Understanding the Pakistan Budgeting Process: Basics and Key Insights

Keynote capitals india morning note jun 4-'12

1.

India Morning Note

a g

Mond

day, June 04 2012

4,

Dom

mestic Mark

kets Snapsh

hot Views on markets t

today

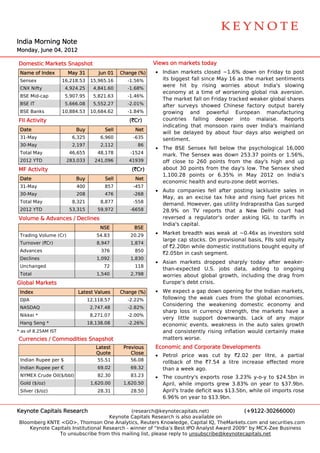

Nam of Index

me May 31 Jun 01 Change (%)

) • India markets closed ~1.

an .6% down on Friday to post

o o

Sensex 16,218.53 15,965.16 -1.56% its biggest fall s

b since May 1 as the market sentim

16 ments

were hit by rising worr

e ries about India's slowing

CNX Nifty

X 4,924.25 4,841.60 -1.68%

econnomy at a t time of wor

rsening glob risk ave

bal ersion.

BSE Mid-cap 5,907.95 5,821.63 -1.46%

The market fall on Friday trracked weaker global s

shares

BSE IT 5,666.08 5,552.27 -2.01% after surveys s

r showed Chiinese factory output bbarely

BSE Banks 10,884.53 10,684.62 -1.84% growwing and powerful European manufacturing

FII A

Activity (`Cr) counntries falling deeper into malaise. Re

m eports

indic

cating that monsoon rains over India's mai inland

Date

e Buy Sell Net

will be delayed by about four days also weighe on

d ed

31-M

May 6,325 6,960 -635 senttiment.

30-M

May 2,197 2,112 86

• The BSE Sense fell below the psyc

ex w chological 1

16,000

Tota May

al 46,655 48,178 -1524 mark. The Sens sex was dow 253.37 points or 1

wn 1.56%,

2012 YTD 283,033 241,096 41939 off close to 26 points fr

c 60 rom the da ay's high an up

nd

MF A

Activity (`Cr) abou 30 points from the day's low. The Sensex shed

ut s T x

1,10

00.28 points or 6.35% in May 2012 on India’s

%

Date

e Buy Sell Net

econnomic health and euro-

-zone debt worries.

w

31-M

May 400 857 -457

• Auto companies fell after posting lacklustre sales in

o

30-M

May 208 476 -268

May, as an exc cise tax hik and risin fuel prices hit

ke ng

Tota May

al 8,321 8,877 -558

mand. Howev

dem ver, gas util

lity Indrapra

astha Gas surged

2012 YTD 53,315 59,972 -6658 28.9

9% on TV reports tha a New Delhi court had

at

Volu

ume & Adva

ances / Dec

clines reve

ersed a reg gulator's ord

der asking IGL to tariffs in

India capital.

a's

NSE BSE

Trad

ding Volume (Cr) 54.83 20.29 • Mark breadth was weak at ~0.46x as investors sold

ket

large cap stock On provisional basis FIIs sold e

e ks. s, equity

Turn

nover (`Cr) 8,947 1,874

of `2

2.20bn while domestic institutions bought equ

e uity of

Advances 376 850

`2.05bn in cash segment.

h

Declines 1,092 1,830

• Asian markets dropped sharply toda after we

ay eaker-

Unchanged 72 118

n-expected U.S. jobs data, add

than ding to on

ngoing

Tota

al 1,540 2,798 worrries about g

global grow

wth, includin the drag from

ng g

Glob Markets

bal Euro

ope’s debt c

crisis.

Inde

ex Late Values

est Change (%)

) • We expect a gap down ope

e ening for the Indian ma

e arkets,

DJIA

A 12,118.57 -2.22% following the wweak cues f from the global econo omies.

Cons sidering the weakenin domesti economy and

ng ic y

NAS

SDAQ 2,747.48 -2.82%

shar loss in c

rp currency str

rength, the markets have a

Nikk *

kei 8,271.07 -2.00%

very little support downw

y wards. Lack of any major

Hang Seng * 18,138.08 -2.26% econnomic events, weaknes in the auto sales g

ss growth

* as o 8.25AM IST

of and consistently rising inflation would certainly make

d

Curr

rencies / Co

ommodities Snapshot

s matt ters worse.

Latest Previous Econom and Cor

mic rporate Dev

velopments

s

Quote Close • Petro price was cut by `2.02 per litre, a p

ol r partial

Indian Rupee per $ 55.51 56.08 rollb

back of the `7.54 a litre increas effected more

se

Indian Rupee per € 69.02 69.32 than a week ago.

n

NYM

MEX Crude Oil($/bbl) 82.30 83.23 • The country's e exports rose 3.23% y-o to $24.5

e o-y 5bn in

Gold ($/oz)

d 1,620.00 1,620.50 April, while impports grew 3.83% on year to $37

y 7.9bn.

Silve ($/oz)

er 28.31 28.50 April's trade def

ficit was $13.5bn, while oil imports rose

e s

6.96 on year t $13.9bn.

6% to

Keyn

note Capitals Research

h (reseaarch@keyno otecapitals.net) (+91222-3026600 00)

Keyynote Capita Research is also available on

als h

Bloo

omberg KNTE <GO>, Tho

E omson One A Analytics, Re

euters Knowwledge, Capit IQ, TheMa

tal arkets.com and securitie

a es.com

Keynote Capitals Institu

utional Resea

arch - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

To unsubsc cribe from th mailing lis please reply to unsub

his st, bscribe@keyynotecapitals

s.net

2.

TOP GAINERS Buzzin Stocks

ng

(BSE A-Group)

E • Reliance Industtries agreed to sign ag

d greements with

Previous Currennt Change gati Power Corp and N

Prag NTPC for su

upply of nat

tural

Com

mpany Name

e

Close(`

`) Price(`

`) (%) gas from its eas

stern offsho KG-D6 fields.

ore

Indr

raprastha Gas

s 193.75

5 249.35 28.70

• Bharati Shipyard has agreeed to infus `118Cr f

se fresh

Neyveli Lignite 74.25

5 85.25 14.81

capital into the debt- -laden commpany, as a s

Guja

arat Gas 291.00

0 333.55 14.62 prec

condition fo its `5,800 debt res

or 0Cr structuring p

plan,

Guja

arat State Pet

t 63.40

0 70.50 11.20 sour

rces said.

Petr

ronet LNG 127.90

0 139.40 8.99

• Jindal Stainless approached lenders to resche

s edule

(BSE Mid-Cap)

E repaayments of its over `9,0

000Cr debt.

.

Previous Currennt Change • NMDDC, which is setting up a 3 MTPA steel plan in

A nt

Com

mpany Name

e

Close(`

`) Price(`

`) (%) Chhattisgarh, h

hopes to sta producin coal from its

art ng m

Indr

raprastha Gas

s 193.75 249.35 28.70 capt

tive mine by 2014 4, coinciding with the

Guja

arat Gas 291.00 333.55 14.62 com

mmissioning of facility fo the alloy.

or

Guja

arat State Pet

t 63.40 70.50 11.20

• Maruti Suzuki will invest `4,000Cr to set up a new

o

Amt

tek Auto-$ 100.15 106.75 6.59 mannufacturing facility in Gujarat, raising its total

r

Info Edge India 714.80 739.00 3.39 capa

acity to two million units by 2015-16.

o

• Pow

werGrid Corp poration has firmed up plans to sp

s pend

TOP LOSERS

`10,,000Cr in the next thr ree financia years on the

al

(BSE A-Group)

E sett

ting up of in ransmission lines. For this,

ntra-state tr n

Previous Currennt Change Pow

wrGrid has initiated t talks with Bihar, Odi isha.

Com

mpany Name

e

Close(`

`) Price(`

`) (%) Jhar

rkhand, Chhattisgarh, Manipur, Uttar Prad desh,

Adani Enter 261.30

0 239.90

0 -8.19 Maddhya Prades Tamil Na

sh, adu and Karnataka.

Pant

taloon Retl 150.60

0 138.85

5 -7.80 US markets

JSW ENERGY 45.00

0 42.05

5 -6.56

US markets fell mmore than 2% Friday, turning the Dow

Asia Paints

an 4034.65

5 3777.15

5 -6.38

rials negativ for the y

Industr ve year and pushing the S&P

Apollo Tyres 86.50

0 81.20

0 -6.13

500 into correc ction territtory, after weaker-t

r than-

(BSE Mid-Cap)

E expectted U.S. jobs report in M

s May.

Previous Currennt Change The Do Jones Ind

ow dustrial Ave

erage fell 2774.88 points, or

Com

mpany Name

e

Close(`

`) Price(`

`) (%) 2.2%, to 12,118.5 The S&P 500 Index dropped 32.29

t 57. P x

Fres

senius Kabi 108.10 89.60 -17.11 points, or 2.5%, to 1,278.04 The Nas

4. sdaq Compo osite

Pant

taloon Retl 150.60 138.85 -7.80 Index declined 79.86 points, o 2.8%, to 2,747.48.

d or

Arvind 77.40 71.70 -7.36

INDI

IAB POWER 12.97 12.07 -6.94

Apollo Tyres 86.50 81.20 -6.13

Keyn

note Capitals Research

h (resea

arch@keyno

otecapitals.net) (+912

22-3026600

00)

3.

India and Globa Economic Calendar

a al c

Countries / Mon

nday Tuesday Wed

dnesday Thursday

Reg

gions 4-

-Jun 5-Jun

5 6-Jun 7-Jun

Ind

dia

US Factory Orders ISM Non-Mfg Index Consum Credit

mer

Change

e

ICSC-Gold

dman Store Fed's Bernanke

Sales s

testifies

Glo

obal UK House prices Germanyy's Euro zon ECB

ne UK's Purchasing

data Purchasin Manager

ng r interest rate Manage Index

er

Index Ser

rvices decision & press Services

conferennce

Germany IIP

y UK's Bo Interest

oE

Rate De

ecision

Japan's Leading

Econom Index

mic

KEYN

NOTE CAPITTALS LTD.

The Rub 9th Floo Senapati Bapat Marg, Dadar (W), Mumba – 400 028

by, or, ai 8

Tel. : +9

9122-30266

6000 • www

w.keynotec

capitals.com

m

Disclaiimer: This re

eport is purely for informa ation purpose and is bassed on public information News cont

c n. tent is attribu

utable to

various media, unle specified otherwise. A market related statistic data perta

ess All cal ains to the im

mmediately preceding trad ding day,

unless stated other

s rwise. Neithe the informa

er ation nor any opinion expressed in this report constitutes an off

y s fer, or an invitation to

make an offer, to bbuy or sell the securities m

mentioned he erein. We or any of our directors, offic

cers or emplo

oyees shall not in any

way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgmen before

e e s m e o nt

acting on the conteents of this re

eport. The rep

port has not been edited due to time c

d constraints.