Downloaded 163 times

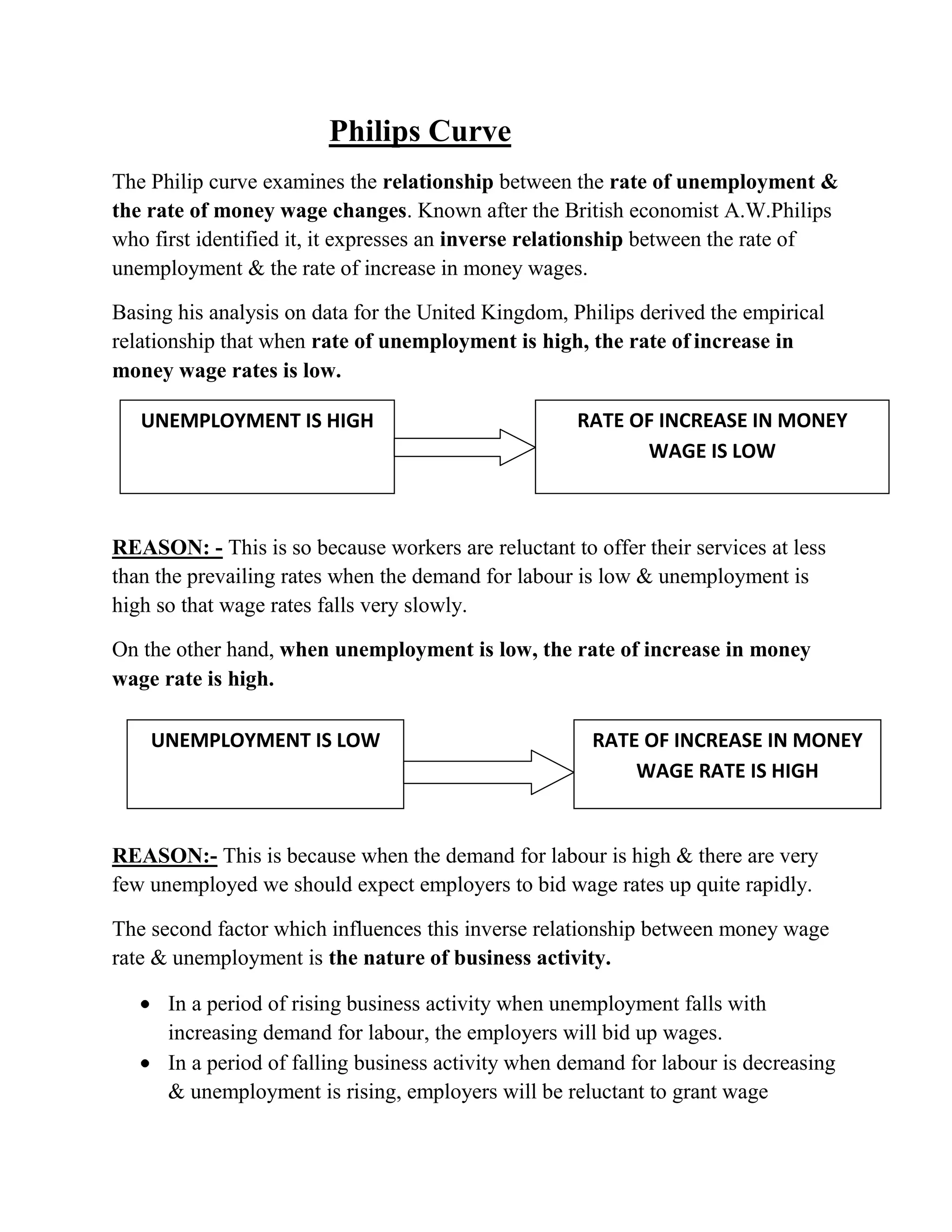

The Philip curve shows an inverse relationship between the rate of unemployment and the rate of change in money wages in the short run. Friedman argued that in the long run, there is no tradeoff between inflation and unemployment - the Philip curve becomes vertical at the natural rate of unemployment, which is the rate where expected and actual inflation are equal. Temporary reductions in unemployment below the natural rate are only possible if inflation rises above expectations, but eventually expectations will adjust and unemployment will return to the natural rate, even as inflation accelerates.