Download as PDF, PPTX

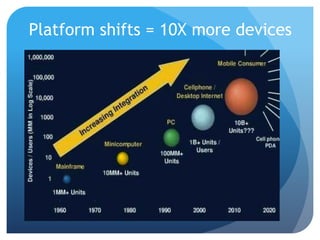

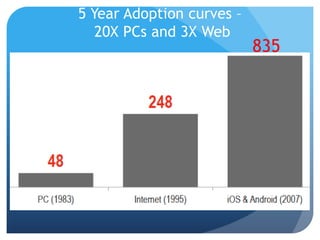

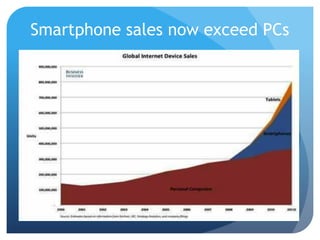

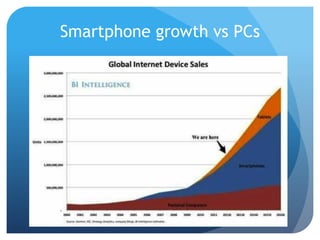

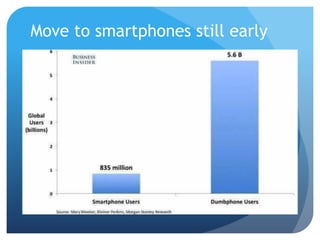

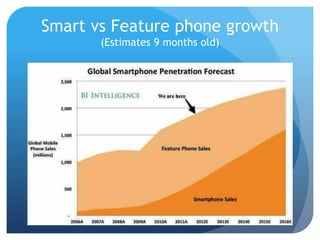

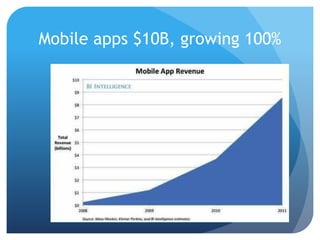

This document discusses how platform shifts happen every 10-15 years and lead to new market leaders. It notes that the smartphone platform shift is already resulting in 10x more devices than PCs and that smartphone sales now exceed PCs. The mobile platform is still in the early stages of growth and represents huge opportunities in areas like mobile apps, games, payments and ecommerce. The document advocates investing in the long term potential of the mobile platform despite challenges in estimating its true size and impact.