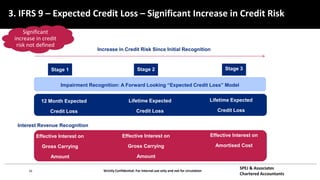

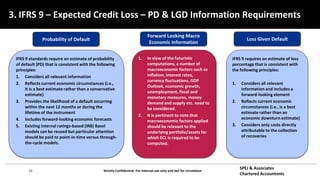

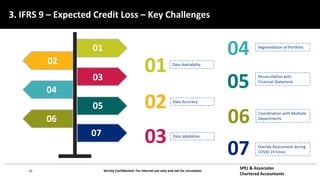

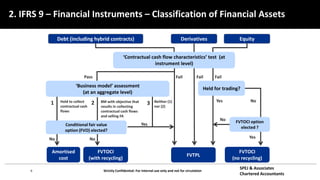

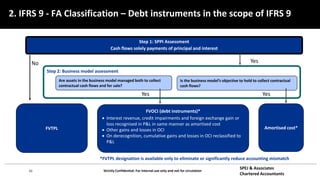

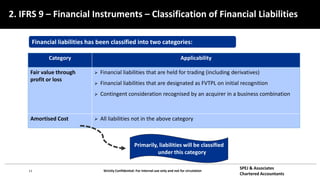

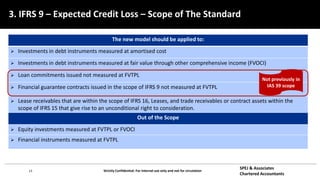

This document discusses IFRS 9 expected credit loss requirements. It provides an overview of topics to be covered, including introduction of IFRS 9 and its impact on UAE banks, classification of financial assets and liabilities, impairment of financial assets using the simplified, general and POCI approaches, examples, and Q&A. The document also analyzes IFRS 9 transition impact on GCC banks and provides guidance on significant credit risk increase, ECL calculation methodology, and information requirements for probability of default and loss given default estimates.

![15 Strictly Confidential: For internal use only and not for circulation

SPEJ & Associates

Chartered Accountants

Is asset being tested a trade receivable, lease

receivable (IFRS 16/IFRS 17) or contract asset

(IFRS 15)?

Policy choice

Calculate the credit loss provision using the 3 stage IFRS 9 model

Analyse credit risk deterioration or improvement since initial recognition

[Stage 1, 2 and 3]

Stage 1:

12 month expected credit loss

Stage 2 and 3:

Lifetime expected credit loss

No

Consider forward looking information

Does the asset have a significant financing

component?

Yes

No

Yes

Lifetime expected credit losses

3 stage IFRS 9 model

Provision matrix

approach

3. IFRS 9 – Impairment model – Decision Tree

Option 1

Option 2](https://image.slidesharecdn.com/1icaidubaiifrs9expectedcreditlossfinal-221107195749-9eaa224f/85/1_icai_dubai_ifrs_9_expected_credit_loss_final-pdf-15-320.jpg)