This document discusses economic concepts related to equilibrium, including:

- Equilibrium price is where quantity demanded equals quantity supplied

- Equilibrium quantity is the quantity where demand and supply are equal at a given price

- Equilibrium state is when there are no economic pressures from excess demand or supply

- Disequilibrium state is when there is a surplus or shortage in the market

It also defines consumer surplus as the benefit consumers receive from purchasing below the maximum price they would be willing to pay, and producer surplus as the benefit sellers receive from selling above the minimum price they would be willing to accept.

WARM UP:

1.Write your name on the small piece of paper

on your desk.

!

2. When I say “GO” - find 4 different partners:

sign your names on each other’s paper next to

one of the keywords: “opportunity cost,”

“incentive,” and “demand.”

!

* You are not allowed to trade signatures with

someone sitting next to you!

3.

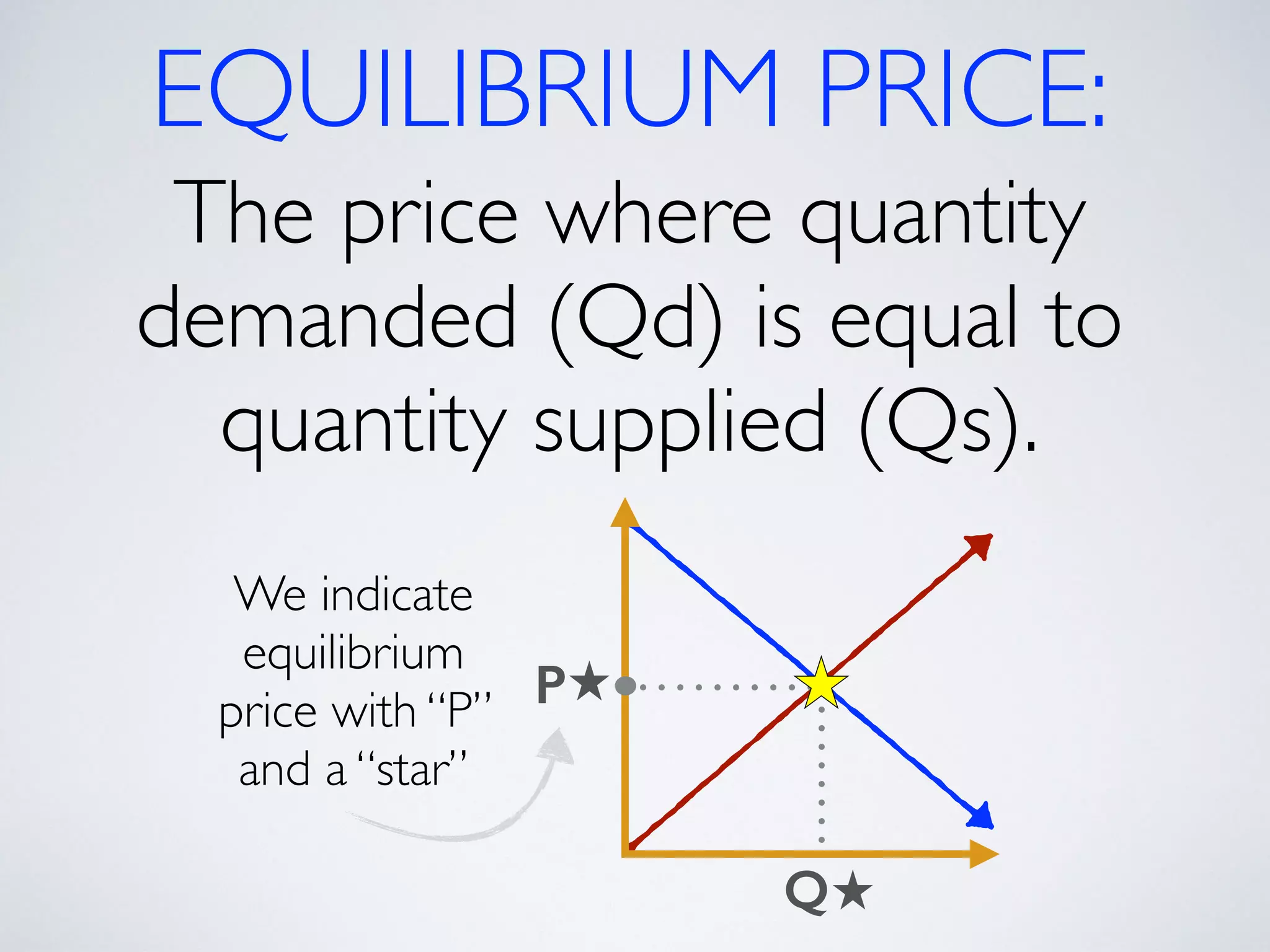

EQUILIBRIUM PRICE:

Theprice where quantity

demanded (Qd) is equal to

quantity supplied (Qs).

Q

P

We indicate

equilibrium

price with “P”

and a “star”

4.

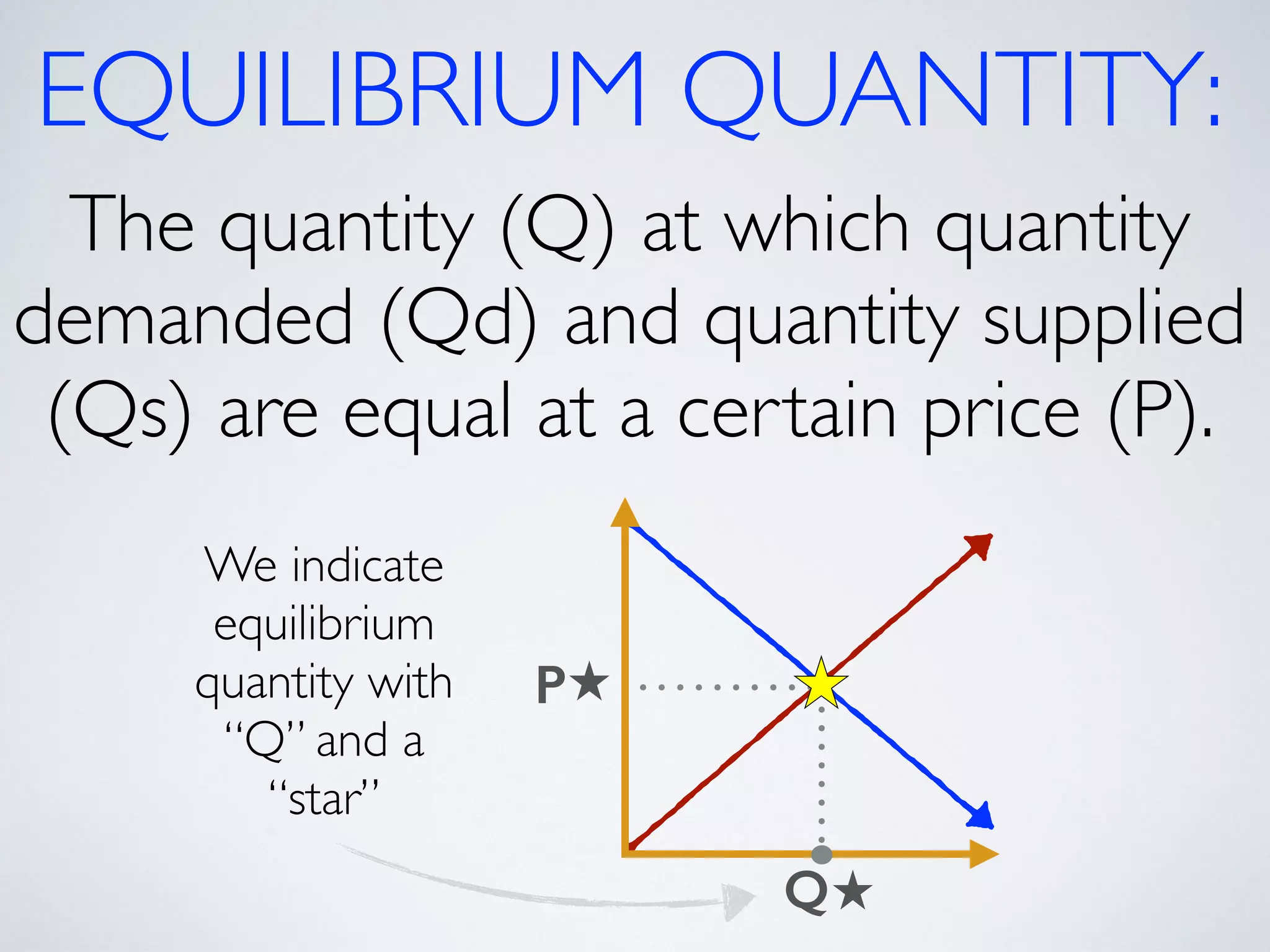

EQUILIBRIUM QUANTITY:

Thequantity (Q) at which quantity

demanded (Qd) and quantity supplied

(Qs) are equal at a certain price (P).

Q

P

We indicate

equilibrium

quantity with

“Q” and a

“star”

5.

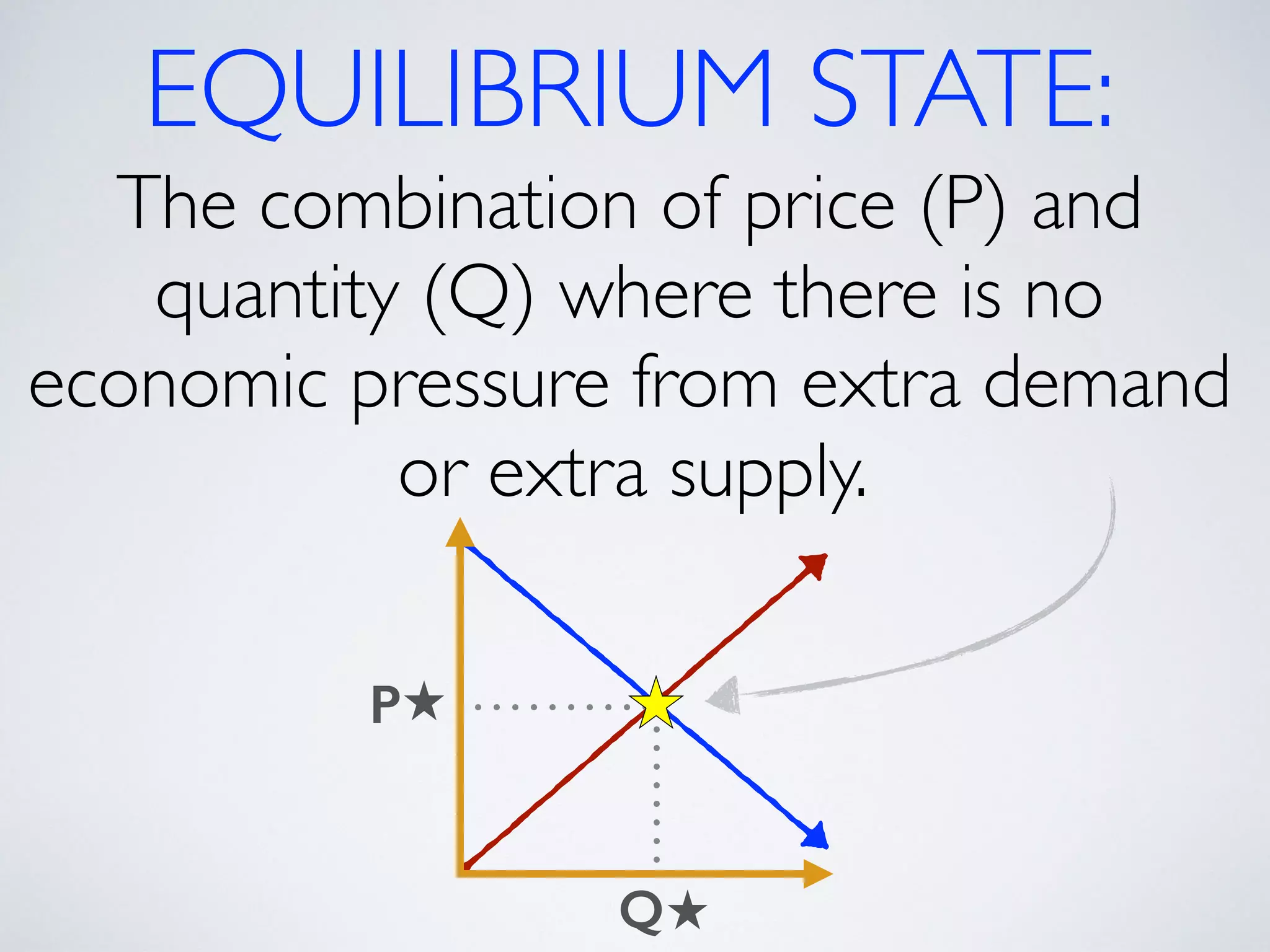

EQUILIBRIUM STATE:

Thecombination of price (P) and

quantity (Q) where there is no

economic pressure from extra demand

or extra supply.

Q

P

6.

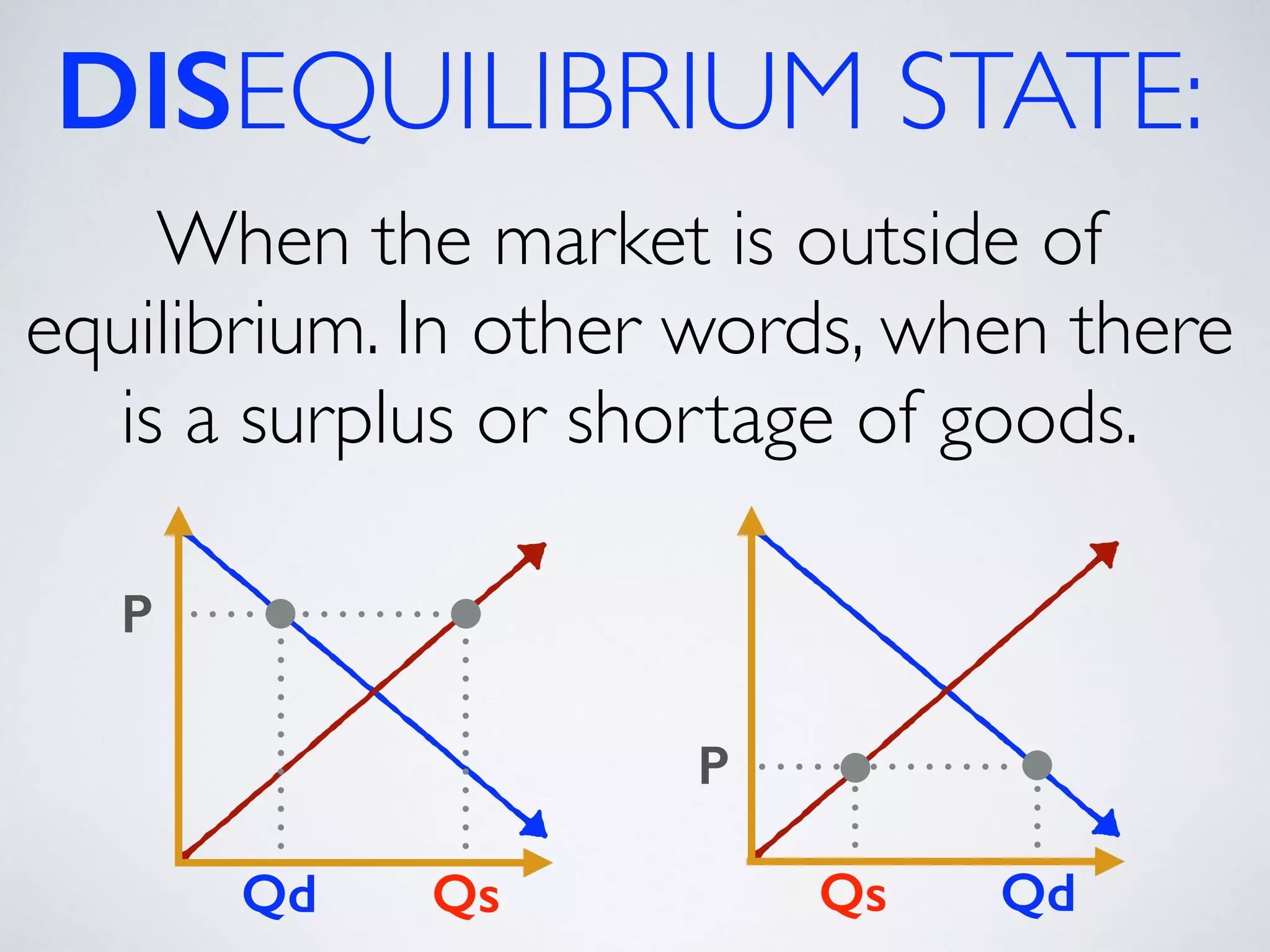

DISEQUILIBRIUM STATE:

Whenthe market is outside of

equilibrium. In other words, when there

is a surplus or shortage of goods.

Qs

P

P

Qd Qs

Qd

7.

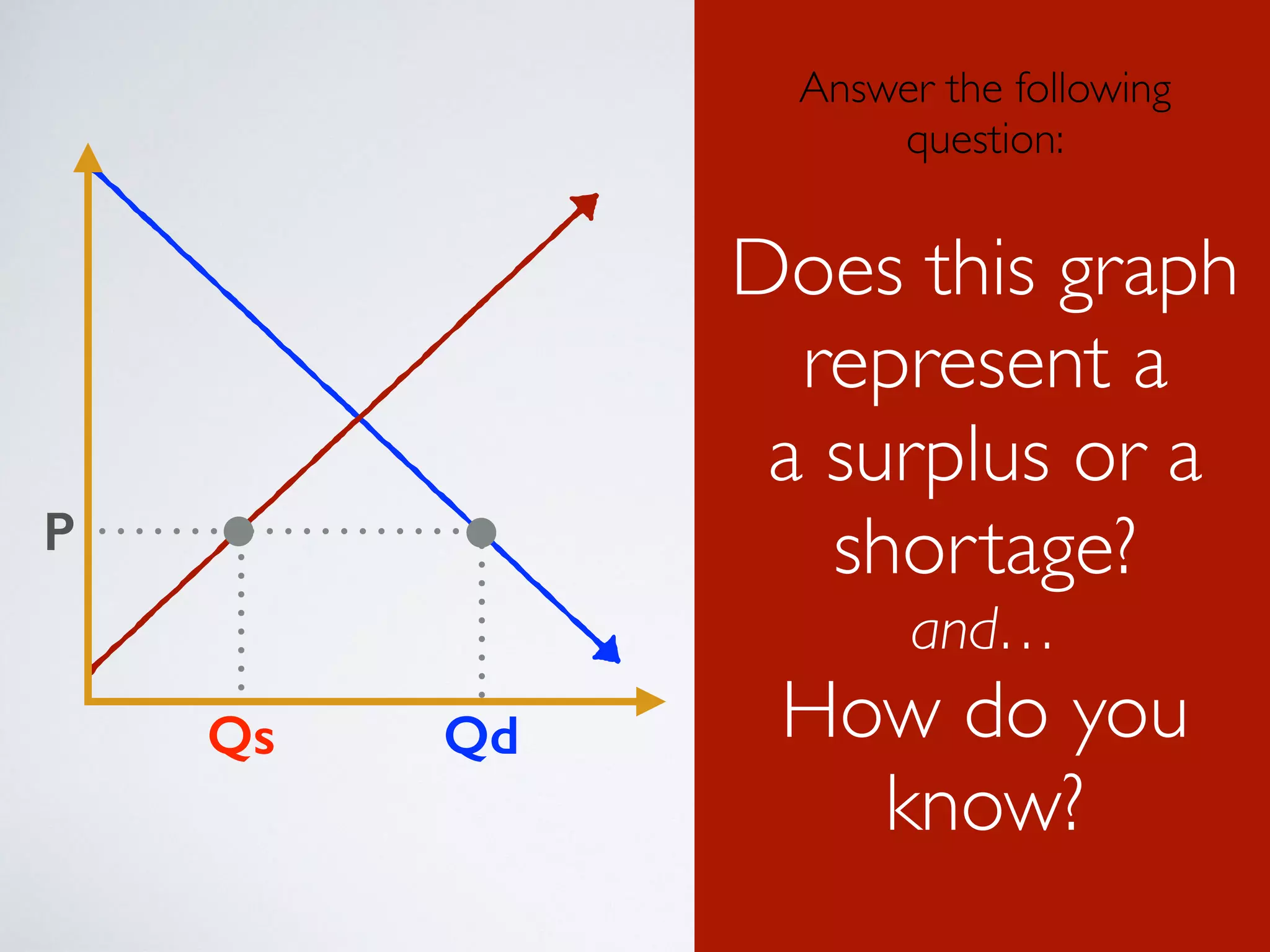

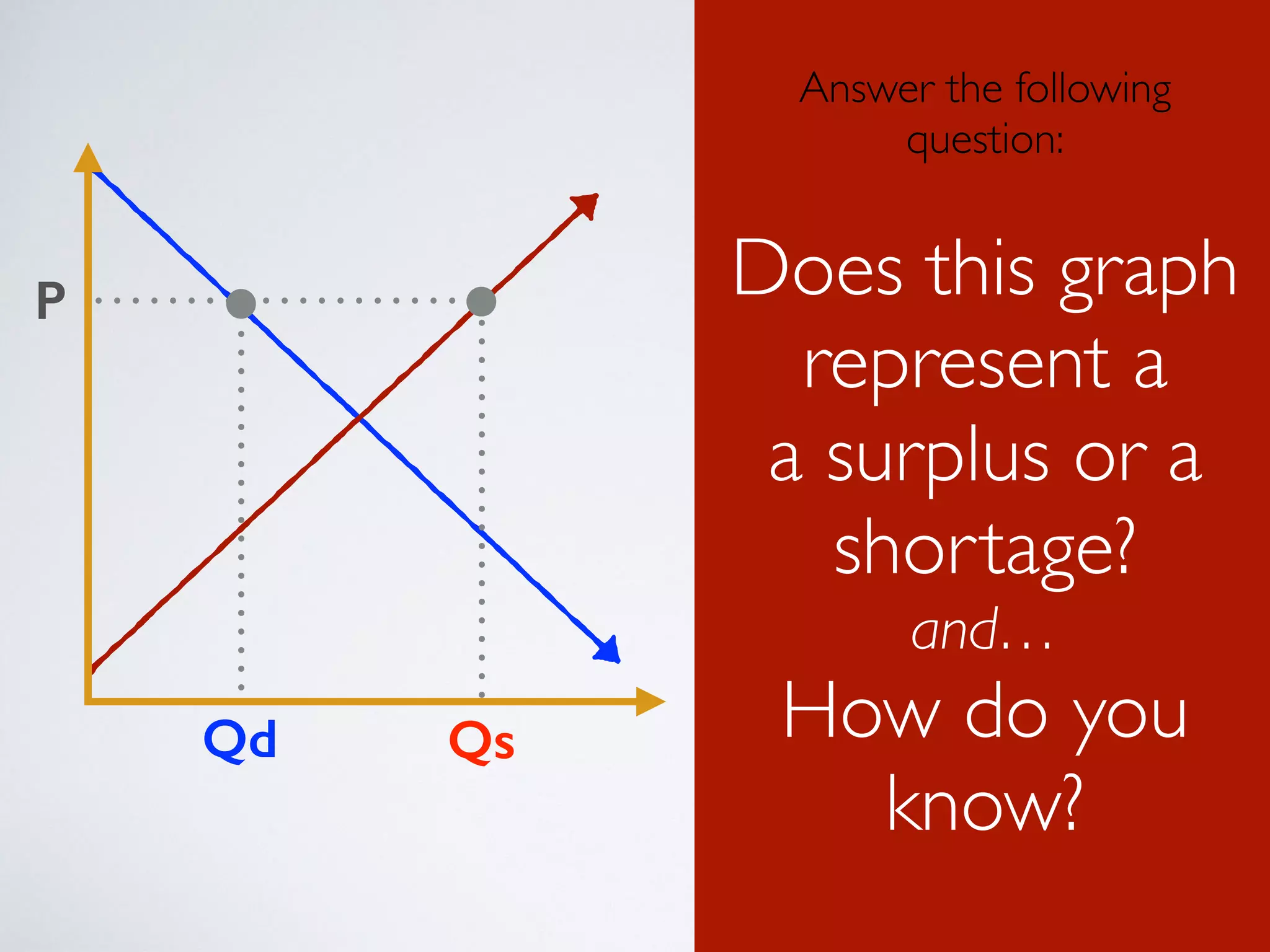

Qs

P

Qd

Answer the following

(Don’t answer question:

out loud!)

Does this graph

represent a

a surplus or a

shortage?

Does this graph

represent a

a surplus or a

shortage?

and…

and…

How do you

know?

How do you

know?

8.

Qs

P

Qd

Answer the following

(Don’t answer question:

out loud!)

Does this graph

represent a

a surplus or a

shortage?

and…

How do you

know?

9.

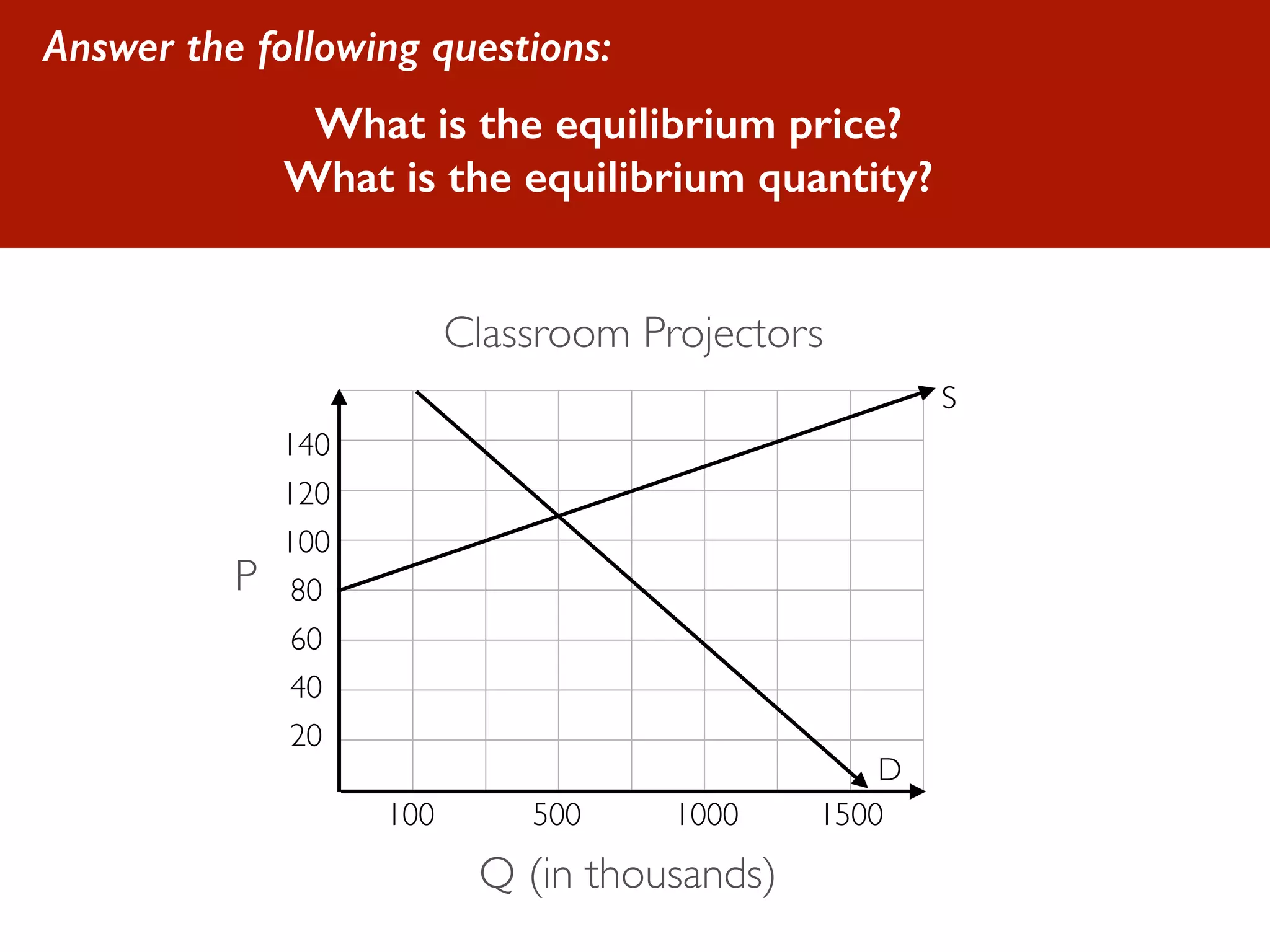

Answer the followingquestions:

Classroom Projectors

140

120

100

80

60

40

20

100 500 1000 1500

S

D

Q (in thousands)

P

What is the equilibrium price?

What is the equilibrium quantity?

10.

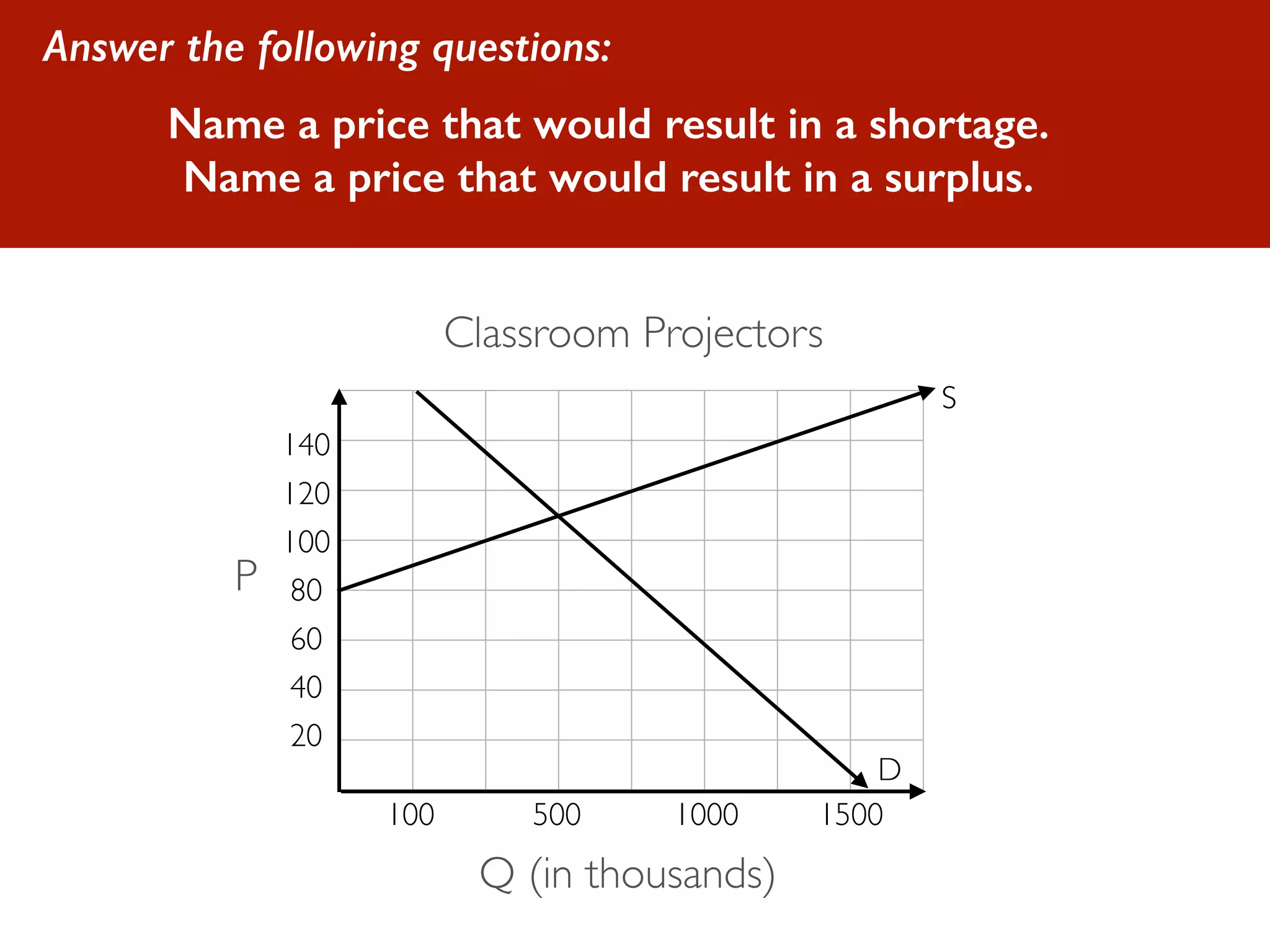

Answer the followingquestions:

Name a price that would result in a shortage.

Name a price that would result in a surplus.

Classroom Projectors

140

120

100

80

60

40

20

100 500 1000 1500

S

D

Q (in thousands)

P

11.

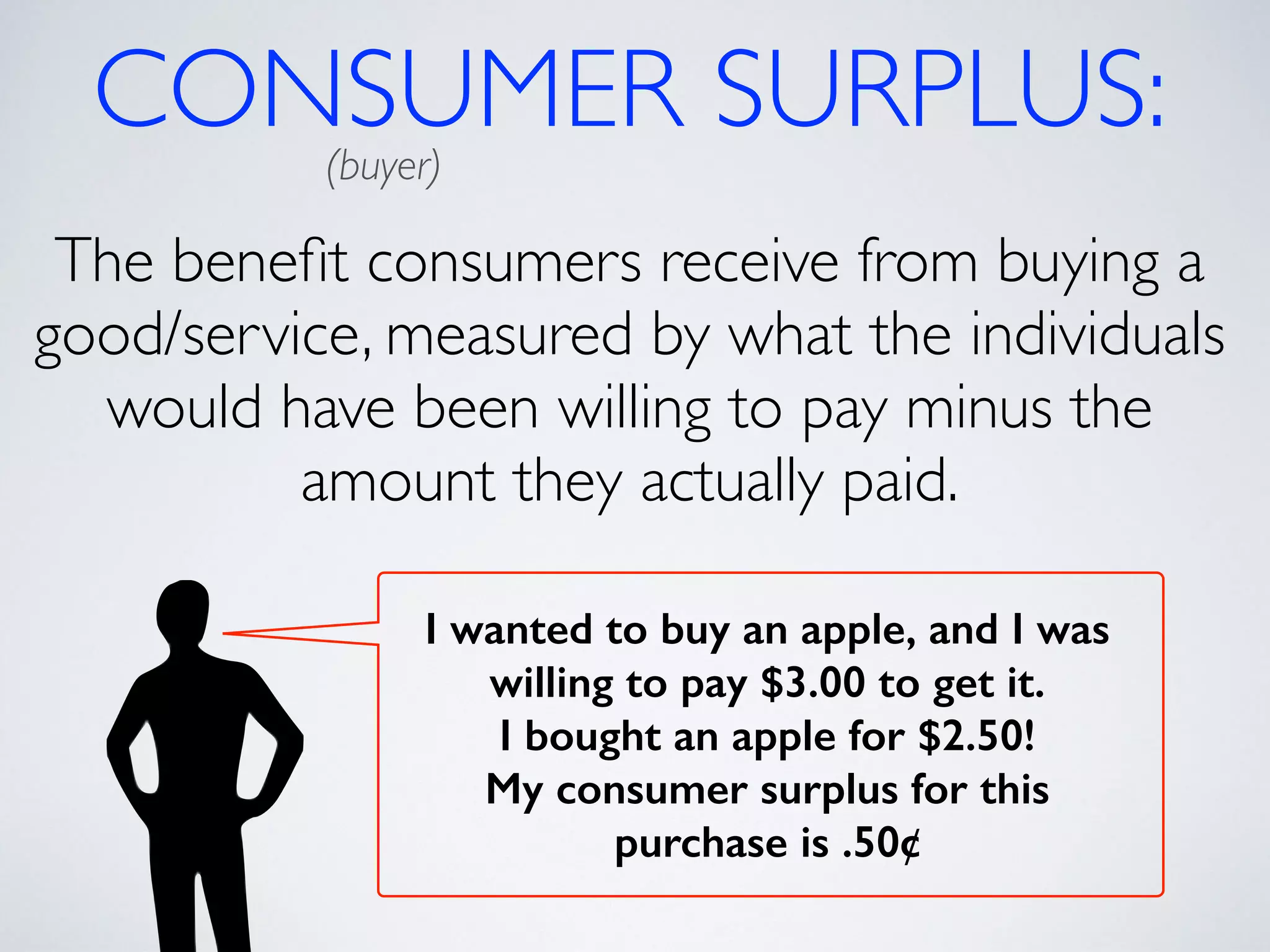

CONSUMER SURPLUS: (buyer)

The benefit consumers receive from buying a

good/service, measured by what the individuals

would have been willing to pay minus the

amount they actually paid.

I wanted to buy an apple, and I was

willing to pay $3.00 to get it.

I bought an apple for $2.50!

My consumer surplus for this

purchase is .50¢

12.

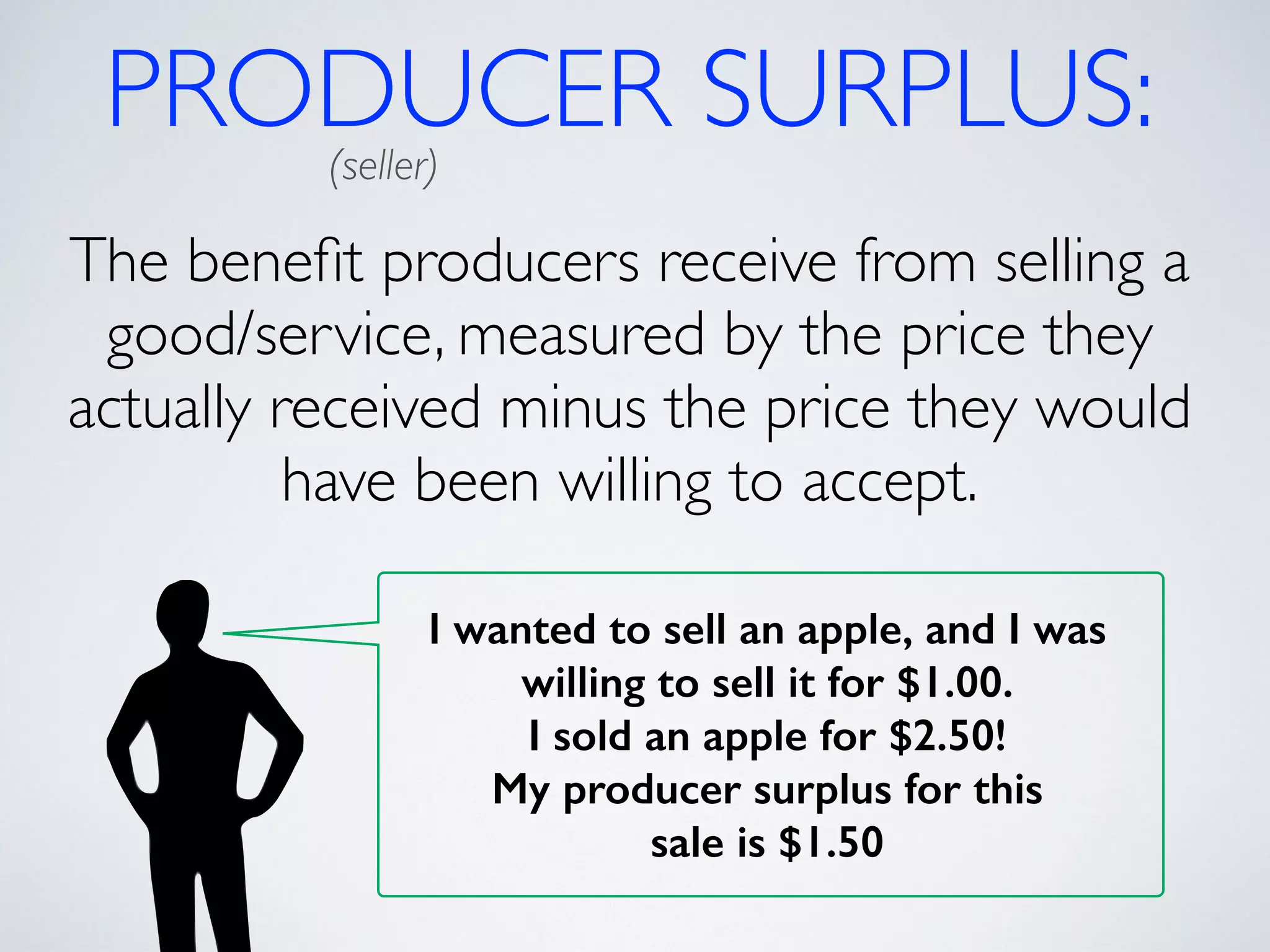

PRODUCER SURPLUS: (seller)

The benefit producers receive from selling a

good/service, measured by the price they

actually received minus the price they would

have been willing to accept.

I wanted to sell an apple, and I was

willing to sell it for $1.00.

I sold an apple for $2.50!

My producer surplus for this

sale is $1.50

13.

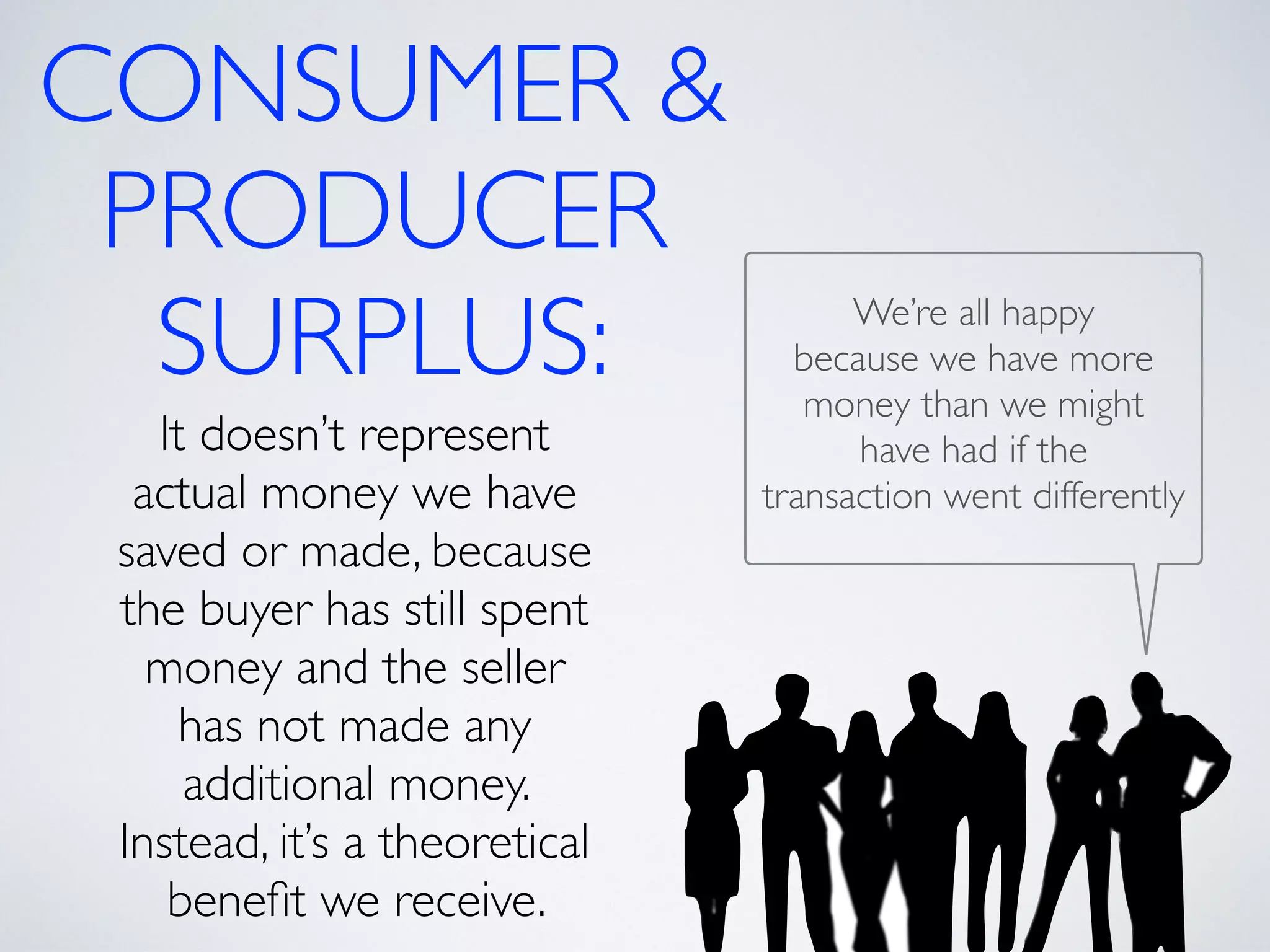

CONSUMER &

PRODUCER

SURPLUS:

It doesn’t represent

actual money we have

saved or made, because

the buyer has still spent

money and the seller

has not made any

additional money.

Instead, it’s a theoretical

benefit we receive.

We’re all happy

because we have more

money than we might

have had if the

transaction went differently

14.

* An auctioncan potentially eliminate consumer

surplus for the individual who wins.

15.

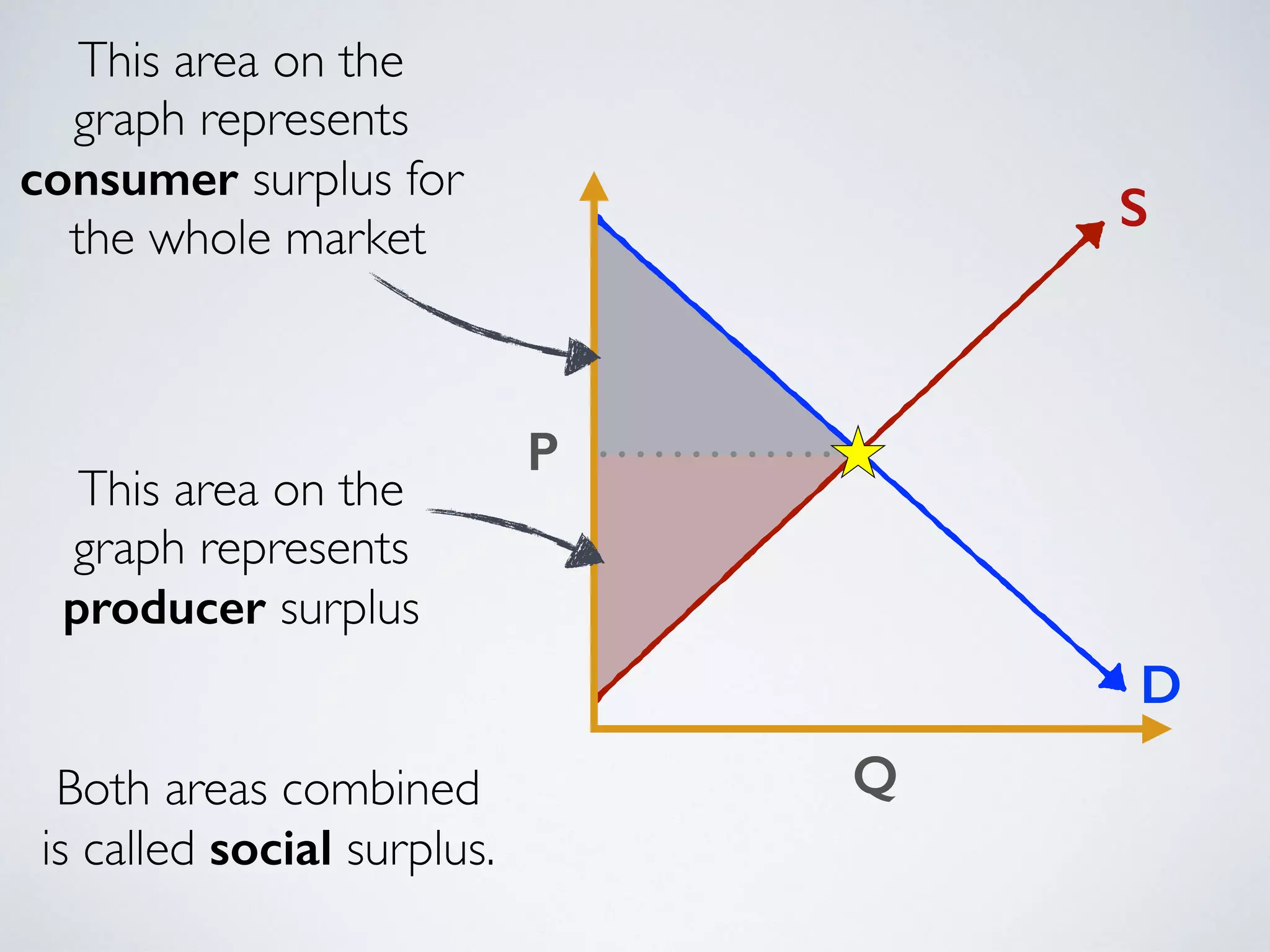

P

Q

S

D

This area on the

graph represents

consumer surplus for

the whole market

This area on the

graph represents

producer surplus

Both areas combined

is called social surplus.

16.

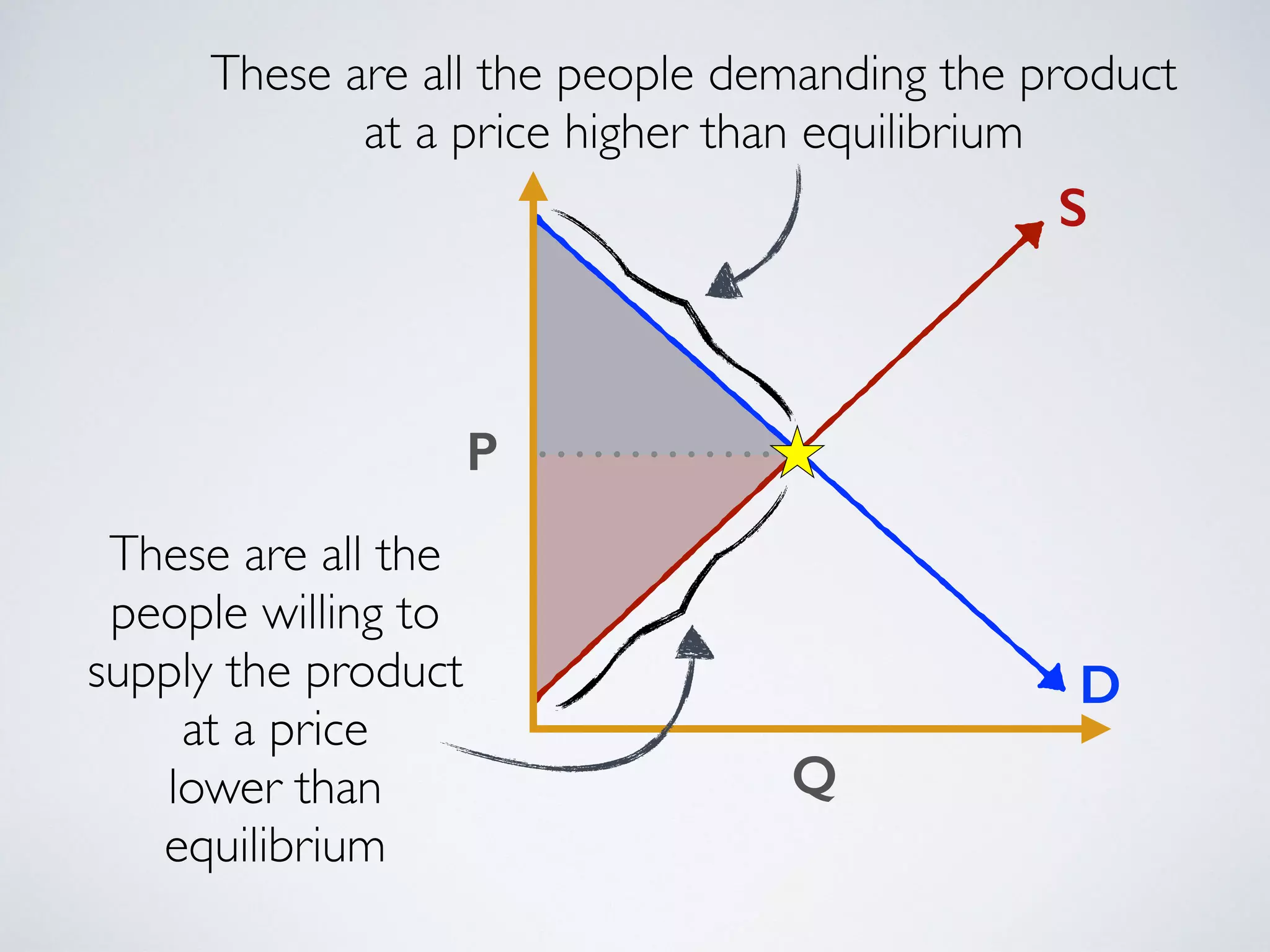

These are allthe people demanding the product

P

Q

S

D

at a price higher than equilibrium

These are all the

people willing to

supply the product

at a price

lower than

equilibrium

17.

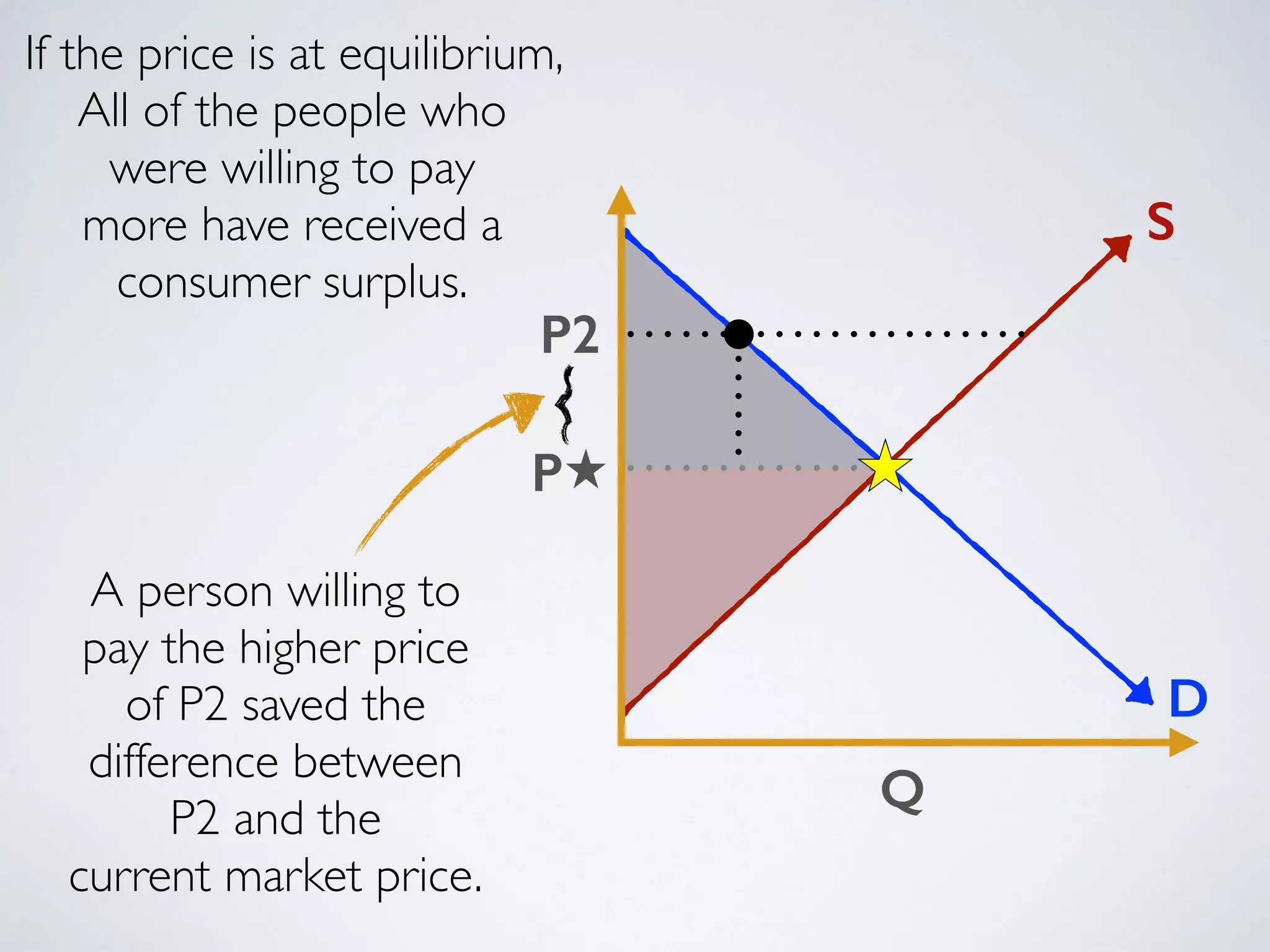

Q

S

D

P2

P

!

If the price is at equilibrium,

All of the people who

were willing to pay

more have received a

consumer surplus.

A person willing to

pay the higher price

of P2 saved the

difference between

P2 and the

current market price.

!

18.

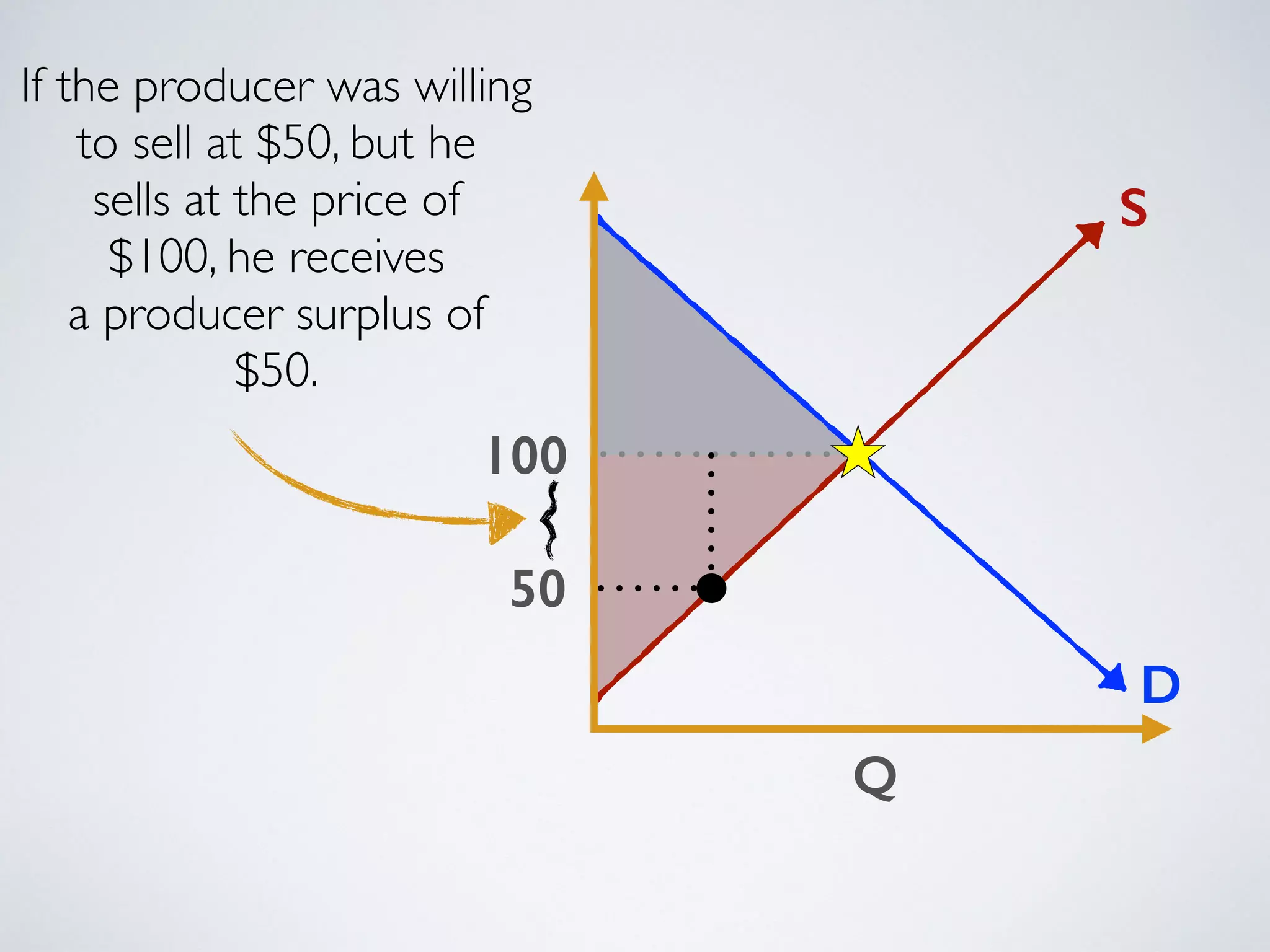

Q

S

D

If the producer was willing

to sell at $50, but he

sells at the price of

100

50

$100, he receives

a producer surplus of

$50.

19.

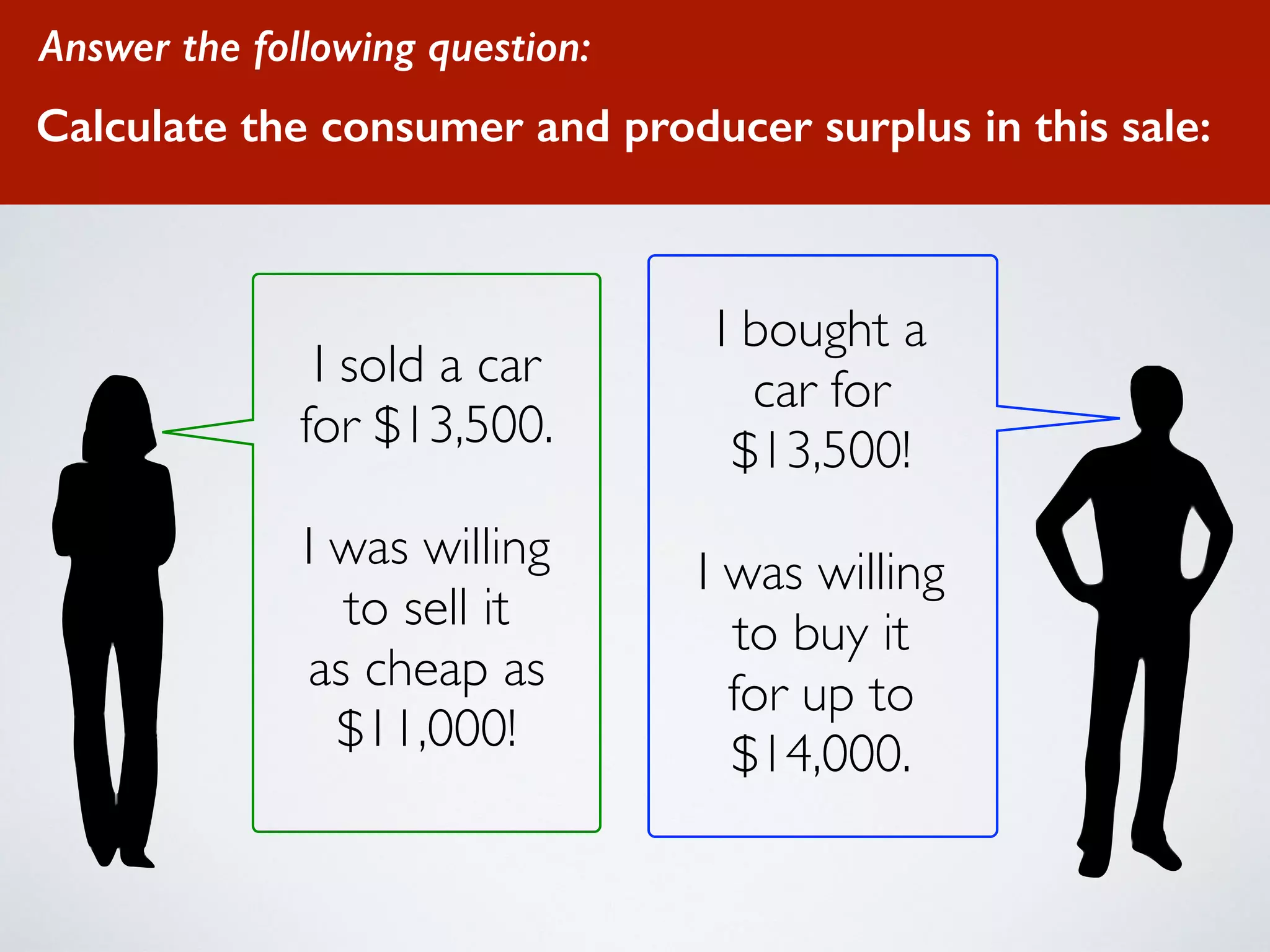

Answer the followingquestion:

Calculate the consumer and producer surplus in this sale:

I sold a car

for $13,500.

!

I was willing

to sell it

as cheap as

$11,000!

I bought a

car for

$13,500!

!

I was willing

to buy it

for up to

$14,000.

![Lesson 8--equilibrium[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-8-equilibrium1-130409201835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)