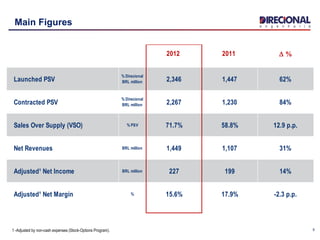

This corporate presentation summarizes the history, business model, and key operating metrics of a real estate development company. Some key points:

- The company has over 30 years of experience developing large-scale, low-income housing projects in Brazil.

- It has a vertically integrated business model focused on industrialized construction techniques to efficiently develop projects at scale.

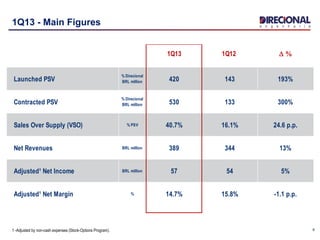

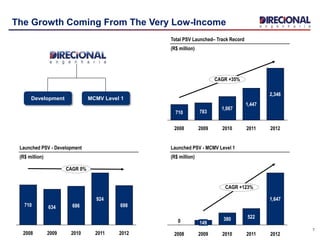

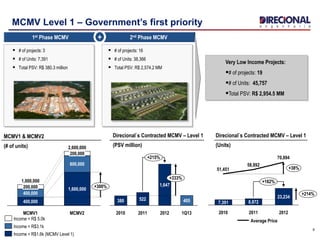

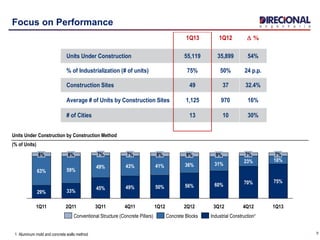

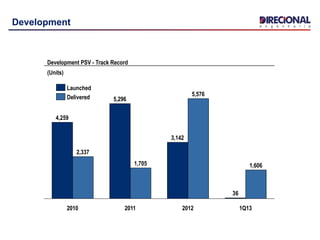

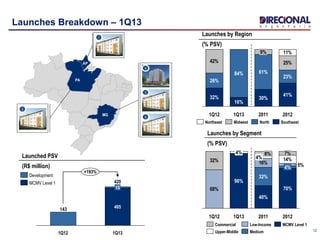

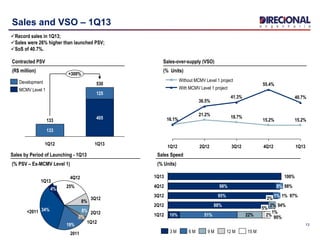

- In 1Q13, the company saw strong growth with launched PSV up 193% year-over-year and contracted PSV up 300% year-over-year. Sales were also up significantly.

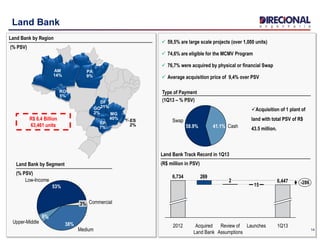

- The land bank as of 1Q13 had a PSV of $6.4 billion and was mostly comprised of large-scale