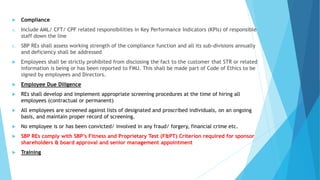

Downloaded 32 times

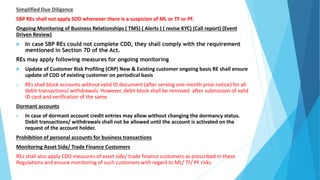

![Detail of Amended Regulations: Regulation – 4

Targeted Financial Sanctions under UNSC Act, 1948 and ATA, 1997

3) SBP REs shall ensure mechanisms, processes and procedures for real-time

screening of customers/ occasional customers, by implementing effective name

screening solution and allocate sufficient trained resources. Unquote]

In this regard you are advised to coordinate with Country Operations to create

tool for screening of Home remittance transactions with Sanctions Lists i.e. UNSC,

OFAC, EU, NACTA and FIA Redbook, and share it with concerns who perform Homer

remittance transactions and instruct them to keep proper record of screen results

alongwith copy of valid ID document with each transaction for audit review.](https://image.slidesharecdn.com/mainpresentationamlcft-211201060711/85/Main-presentation-aml-cft-13-320.jpg)

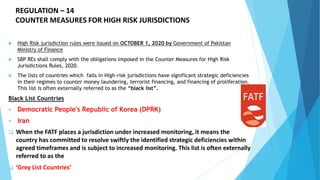

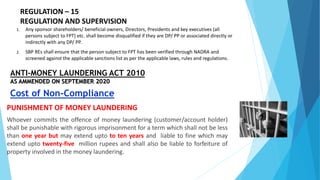

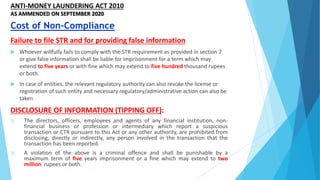

This document outlines regulations for State Bank of Pakistan's regulated entities regarding anti-money laundering, combating the financing of terrorism, and countering proliferation financing. It discusses requirements for a risk-based approach, customer due diligence, enhanced due diligence for high-risk situations, reliance on third parties for customer due diligence, financial sanctions, and politically exposed persons. Key points include applying a risk assessment to policies and procedures, verifying customer identities, monitoring transactions, screening for sanctions lists, and obtaining senior management approval and monitoring high-risk customers like politically exposed persons.