Download as PDF, PPTX

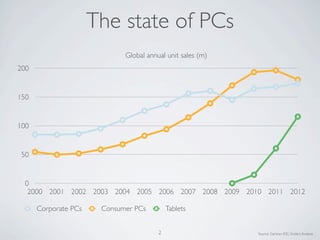

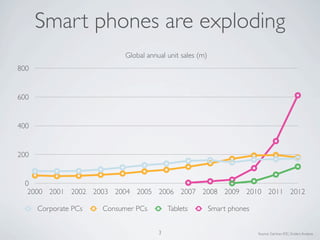

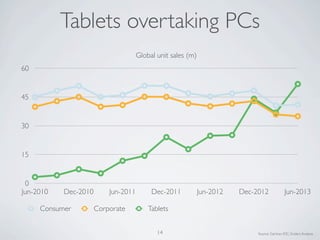

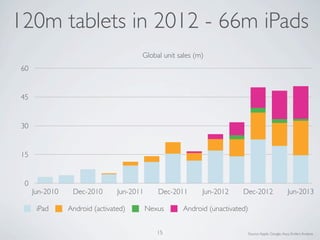

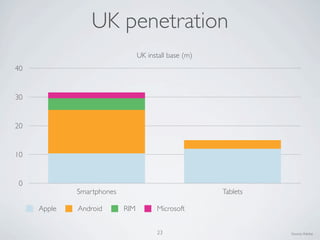

The document discusses the significant shift towards mobile technology, highlighting explosive growth in smartphone and tablet sales compared to PCs. It emphasizes the merging of technology and mobile worlds, the fundamental changes in user behavior, and the dominance of major players like Apple and Samsung. The analysis points to a future where mobile devices drive not just sales but also the integration of various services and experiences in daily life.