VVIP Pune Call Girls Katraj (7001035870) Pune Escorts Nearby with Complete Sa...

Essel Propack

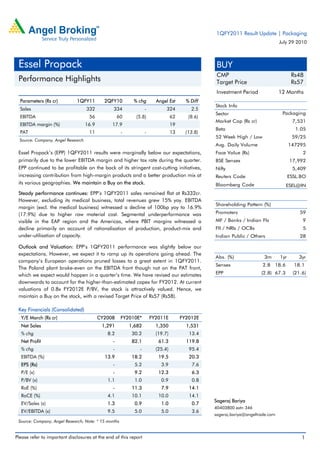

1. 1QFY2011 Result Update | Packaging

July 29 2010

Essel Propack BUY

CMP Rs48

Performance Highlights Target Price Rs57

Investment Period 12 Months

Parameters (Rs cr) 1QFY11 2QFY10 % chg Angel Est % Diff

Stock Info

Sales 332 334 - 324 2.5

Sector Packaging

EBITDA 56 60 (5.8) 62 (8.6)

Market Cap (Rs cr) 7,531

EBITDA margin (%) 16.9 17.9 19

Beta 1.05

PAT 11 - - 13 (13.8)

52 Week High / Low 59/25

Source: Company, Angel Research

Avg. Daily Volume 147295

Essel Propack’s (EPP) 1QFY2011 results were marginally below our expectations, Face Value (Rs) 2

primarily due to the lower EBITDA margin and higher tax rate during the quarter. BSE Sensex 17,992

EPP continued to be profitable on the back of its stringent cost-cutting initiatives, Nifty 5,409

increasing contribution from high-margin products and a better production mix at Reuters Code ESSL.BO

its various geographies. We maintain a Buy on the stock. Bloomberg Code ESEL@IN

Steady performance continues: EPP’s 1QFY2011 sales remained flat at Rs332cr.

However, excluding its medical business, total revenues grew 15% yoy. EBITDA

Shareholding Pattern (%)

margin (excl. the medical business) witnessed a decline of 100bp yoy to 16.9%

(17.9%) due to higher raw material cost. Segmental underperformance was Promoters 59

visible in the EAP region and the Americas, where PBIT margins witnessed a MF / Banks / Indian Fls 9

decline primarily on account of rationalisation of production, product-mix and FII / NRIs / OCBs 5

under-utilisation of capacity. Indian Public / Others 28

Outlook and Valuation: EPP’s 1QFY2011 performance was slightly below our

expectations. However, we expect it to ramp up its operations going ahead. The

Abs. (%) 3m 1yr 3yr

company’s European operations pruned losses to a great extent in 1QFY2011.

Sensex 2.8 18.6 18.1

The Poland plant broke-even on the EBITDA front though not on the PAT front,

which we expect would happen in a quarter’s time. We have revised our estimates EPP (2.8) 67.3 (21.6)

downwards to account for the higher-than-estimated capex for FY2012. At current

valuations of 0.8x FY2012E P/BV, the stock is attractively valued. Hence, we

maintain a Buy on the stock, with a revised Target Price of Rs57 (Rs58).

Key Financials (Consolidated)

Y/E March (Rs cr) CY2008 FY2010E* FY2011E FY2012E

Net Sales 1,291 1,682 1,350 1,531

% chg 8.2 30.2 (19.7) 13.4

Net Profit - 82.1 61.3 119.8

% chg - - (25.4) 95.4

EBITDA (%) 13.9 18.2 19.5 20.3

EPS (Rs) - 5.2 3.9 7.6

P/E (x) - 9.2 12.3 6.3

P/BV (x) 1.1 1.0 0.9 0.8

RoE (%) - 11.3 7.9 14.1

RoCE (%) 4.1 10.1 10.0 14.1

Sageraj Bariya

EV/Sales (x) 1.3 0.9 1.0 0.7

40403800 extn 346

EV/EBITDA (x) 9.5 5.0 5.0 3.6

sageraj.bariya@angeltrade.com

Source: Company, Angel Research; Note: * 15 months

Please refer to important disclosures at the end of this report 1

2. 1QFY2011 Result Update | Essel Propack

Exhibit 1: Quarterly performance

Consolidated business Packaging Business only

Y/E March (Rs cr) 1QFY11 2QFY10 % chg FY2010* CY2008 % chg 1QFY11 2QFY10 % chg

Total Revenue 332 334 - 1682 1291 30 332 289 15

Total RM 157 141 11 729 581 25 157 130 21

as % of sales 48.6 42.3 43.3 45.0

Gross Profit 175 193 (9) 953 710 34 175 159 10

Gross margin (%) 52.6 57.7 56.7 55.0 53 55

Staff cost 54 65 (16) 310 253 22 54 47 15

as % of sales 16.7 19.4 18.4 19.6 16 16

Other Expenses 64 68 (5) 337 70 378 64 60 7

as % of sales 19.9 20.4 20.0 5.5 19 21

Total Exp 276 274 1 1375 1111 24 276 238 16

as % of sales 83.1 82.1 81.8 86.1 83 82

EBITDA 56 60 (6) 306 180 70 56 51 10

EBITDA % 16.9 17.9 18.2 13.9 17 18

Depreciation 27 28 (5) 137 112 23 27 27 (2)

EBIT 30 32 (6) 169 68 148 30 24 24

EBIT % 8.9 9.5 10.0 5.3 9 8

Other Income 1 2 11 4 1 1

Interest 16 15 8 85 70 21 16 14 10

PBT 15 19 (23) 95 2 - 15 10 42

Extra-ord Items 0 1 30 (51) 0 0

PBT 15 18 125 (48) 15 10

Total tax 6 11 (47) 37 35 7 6 9 (37)

tax rate 40 58.4 38.8 1680.2 40 90

PAT 9 7 88 (83) 9 1

NPM (%) 2.7 2.0 5.2 (6.4) 3 0

Minority & Others (0) 2 (6) (5) 2 (1)

Adj PAT 11 (0) 82 (88) 11 0

Adj NPM (%) 0.0 (0.1) 4.9 (6.8) 3 0

Equity 31 31 31 31 31 31

EPS 0.6 0.4 31 5.6 (5.3) 0.6 0.1

Adj EPS 0.7 (0.0) 5.2 (5.6) 0.7 0.0

Source: Company, Angel Research. *15 month

Growth across geographies

EPP reported net sales of Rs332cr in 1QFY2011 as against Rs334cr in 2QFY2010.

However, excluding the medical business, sales grew by 15%. EPP‘s core

packaging business witnessed strong growth across regions. The AMESA region

primarily comprising India recorded robust growth of 22.6%, while Europe grew

24.6%. EAP comprising China registered healthy growth of 14% during the

quarter. However, the Americas remained flat at Rs81cr, due to lower utilisation

levels as major customers witnessed decline in key products. However,

management expects the same to recover by end of the September quarter.

July 29 2010 2

3. 1QFY2011 Result Update | Essel Propack

Exhibit 2: Segmental performance

Consolidated business Packaging Business only

Y/E March (Rs cr) 1QFY11 2QFY10 % chg FY2010 CY2008 % chg 1QFY11 2QFY10 % chg

Revenues

AMESA 157 128 22.6 686 500 37.1 157 128 22.6

EAP 61 57 6.4 306 215 42.6 61 53 14.4

Americas 81 121 (33.5) 532 420 26.7 81 81 0.1

Europe 34 27 24.6 158 156 1.2 34 27 24.6

Other 0 0 1 0 0 0

Total 332 334 (0.4) 1682 1291 30.3 332 289 15.0

PBIT

AMESA 22 19 15.9 90 84 6.5 22 19 15.9

EAP 15 19 (23.4) 100 74 35.6 15 16 (6.3)

Americas (1) 5 (113.7) 11 13 (19.6) (1) 1 (164.3)

Europe (4) (10) (61.4) (45) (92) (51.1) (4) (10) (61.4)

Other 15 37 (57.7) 78 58 34.6 15 37 (57.7)

Total 47 70 (32.2) 233 137 70.6 47 62 (23.6)

PBIT margins (%)

AMESA 13.9 14.7 13.1 16.8 13.9 14.7

EAP 24.5 34.0 32.8 34.5 24.5 29.9

Americas (0.9) 4.4 2.0 3.1 (0.9) 1.4

Europe (11.7) (37.9) (28.7) (59.4) (11.7) (37.9)

Other - - - - - -

Total 14.3 20.9 13.9 10.6 14.3 21.5

Source: Company, Angel Research; Note: EAP - East Asia Pacific - China, Indonesia, Singapore & Philippines, AMESA- Africa, Middle East and South Asia

(includes Egypt and India), Americas-USA, Mexico and Colombia, EU - UK, Germany, Poland and Russia

Cost-cutting measures restrict margin erosion; Europe reduces losses

EPP (core packaging business) posted EBITDA margin of 17% (18%) in 1QFY2011,

a yoy decline of 100bp, mainly on account of higher prices of key raw material

(like polymer and polyester) during the quarter. Gross margin fell by 200bp to

53% during the quarter.

July 29 2010 3

4. 1QFY2011 Result Update | Essel Propack

Exhibit 3: Margin trend

56.0 17.7 18.0

17.5

55.0

17.0 16.9

17.0

54.0

(%)

(%)

16.5

53.0 16.0

16.0

52.0 15.5

54.0 55.0 53.0 52.6

51.0 15.0

1QFY10 2QFY10 5QFY10 1QFY11

Gross margin (LHS) EBITDA margin (RHS)

Source: Company, Angel Research

Although OPM declined by 100bp, it continued to be in the 16-18% band

compared to the bottom of 4-7% hit in 4QCY2008 and 3QCY2008. Cost-cutting

initiatives undertaken by the company at its various manufacturing units restricted

the decline in margins. Europe was the biggest contributor, as it reduced losses on

a quarterly basis. During 1QFY2011, Europe pruned losses to Rs4cr from Rs5.5cr

in 5QFY2010 and Rs10.3cr in 2QFY2010.

Exhibit 4: Europe region – Prunes losses

0

(10)

Rs cr

(20)

(30)

(40)

3QCY08

4QCY08

1QFY10

2QFY10

3QFY10

4QFY10

5QFY10

1QFY11

Source: Company, Angel Research

Focus to improve profitability

The company is currently consolidating its operations wherein it is increasing focus

on the high-margin business of plasti-tubes. Hence, although the company may

report muted sales growth going ahead, the same will be compensated by better

profitability and earnings.

July 29 2010 4

5. 1QFY2011 Result Update | Essel Propack

Investment Arguments

Global leader, substantial market share to help garner more business: EPP is a

global leader in the tubes packaging business, with an estimated current market

share of 32%. Around 38% of the market is controlled by the small regional

players. As economic recovery gets underway, further consolidation can not be

ruled out.

New business offers good opportunity: EPP is present in speciality packaging

offering a solution to the food processing industry, which is recession proof in

nature. Speciality packaging is a high-need requirement of consumers. The

domestic food processing industry is still at a nascent stage, but it is fast gaining

momentum. The market size of this segment is huge and offers the company a

chance to diversify its existing revenue mix that is heavily dominated by lamitubes.

Stabilisation in operations at subsidiary level: In CY2008, EPP posted losses on a

consolidated basis, due to deterioration in the performance of its key subsidiaries.

This was on account of the drying-up of orders, shifting of operations by one of the

company's key clients and teething problems at the new plant. We believe EPP has

been able to tackle most of the problems at its various plants and its operations

are now stable and profitable.

Outlook and Valuation

We have marginally revised our estimates downwards to account for the higher-

than-estimated capex to be incurred in FY2012.

Exhibit 5: Change in estimates

Old New % chg

FY11 FY12 FY11 FY12 FY11 FY12

Sales 1,350 1,811 1,350 1,531 - (15.5)

EBITDA 263 367 263 310 - (15.5)

EBITDA % 19.5 20.3 11.4 13.2

Adj PAT 63 155 61 120 (2.7) (22.7)

Source: Company, Angel Research

EPP’s European operations reduced losses to Rs4cr in 1QFY2011, as against

Rs35cr in 3QCY2008, an improvement of 88%. Currently, operations are almost

EBITDA neutral, and we expect them to turn profitable by 2QFY2011. The

company has been aggressively adding new customers from the cosmetic and

pharma sectors, which is likely to result in a changed revenue mix. The current

revenue mix is dominated by lamitubes, while the cosmetic and pharma industries

consume plastic tubes, which have higher margins.

At current levels, the stock is trading at attractive valuations of 0.7x FY2012E

EV/Sales and 0.8x FY2012E P/BV. Hence, we maintain a Buy on the stock, with a

revised Target Price of Rs57 (Rs58).

July 29 2010 5

6. 1QFY2011 Result Update | Essel Propack

Exhibit 6: Key assumption

FY11 FY12 Comments

Sales growth (%)

AMESA (9.8) 14.0 New capacity to aid growth

EAP (20.7) 17.0 Ramp-up in new capacity to aid growth

Americas (39.3) 6.0 Plasti-tube segment to drive growth

EU 5.0 20.0 Plasti-tube segment to drive growth

Total (19.7) 13.4

EBITDA margins (%) 19.5 20.3 Continuing benefit of restructuring

Tax rate 33.8 25.2

Source: Company, Angel Research

Exhibit 7: One-year forward P/BV band

100

80

60

Rs

40

20

0

Jul-05

Jul-06

Jul-07

Jul-08

Jul-09

Jul-10

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Price 0.5x 0.8x 1.0x 1.3x 1.5x

Source: C-line, Angel Research

July 29 2010 6

11. 1QFY2011 Result Update | Essel Propack

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

Disclaimer

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Essel Propack

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 29 2010 11