Downloaded 597 times

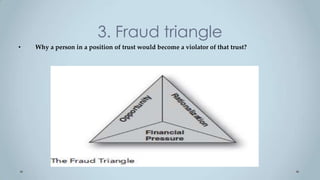

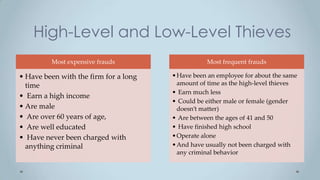

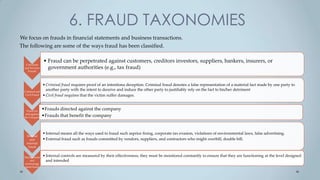

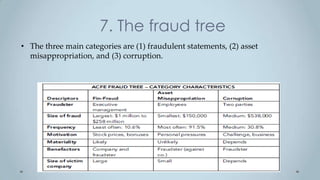

The document discusses various principles of fraud including: 1) Definitions of fraud, corporate fraud, management fraud, and financial statement fraud. 2) The fraud triangle consisting of pressure/motivation, opportunity, and rationalization as the three elements common to every fraud. 3) Characteristics of typical fraudsters including that they are usually someone trusted and not initially suspected, and profiles of high-level and low-level thieves. 4) Taxonomies used to classify fraud including against customers/investors, criminal/civil, for/against the company, and internal/external fraud. 5) The "fraud tree" categorizing fraud into fraudulent statements, asset