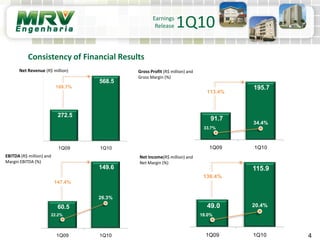

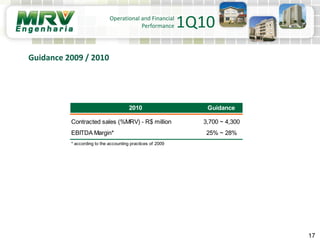

MRV reported strong financial results for the first quarter of 2010. Net revenue increased 108.7% to R$568.5 million while net income rose 147.4% to R$115.9 million. EBITDA also grew 136.4% to R$195.7 million compared to the first quarter of 2009. For 2010, MRV expects contracted sales to be between R$3.7-4.3 billion with an EBITDA margin of 25-28%.