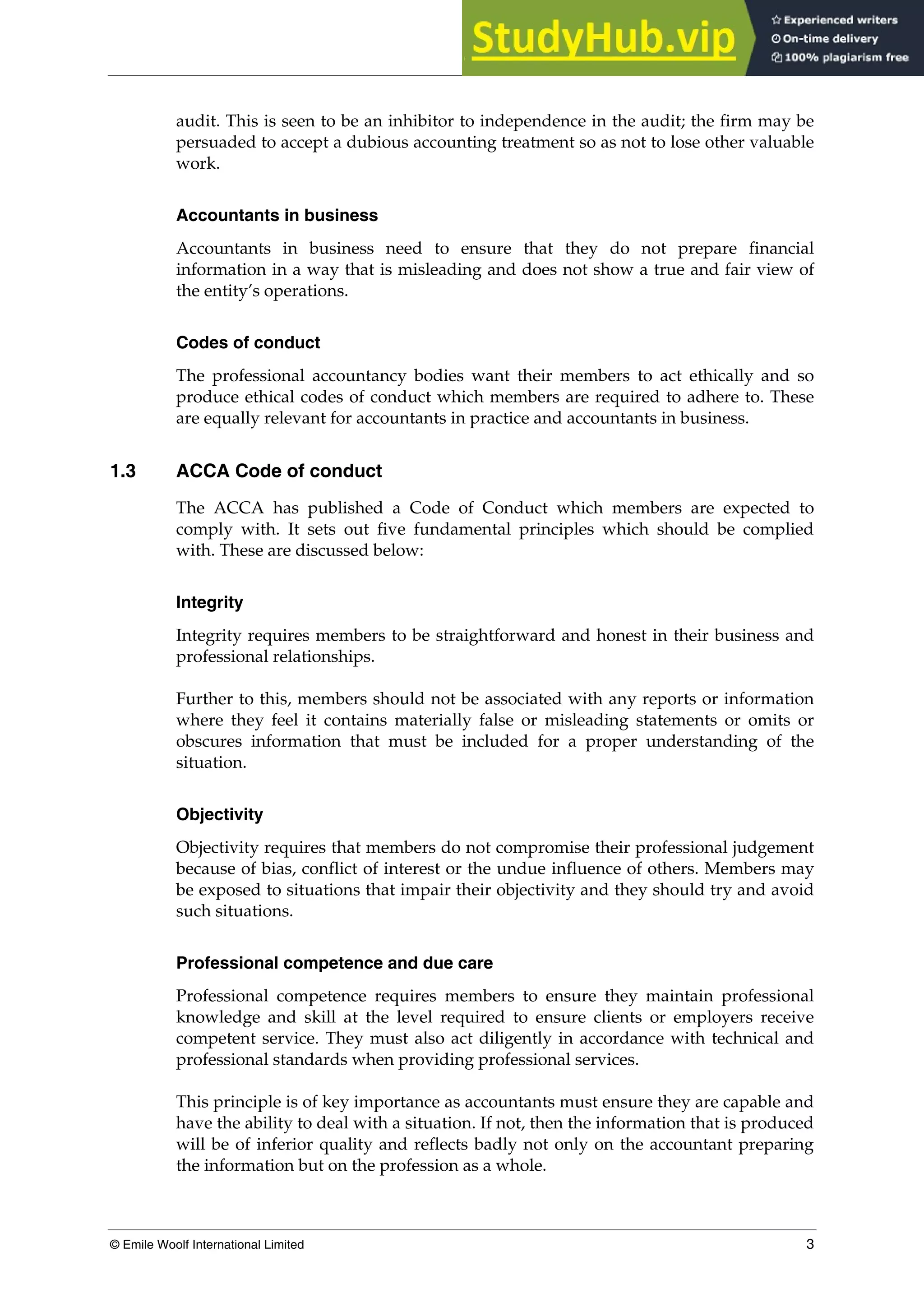

Answer

If a provision is to be made:

there must be a present obligation as a result of a past event

it must be probable that an outflow of economic benefits will be required to

settle the obligation, and

it must be possible to make a reliable estimate of the amount of the obligation.

Applying this to the facts in the example:

(1) Entity G has a legal obligation under the health and safety legislation. The

obligation has arisen from a past event, which is the accident on 15 December

Year 1.

(2) It is probable that Entity G will have to pay the employee. A ‘60% chance of

success’ means that success is ‘more likely than not’. (A probability above 50%

meets the IAS 37 definition of ‘probable’.)

(3) A reliable estimate can be made. This is $60,000.

Conclusion: A provision of $60,000 should be made at 31 December Year 1.

Example

An entity sells high-definition televisions with a 12-month warranty under which

customers are covered for the cost of repairs or replacement of manufacturing

defects found during the period after purchase. If every product sold required

minor repairs, the annual cost would be $0.5 million. If every product was

replaced, the annual cost would be $3 million.

Based on trading history, it is believed that 80% of all goods sold will have no

defects, 15% will have minor defects and 5% will need replacing.

The warranty period covers just 12 months, and a provision should therefore be

created for the expected value of $225,000 [(80% × $0 nil) + (15% × $0.5 million) +

(5% × $3 million)].

Discounting

Where the provision will not be settled for some years and so the effect of the time

value of money is material, the provision should be measured at its present value.

The discount rate used should be the pre-tax market rate that reflects the risks

specific to the liability.

Reimbursements

Where some or all of the costs to settle the provision will be reimbursed by another

party, the reimbursement should only be recognised when it is virtually certain that

the reimbursement will be received.](https://image.slidesharecdn.com/accastrategicbusinessreportingstudytext-230807154039-3fc63967/75/ACCA-Strategic-Business-Reporting-Study-Text-pdf-437-2048.jpg)

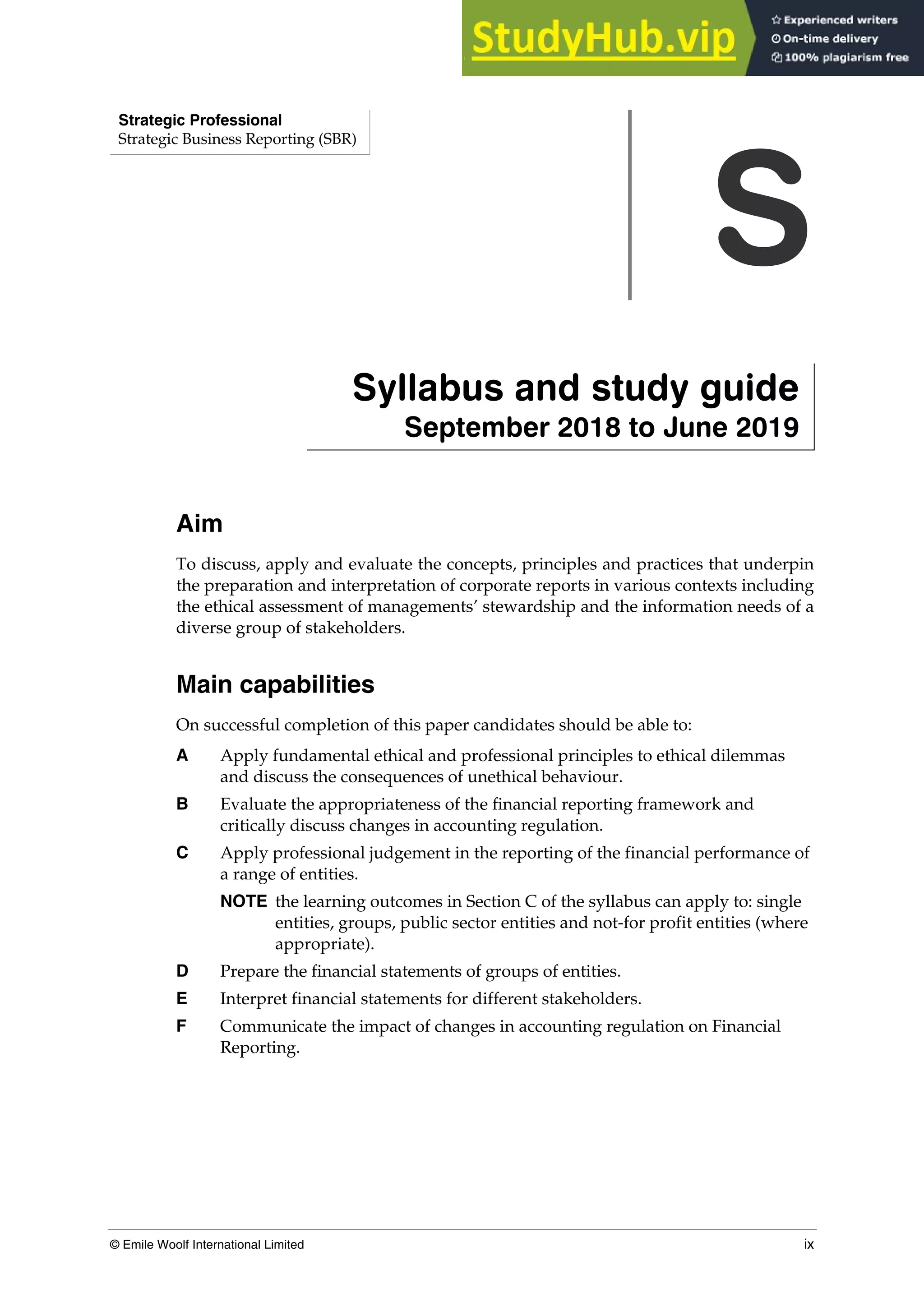

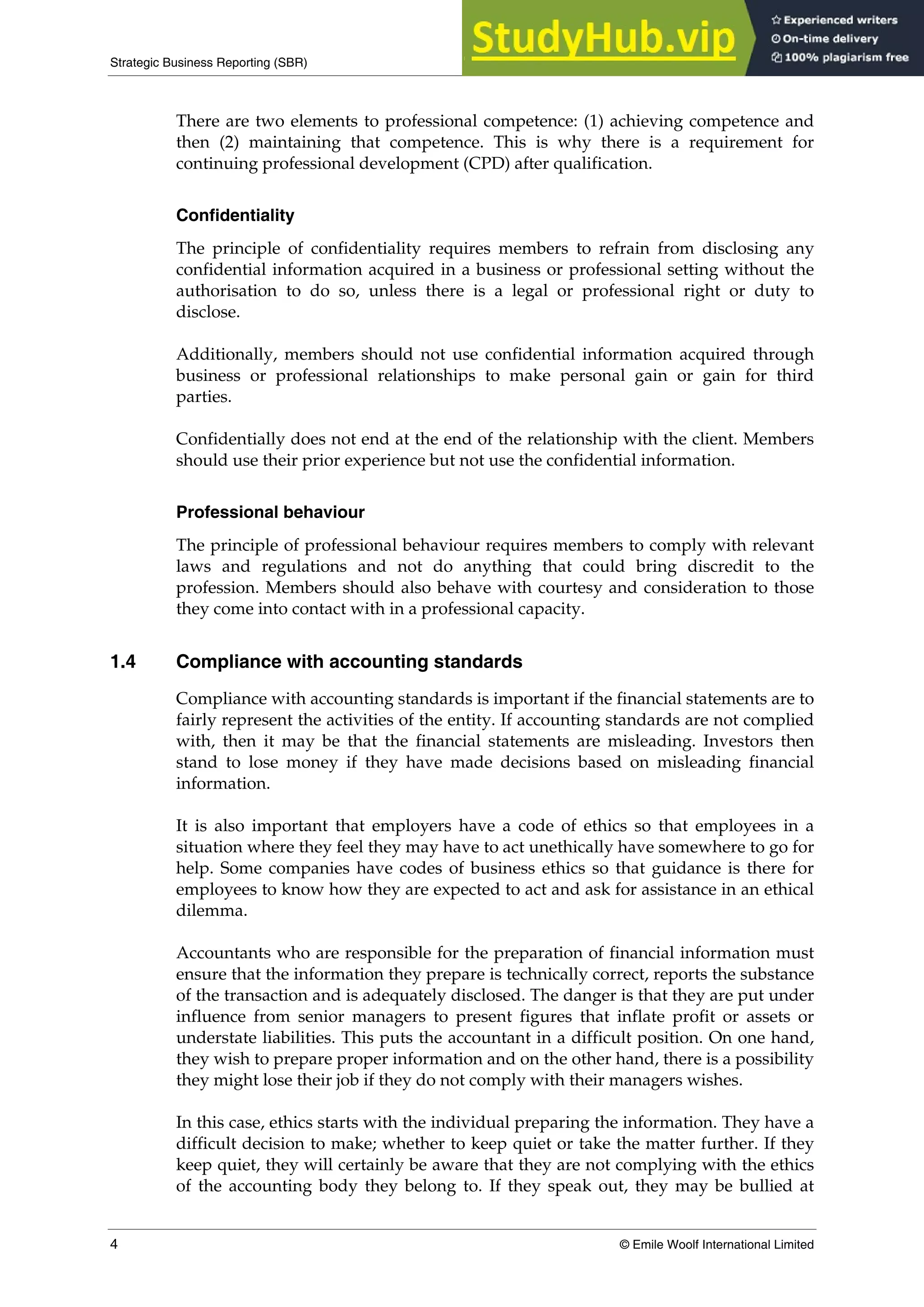

![Strategic Business Reporting (SBR)

514 © Emile Woolf International Limited

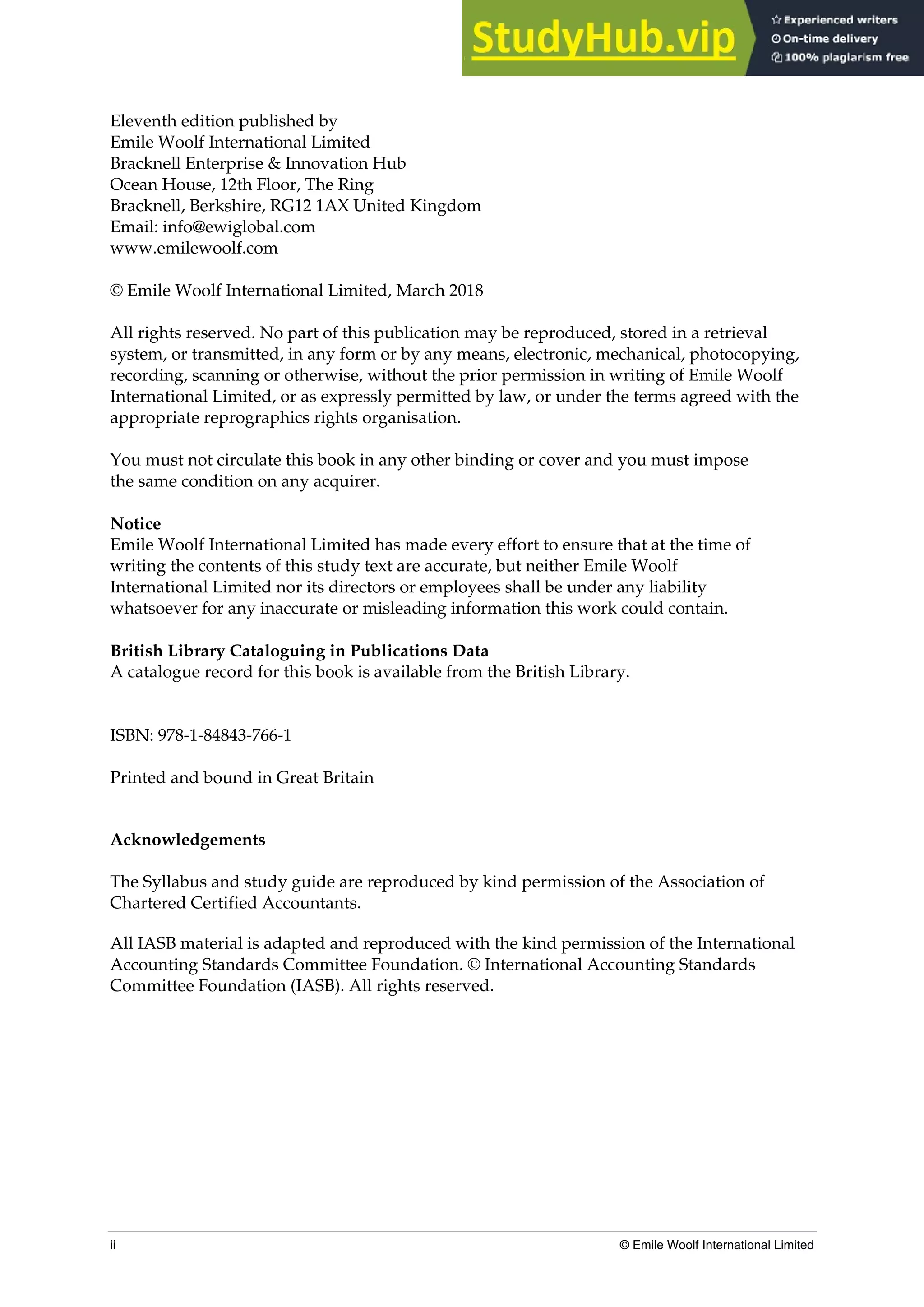

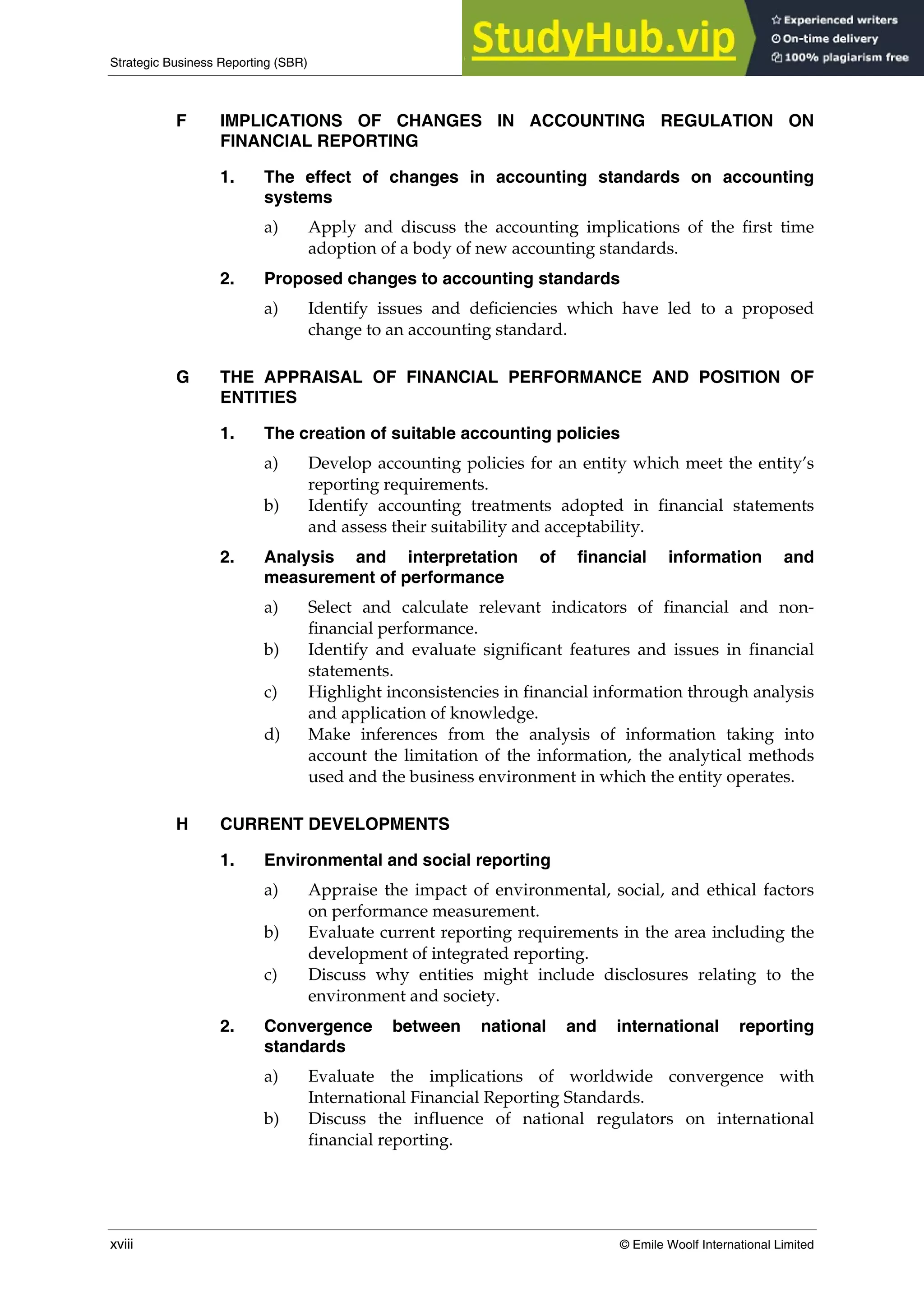

In the year to 31 December Year 6, Entity P sold $200,000 of goods to Entity A, and

the mark-up was 100% on cost. Of these goods, $30,000 were still held as inventory

by Entity A at the year-end.

Required

What is the necessary adjustment for unrealised profit?

Answer

The unrealised profit on this inventory is $30,000 × (100/200) = $15,000.

Entity P’s share of this unrealised profit is (40%) $6,000.

The double entry is:

Dr Cost of sales 6,000

Cr Investment in associate 6,000

The investment in the associate (or JV) at 31 December Year 6 is as follows:

$

Cost of the investment 205,000

Entity P’s share of post-acquisition profits of Entity A

[$90,000 + (40% × $50,000)] 110,000

Minus: Entity P’s share of unrealised profit in inventory (6,000)

–––––––––––––––––––

309,000

–––––––––––––––––––](https://image.slidesharecdn.com/accastrategicbusinessreportingstudytext-230807154039-3fc63967/75/ACCA-Strategic-Business-Reporting-Study-Text-pdf-536-2048.jpg)

This document provides an overview and introduction to the Emile Woolf study text for the ACCA Strategic Business Reporting (SBR) exam. It discusses the following key points: - The study text is written by tutors, is comprehensive yet concise, uses simple English, and is used worldwide by Emile Woolf students. - It provides coverage of the SBR syllabus and exam, which assesses professional competencies in the business reporting environment through an evaluation of concepts, theories, principles and practical situations. - The exam requires the ability to relate professional issues to relevant concepts and practical scenarios, and involves exercising professional and ethical judgement as well as integrating technical knowledge. - The study text