Downloaded 964 times

The document outlines the importance of a robust anti-money laundering (AML) risk assessment process as a core component of a compliant AML program. It details the cyclical evaluation of AML risks across banks, emphasizes the need for a data-driven approach to identify vulnerabilities, and suggests a structured methodology for executing and improving the risk assessment process. Common challenges faced in AML risk assessments, such as time constraints and data limitations, are discussed alongside potential solutions to enhance effectiveness and scalability.

Overview of AML risk assessment program initiated in August 2016.

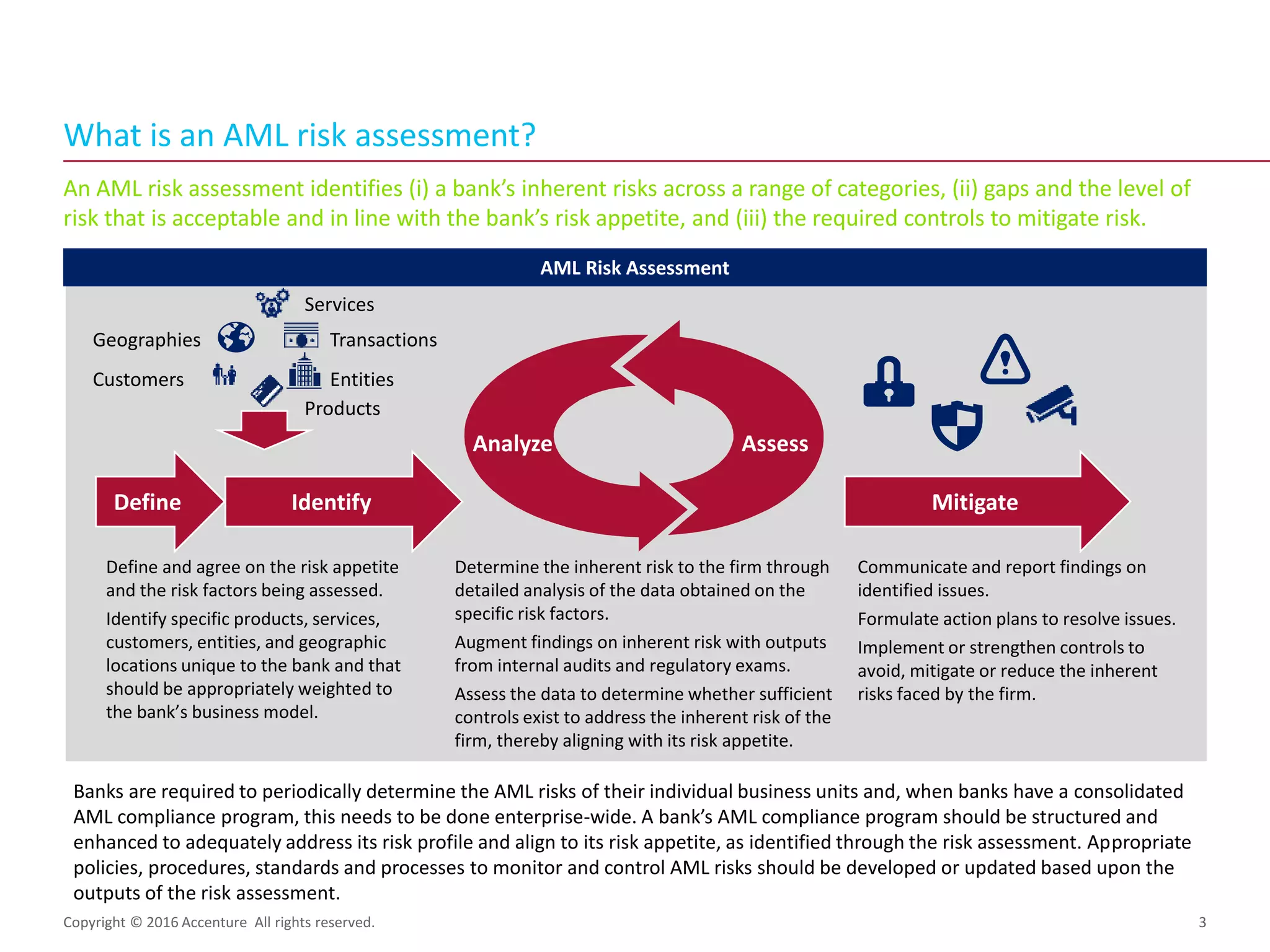

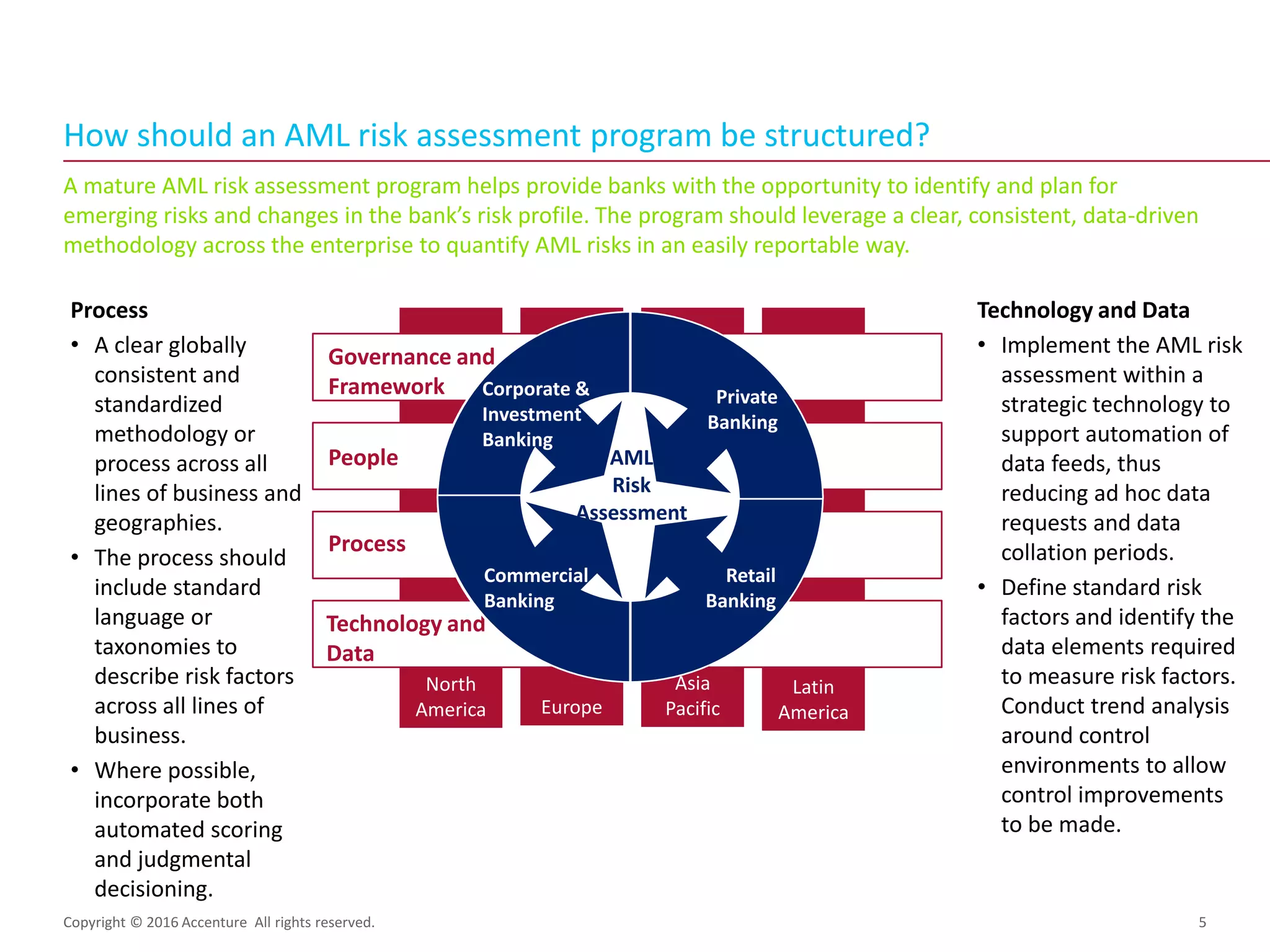

Importance of a robust AML risk assessment process evaluating risks, controls, and regulatory adherence.

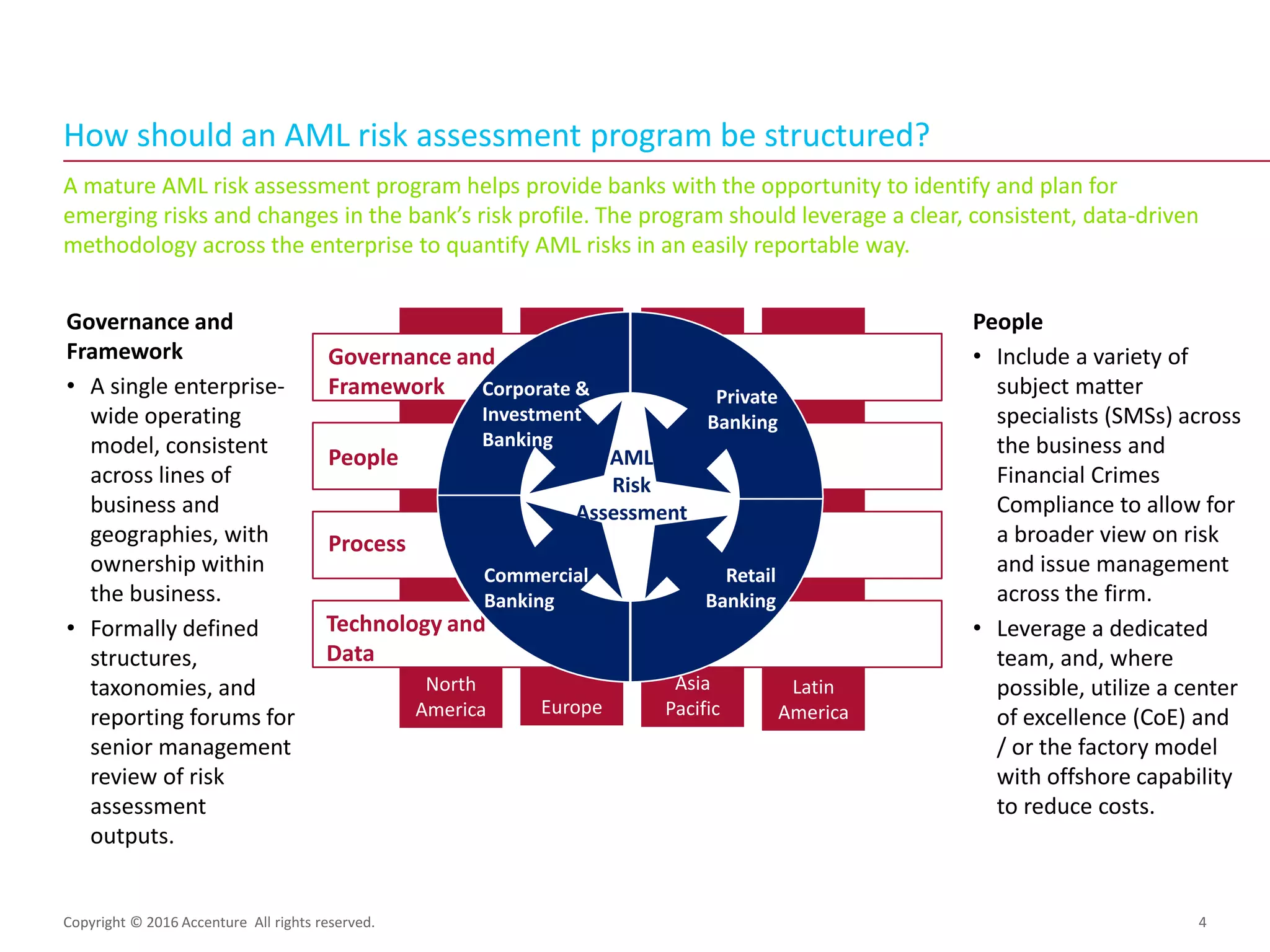

Key components including people, governance, processes, technology, and data for a solid AML framework.

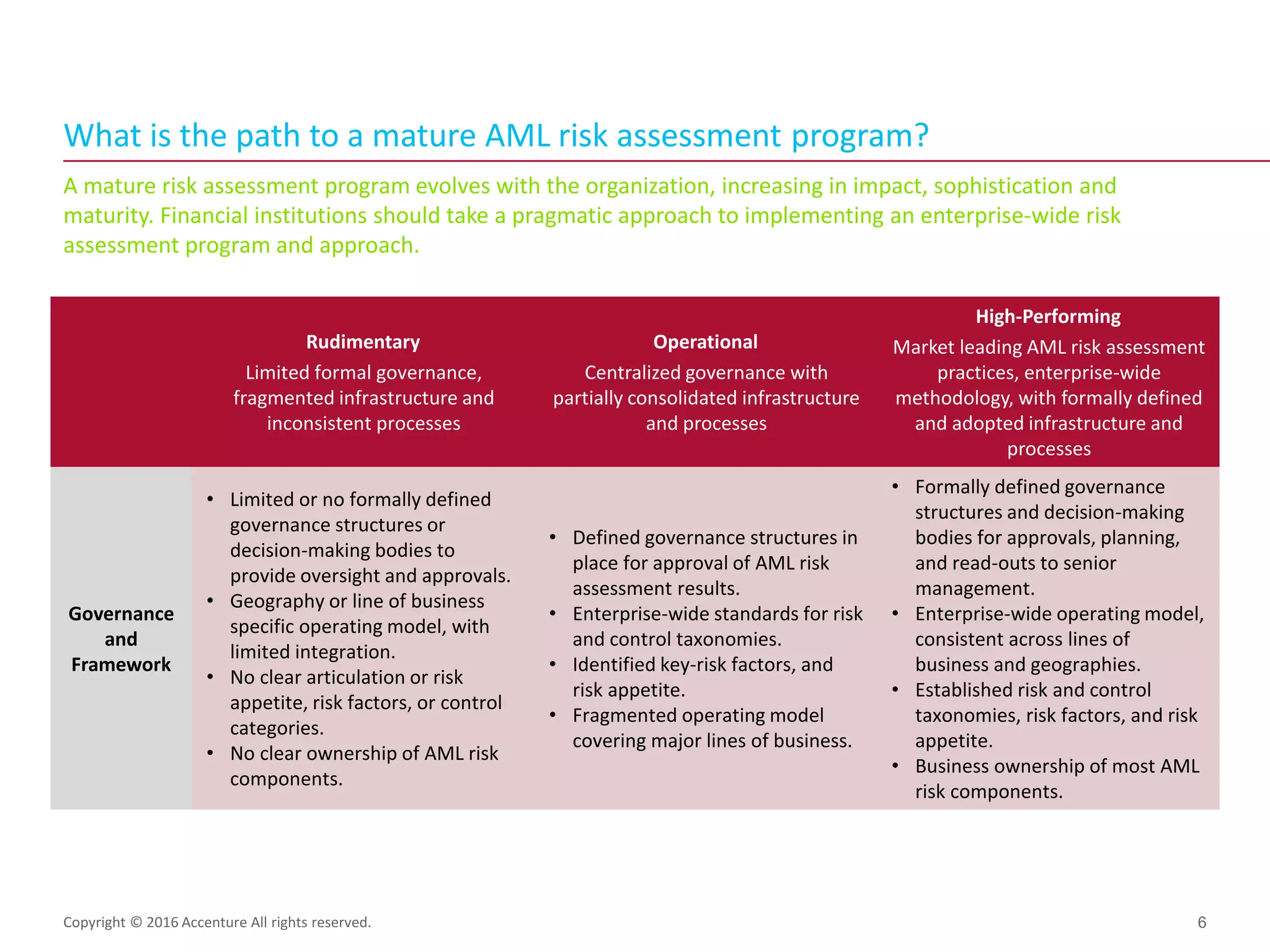

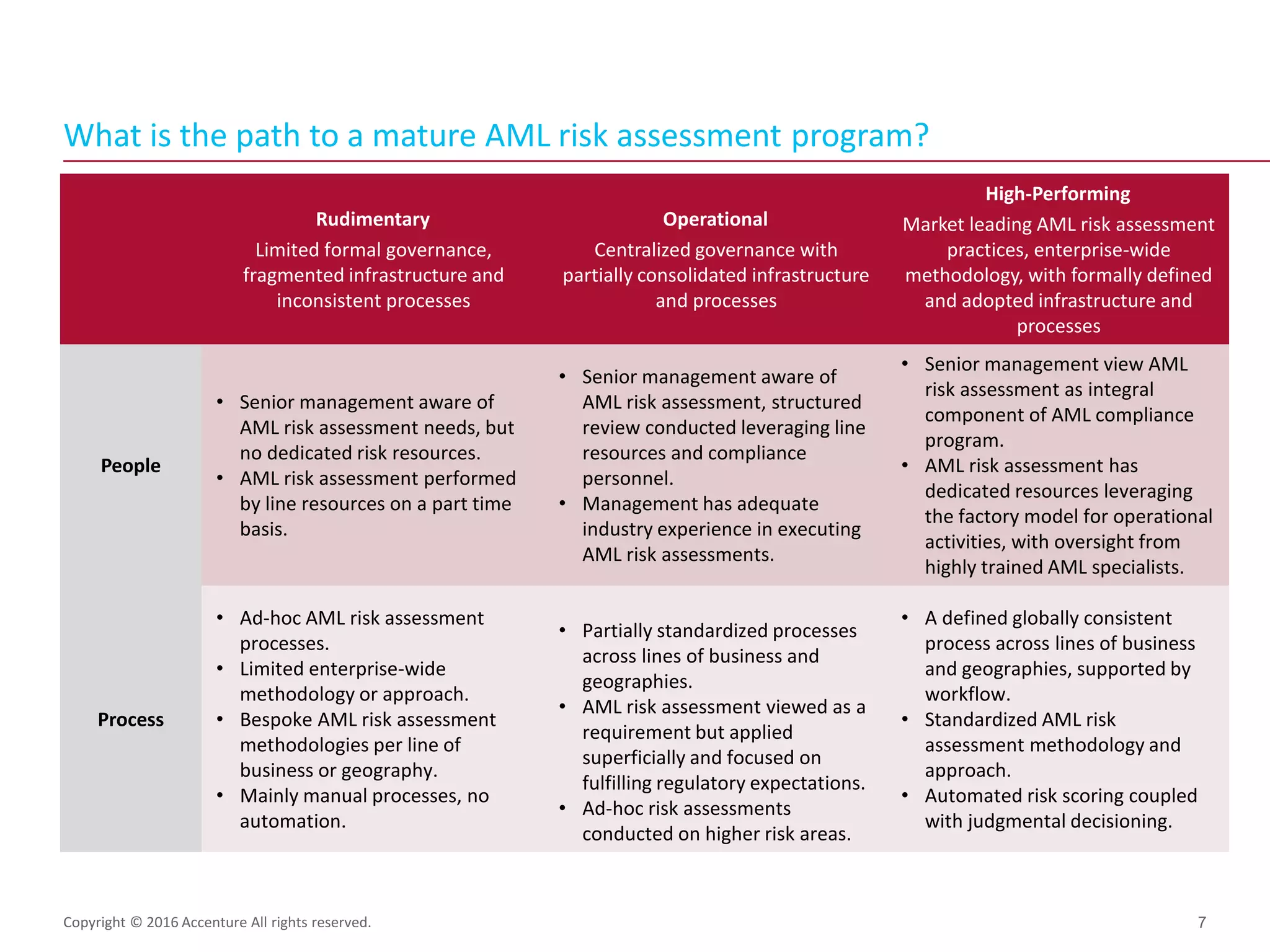

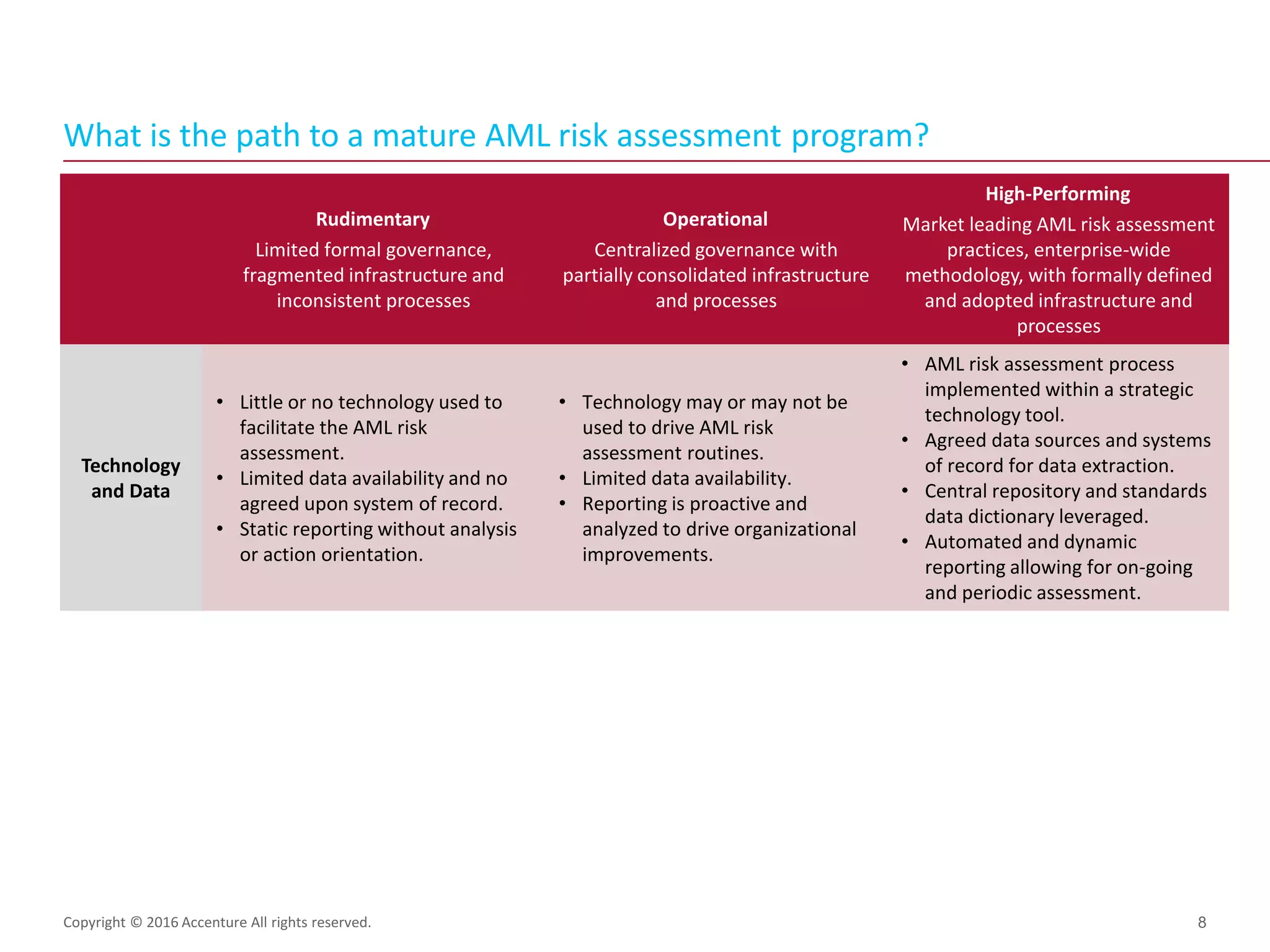

Overview of stages from rudimentary to high-performing AML assessment capabilities and governance.

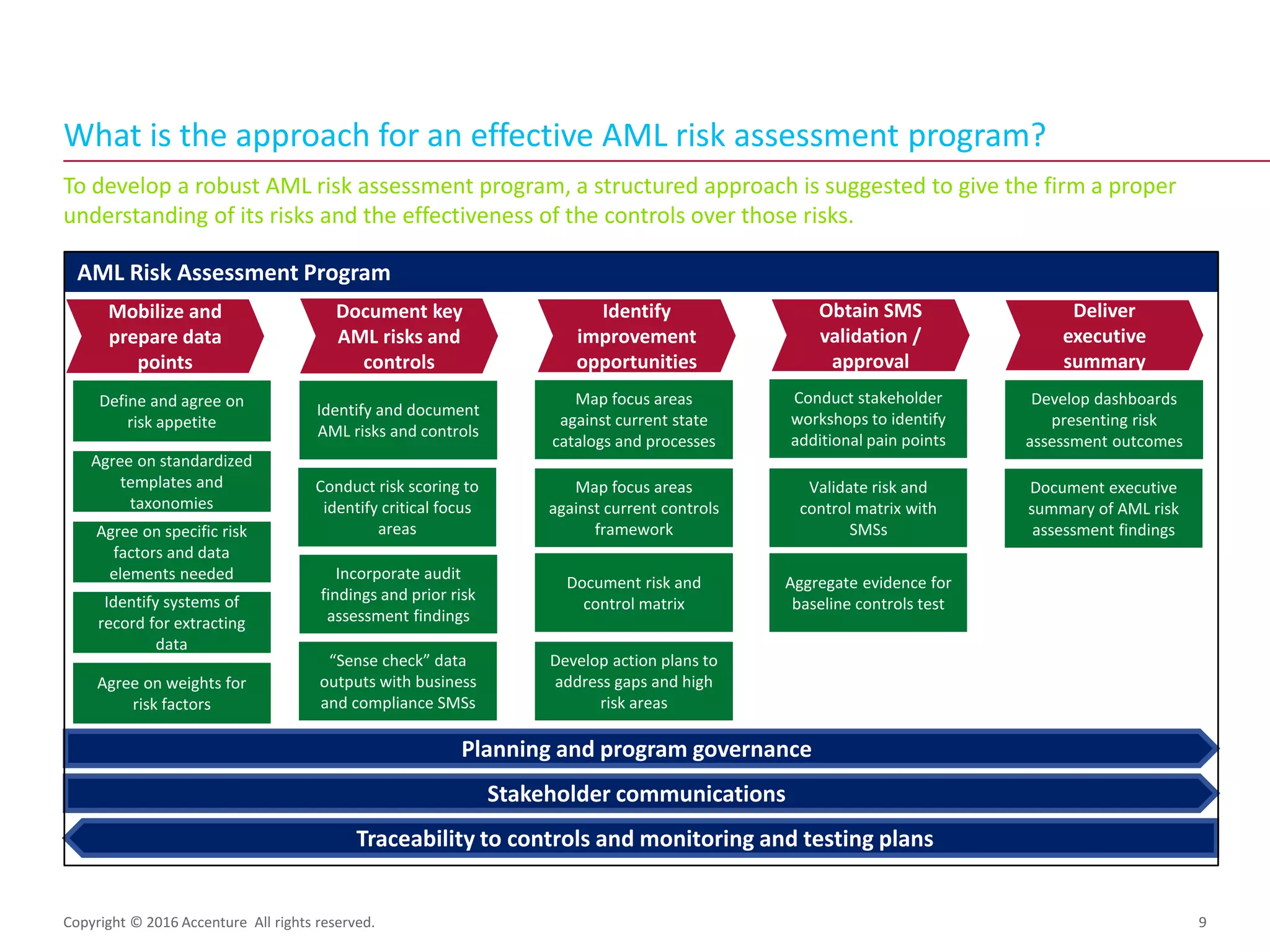

Recommended structured approach for developing and maintaining an effective AML risk assessment.

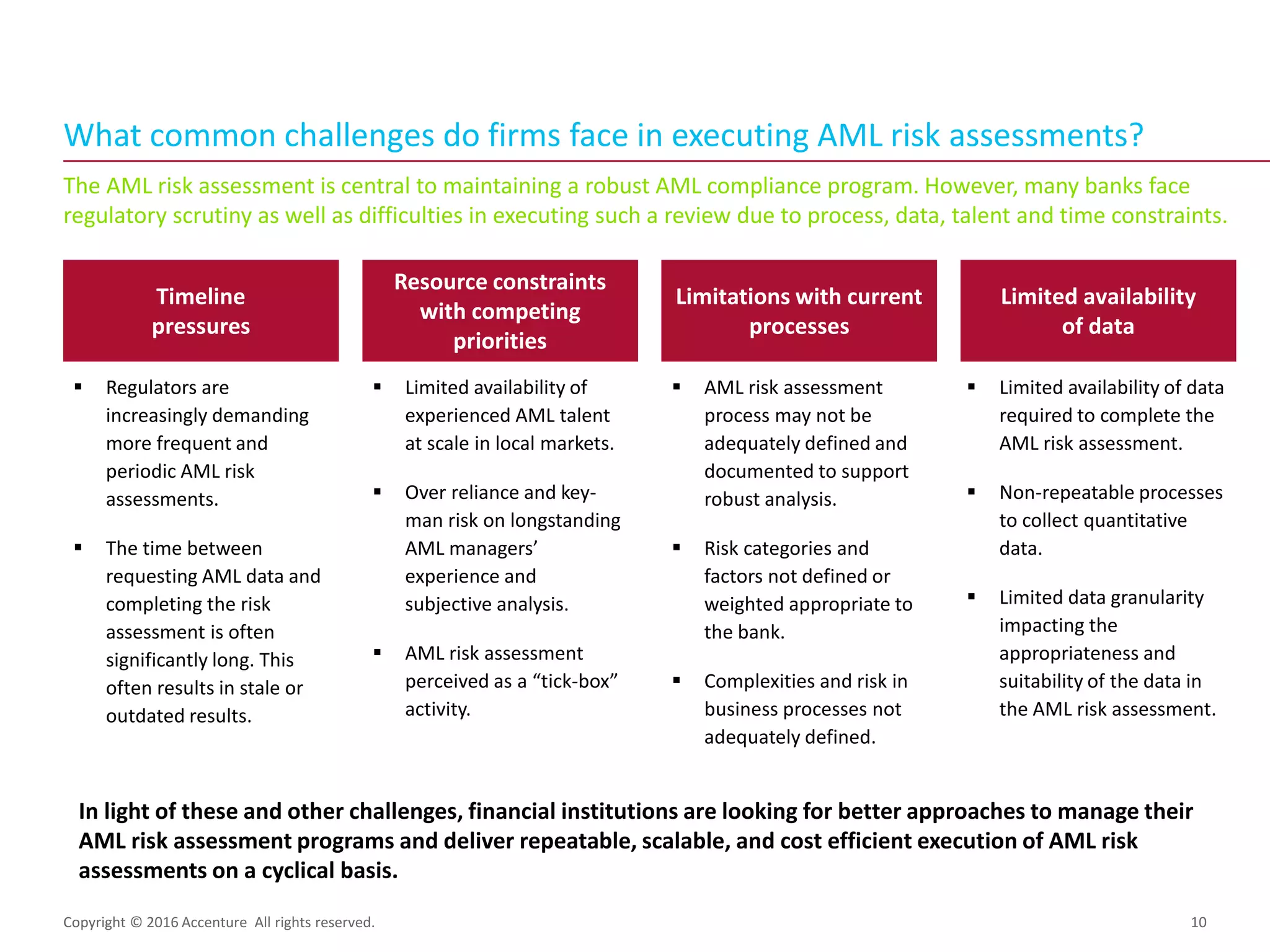

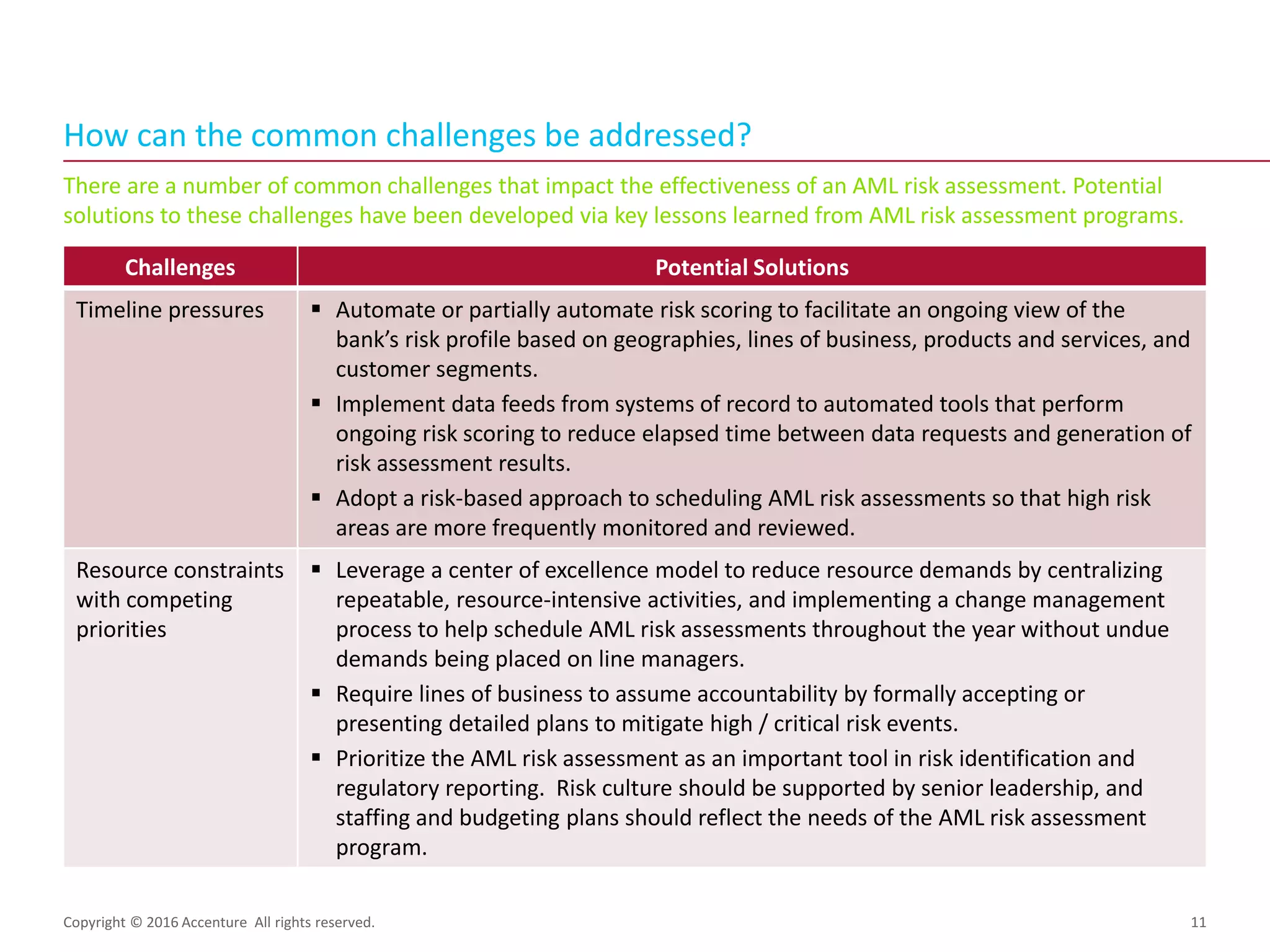

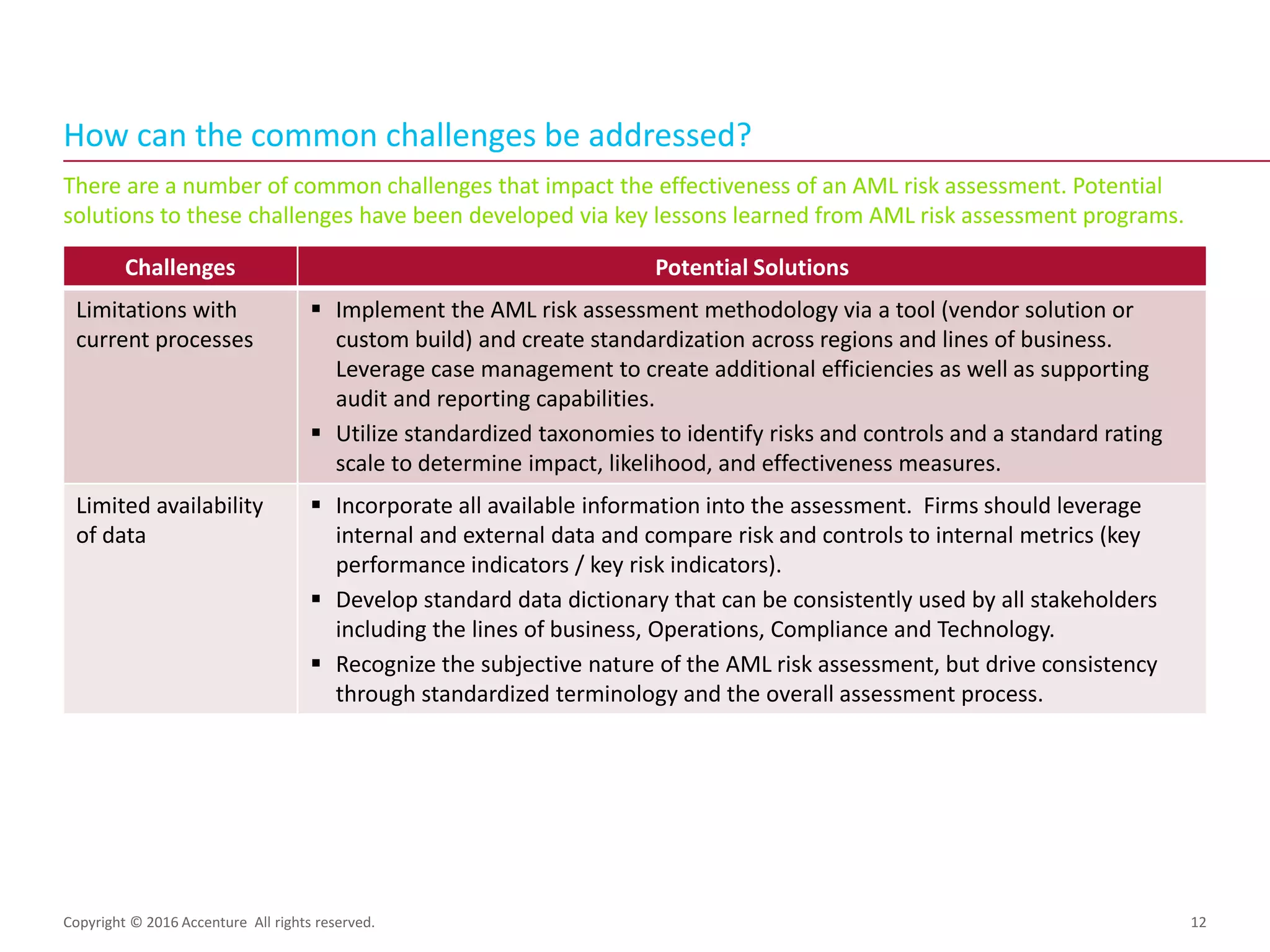

Common issues like timeline pressures and limited data affecting effectiveness, along with proposed solutions.

Links to additional perspectives on AML processes and a disclaimer regarding the presentation.