(8264348440) 🔝 Call Girls In Mahipalpur 🔝 Delhi NCR

Indiabulls Zee Ent 15 May09

1. 4 Zee Entertainment Enterprises Limited

RESEARCH

EQUITY RESEARCH May 14, 2009

RESULTS REVIEW Zee Entertainment Enterprises Limited Hold

Share Data Near-term weakness in advertisement revenue

Market Cap Rs. 60.46 bn Zee Entertainment Enterprises Ltd. (Zee) reported a disappointing Q4’09

Price Rs. 139.15 result as its revenue fell 2.3% yoy and 5.8% qoq to Rs. 5.14 bn. The fall was

BSE Sensex 11,872.91

primarily due to a poor performance by advertisement segment, which

Reuters ZEE.BO

slipped 7.4% yoy and 14.9% qoq to Rs. 2.3 bn. However, subscription

Bloomberg Z IN

Avg. Volume (52 Week) 0.41 mn revenue grew at 13.3% yoy and 3.1% qoq to Rs. 2.35 bn. EBITDA margin

52-Week High/Low Rs. 251.80 / 88.10 dipped by 1.4% pts yoy to 23.4% due to higher staff and programming cost.

Shares Outstanding 434.52 mn Our DCF based valuation gives a fair price of Rs. 138, a downside of 1%

from the CMP of Rs. 139.15. Thus, we maintain our Hold rating on the stock.

Valuation Ratios (Consolidated)

Year to 30 March 2010E 2011E

A likely decline in advertisement revenue in FY10; but revival seen in

EPS (Rs.) 10.5 13.8 FY11: We expect advertisement revenue to decline by 8.5% in FY10

+/- (%) (12.6%) 31.6% impacted by current economic weakness. Besides, loss of viewership to IPL

PER (x) 13.3x 10.1x telecast and Colors is likely to pose a serious challenge to Zee TV as it has

EV/ Sales (x) 2.8x 2.5x

constantly lost market share with a drop in GRP from 273 in Q4’08 to 208 in

EV/ EBITDA (x) 11.8x 9.2x

Q4’09. However, post FY10 we expect the advertisement revenue to improve

Shareholding Pattern (%)

as the economic condition improves and corporate start spending more

Promoters 42 aggressively on advertisement to remain competitive. Besides, Zee TV’s

FIIs 30

GRP is likely to improve on back of launches of new programs.

Institutions 21

Public & Others 8

Subsequently, we expect a 4.4% growth in advertisement revenue in FY11.

Subscription revenue to maintain momentum: We expect subscription

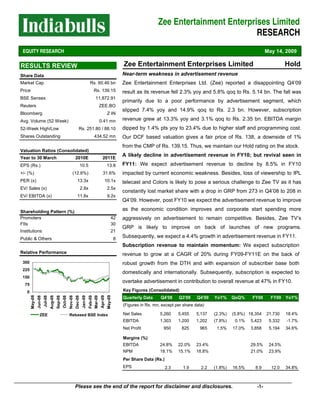

Relative Performance revenue to grow at a CAGR of 20% during FY09-FY11E on the back of

300 robust growth from the DTH and with expansion of subscriber base both

225

domestically and internationally. Subsequently, subscription is expected to

150

overtake advertisement in contribution to overall revenue at 47% in FY10.

75

0 Key Figures (Consolidated)

May-08

May-09

Aug-08

Nov-08

Apr-09

Sep-08

Dec-08

Jun-08

Jul-08

Oct-08

Jan-09

Feb-09

Mar-09

Quarterly Data Q4'08 Q3'09 Q4'09 YoY% QoQ% FY08 FY09 YoY%

(Figures in Rs. mn, except per share data)

ZEE Rebased BSE Index Net Sales 5,260 5,455 5,137 (2.3%) (5.8%) 18,354 21,730 18.4%

EBITDA 1,303 1,200 1,202 (7.8%) 0.1% 5,423 5,332 -1.7%

Net Profit 950 825 965 1.5% 17.0% 3,858 5,194 34.6%

Margins (%)

EBITDA 24.8% 22.0% 23.4% 29.5% 24.5%

NPM 18.1% 15.1% 18.8% 21.0% 23.9%

Per Share Data (Rs.)

EPS 2.3 1.9 2.2 (1.8%) 16.5% 8.9 12.0 34.8%

Please see the end of the report for disclaimer and disclosures. -1-

2. 4 Zee Entertainment Enterprises Limited

RESEARCH

EQUITY RESEARCH May 14, 2009

Valuation

We have revised our target price to Rs. 138 from Rs. 114 on the

expectation of better operating margin due to reduced staff, SG&A (mainly

carriage cost) and programming cost; however we are cautious on

advertisement segment due to still weak economic environment. However,

we maintain our medium- to long-term positive view on the stock on the

back of its strong momentum in subscription revenue, a wide buffet of

channels and global presence.

Based on our DCF valuation (assuming a 5% terminal growth rate, and a

14.5% WACC), we have arrived at a target price of Rs. 138. Thus, we

maintain a Hold rating on the stock.

Sensitivity of Our Fair Value Estimates:

Terminal Rate (%)

Cost of Capital (%)

137.97 13.0 13.5 14.5 14.0 14.5

4.0 156 147 132 139 131

4.5 161 151 135 142 134

5.0 166 155 138 146 138

5.5 172 160 142 150 141

6.0 179 166 146 155 145

Result Highlights and Outlook

Zee posted a weak Q4’09 result as its net sales slipped 2.3% yoy and 5.8%

qoq to Rs. 5.1 bn due to a 7.4% yoy and 14.9% qoq decline in advertisement

revenue to Rs. 2.3 bn. The decline in the advertisement revenue can be

blamed to slowdown in the economy and stiff competition from the new

Advertisement revenue to remain players (Colors, 9X etc). However, subscription revenue provided some

under pressure in next two to three

cushion to the overall revenue as segment grew by 13.3% yoy and 3.1% qoq

quarter

to Rs. 2.3 bn on the back of an outstanding 104% yoy and 35% qoq jump in

the DTH revenue.

We expect the Company’s revenue to grow at a 4% in FY10E due to de-

Subscription revenue is likely to

be a stronghold for the Company growth in the advertisement segment. We believe advertisement revenue to

decline by 8.5% in FY10 due to cut in corporate advertisement spending and

a fall in the GRP. But, we expect a 4.4% growth in advertisement revenue in

FY11 as the economy revives. Moreover, a launch of new programs is likely

to support the growth in advertisement segment. On the contrary,

Please see the end of the report for disclaimer and disclosures. -2-

3. 4 Zee Entertainment Enterprises Limited

RESEARCH

EQUITY RESEARCH May 14, 2009

subscription revenue is likely to maintain growth momentum at a CAGR of

around 20% during FY09-FY11 with the help of growing traction in DTH and

increasing subscriber base.

EBITDA fell 7.8% yoy to Rs. 1.2 bn while the EBITDA margin dropped

138 bps yoy to 23.4% due to high staff and programming costs. However, on

sequential basis programming cost has come down to

Higher staff and programming cost

dragged down the EBITDA margin Rs. 2.2 bn, a slide of 16.5% as no new programmes were launched in the

last quarter.

We expect the EBITDA margins will remain flat for FY10 at around 24% but

will improve post FY10 as the carriage cost comes down. Moreover, low staff

cost would also help in margin improvement. For FY11E we expect EBITDA

margin to increase by 309 bps yoy to 27.1%.

Key Risks

The following factors can pose a risk to our rating:

• Increasing competition from the new channels

• Falling GRPs and market share

• Drop in advertisement rates

Key Figures (Consolidated)

Year to March FY06 FY07 FY08 FY09 FY10E FY11E CAGR (%)

(Figures in Rs. mn, except per share data) (FY08-11E)

Net Sales 16,544 15,159 18,354 21,730 22,604 25,499 11.6%

EBITDA 2,849 3,210 5,423 5,332 5,421 6,904 8.4%

Net Profit 2,277 2,382 3,858 5,194 4,542 5,977 15.7%

Margins(%)

EBITDA 17.2% 21.2% 29.5% 24.5% 24.0% 27.1%

NPM 13.8% 15.7% 21.0% 23.9% 20.1% 23.4%

Per Share Data

EPS (Rs.) 5.2 5.6 8.9 12.0 10.5 13.8 15.8%

PER (x) 45.5x 44.6x 27.6x 11.6x 13.3x 10.1x

Please see the end of the report for disclaimer and disclosures. -3-

4. 4 Zee Entertainment Enterprises Limited

RESEARCH

EQUITY RESEARCH May 14, 2009

Disclaimer

This report is not for public distribution and is only for private circulation and use. The Report should not be reproduced

or redistributed to any other person or person(s) in any form. No action is solicited on the basis of the contents of this

report.

This material is for the general information of the authorized recipient, and we are not soliciting any action based upon it.

This report is not to be considered as an offer to sell or the solicitation of an offer to buy any stock or derivative in any

jurisdiction where such an offer or solicitation would be illegal. It is for the general information of clients of Indiabulls

Securities Limited. It does not constitute a personal recommendation or take into account the particular investment

objectives, financial situations, or needs of individual clients. You are advised to independently evaluate the investments

and strategies discussed herein and also seek the advice of your financial adviser.

Past performance is not a guide for future performance. The value of, and income from investments may vary because

of changes in the macro and micro economic conditions. Past performance is not necessarily a guide to future

performance.

This report is based upon information that we consider reliable, but we do not represent that it is accurate or complete,

and it should not be relied upon as such. Any opinions expressed here in reflect judgments at this date and are subject

to change without notice. Indiabulls Securities Limited (ISL) and any/all of its group companies or directors or employees

reserves its right to suspend the publication of this Report and are not under any obligation to tell you when opinions or

information in this report change. In addition, ISL has no obligation to continue to publish reports on all the stocks

currently under its coverage or to notify you in the event it terminates its coverage. Neither Indiabulls Securities Limited

nor any of its affiliates, associates, directors or employees shall in any way be responsible for any loss or damage that

may arise to any person from any error in the information contained in this report.

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal

views about the subject stock and no part of his or her compensation was, is or will be, directly or indirectly related to

specific recommendations or views expressed in this report. No part of this material may be duplicated in any form

and/or redistributed without Indiabulls Securities Limited prior written consent.

The information given herein should be treated as only factor, while making investment decision. The report does not

provide individually tailor-made investment advice. Indiabulls Securities Limited recommends that investors

independently evaluate particular investments and strategies, and encourages investors to seek the advice of a financial

adviser. Indiabulls Securities Limited shall not be responsible for any transaction conducted based on the information

given in this report, which is in violation of rules and regulations of National Stock Exchange or Bombay Stock

Exchange.

Indiabulls (H.O.), Plot No- 448-451, Udyog Vihar, Phase - V, Gurgaon - 122 001, Haryana. Ph: (0124) 3989555, 3989666 -4-