India Morning Note markets fell on weak GDP data

•

0 likes•78 views

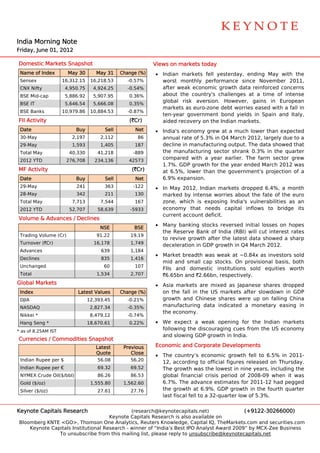

- Indian markets fell on May 31, ending May with their worst monthly performance since November 2011, after weak economic growth data reinforced concerns about the country's challenges at a time of intense global risk aversion. - India's economy grew at a much lower than expected annual rate of 5.3% in Q4 March 2012, largely due to a decline in manufacturing output. - Many banking stocks recovered initial losses on hopes the Reserve Bank of India will cut interest rates to revive growth after the latest data showed a sharp deceleration in GDP growth in Q4 March 2012.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (17)

Similar to India Morning Note markets fell on weak GDP data

Similar to India Morning Note markets fell on weak GDP data (18)

More from Keynote Capitals Ltd.

More from Keynote Capitals Ltd. (20)

Recently uploaded

Recently uploaded (20)

India Morning Note markets fell on weak GDP data

- 1. India Morning Note a g Frida June 01, 2012 ay, Dom mestic Mark kets Snapsh hot Views on markets t today Nam of Index me May 30 May 31 Change (%) ) • India markets fell yesterday, endin May wit the an s ng th Sensex 16,312.15 16,218.53 -0.57% wors monthly performan st nce since November 2011, N CNX Nifty X 4,950.75 4,924.25 -0.54% after weak econ r nomic grow data rein wth nforced conncerns BSE Mid-cap 5,886.92 5,907.95 0.36% abou the coun ut ntry's challe enges at a time of inntense glob bal risk aversion. However, gains in Euro opean BSE IT 5,646.54 5,666.08 0.35% markets as euroo-zone debt worries ea t ased with a fall in BSE Banks 10,979.86 10,884.53 -0.87% year govern ten-y nment bond yields in Spain and Italy, d FII A Activity (`Cr) aided recovery on the India markets. an Date e Buy Sell Net • India economy grew at a much lowe than exp a's y er pected 30-M May 2,197 2,112 86 annu rate of 5 ual 5.3% in Q4 MMarch 2012, largely due to a 29-M May 1,593 1,405 187 decline in manu ufacturing output. The data showed that d Tota May al 40,330 41,218 -889 the manufacturring sector shrank 0.3% in the qu uarter 2012 YTD 276,708 234,136 42573 compared with a year earlier. The farm sector grew 1.7% GDP grow for the y %. wth year ended March 2012 was MF A Activity (`Cr) at 6.5%, lower than the government' projection of a 's n Date e Buy Sell Net 6.9% expansion % n. 29-M May 241 363 -122 • In May 2012, In M ndian markets dropped 6.4%, a m d month 28-M May 342 211 130 marked by inte ense worries about the fate of the euro s e Tota May al 7,713 7,544 167 zone which is exposing I e, India's vuln nerabilities as an 2012 YTD 52,707 58,639 -5933 econ nomy that needs cap pital inflow to bridg its ws ge curre account deficit. ent t Volu ume & Adva ances / Dec clines • Many banking s ersed initial losses on hopes stocks reve NSE BSE the Reserve Ba ank of India (RBI) will cut interest rates c Trad ding Volume (Cr) 91.22 19.19 evive growt after the latest data showed a sharp to re th a Turn nover (`Cr) 16,178 1,749 deceeleration in GDP growth in Q4 Marc 2012. h ch Advances 639 1,184 • Mark breadth was weak at ~0.84x as investors sold ket Declines 835 1,416 mid and small cap stocks. On provis sional basis, both , Unchanged 60 107 FIIs and dome estic institu utions sold equities worth Tota al 1,534 2,707 `6.65bn and `2.66bn, respeectively. Glob Markets bal • Asia markets are mixed a Japanese shares dro as e opped Inde ex Late Values est Change (%) ) on the fall in the US mark t kets after slowdown in GDP s n DJIA A 12,393.45 -0.21% grow wth and Chinese share were up on falling China es NAS SDAQ 2,827.34 -0.35% mannufacturing data indica ated a mon netary easi ing in the economy. e Nikk * kei 8,479.12 -0.74% Hang Seng * 18,670.61 0.22% • We expect a w weak opening for the Indian ma e arkets * as o 8.25AM IST of following the di iscouraging cues from the US eco onomy and slowing GD growth in India. DP Curr rencies / Co ommodities Snapshot s Latest Previous Econom and Cor mic rporate Dev velopments s Quote Close • The country’s e economic growth fell to 6.5% in 2011- t Indian Rupee per $ 56.08 56.20 12, according to official fig a gures releas sed on Thur rsday. Indian Rupee per € 69.32 69.52 The growth was the lowest in nine yea s t ars, includin the ng NYM MEX Crude Oil($/bbl) 86.26 86.53 glob financial crisis perio of 2008 bal od 8-09 when i was it Gold ($/oz) d 1,555.80 1,562.60 6.7% The adva %. ance estimates for 2011-12 had pe egged Silve ($/oz) er 27.61 27.76 the growth at 6 6.9%. GDP ggrowth in th fourth qu he uarter last fiscal fell to a 32-quart low of 5.3%. o ter Keyn note Capitals Research h (reseaarch@keyno otecapitals.net) (+91222-3026600 00) Keyynote Capita Research is also available on als h Bloo omberg KNTE <GO>, Tho E omson One A Analytics, Re euters Knowwledge, Capit IQ, TheMa tal arkets.com and securitie a es.com Keynote Capitals Institu utional Resea arch - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business To unsubsc cribe from th mailing lis please reply to unsub his st, bscribe@keyynotecapitals s.net

- 2. TOP GAINERS Buzzin Stocks ng (BSE A-Group) E • BHE bagged a `1,143Cr contract fro NTPC to set EL om o Previous Currennt Change up a 500-Mw power generating unit at its w g Com mpany Name e Close(` `) Price(` `) (%) Vind dhyachal Su uper Therma Power Sta al ation in Mad dhya Bank of India 319.40 0 340.45 6.59 Prad desh. Uco Bank 65.70 0 69.40 5.63 • Spic ceJet hopes to take delivery of the first shipm e ment Asia Paints an 3821.90 0 4034.65 5.57 of directly impo orted aviatio fuel by early July. on Central Bank 72.75 5 76.45 5.09 • Oil and Natural Gas Corporation (ONG a GC), through the h Synd dicate Bank 88.30 0 92.50 4.76 Persspective Pla 2030, ha set ambi an as itious long-t term (BSE Mid-Cap) E targ gets. In 18 y years, ONGC would see to double its C ek exploration and produc ction grow wth, triple its Previous Currennt Change Com mpany Name e reveenues and earnings before in nterest, taaxes, Close(` `) Price(` `) (%) MCX X 862.05 935.05 8.47 depreciation, aand amortis sation, and quadruple its d e Jagr ran Prakashan n 87.15 94.00 7.86 mar rket capital. It also plans a six-fold rise in s e INDI IAB POWER 12.11 12.97 7.10 international ex xploration a and productiion (E&P). IL&F TRANS FS 170.45 181.80 6.66 • M&M plans to s M spend `5,0000Cr as inve estment tow wards Dena Bank 86.65 91.60 5.71 expansion and new produ uct develop pment over the r financial years 2013, 20 s 014 and 20 015. Expan nsion TOP LOSERS plan include the next phase of plant augmenta ns ation at it Chakan unit, near Pu ts une. (BSE A-Group) E • IL&F FS Transp portation N Networks said that a t Previous Currennt Change Com mpany Name e conssortium coomprised o the com of mpany and its d Close(` `) Price(` `) (%) Suzl lon Energy 19.75 5 18.05 5 -8.61 subs sidiary, Futturcage Inffrastructure India Limited, Unit ted Spirits 612.05 5 563.60 0 -7.92 has been mand dated to de evelop an inntegrated m multi- Tata Motors a 243.35 5 233.20 0 -4.17 leve automatic car par el rking facility at Khil lwat, Astr razeneca Hyderabad, on BOT basis by the Greater Hydera abad 1914.40 0 1835.60 0 -4.12 Phar Munnicipal Corrporation ( (GHMC). The conces T ssion ICIC Bank CI 817.00 0 784.30 0 -4.00 period for the project is 30 years, including two s , (BSE Mid-Cap) E years of construction perio and the revenue wi be od, ill Previous Currennt Change rued from t accr the parking fee and leasing of r g retail Com mpany Name e spac a release said. ce, Close(` `) Price(` `) (%) Fres senius Kabi 135.10 108.10 -19.99 • GMR Infrastruct R ture alleged that state- d -run Tamil N Nadu S Mo obility-$ 42.75 38.60 -9.71 Elec ctricity Boar and its g rd generation arm Tamiln nadu BOC India C 424.95 384.85 -9.44 Genneration and Distrib bution Corporation Ltd. Suzl lon Energy 19.75 18.05 -8.61 NGEDCO) ow around `850Cr to the compan (TAN wes t ny. REI Agro 8.94 4 8.27 -7.49 US markets U.S. stoocks on Thuursday close one of th worst mo ed he onths in year as the c rs, country revi ised its GDP growth in the P n first qu uarter to a 1 1.9% annualized pace, slower than the n 2.2% rate first esttimated and expectations for the May d jobs reeport decline sharply. ed Keyn note Capitals Research h (resea arch@keyno otecapitals.net) (+912 22-3026600 00)

- 3. India and Globa Economic Calendar a al c Countries / Fri iday Mo onday Tu uesday We ednesday Reg gions 1/ /Jun 4/Jun 4 5/Jun 6/Jun Ind dia Forex Reserves Data Bank Loan Growth n US Average H Hourly Factory O Orders ISM Non-Mfg Index Earnings ( (YoY & MoM), Aveerage Weekly Hoours Nonfarm P Payrolls, ICSC-Goldman Store e Unemploy yment Rate Sales Construction Spending (MoM) Glo obal UK Purcha asing UK House prices e Germanyy's Euro zo one ECB Manager Index data Purchasi ing Manage er interest rate t uring Manufactu Index Se ervices decision & press n confere ence German IIP Data ny KEYN NOTE CAPITTALS LTD. The Rub 9th Floo Senapati Bapat Marg, Dadar (W), Mumba – 400 028 by, or, ai 8 Tel. : +9 9122-30266 6000 • www w.keynotec capitals.com m Disclaiimer: This re eport is purely for informa ation purpose and is bassed on public information News cont c n. tent is attribu utable to various media, unle specified otherwise. A market related statistic data perta ess All cal ains to the im mmediately preceding trad ding day, unless stated other s rwise. Neithe the informa er ation nor any opinion expressed in this report constitutes an off y s fer, or an invitation to make an offer, to bbuy or sell the securities m mentioned he erein. We or any of our directors, offic cers or emplo oyees shall not in any way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgmen before e e s m e o nt acting on the conteents of this re eport. The rep port has not been edited due to time c d constraints.