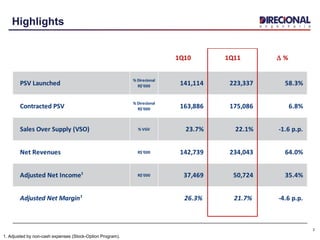

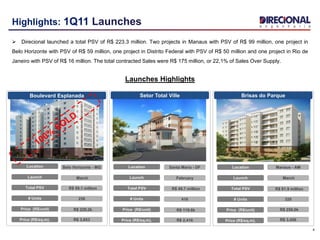

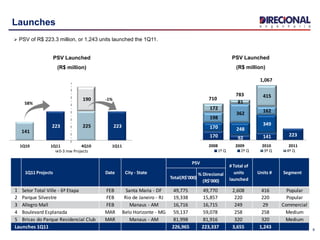

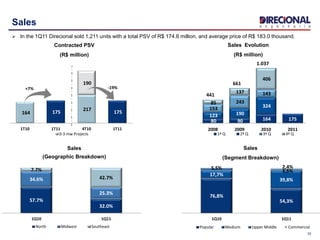

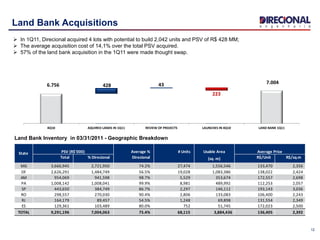

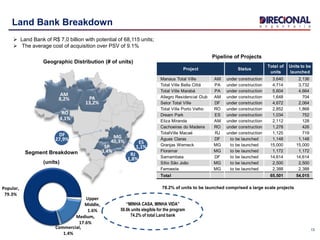

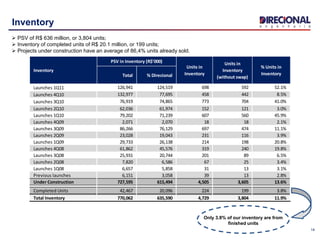

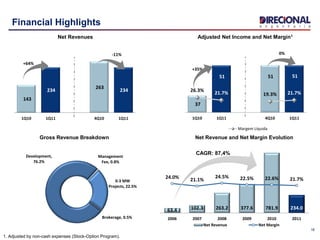

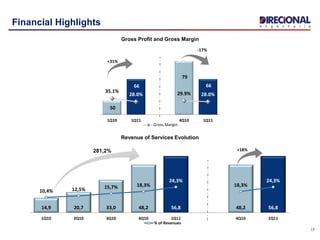

The document summarizes the key highlights from Direcional's 1Q11 earnings release and conference call. It discusses strong operating results with launched PSV of R$223 million, contracted sales of R$175 million, and land bank acquisitions totaling R$428 million. Financially, net revenues increased 64% to R$234 million while adjusted net income grew 35% and margin declined to 21.7% due to higher costs.