Downloaded 11 times

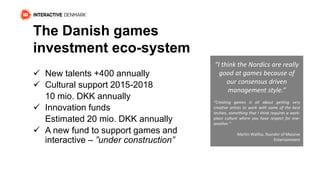

The document discusses the growth of the Danish video game industry, highlighting a 27% increase in turnover and significant profit growth among game companies in 2014. It emphasizes the importance of high-quality games, diverse platforms, and education in fostering success in the industry. Additionally, it outlines support for innovation and talent development in the sector through various funding initiatives.

![[dk] Bestyrelse og advisory board. Ib Paaskesen, Growing Games 2015](https://cdn.slidesharecdn.com/ss_thumbnails/boardsgrowinggames3-150908072033-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)