2

INTRODUCTION

Accounts receivable ispart of the "current assets“ section on a company's

balance sheet.

It represents the balance owed by customers for products sold or services

rendered.

For small businesses that sell on credit, this account can represent a large

portion of its current assets.

In many companies, individual transactions are small and frequent.

As such, there is ample opportunity for errors in prices and dates that could

leave accounts receivable misstated.

Audits can help clear up these errors.

Auditors typically follow a standard set of procedures when it comes to

auditing accounts receivable.

3.

3

Sources of AccountsReceivable

Claims against customers from sale

of goods

Loans to officers or employees

Loans to subsidiaries

Claims against various other

refunds

Claims for tax refunds

Advances to suppliers

Sources of Notes Receivable

Written promises to pay certain

amounts at future dates

Notes for substantial amounts

Installment note or contract can

allow seller to hold lien (right) on

goods

•Examples:

Sale of industrial machinery, farm

equipment

Issuance of capital stock

4.

4

2.1. SOURCES ANDNATURE OF RECEIVABLE

The sales and collection cycle involves the decisions and

processes necessary for the transfer of the ownership of goods

and services to customers after they are made available for

sale.

It begins with a request by a customer and ends with the

conversion of material or service into an account receivable,

and ultimately into cash

Receivables from customers include both accounts receivable

and various types of notes receivable.

It is important to differentiate the origin and nature of

receivables to ensure their appropriate classification and

valuation.

5.

5

What is theSales and Collection Cycle?

• Also known as the Revenue, Receivables, and Receipts

(RRR) Cycle.

• Journal entries that debit accounts receivable and credit

sales revenue, and debit cash and credit accounts

receivable, respectively.

2.1.Overview of the cycle

7

Why Are RevenueCycle Accounts Important?

Sales transactions are always material to a company's

financial statements

According to the SEC, a majority of financial statement

manipulations and audit failures involve overstated

revenues

Therefore, revenue cycle accounts must be examined with

great care

8.

8

• The revenuecycle involves the process of

Receiving a customer’s order,

Approving credit for a sale,

Determining whether the goods are available for shipment,

Shipping the goods, billing the customer,

Collecting cash, and

Recognizing the effect of this process on other related

accounts such as accounts receivable, inventory, and sales

commission expense

In the revenue cycle, the most significant accounts include revenue and

accounts receivable. The auditor will likely obtain evidence related to each

of the financial statement assertions

9.

9

The process usuallybegins when a customer approaches

the company and files a customer purchase order

The sales department receives the document and prepares

a sales order that is then sent to the credit department for a

credit check.

Remember that salespeople will not perform credit checks

because their position as a salesperson may influence their

bias when making credit decisions on customers. This

separation is called segregation of duties.

10.

10

Once the creditdepartment approves the customer and the

order, the sales order is sent to the shipping department,

which will generate a shipping document, also referred to

as a bill of lading or a waybill.

The approved sales order and the shipping document are

then sent to the accounts receivable clerk, who then

generates a sales invoice and makes the necessary journal

entry.

Finally, once the cash is received from the customer,

accounting or treasury records the credit to cash and debits

the balance in accounts receivable.

11.

11

2.2. KEY INTERNALCONTROL OF SALES AND RECEIVABLES

2.2.1 Internal Controls for Sales Class of Transactions

There are five applicable assertions: cut-off, classification, completeness,

occurrence, and accuracy.

Occurrence assertion is that each sales transaction is supported by the

necessary documents, such as the approved sales order, shipping

documents, and invoice.

Completeness assertion, shipping documents are typically sequentially pre-

numbered so that any duplicate transaction or a missing transaction can be

12.

12

2.2.2 Internal Controlsfor Cash Receipts

• Some internal controls for the cash receipts class include

the segregation of duties between the cash handler and

the record-keeper, and monthly bank reconciliations.

• These two controls pertain mainly to the occurrence

assertion.

• In terms of the completeness assertion, monthly customer

statements are a strong control, as well as the use of

remittance invoices or pre-listing of cash, and the

reconciliation of the documents with deposit slips.

13.

13

2.2.3. The objectivesof internal controls over receivables

are to ensure:

All goods dispatched/Shipped are invoiced.

Invoicing is at correct price and discount.

Goods are only dispatched on credit to approved customers.

Invoices are recorded and related to subsequent cash

receipts.

Receivables are controlled and bad debts pursued.

Credit notes approved.

14.

14

INTERNAL CONTROL OFSALES AND RECEIVABLES

In addition the internal control over receivables, there

should be such that the possibility of any falsification of

the receivables accounts is eliminated.

An important part of the controls would be to ensure

that the cashier does not have access to the sales

ledger, and the sales ledger clerk does not have access

to cash received.

15.

15

Internal Control procedures,over sales and receivables include

the following.

Orders

The orders should be checked against the customer’s account

All orders received should be recorded on pre- numbered sales order

documents.

All orders should be authorized before goods are dispatched.

Dispatch

-Dispatch notes should be pre-numbered and a register kept of

them to relate to sales invoices and orders.

-Goods dispatch notes should be authorized as goods leave.

16.

16

Control procedures, oversales and receivables include the following.

Invoicing

- Sales invoices should be authorized by a responsible official.

- Sales invoices should be checked for prices and calculations by a

person other than the one preparing the invoice.

- All invoices should be pre-numbered consecutively.

- Copies of cancelled invoices should be retained/booked.

17.

17

Control procedures Contin…

Receivables.

-A receivable ledger control account should be prepared and checked to individual sales ledger

balances.

- Receivables ledger personnel should be independent of dispatch and cash receipt functions.

- Statements should be sent regularly to customers.

Bad Debts.

- The authority to write off a bad debt should be given in writing and adjustments made to

the accounts receivable ledger.

- The use of court action or write-off of a bad debt should be authorized by an official

independent of the cash receipts function.

19

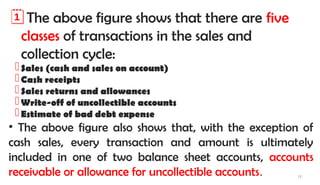

The above figureshows that there are five

classes of transactions in the sales and

collection cycle:

Sales (cash and sales on account)

Cash receipts

Sales returns and allowances

Write-off of uncollectible accounts

Estimate of bad debt expense

• The above figure also shows that, with the exception of

cash sales, every transaction and amount is ultimately

included in one of two balance sheet accounts, accounts

receivable or allowance for uncollectible accounts.

20.

20

The Classes ofTransactions, Accounts, Business functions, and related

Documents and Records for the Sales and Collection Cycle.

1. SALES TRANSACTION

Accounts

Sales

Accounts receivable

Business Functions

Processing customer orders, - Customer places an order using

Customer Order document.

This is often followed by the issuance of Sales Order.

Granting credit- a properly authorized person must approve credit to

the customer for sales on account.

•

21.

21

Minimizes the possibilityof bad debts.

• It may be a programmed approval- based on

preapproved credit limit maintained in a customer master

file.

Shipping goods

• A point at which most companies recognize sale.

• A shipping document is prepared.

• The shipping document may be a multi copy bill of

lading.

• Update perpetual inventory record.

22.

22

Billing customers andrecording sales- Billing is a means by which the

customer is informed of the amount due for the goods.

• All shipments should be billed and no shipment should be billed

more than once.

• Billing should consider authorized price, quantity shipped and other

terms.

Done with multi copy sales invoice and simultaneously updating of

the sales transaction file, accounts receivable master file, and the general

ledger master file for sales and accounts receivable

23.

23

Documents and Records

Customer Order- a request for merchandise by a customer.

Sales Order- used to communicate the description, quantity and

related specification of goods ordered.

Shipping Document- a document prepared to initiate shipment of goods.

Sales invoice-a document indicating the description and quantity

of goods sold the price, freight charges, insurance, terms, and

other relevant data.

Sales transaction file- a computer generated file that includes all sales

transaction processed by the accounting system for a period.

24.

24

• Sales journalor listing- a report generated from the

sales transaction file that typically includes the customer name,

date, amount, and account classification or classifications

for each transaction, such as division or product line.

• Accounts receivable master file- a file used to record

individual sales, cash receipts, and sales returns and

allowances for each customer and to maintain customer

account balances.

25.

2. SALES RETURNSAND ALLOWANCES TRANSACTION

Accounts

Sales returns and allowances

Accounts receivable

Business Functions

Processing and recording sales returns and allowances

• When a customer is dissatisfied with the goods, the seller often accepts

the returned goods or grants a reduction in the charges.

• It is necessary to issue a Receiving Report and return the goods to store

25

26.

26

• Record thetransaction promptly and accurately on the

Sales and Returns Journal & A/R master file.

• As an aid for control & to facilitate recording Credit

Memos are issued.

Documents and Records

Credit memo- a document indicating a reduction in the amount due

from a customer because of returned goods and allowances granted.

Sales returns and allowances journal- a journal used to

record sales returns and allowances.

27.

27

3. CHARGE-OFF OFUNCOLLECTIBLE ACCOUNTS TRANSACTION

Accounts

1. Accounts receivable

2. Allowance for uncollectible accounts

Business Functions

Charging off uncollectible accounts receivable

• When the company concludes that an amount is no longer collectible, it must be charged off- e.g. if a

customer becomes bankrupt.

Documents and Records

a. Uncollectible account authorization form- a document used initially to indicate authority to write an account

receivable off as uncollectible.

b. General journal

4. CASH RECEIPTS

Accounts : Cash and Accounts Receivable Functions: Recording the accounts &Posting

28.

28

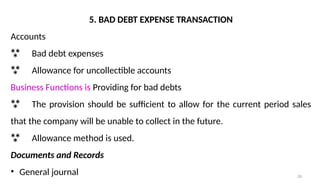

5. BAD DEBTEXPENSE TRANSACTION

Accounts

Bad debt expenses

Allowance for uncollectible accounts

Business Functions is Providing for bad debts

The provision should be sufficient to allow for the current period sales

that the company will be unable to collect in the future.

Allowance method is used.

Documents and Records

• General journal

29.

29

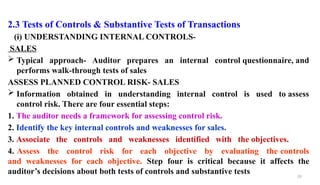

2.3 Tests ofControls & Substantive Tests of Transactions

(i) UNDERSTANDING INTERNAL CONTROLS-

SALES

Typical approach- Auditor prepares an internal control questionnaire, and

performs walk-through tests of sales

ASSESS PLANNED CONTROL RISK- SALES

Information obtained in understanding internal control is used to assess

control risk. There are four essential steps:

1. The auditor needs a framework for assessing control risk.

2. Identify the key internal controls and weaknesses for sales.

3. Associate the controls and weaknesses identified with the objectives.

4. Assess the control risk for each objective by evaluating the controls

and weaknesses for each objective. Step four is critical because it affects the

auditor’s decisions about both tests of controls and substantive tests

30.

30

The following arekey control points auditors will consider in

their evaluation of the internal control system of the client.

Adequate Separation Of Duties

Proper Authorization

Adequate Documents And Records

Prenumbered Documents

Monthly Statements

Internal Verification Procedure

31.

31

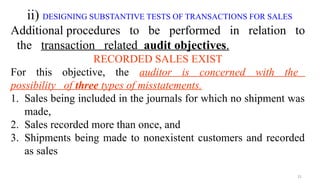

ii) DESIGNING SUBSTANTIVETESTS OF TRANSACTIONS FOR SALES

Additional procedures to be performed in relation to

the transaction related audit objectives.

RECORDED SALES EXIST

For this objective, the auditor is concerned with the

possibility of three types of misstatements.

1. Sales being included in the journals for which no shipment was

made,

2. Sales recorded more than once, and

3. Shipments being made to nonexistent customers and recorded

as sales

32.

32

Methodology for DesigningControls

and Substantive Tests: Sales

Understand internal

control – sales

Assess planned

control risk – sales

Evaluate cost-benefit

of testing controls.

Design tests of controls

and substantive tests

of transactions for sales

to meet transaction-

related audit objectives.

Audit procedures

Sample size

Items to select

Timing

33.

33

Transaction-Related Audit

Objectives forSales

Existence:

Recorded sales are for shipments actually made.

Accuracy:

Recorded sales are for the amount shipped.

Completeness:

Existing sales transactions are recorded.

34.

34

Design Substantive Tests

ofTransactions for Sales

Classification:

Sales transactions are properly classified.

Timing:

Sales are recorded on the correct dates.

Posting and summarization:

Sales transactions are properly included

in the accounts receivable master file.

35.

35

EXISTING SALES TRANSACTIONSARE

RECORDED

Substantive test for completeness is

less emphasized.

But if controls are inadequate, which is likely

if the client does no independent internal

tracing from shipping documents to the sales

journal, substantive testes are necessary.

36.

36

Direction of Testing

Tracing from source documents

to the journals

Tracing from the journals back

to source documents

37.

37

Direction of Testsfor Sales

Customer

order

Shipping

document

Duplicate

sales invoice

Sales

journal

General

ledger

Accounts

receivable

master file

=

Completeness Start

Existence Start

38.

38

SALES ARE ACCURATELYRECORDED

Accurate recording of sales - shipping the amount of

goods ordered, accurate billing for the amount of

goods shipped, and accurately recording the amount

billed.

Typical substantive tests include:

Re computing information in the accounting records

39.

39

RECORDED SALES AREPROPERLY CLASSIFIED

• Sales of cash vs. credit sales

•Exclude sales of operating assets such as machinery

•Use of more than one sales classification….. Regular,

installment

SALES ARE RECORDED ON THE CORRECT DATES

•Sales should be billed and recorded as soon after

shipment takes place as possible to prevent the unintentional

omission of transactions from the records and to make sure that

sales are recorded in the proper period.

40.

40

SALES TRANSACTIONS AREPROPERLY INCLUDED

IN THE MASTER FILE AND CORRECTLY

SUMMARIZED

Needed b/c the accuracy of these records affect’s

the client’s ability to collect outstanding

receivables.

The sales journal must be correctly totaled and

posted to the GL

41.

41

METHODOLOGY FOR DESIGNINGTESTS OF

CONTROLS AND SUBSTANTIVE TESTS OF

TRANSACTIONS FOR CASH RECEIPTS

• The same methodology used for designing tests of

controls and substantive tests of transactions for sales is used

for cash receipts.

• An essential part of the auditor’s responsibility in auditing

cash receipts is identification of weaknesses in

internal control that increase the likelihood of fraud.

42.

42

2.4 TESTS OFDETAILS OF BALANCES

METHODOLOGY FOR DESIGNING TESTS OF DETAILS OF BALANCES

Deciding the appropriate tests of details

of balances evidence is complicated because

it must be decided on an objective-by-objective

basis, and there are several interactions

that affect the evidence decision.

43.

43

In designing testsof details of balances for accounts receivable, it is

essential to satisfy each of the nine balance-related audit objectives.

Existence

Completeness

Accuracy

Classification

Cutoff

Realizable value

Rights and obligations

Valuation and allocation

Presentation and disclosure

44.

FINANCIAL REPORTING STANDARDS

•Financial reporting standards for receivables require:

separation of trade from non – trade receivables.

assurance of ownership disclosure.

assurance of collectability of receivables.

assurance of consideration for returns and allowances.

appropriate classification of current and non - current.

45.

AUDIT OBJECTIVES OF:

theaudit of the sales and collection cycle

• The audit objectives for the receivables and sales relate to obtain to

sufficient competent evidence about each significant financial statement

assertion that pertains receivables and sales transactions and balances.

• To achieve each of these specific audit objectives, the auditors employ

various parts of the audit planning and audit testing methodology.

The overall objective in balances affected by the cycle are fairly presented

in accordance with accounting standards (IFRS).

46.

The auditors’ objectivesin the examination of receivables and sales

are:

To consider internal control over receivables and sales transactions.

To determine the existence of receivables, the clients ownership of these

assets, and the occurrence of sales transactions.

To establish the completeness of receivables and sales transactions.

To establish the clerical accuracy of records and supporting schedules of

receivables and sales.

To determine that the valuation of receivables is at appropriate net

realizable values.

To determine that the statement presentation of receivables and sales is

adequate.

47.

Assertion

Category

Transaction class

Audit objective

Accountbalance

Audit objective

Category Existence

or Occurrence

Recorded sales transactions represent

goods shipped during the period.

Recorded cash receipts transactions

represent cash received during the period.

Accounts receivable include all

amounts owed by the customers exists

at the balance sheet date.

Completeness

All sales, cash receipts sales adjustments

that occurred during the period have been

recorded.

Accounts receivable include all claims

on customers at the balance sheet date.

Rights and

Obligations

The entity has rights to the receivables and

cash resulting from sales transactions.

Accounts receivable at the balance sheet

date represents legal claims of the

entity.

Valuation

All sales, cash receipts and sales

adjustments transactions are correctly

journalized, summarized, and posted.

Accounts receivable represent gross

claims, On customers at the balance

sheet date. The allowance for

uncollectible accounts represent a

reasonable estimate.

Presentation ad

disclosure

The details of sales, cash receipts and sales Accounts receivables are properly

identified and classified.

48.

AUDIT PROGRAM FORRECEIVABLES AND SALES

TRANSACTIONS

• The following audit procedures are typical of the work done in the

verification of notes, accounts receivable, and sales transaction.

A.) Consider internal control for receivables and sales.

Obtain an understanding of internal control for receivables and

sales.

The auditors’ consideration of internal controls over receivables

and sales may begin with the preparation of a written narrative or

flow chart and the completion of an internal control questionnaire.

49.

As the auditors’confirm their understanding of the sales and

collection cycle, they will observe whether there is appropriate

segregation of duties, and enquire as to who performed various

functions throughout the year.

Assess control risk and design additional tests of controls for

receivables and sales. After obtain an understanding of the

client’s internal control for receivables and sales transactions, the

auditors perform their initial assessment of control risk for the

variant financial statement assertions.

50.

Perform additional testsand controls: Tests directed

towards the effectiveness of control that help to evaluate

the client’s internal control, and

*determine the extent to which the auditors are justified

in reducing their assessed levels of control risk for the

assertion about the receivables and sales accounts.

51.

The following areexamples of additional tests:

1. Examine significant aspects of a sample of sales transactions.

2. Compare a sample of shipping documents to related sales

invoices.

3. Review the use and authorization of credit memoranda.

A credit memo indicates a reduction in the amount due from a

customer because of returned goods or an allowance.

It often takes the same general form as a sales invoice, but it

supports reductions in accounts receivable rather than increases

4. Reconcile selected cash register tapes and sales invoices with sales

journals.

52.

B) Substantive tests

1.Obtain an aged trail balance of trade accounts receivable and analyses of

other accounts receivable and reconcile to ledgers. When trial balances or

analyses of accounts receivable are furnished to the auditors by the client’s

employees, some independent verification of the listings is essential.

2. Obtain analyses of notes receivable and related interest.

3. Inspect notes on hand and confirm those not on hand with holders.

4. Confirm receivables with debtors.

5. Receive the year-end cutoff/limit of sales transactions.

53.

6. Perform analyticalprocedures for accounts receivable, sales, notes

receivable, and interest revenue.

7. Verify interest earned on notes and accrued interest receivable.

8. Evaluate the propriety/ appropriate of the client’s accounting for

receivables and sales.

9. Determine adequacy of allowance for uncollectible accounts.

10. Ascertain whether any receivables have been pledged/promised.

11. Investigate fully any notes or accounts receivable from related

parties.

12. Evaluate financial statement presentation and disclosure.