Downloaded 258 times

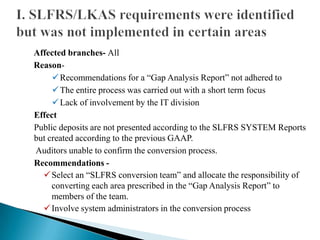

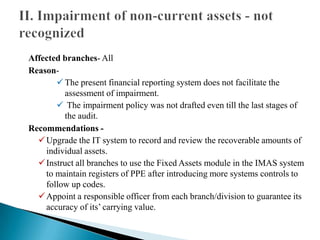

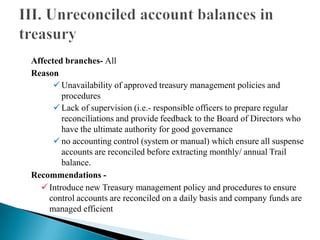

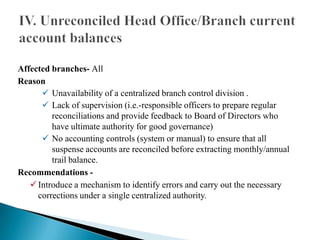

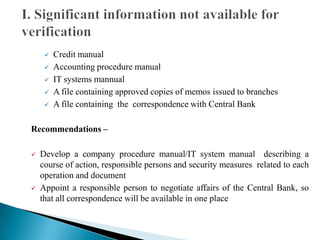

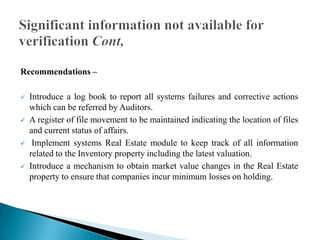

The document summarizes observations from an audit of a company's financial statements. It identifies several risk areas and internal control deficiencies. Key points include: misstatements were identified in all branches due to non-adherence to recommendations and lack of involvement in an SLFRS conversion; impairment was not properly assessed due to insufficient IT systems and policies; treasury management policies and procedures were lacking; and bank reconciliations were either not performed or not reviewed at some branches. Upgrades to IT systems and the development of formal policies and procedures are recommended.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)