Introduction

• The Salesand Collection Cycle refers to the process through

which a business generates revenue by selling goods or services

and receives payment for these sales.

• This cycle involves a series of activities related to the sale of

products, from order receipt to cash collection. Auditing this

cycle ensures that financial transactions are accurate, legitimate,

and properly recorded.

• When conducting an audit of the Sales and Collection Cycle,

the auditor examines the processes, records, and controls to

verify that the revenue and related cash inflows are accurate,

properly authorized, and not subject to fraud or misstatement.

3.

•Before studying theprocess of assessing control risk and

designing tests of controls and substantive tests of transactions

for each class of transactions, it is important to know the sales

and collection cycle classes of transactions and account

balances.

•It is also important to understand the typical documents and

records used in the cycle.

4.

I. Accounts andClasses of Transactions in the Sales and

Collection Cycle

• The overall objective in the audit of the sales and collection cycle is

to evaluate whether the account balances affected by the cycles

are fairly presented :

1. Accounts in the Sales and Collection Cycle:

Accounts refer to the financial statement line items that reflect a

company’s financial position and performance. These include

assets, liabilities, equity, revenue, and expenses. The accounts related

with sales and collection cycle are:

5.

Accounts in theSales and

Collection Cycle

Sales

Accounts receivable

Cash in bank

Cash discount taken

Sales returns and allowances

Allowance for uncollectible accounts

Bad debt expense

6.

2. Classes ofTransactions in the Sales and Collection

Cycle:

A class of transactions refers to a group of similar financial

transactions recorded in a specific period that affect financial

statement accounts. The classes of transactions in the sales and

collection cycle are:

Sales Transactions

Cash receipts Transactions

Sales returns and allowances Transactions

Charge-off of uncollectible accounts Transactions

Bad Debt Expense and Write-offs Transactions

7.

II. Business Functionsand Related Documents &Records in the Cycle

• A business function in the sales cycle refers to a specific activity that takes

place in the process of selling goods or services. These functions ensure

that sales transactions are properly executed, recorded, and controlled.

• Each function involves documents and records that serve as evidence of

transactions and help maintain accuracy in financial reporting.

• The Sales and Collection Cycle involves the decisions and processes

necessary for the transfer of the ownership of goods and services to

customers after they are made available for sale.

• It begins with a request by a customer and ends with the conversion of

material or service into an account receivable, and ultimately into cash.

8.

•There are eightBusiness Functions for sales and collection

cycle. They occur in every business in the recording of the five

classes of transactions in the sales and collection cycle.

•Below you will find summary discussions of the Classes of

Transactions, Accounts, Business functions, and related

Documents and Records for the Sales and Collection Cycle.

9.

1. Sales Transaction

Accountsaffected by sales transaction:

Sales

Accounts receivable

Business Functions

i. Processing customer orders, - Customer places an order using Customer

Order document. The request for goods by a customer is the starting point for

the entire cycle

o This is often followed by the issuance of Sales Order.

ii. Granting credit- a properly authorized person must approve credit to the

customer for sales on account.

o Minimizes the possibility of bad debts.

o It may be a programmed approval- based on preapproved credit limit

maintained in a customer master file.

10.

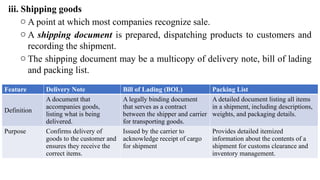

iii. Shipping goods

oA point at which most companies recognize sale.

o A shipping document is prepared, dispatching products to customers and

recording the shipment.

o The shipping document may be a multicopy of delivery note, bill of lading

and packing list.

Feature Delivery Note Bill of Lading (BOL) Packing List

Definition

A document that

accompanies goods,

listing what is being

delivered.

A legally binding document

that serves as a contract

between the shipper and carrier

for transporting goods.

A detailed document listing all items

in a shipment, including descriptions,

weights, and packaging details.

Purpose Confirms delivery of

goods to the customer and

ensures they receive the

correct items.

Issued by the carrier to

acknowledge receipt of cargo

for shipment

Provides detailed itemized

information about the contents of a

shipment for customs clearance and

inventory management.

11.

iv. Billing customersand recording sales- Billing is a means by

which the customer is informed of the amount due for the

goods.

oAll shipments should be billed and no shipment should be

billed more than once.

oBilling should consider authorized price, quantity shipped

and other terms.

oDone with multicopy sales invoice and simultaneously

updating of the sales transaction file, accounts receivable

master file, and the general ledger master file for sales and

accounts receivable.

12.

Documents and Records

Customer Order- a request for merchandise by a customer.

o It may be received in differing formats.

Sales Order- used to communicate the description, quantity and related specification of

goods ordered with in the company.

o Often used to indicate credit approval and authorization for shipment.

Shipping Document- a document prepared to initiate shipment of goods.

o Prepared in at lease in three copies – customer, accounts, retained

Sales invoice-a document indicating the description and quantity of goods sold, price,

freight charges, insurance, terms, and other relevant data.

o Prepared in at least three copies.

13.

Sales transactionfile- is a database (computer generated file) or record that

contains details of all sales transactions during a specific period. This file is

essential for financial reporting, auditing, and business analysis.

It includes all information entered into the system and information for each

transaction- like invoice number date of sale, customer information(Name, ID,

address…), product detail(qty, price, total amount), payment term (credit or

cash, payment due date, discounts if any), account classifications, sales person,

and commission rate.

o The information in this file is used for a variety of records, listing, or

reports- e.g. sales journal, A/R master file, and transactions for certain

account balance or division.

14.

Sales journalor listing- a report generated from the sales transaction file that

typically includes the customer name, date, amount, and account classification

or classifications for each transaction, such as division or product line.

o It also identifies whether the sale was for cash or credit.

Accounts receivable master file- a file used to record individual sales, cash

receipts, and sales returns and allowances for each customer and to maintain

customer account balances. A summary file that tracks customer balances and

outstanding receivables.

o The master file is updated from the sales, sales returns and allowances, and

cash receipts computer transaction files.

o It is also called the A/R subsidiary ledger or subledger

15.

Accounts Receivabletrial balance- a list of the amounts owed by each

customer at a point in time.

o This is prepared directly from the A/R master file.

o It is often an aged trial balance.

Monthly statements- a document sent by mail or electronically to each

customer indicating the beginning balance of A/R, the amount and due

date of each sale, cash payments received, credit memos issued, and the

ending balance due.

16.

2. Cash ReceiptsTransaction

Accounts

Cash in bank (debits from cash receipts)

Accounts receivable

Business Functions

v. Processing and recording cash receipts- includes receiving, depositing and

recording cash- currency & checks.

o The possibility of theft is the most important concern (both before and

after recorded).

o All cash receipts must be deposited intact and recorded in the cash receipts

transaction file.

o Remittance advices are important for this purpose.

17.

Documents and Records

Remittance advice-

o is a document sent by a customer to a supplier (or creditor) to inform them that

a payment has been made.

o a document that accompanies the sales invoice mailed to the customer and can

be returned to the seller with the cash payment.

o Used to permit the immediate deposit of cash & to improve control over

custody of assets.

Prelisting of cash receipts- a list prepared when cash is received by someone who

has no responsibility for recording sales, A/R, or cash and who has no access to

accounting records.

o It is used for verifying whether cash received was recorded and deposited.

18.

Cash receiptstransaction file- a computer generated file that

includes all cash receipts transactions processed by the accounting

system for a period.

o Used to prepare the cash receipts journal and update the A/R and

general ledger master files.

Cash receipts journal or listing- a report generated from the cash

receipts transaction file that includes all transactions for any time

period.

19.

3. Sales Returnsand Allowances Transaction

Accounts

Sales returns and allowances

Accounts receivable

Business Functions

vi. Processing and recording sales returns and allowances

o When a customer is dissatisfied with the goods, the seller often accepts the

returned goods or grants a reduction in the charges.

o It is necessary to issue a Receiving Report and return the goods to store.

o Record the transaction promptly and accurately on the Sales and Returns

Journal & A/R master file.

o As an aid for control & to facilitate recording Credit Memos are issued.

20.

Documents and Records

Credit memo- a document indicating a reduction in the amount due from

a customer because of returned goods and allowances granted.

Sales returns and allowances journal- a journal used to record sales

returns and allowances.

o Sales journal can be used instead.

21.

4. Charge-off ofuncollectible accounts Transactions

Accounts

Allowance for uncollectible accounts

Accounts receivable

Business Functions

vii. Charging off uncollectible accounts receivable

o When the company concludes that an amount is no longer collectible,

it must be charged off- e.g. if a customer becomes bankrupt.

o Necessary adjusting entries are made.

Documents and Records

Uncollectible account authorization form- a document used initially to

indicate authority to write an account receivable off as uncollectible.

General journal

22.

5. Bad DebtExpense Transaction

Accounts

Bad debt expense

Allowance for uncollectible accounts

Business Functions

viii. Providing for bad debts

o The provision should be sufficient to allow for the current period sales

that the company will be unable to collect in the future.

o Allowance method is used.

Documents and Records

General journal

23.

III. Methodology forDesigning Tests of Controls and

Substantive Tests of Transactions for Sales

When auditing sales transactions, auditors use a structured approach

to assess internal controls and test transactions for potential

misstatements. This methodology includes tests of controls and

substantive tests of transactions to ensure the accuracy,

completeness, and legitimacy of recorded sales.

1. Designing tests of control for sales :

Tests of controls assess whether a company’s internal controls over

sales transactions are operating effectively. The goal is to determine

whether the company is following established procedures to prevent

or detect errors and fraud.

24.

Steps in DesigningTests of Controls of sales:

For each control the auditor plans to rely on to reduce assessed control risk,

one or more tests of controls must be designed to verify its effectiveness.

Step 1. Understanding Internal Controls

Typical approach for sales involves studying the client's flowcharts,

Auditor prepares an internal control questionnaire, and performs walk-

through tests of sales. Identify key controls in the sales cycle (e.g., order

approvals, credit checks, invoicing procedures)

Example:

• The auditor observes the sales process and documents of x company that:

• Sales orders must be approved by a credit manager.

• Goods are only dispatched upon authorization.

• Sales invoices are automatically generated from the system after goods are

shipped.

25.

Step 2. AssessPlanned Control Risk- Sales i.e. Identify Key Control

Activities:

Information obtained in understanding internal control is used to assess

control risk. i.e.

Based on the understanding of internal controls, the auditor assesses

how much they can rely on controls to prevent or detect errors. This

influences how much substantive testing is needed.

Make a preliminary control risk assessment (low, moderate, high)

There are four essential steps:

26.

There are fouressential steps:

1. The auditor needs a framework for assessing control risk. The framework for

all classes of transactions is the six transaction-related audit objectives The

six transaction-related audit objectives serve as a framework to ensure

transactions are valid, complete, accurate, properly classified, and recorded

in the correct period.

2. Identify the key internal controls and weaknesses for sales.

3. Associate the controls and weaknesses identified with the objectives.

4. Assess the control risk for each objective by evaluating the controls and

weaknesses for each objective.

27.

Example of controls:

1.Adequate Separation of Duties

Segregation of Duties :Different employees handle sales orders, shipping, and

invoicing.

Separation of duties reduces the risk of:

• Fraud (e.g., embezzlement, fictitious sales)

• Concealment (if one person does everything, they can cover up mistakes or

fraud)

Person responsible for inputting sales and cash receipts transaction

information into the computer vs. person having access to cash.

Credit granting function vs. the sales function (to minimize the sales people

tendency to optimize volume even at the expense of high bad debt write-offs).

Personnel responsible for doing internal comparisons vs. those entering the

original data.

28.

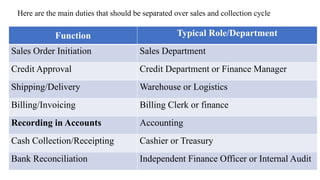

Here are themain duties that should be separated over sales and collection cycle

Function Typical Role/Department

Sales Order Initiation Sales Department

Credit Approval Credit Department or Finance Manager

Shipping/Delivery Warehouse or Logistics

Billing/Invoicing Billing Clerk or finance

Recording in Accounts Accounting

Cash Collection/Receipting Cashier or Treasury

Bank Reconciliation Independent Finance Officer or Internal Audit

29.

2. Proper Authorization

Authorization means approval of sales orders before processing.

Three key points of authorization

Credit must be properly authorized before sales takes place,

Goods should be shipped only after proper authorization, and

Price, including freight and discount, must be properly approved- to

ensure sales is billed at the price set by company policy.

30.

3. Adequate Documentsand Records

Documents and records used must be adequate.

Should contain sufficient information.

Most companies automatically prepare a multi-copy prenumbered sales invoice at

the time the customer places an order. –Useful for minimizing the chance of failure

to bill the customer if all invoices are accounted for periodically.

Use of prenumbered documented prevents both the failure to bill or record sales

and the occurrence of duplicate billings and recordings. i.e. Use of pre-numbered

sales invoices to prevent missing transactions

31.

4. Monthly Statements/Reconciliation

Matchingsales records with shipping documents and bank deposits.

Sent by someone having no responsibility for handling cash or preparing

the sales and A/R records.

Encourages response from customers if the balance is improperly stated.

All disagreements about the balance in the account should be directed to

the independent designated official.

32.

5. Internal VerificationProcedure

For fulfilling each of the six transaction related audit objectives,

a computer program or an independent person check the

processing and recording of sales. e.g.

accounting for numerical sequence of prenumbered documents,

Checking the accuracy of document preparation.

Reviewing reports for unusual or incorrect items.

33.

Step 3: SelectControl Tests:

•Observation: Watching employees perform sales transactions.

•Inspection: Reviewing sales documents for manager approvals.

•Reperformance: Recalculating discounts or credit limits to verify

system accuracy.

•Inquiry: Asking sales personnel about procedures for approving

orders.

Step 4: Evaluate Control Effectiveness:

•If controls are effective, the auditor may reduce substantive testing.

•If controls are weak, substantive tests of transactions are increased.

34.

II: Designing SubstantiveTests of Transactions for Sales

Substantive tests of transactions are audit procedures used to verify the

monetary accuracy of transactions recorded in the accounting records.

Substantive tests of transactions aim to detect misstatements in sales

transactions.

Understanding the substantive tests of transactions for sale is crucial in

the auditing process. These tests are designed to uncover any monetary

misstatements with in sales transaction and are influenced by the

company’s internal controls and related audit objectives

• The procedures vary depending on the circumstances and often require

careful auditor’s judgement, especially when internal controls are deemed

inadequate.

35.

Steps in DesigningSubstantive Tests of Transactions:

Step 1:Identify Key Assertions at Risk (The Six Transaction-Related Audit

Objectives)

i. Occurrence: Sales recorded actually took place.

ii. Completeness: All sales are recorded.

iii. Accuracy: Sales amounts are correctly calculated.

iv. Cutoff: Sales are recorded in the correct period.

v. Classification: Sales are recorded in the right accounts.

vi. Posting & Summarization: Trace sales from journal to general

ledger to verify correct account posting.

Let us see one by one:

36.

i. Recorded SalesExist (Occurrence Assertion)

All sales transactions recorded in the accounting records actually

happened in reality. I.e.

The sales it reports in the financial statements are genuine and

supported by documents.

For this objective, the auditor is concerned with the possibility of three

types of misstatements:

a) Sales being included in the journals for which no shipment was made,

b) Sales recorded more than once, and

c) Shipments being made to nonexistent customers and recorded as sales

37.

a) Recorded Salesfor which there was no Shipment

Trace selected entries from the sales journal to make sure that related copies

of the shipping and other supporting documents exist.

If the possibility of fictitious duplicate copy of a shipping document, trace

amounts to the perpetual inventory records.

Trace the credit in the A/r master file to its source- if collected or goods

returned, there must originally have been a sale. If credited for bad debt or if

the account was still unpaid, intensive follow-up by examining shipping

documents and customer order docs.

38.

b) Sales RecordedMore than Once

Duplicate sales can be determined by reviewing a numerically sorted list of

recorded sales transactions for duplicate numbers.

Also test proper cancellation of shipping documents.

c) Shipment Made to Nonexistent Customers

Can occur only when the person recording sales is also in a position to

authorize shipments.

If controls are weak, it is difficult to detect.

39.

Sales is oneof the highest-risk areas for misstatement due to:

• Pressure to meet revenue targets

• Incentives like performance bonuses

• Desire to show business growth to investors or lenders

Common risks related to the occurrence assertion include:

• Fictitious sales recorded near year-end to inflate revenue

• Recording duplicate sales

• Posting of sales without proper shipment or customer

approval

• Creating fake customers or invoices

40.

ii. Existing SalesTransactions are Recorded ( completeness)

All sales transactions that actually happened have been fully recorded in

the accounting system. i.e. No real sales are left out or missed.

Normally, substantive test for completeness is less emphasized.

If real sales are not recorded:

• Revenue is understated

• Accounts receivable may be understated

• Financial statements become misleading

Common risks of incompleteness in sales include:

• Manual invoices that are not entered into the system

• Unauthorized deliveries without documentation

41.

Direction of Testingactivities

Tracing from source documents to the journals-

a test for omitted transactions- Completeness Objective…likely starting

point could be a shipping doc…a sample selected and traced to sales

invoices and sales journal.

Tracing from the journals back to source documents-

a test for nonexistent transactions- existence objective….likely starting

point could be the journal… a sample of invoice numbers is selected from

the journals and traced to duplicate sales invoices, shipping docs, and

customer orders.

42.

iii. Sales areAccurately Recorded

Accurate recording of sales - shipping the amount of goods ordered,

accurate billing for the amount of goods shipped, and accurately recording

the amount billed.

Typical substantive tests include: Recomputing information in the

accounting records

Start with entries in the sales journal to compare the total of selected

transactions with A/R master file entries & duplicate sales invoices.

Compare prices on the duplicate sales invoices with an approved price

list,

Recompute extensions and footings

43.

Compare detailslisted on the invoices with shipping records for description,

quantity, and customer identification

When sales invoices are automatically calculated and posted by a

computer, the auditor may be able to reduce substantive tests of

transactions for the accuracy objective.

If the auditor determines that the computer is programmed accurately and

the price list master file is authorized and correct, detailed invoice

calculations can be reduced or eliminated. In this case, the focus will be on

determining if effective computer controls exist.

44.

iv. Sales arerecorded on the correct dates (Cut-off Assertion )

The cutoff assertion ensures that transactions are recorded in the correct

accounting period. It is particularly important at the end of a reporting

period to prevent early or late recognition of revenue or expenses.

Sales should be billed and recorded as soon after shipment takes place

as possible to prevent the unintentional omission of transactions from

the records and to make sure that sales are recorded in the proper

period.

45.

Importance of CutoffTesting

1.Prevents Misstated Financial Statements – If sales or expenses are recorded

in the wrong period, financial statements will be misleading.

2.Ensures Compliance with Accounting Standards – GAAP and IFRS

require proper revenue and expense recognition.

3.Detects Revenue Manipulation (Fraud Risk) – Companies may shift

revenue to inflate earnings in a given period.

4.Affects Profitability Analysis – Incorrect timing of transactions can distort

financial ratios and performance evaluation.

46.

V. RECORDED SALESARE PROPERLY CLASSIFIED

The key idea, Sales must be posted to the correct account,

department, product line, or cost center based on their

nature.

Sales of cash vs. credit sales

Exclude sales of operating assets such as machinery

Use of more than one sales classification…..

Regular/domestic sale, export sale, installment sale…

Incorrect classification leads to:

Misleading financial statements

Wrong segment reporting

47.

This objective ensuresthat sales transactions are accurately

transferred (posted) from: Sales journals to the general ledger,

and Summarized correctly in the financial statements

Sales Transactions are Properly Included in the Master File and

Correctly Summarized, b/se the accuracy of these records affect’s

the client’s ability to collect outstanding receivables.

The sales journal must be correctly totaled and posted to the GL

Perform clerical accuracy tests such as footing the journals and

tracing the totals and details to the GL and the master file to check

whether there are misstatements.

VI. Posting & Summarization

48.

Step 2. SelectSubstantive Testing Procedures:

Vouching: Select recorded sales and match them with supporting

documents (e.g., invoices, shipping records). i.e. verifies transactions

by examining supporting documents

Tracing: Select shipping documents and trace them to sales records

to ensure completeness.

Recalculation: Verify invoice totals, discounts, and tax calculations.

Analytical Procedures: Compare monthly sales trends to prior years

or industry benchmarks.

Step 3. Perform Substantive Tests:

Use sampling techniques to verify transactions.

Investigate unusual or large transactions.

Compare recorded sales with cash receipts and customer

confirmations.

49.

Exercises

1. Invoice showsa sale of 5,000 bottles of energy drink to a new customer

“Bright Trade Plc.” No delivery note, no customer order, no payment

received. What assertion is at risk?

Occurrence, This could be a fictitious sale recorded to boost end-of-

year revenue.

2. A customer was billed ETB 14,000 instead of the correct ETB 12,000 due to

an error in applying a 10% discount. Which assertion is most relevant?

Accuracy

3. A sale of imported wine is mistakenly recorded under local beer revenue.

Which audit objective does this violate?

Classification

50.

4. Goods wereshipped to a customer on January 2, 2025, but the

invoice was dated and recorded on December 31, 2024. Which assertion

is impacted?

Cut-off

5. Imagine a company where sales are manually entered. A delivery is

made to a regular customer, but the salesperson forgets to prepare an

invoice. Which audit objectives are likely violated?

Completeness and accuracy

6. The sales journal total for the week is ETB 580,000, but only ETB

550,000 was posted to the general ledger. Which objective is impacted?

Posting & Summarization

51.

7 Auditor findsthat sales invoices are generated manually, and many

shipping documents are missing. Sales are still being recorded based on

sales manager’s verbal confirmation.

What are the potential assertions at risk?

Occurrence – No evidence the sale actually took place.

Completeness – Manual records may omit some real transactions.

Accuracy – Without supporting docs, amounts may be incorrect.

52.

Iv. Methodology forDesigning Tests of Controls and Substantive

Tests of Transactions for Cash Receipts

The same methodology used for designing tests of controls and substantive tests of

transactions for sales is used for cash receipts.

Cash receipts tests of controls and substantive tests of transactions audit procedures

are developed around the same framework used for sales.

Key internal controls for each objective are determined, tests of controls are developed

for each control, and substantive tests of transactions for the monetary misstatements

related to each objective are developed.

The tests of controls depend on the controls the auditor has identified and the extent

they will be relied on to reduce assessed control risk.

An essential part of the auditor’s responsibility in auditing cash receipts is

identification of weaknesses in internal control that increase the likelihood of fraud.

53.

Determine Whether CashReceived was Recorded

It is difficult to detect a cash fraud occurred before the cash is recorded in the

cash receipt journal or other cash listing.

Internal controls designed to satisfy completeness objective are important.

Trace from prenumbered remittance advices or prelists of cash receipts to

the cash receipt journal and subsidiary A/R records as a substantive tests of

the recording of the actual cash received… effective only if a cash register

tape or some other prelisting was prepared at the time cash was received

54.

Prepare Proof ofCash

A useful audit procedure to test whether all recorded cash receipts have

been deposited in the bank account.

Total cash receipts recorded in the journal vs. actual deposits made during

the month…

Helps to detect recorded cash receipts that haven’t been deposited,

unrecorded deposits, unrecorded loans, bank loan deposited directly into the

bank account etc.

Can not help to detect cash receipts that have not been recorded inn the

journals or time lags in making deposits.

Performed only when controls are weak.

55.

Test to DiscoverLapping of A/R

Lapping of A/R is the postponement of entries for the collection of receivables

to conceal an existing cash shortage.

The defalcation is perpetrated by a person who handles cash receipts and then

enters them into the computer system.

Involves differing recording the cash receipts from one customer and covers

the shortage with receipts of another. This in turn is covered from the receipts

of a third customer few days later.

Prevention…. Separate duties and mandatory vacation policy for employees

who both handle cash and enter cash receipts into the system.

Detection… Compare the name, amount, and dates shown on remittance

advices with cash receipts journal entries and related duplicate deposit slips.

![[SAPP Academy] Tóm tắt kiến thức quan trọng môn FAF3 ACCA.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/sappacademytomtatkienthucquantrongmonfaf3acca-240701084356-d95bfac0-thumbnail.jpg?width=640&height=640&fit=bounds)