Downloaded 2,168 times

The document provides objectives and content for Chapter 4 of the textbook "Accounting Information Systems, 6th edition". It covers the revenue cycle, including key processes like sales orders, billing, cash receipts, and collections. It describes the flow of transactions, necessary documents and journals, risks and controls at each step. It also discusses how technology can automate or reengineer the revenue cycle through systems like real-time processing, EDI, point-of-sale, and the implications for internal controls.

Overview of 'Accounting Information Systems, 6th edition' by James A. Hall, published by Cengage Learning.

Objectives including revenue cycle tasks, functional departments, audit trails, risks, and technology implications.

Visual representation of revenue cycle subsystems: Sales Order, Billing, Cash Receipts, Shipping, and Customer Service.

Process of preparing journal vouchers for Accounts Receivable, Inventory Control, and Cash Receipts departments.

Details of revenue cycle databases, including master files and transaction files related to customers and inventory.

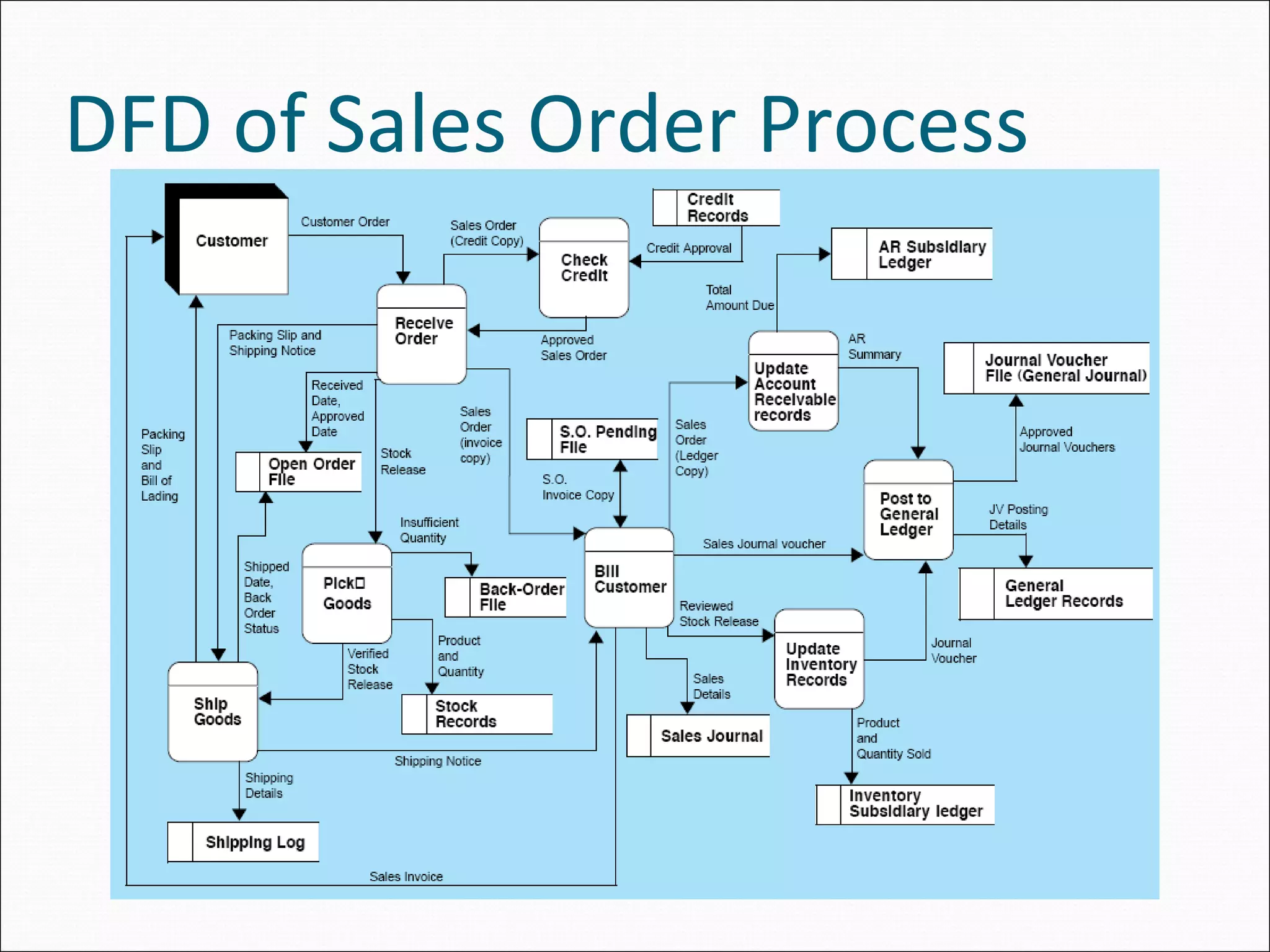

Data Flow Diagram (DFD) illustrating the process of handling sales orders.

Flowchart detailing the steps involved in the sales order processing.

Outline of manual sales order processing, including order placement, authorization, shipping, and A/R entries.

Data Flow Diagram (DFD) depicting sales returns process.

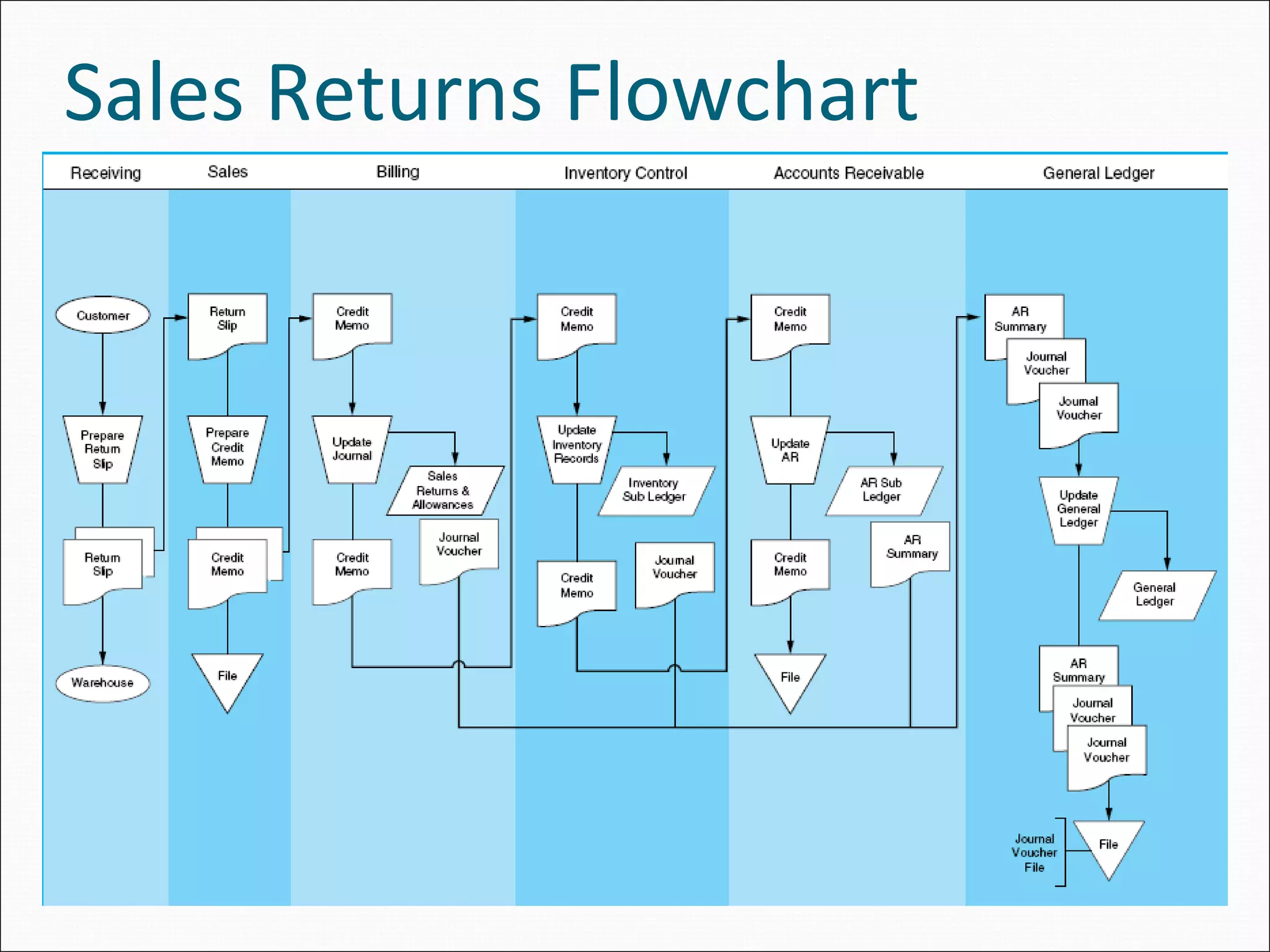

Flowchart detailing the steps involved in processing sales returns.

Journal entries required for sales return transactions, including adjustments in accounts.

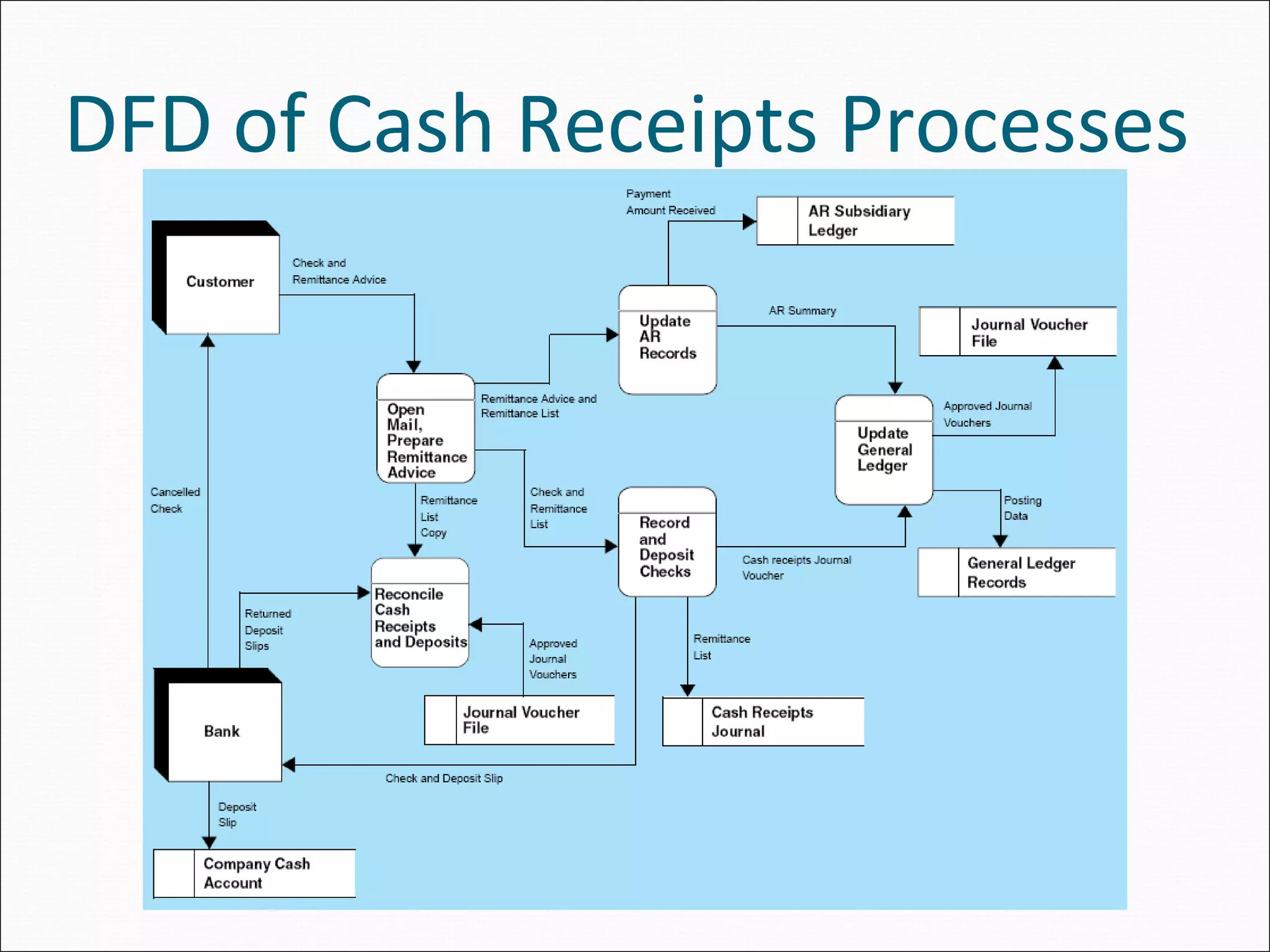

Data Flow Diagram (DFD) representing processes involved in cash receipts.

Flowchart detailing the cash receipts processing steps from preparation to updating records.

Detailed steps involved in manual processing of cash receipts, from mailroom to general ledger updates.

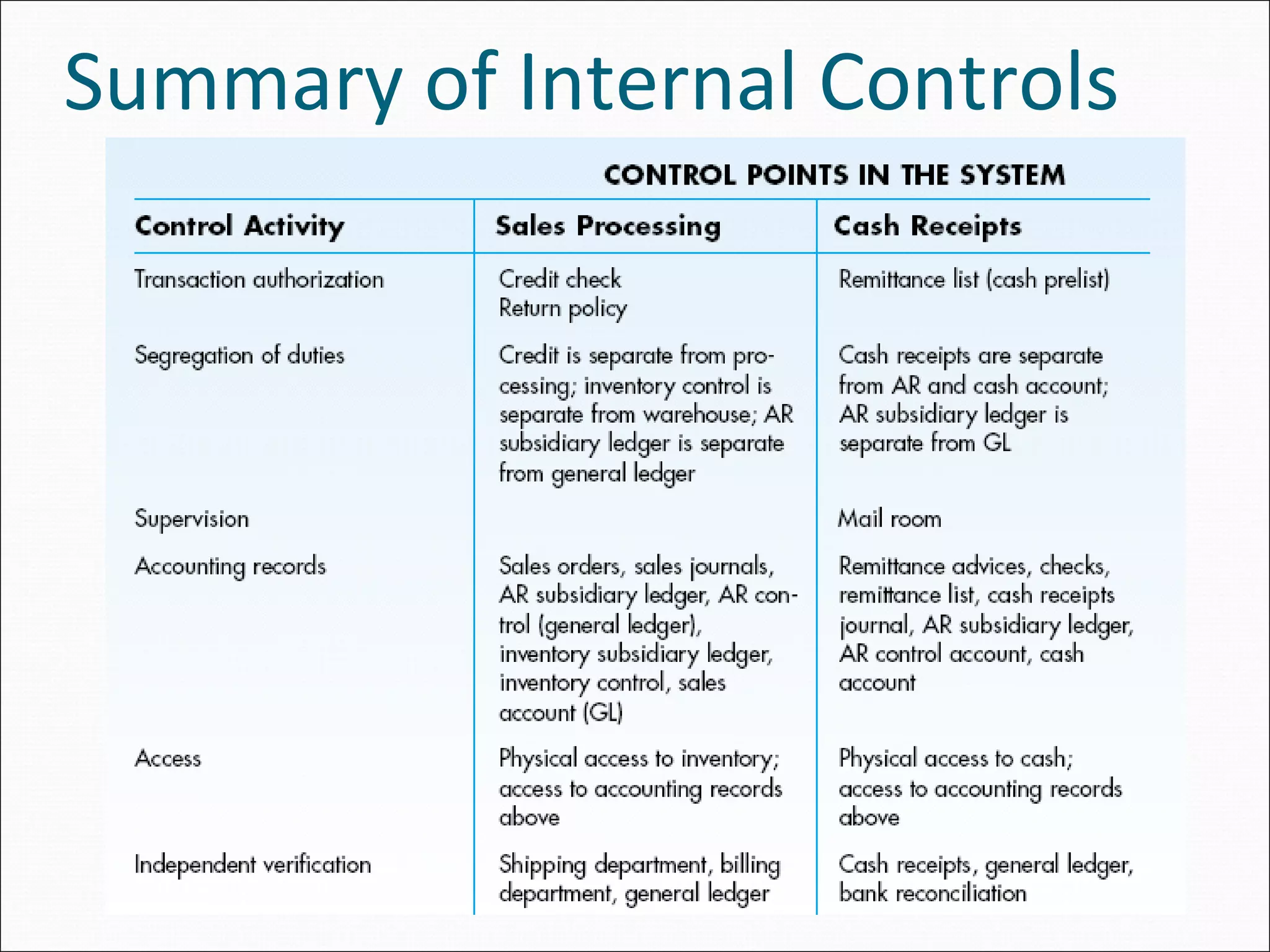

Overview of internal controls related to the revenue cycle.

Importance of proper authorizations and documentation to prevent unauthorized transactions.

Three rules for effective segregation of functions to prevent fraud and ensure control.

Role of supervision as a control measure when segregation of duties is not possible.

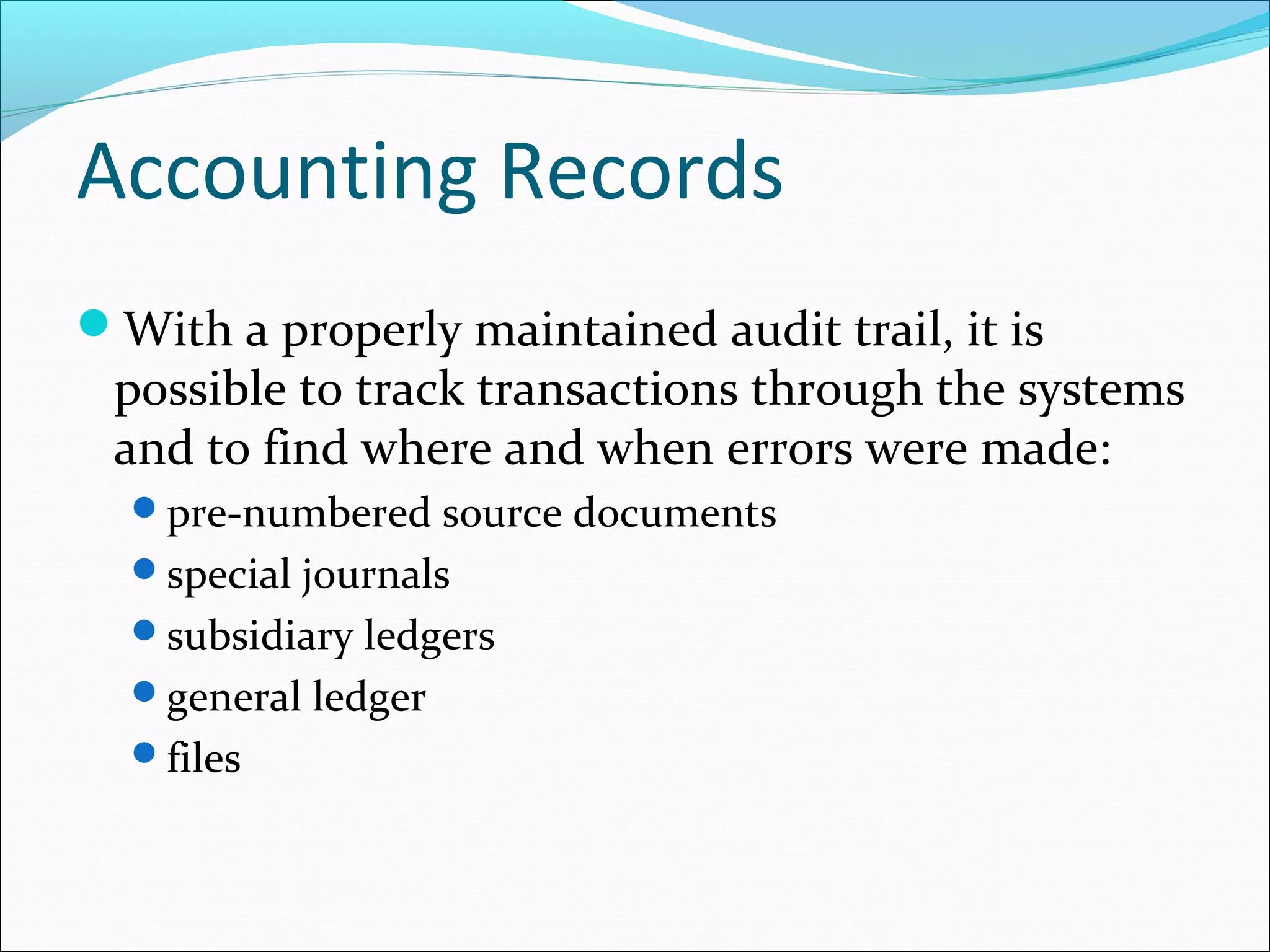

Importance of maintaining an audit trail to track transactions and identify errors.

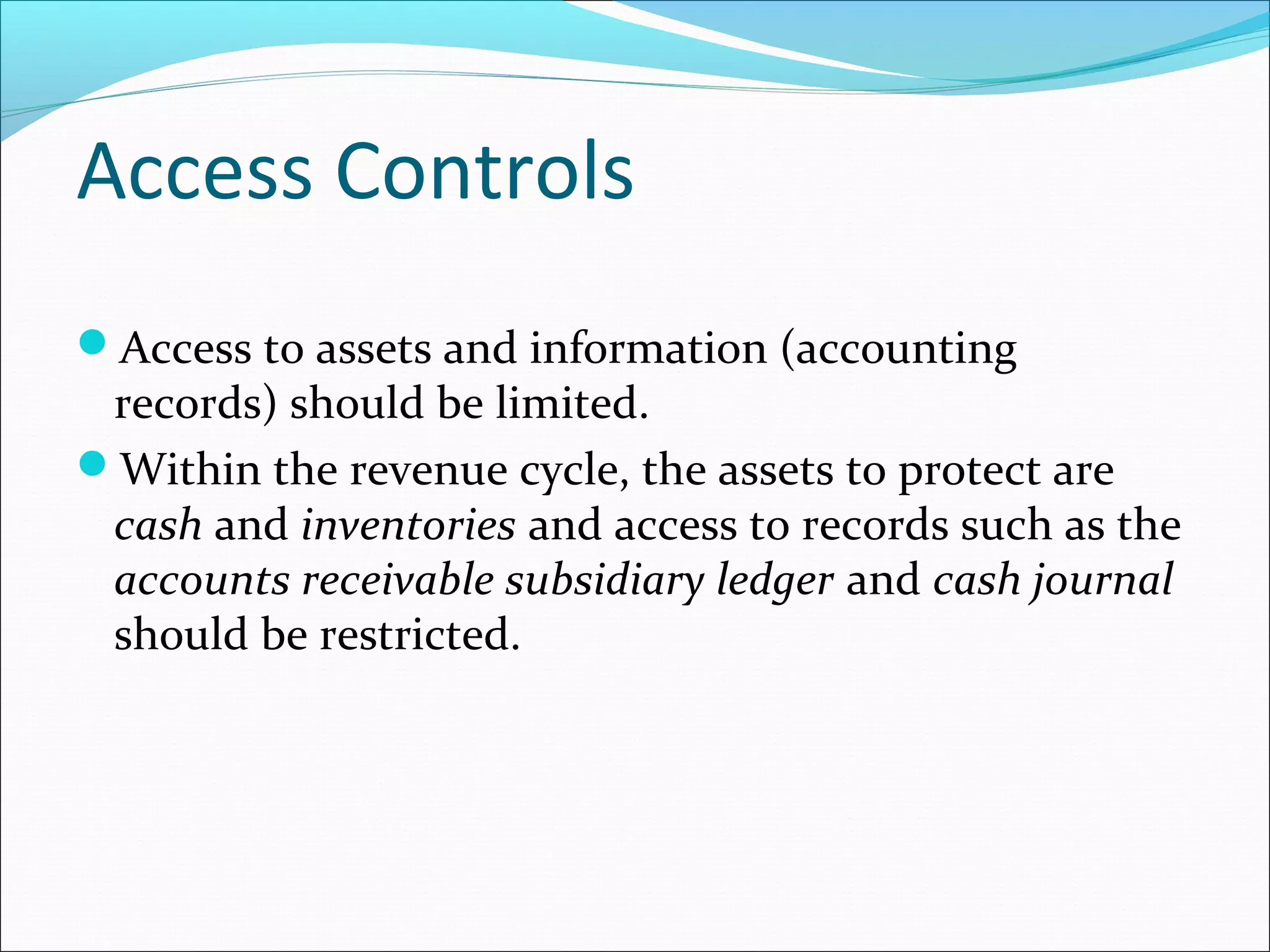

Access control measures to protect assets, records, and sensitive information within the revenue cycle.

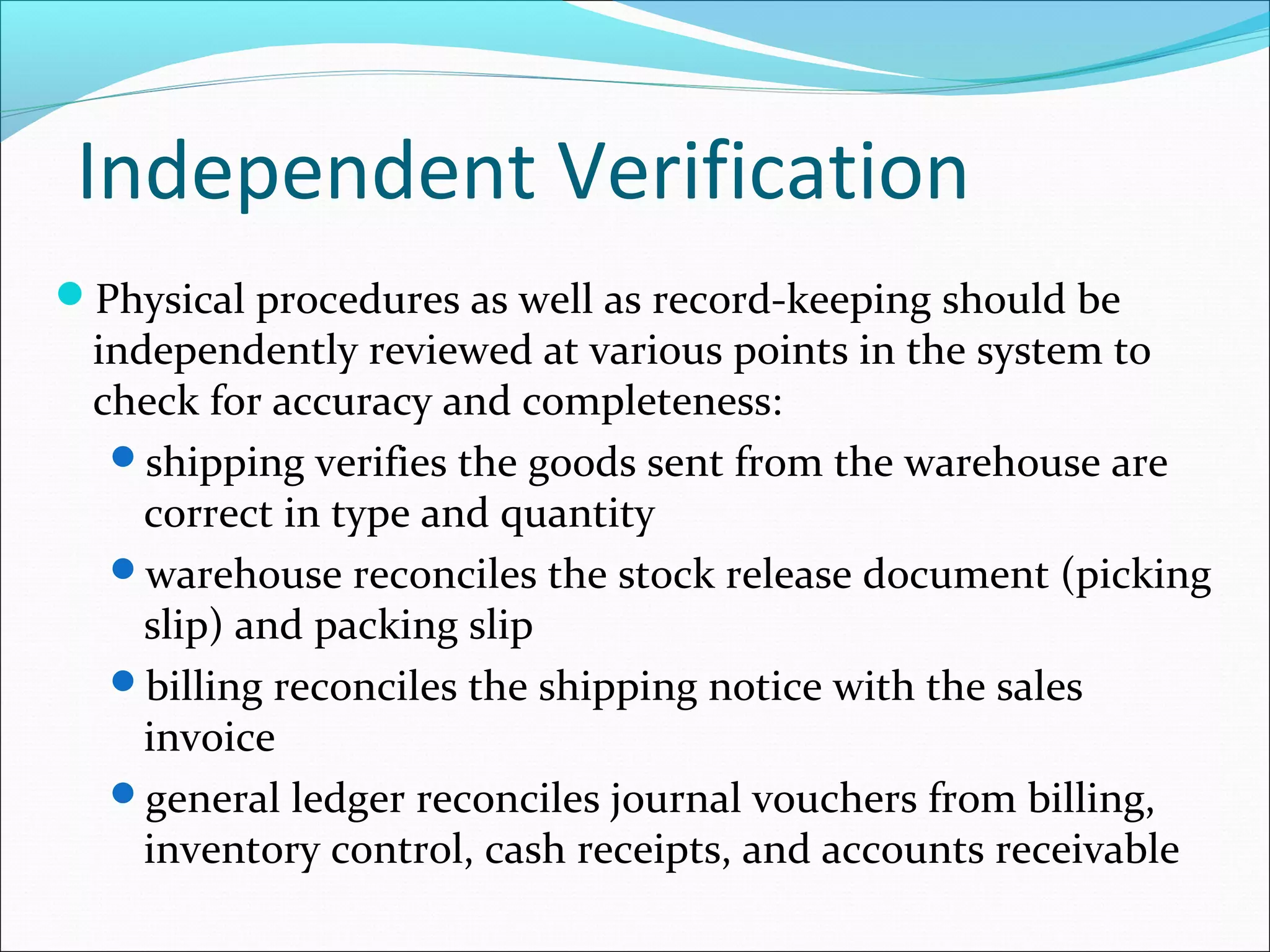

Procedures for independent review of processes and records to ensure accuracy.

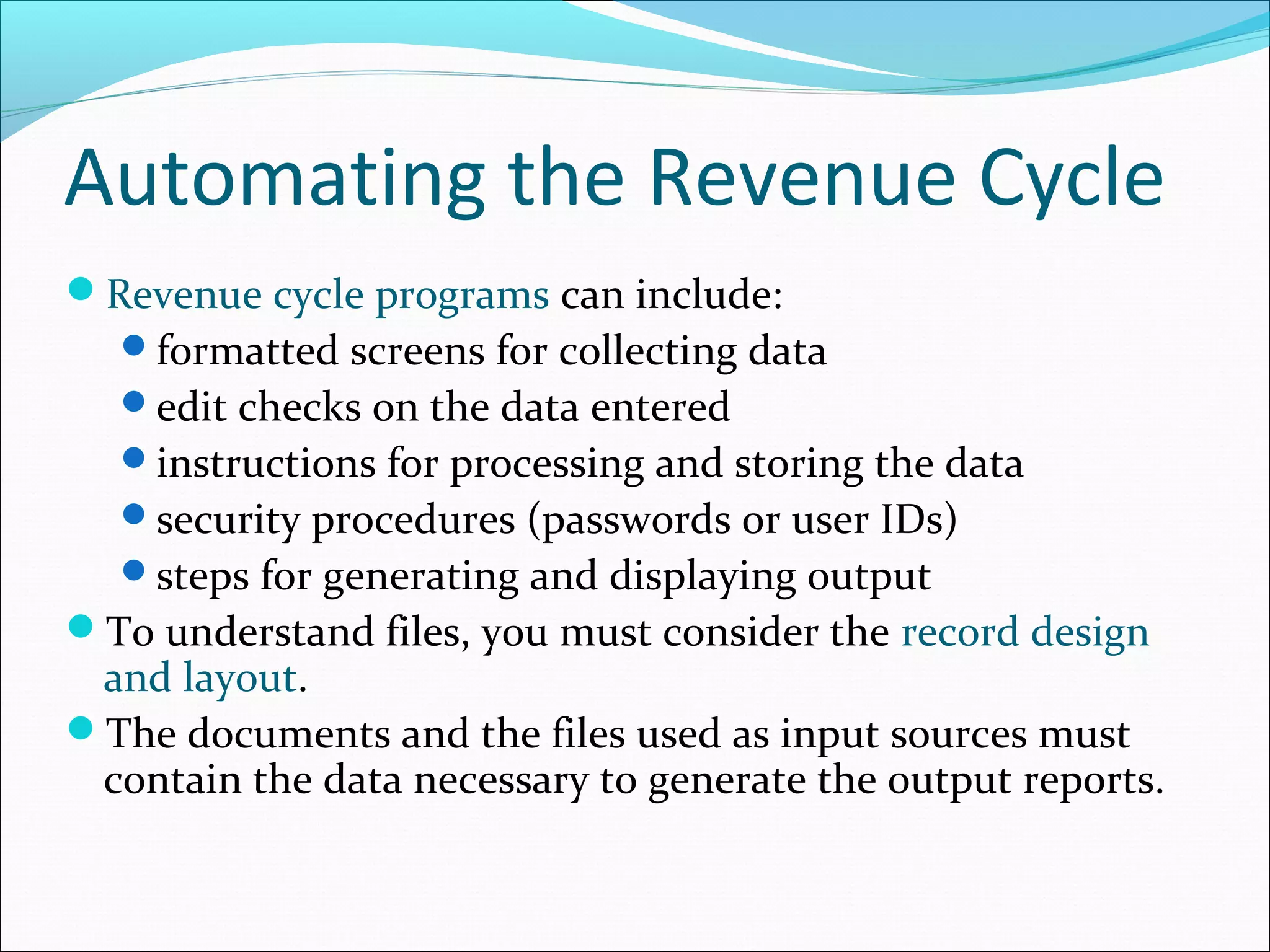

Transformation of revenue cycle through automation, reducing reliance on paper and enhancing efficiency.

Overview of CBAS, focusing on automation and reengineering for efficiency.

Illustration of automated batch sales processes.

Utilization of real-time technology to streamline sales order processing.

Details on features and benefits of real-time sales order input and output.

Benefits include shorter cash cycles, improved inventory management, and reduced errors.

Innovations in cash receipts processes focusing on security and efficiency.

Details of automated processes for handling cash receipts.

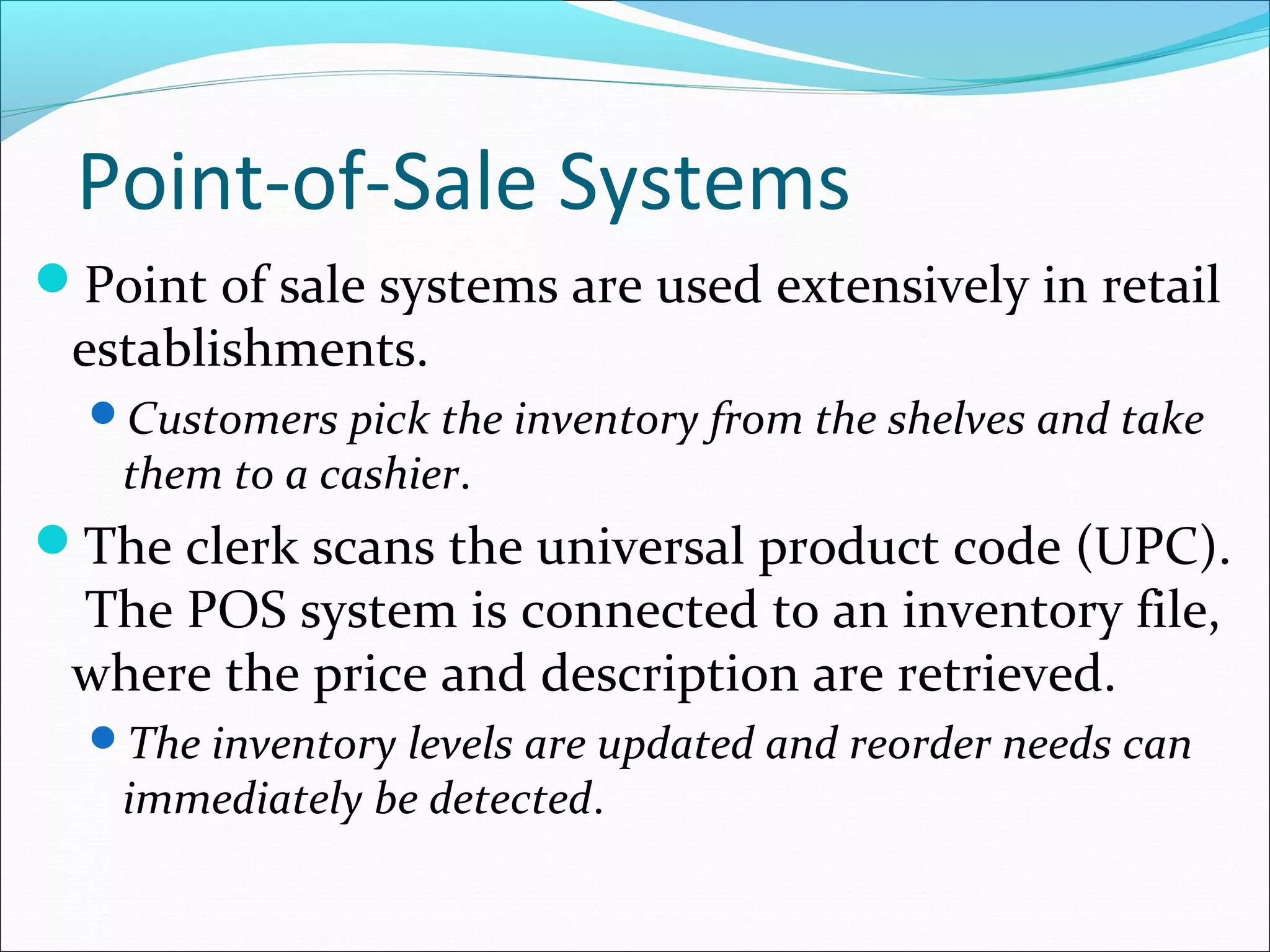

Operation of POS systems in retail, including transaction processing and inventory updates.

Overview of computerized systems for managing POS transactions.

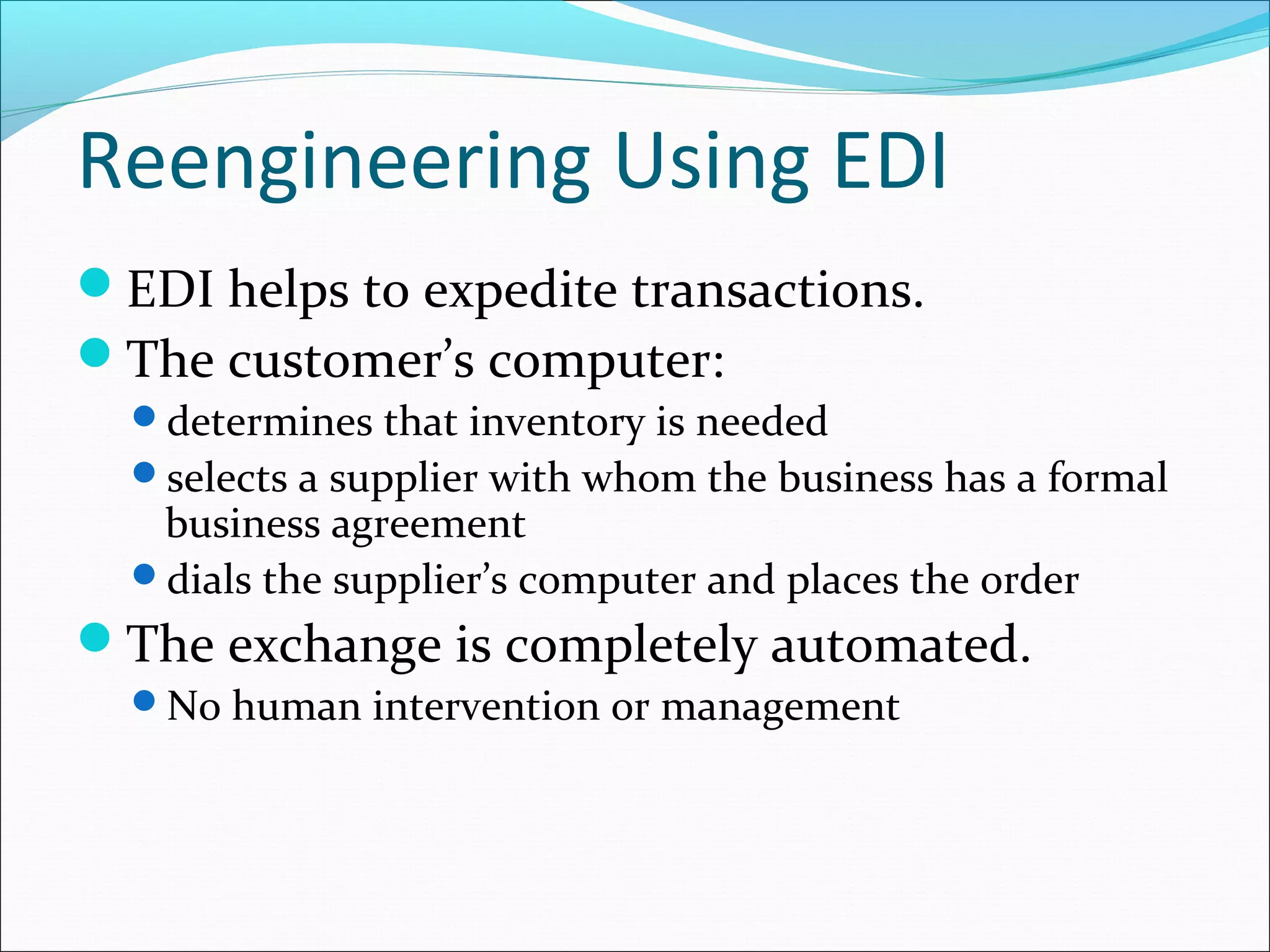

Automation of transactions through EDI, facilitating inventory management and order processing.

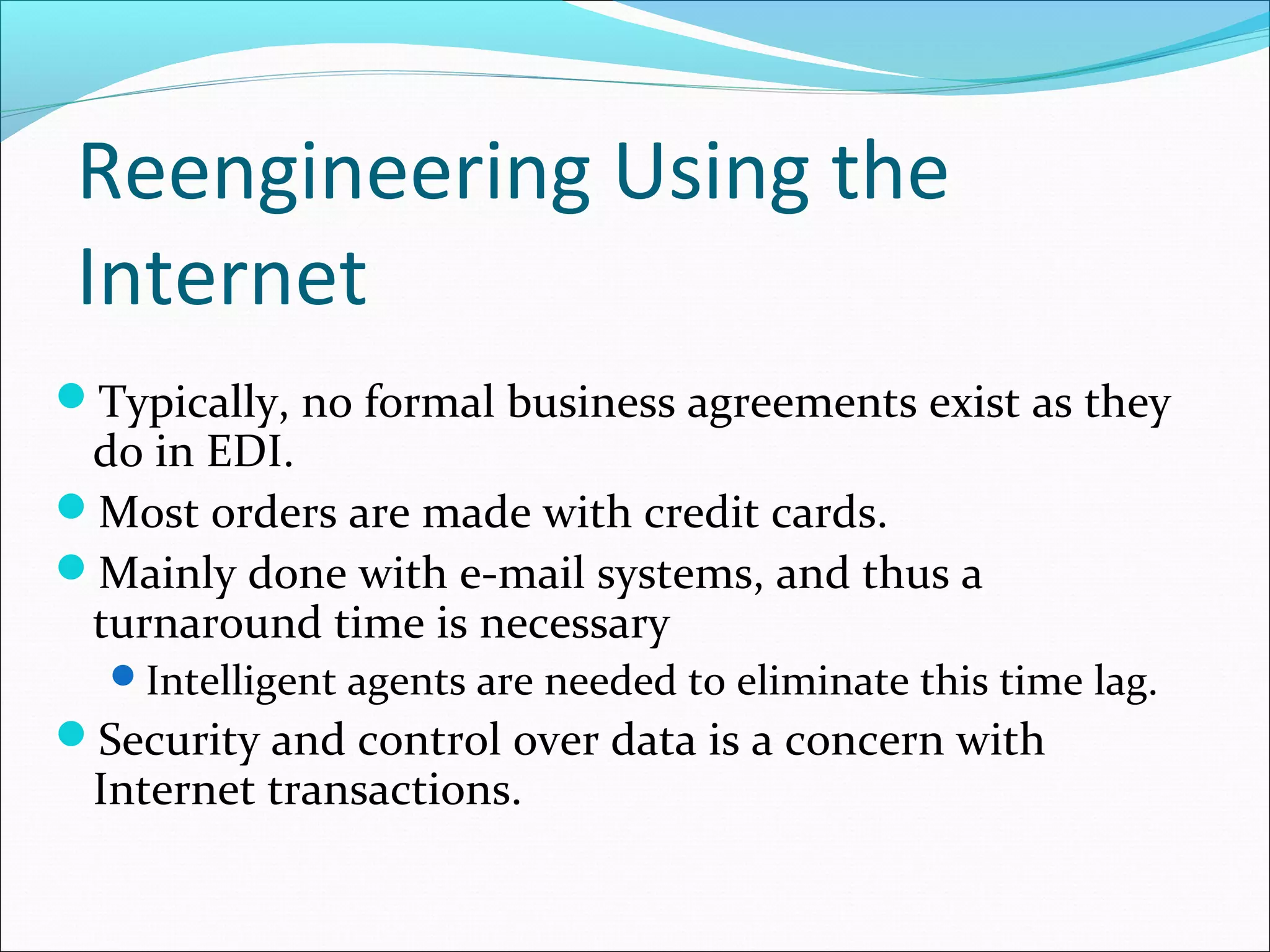

Overview of Internet-based transactions, security issues, and the need for intelligent agents.

Control considerations for CBAS, including authorization, segregation of duties, and independent verification.

Introduction to PC-based systems used for accounting in small and decentralized firms.

Challenges in PC-based systems related to control issues including segregation of duties and data security.