CAMBRIDGE IGCSE HISTORY: THE DAWES PLAN 1924. Contains: Germany's financial problems, imploding Weimar Republic, support for Germany, reflating German economy, reparations, payments, the importance of Dawes plan.

CAMBRIDGE IGCSE HISTORY: THE DAWES PLAN 1924. Contains: Germany's financial problems, imploding Weimar Republic, support for Germany, reflating German economy, reparations, payments, the importance of Dawes plan.

This page examines the reforms made to Germany's currency after the hyperinflation crisis, and also the Dawes and Young Plans regarding World War One reparations.

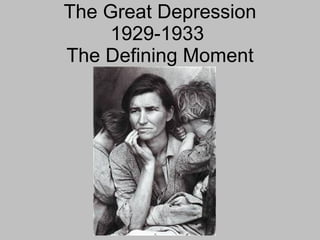

The Great Depression - Presentation (Macroeconomics Perspective)Arjun Parekh

This brief presentation on 'The Great Depression' has been made from the point of view of understanding Macroeconomic factors that played an important role.

This page examines the reforms made to Germany's currency after the hyperinflation crisis, and also the Dawes and Young Plans regarding World War One reparations.

The Great Depression - Presentation (Macroeconomics Perspective)Arjun Parekh

This brief presentation on 'The Great Depression' has been made from the point of view of understanding Macroeconomic factors that played an important role.

This powerpoint accompanies the article "Bringing it to the People, Lessons from the Great Depression" about what museums did during the 1930s economic crisis. http://www.aam-us.org/pubs/mn/depression.cfm

2studEnt Economic rEviEw vol. XXXiiThe Failure of In.docxrhetttrevannion

2

studEnt Economic rEviEw vol. XXXii

The Failure of

International

Multilateralism and the

Great Depression

Melissa Barrett, Senior Freshman

Almost 90 years after its beginning, the causes of the great depression

remain contested and uncertain. In this paper Melissa Barrett attempts

to decipher the chain of effects which caused the initial deflationary

episode to propagate into a deep depression. She explains how the gold

standard monetary became a catalyst of the deflationary crisis. This was

a symptom of an inadequacy in policymakers’ toolkit of response, due

to a lack of understanding and acknowledgement of the business cycle,

and international coordination. She concludes that these key failures

which were the root of policymakers’ miserable failure to mitigate the

crisis.

Introduction

This essay will argue that the primary causes of the Great Depression were the deflationary conditions of the mid 1920s, caused mainly by incompe-

tency in monetary policy. By extension, it is my contention that the internation-

al resentment caused by deflation was a reason behind the deep severity of the

Great Depression. Furthermore, any limited response was muted by the lack of

coordination between the world’s economy, and the prevailing attitude of narrow

national interest, rather than acknowledgement of the interdependent nature of

the global economy.

Deflation was incredibly problematic during the 1920s as it caused a rise

in the real value of debts, which brought already strained creditors to breaking

point. Deflation made paying back intergovernmental debts even more unfeasi-

ble, and this exacerbated the existing strain between countries in the post war

period. This strain was further worsened by debtor nations’ unrealistic expecta-

3

Economic History

tions and so it is the case that by 1923, the French still believed that the Germans

would make their reparation payments (Kemp, 1972).This was despite the fact

that the German mark was not stabilised until 1924, after a period of hyperinfla-

tion (Zacchia, 1976). Hjalmar Schacht, President of the Reichsbank from 1923 to

1930, wrote in 1931 that ‘the French attack upon German currency … was the

seed of that ever-growing lack of confidence which today hangs over the entire

world’ (Kindleberger, 1973).

Origin of deflation

A pertinent question to pose at this point is where did these deflationary

conditions come from? I will discuss two main causes of deflation, the housing

sector in the U.S and the Gold Standard. Both causes will be related back to a

European context. A single example which illustrates the immense importance

of the U.S to the international economy is seen in the fall of U.S exports when

the Federal Reserve raised interest rates in 1927. The fall in U.S exports was due

to other countries raising their own interest rates to keep in line with the domi-

nant currency of the world, the U.S dollar(Eichengreen, 2004).This was not an

advisab.

The Myopia of Hope (Bob Swarup presentation, Feb 2013)Bob Swarup

A presentation based on the first part of Till Debt Us Do Part, a new special report for Lombard Street Research by Dr Bob Swarup and Dario Perkins, which looks at the debt restructurings born of reparations that occurred in Europe in the 1920s and 1930s, and examines the parallels to Europe today. These are striking: a fixed exchange rate (gold vs euro); a complex web of debt (reparations and inter-allied war debts vs inter-European loans today); an intractable debtor (US vs Germany) that slavishly believed all debts needed to be honoured; and a misplaced belief in crushing austerity as the answer. La plus ça change...

The presentation tells about all the aspects that led to the great economic depression in 1929. All the historical, financial and other factors are looked upon with the help of online available data.

Explain how the current economic recession differs from the depressio.pdfrozakashif85

Explain how the current economic recession differs from the depression in the 1930\'s.

Solution

The Great depression was worldwide. It was due to the collapse of the international financial

system It also resulted from the mutual adoption by many countries ( including USA) of high-

tariff policies, which were intended to keep out foreign goods in order to protect domestic

producers. The policies were called \"beggar thy neighbour\" strategies since they attempted to

\"export\" unemployment by improving one country\'s trade position and hence demand for its

goods at the expense of its trading partners And , of course, if each country keeps out foreign

goods, the volume of world trade declines, providing a contractionary influence on the world

economy

Almost every country suffered a deep recession in the 1930s, but some countries did better than

USA Sweden began an expansionary policy in the early 1930s and reduced its unemployment

relatively quicker Britain\'s economy suffered high unemployment but in 1931 it went off the

gold standard and the ensuing devaluation of the pound sterling set the stage for some

improvement. Germany grew rapidly after Hitler came to power and expanded government

spending. China escaped the recession until after 1931, because it had a floating exchange rate.

In 1938, real GNP in US rose above its 1929 level for the first time in the decade, but it was not

until 1942 , after the US formally entered world war II , that the unemployment rate finally fell

below 5%

The experience of the US in the early 1980s- the worst recession since the Great Depression,

casts doubt on the optimistism of recovery. During the 1980s, the US experienced the largest

sustained budget deficits in its peacetime history. Even so cutting spending or raising taxes was

not politically popular. Gradually, in the 1990s, the deficit began to be brought under control,

and toward the end of the decade the budget swung into surplus.This was due to raising the

prices and government spending.

By,

Nishant Bhatt.

Basavarajeeyam is an important text for ayurvedic physician belonging to andhra pradehs. It is a popular compendium in various parts of our country as well as in andhra pradesh. The content of the text was presented in sanskrit and telugu language (Bilingual). One of the most famous book in ayurvedic pharmaceutics and therapeutics. This book contains 25 chapters called as prakaranas. Many rasaoushadis were explained, pioneer of dhatu druti, nadi pareeksha, mutra pareeksha etc. Belongs to the period of 15-16 century. New diseases like upadamsha, phiranga rogas are explained.

micro teaching on communication m.sc nursing.pdfAnurag Sharma

Microteaching is a unique model of practice teaching. It is a viable instrument for the. desired change in the teaching behavior or the behavior potential which, in specified types of real. classroom situations, tends to facilitate the achievement of specified types of objectives.

Explore natural remedies for syphilis treatment in Singapore. Discover alternative therapies, herbal remedies, and lifestyle changes that may complement conventional treatments. Learn about holistic approaches to managing syphilis symptoms and supporting overall health.

ARTIFICIAL INTELLIGENCE IN HEALTHCARE.pdfAnujkumaranit

Artificial intelligence (AI) refers to the simulation of human intelligence processes by machines, especially computer systems. It encompasses tasks such as learning, reasoning, problem-solving, perception, and language understanding. AI technologies are revolutionizing various fields, from healthcare to finance, by enabling machines to perform tasks that typically require human intelligence.

Lung Cancer: Artificial Intelligence, Synergetics, Complex System Analysis, S...Oleg Kshivets

RESULTS: Overall life span (LS) was 2252.1±1742.5 days and cumulative 5-year survival (5YS) reached 73.2%, 10 years – 64.8%, 20 years – 42.5%. 513 LCP lived more than 5 years (LS=3124.6±1525.6 days), 148 LCP – more than 10 years (LS=5054.4±1504.1 days).199 LCP died because of LC (LS=562.7±374.5 days). 5YS of LCP after bi/lobectomies was significantly superior in comparison with LCP after pneumonectomies (78.1% vs.63.7%, P=0.00001 by log-rank test). AT significantly improved 5YS (66.3% vs. 34.8%) (P=0.00000 by log-rank test) only for LCP with N1-2. Cox modeling displayed that 5YS of LCP significantly depended on: phase transition (PT) early-invasive LC in terms of synergetics, PT N0—N12, cell ratio factors (ratio between cancer cells- CC and blood cells subpopulations), G1-3, histology, glucose, AT, blood cell circuit, prothrombin index, heparin tolerance, recalcification time (P=0.000-0.038). Neural networks, genetic algorithm selection and bootstrap simulation revealed relationships between 5YS and PT early-invasive LC (rank=1), PT N0—N12 (rank=2), thrombocytes/CC (3), erythrocytes/CC (4), eosinophils/CC (5), healthy cells/CC (6), lymphocytes/CC (7), segmented neutrophils/CC (8), stick neutrophils/CC (9), monocytes/CC (10); leucocytes/CC (11). Correct prediction of 5YS was 100% by neural networks computing (area under ROC curve=1.0; error=0.0).

CONCLUSIONS: 5YS of LCP after radical procedures significantly depended on: 1) PT early-invasive cancer; 2) PT N0--N12; 3) cell ratio factors; 4) blood cell circuit; 5) biochemical factors; 6) hemostasis system; 7) AT; 8) LC characteristics; 9) LC cell dynamics; 10) surgery type: lobectomy/pneumonectomy; 11) anthropometric data. Optimal diagnosis and treatment strategies for LC are: 1) screening and early detection of LC; 2) availability of experienced thoracic surgeons because of complexity of radical procedures; 3) aggressive en block surgery and adequate lymph node dissection for completeness; 4) precise prediction; 5) adjuvant chemoimmunoradiotherapy for LCP with unfavorable prognosis.

Ozempic: Preoperative Management of Patients on GLP-1 Receptor Agonists Saeid Safari

Preoperative Management of Patients on GLP-1 Receptor Agonists like Ozempic and Semiglutide

ASA GUIDELINE

NYSORA Guideline

2 Case Reports of Gastric Ultrasound

Tom Selleck Health: A Comprehensive Look at the Iconic Actor’s Wellness Journeygreendigital

Tom Selleck, an enduring figure in Hollywood. has captivated audiences for decades with his rugged charm, iconic moustache. and memorable roles in television and film. From his breakout role as Thomas Magnum in Magnum P.I. to his current portrayal of Frank Reagan in Blue Bloods. Selleck's career has spanned over 50 years. But beyond his professional achievements. fans have often been curious about Tom Selleck Health. especially as he has aged in the public eye.

Follow us on: Pinterest

Introduction

Many have been interested in Tom Selleck health. not only because of his enduring presence on screen but also because of the challenges. and lifestyle choices he has faced and made over the years. This article delves into the various aspects of Tom Selleck health. exploring his fitness regimen, diet, mental health. and the challenges he has encountered as he ages. We'll look at how he maintains his well-being. the health issues he has faced, and his approach to ageing .

Early Life and Career

Childhood and Athletic Beginnings

Tom Selleck was born on January 29, 1945, in Detroit, Michigan, and grew up in Sherman Oaks, California. From an early age, he was involved in sports, particularly basketball. which played a significant role in his physical development. His athletic pursuits continued into college. where he attended the University of Southern California (USC) on a basketball scholarship. This early involvement in sports laid a strong foundation for his physical health and disciplined lifestyle.

Transition to Acting

Selleck's transition from an athlete to an actor came with its physical demands. His first significant role in "Magnum P.I." required him to perform various stunts and maintain a fit appearance. This role, which he played from 1980 to 1988. necessitated a rigorous fitness routine to meet the show's demands. setting the stage for his long-term commitment to health and wellness.

Fitness Regimen

Workout Routine

Tom Selleck health and fitness regimen has evolved. adapting to his changing roles and age. During his "Magnum, P.I." days. Selleck's workouts were intense and focused on building and maintaining muscle mass. His routine included weightlifting, cardiovascular exercises. and specific training for the stunts he performed on the show.

Selleck adjusted his fitness routine as he aged to suit his body's needs. Today, his workouts focus on maintaining flexibility, strength, and cardiovascular health. He incorporates low-impact exercises such as swimming, walking, and light weightlifting. This balanced approach helps him stay fit without putting undue strain on his joints and muscles.

Importance of Flexibility and Mobility

In recent years, Selleck has emphasized the importance of flexibility and mobility in his fitness regimen. Understanding the natural decline in muscle mass and joint flexibility with age. he includes stretching and yoga in his routine. These practices help prevent injuries, improve posture, and maintain mobilit

2. Why “Great” Depression

Ben Bernanke: “To understand the Great Depression is the

Holy Grail of macroeconomics. Not only did the Depression

give birth to macroeconomics as a distinct field of study, but

also---to an extent that is not always fully appreciated—the

experience of the 1930s continues to influence

macroeconomists; beliefs, policy recommendations and

research agendas…..We do not yet have our hands on the

Grail by any means…..”(JMCB, 1995)

3. Rex Tugwell

(advisor to Roosevelt)

“The Cat is out of the Bag.

There is no invisible hand.

There never was. If the

depression has not taught us

that we are incapable of

education…..We must now

supply a real and visible

guiding hand to do the task

which that mythical,

nonexistent, invisible agency

was supposed to perform,

but never did.”

4. The Prelude 1919-1929

• U.S. enters the war late. (1917-1918)

effects on U.S. economy relatively small

compared to European economies.

• Huge damage and disruption to European

economies.

• Real GDP = 100 in 1913. In 1919,

UK=101 France=75 Germany=72 US = 116

• Inflation! Price level = 100 in 1914. In 1918

UK=210 France=213 Germany304 US=164

• Huge climb in Debt/GDP ratios.

5. Consequences

1. World War I---9.5 million deaths. Loss of a

generation (UK 1m, France 1.4m, Germany 2m,

US 114,000)

2. Destruction of physical capital especially

Belgium and northern France

3. Distortion of patterns of production, trade and

consumption (e.g. high wartime prices for

commodities—boom and collapse in U.S.

4. High cost of war. Estimated $208 billion.

5. Political and economic borders of Europe are

redrawn.

6. Inter-allied war debts and German reparations.

6. Inter-Allied War Debts ($ billions)

(Kindleberger,The World in Depression

France

4.0 3.0

4.7 3.5

United States United Kingdom

8.1

3.2

Other Countries

To pay principal and interest, war devastated economies would

have to run balance of payments surpluses.

7. German Reparations

• John Maynard Keynes (1919) Reparations

were a “policy of reducing Germany to

servitude for a generation, of degrading

the lives of millions of human beings, and

of depriving a whole nation of happiness.”

They were “abhorrent and detestable.”

• Étienne Mantoux (1946) Reparations not

excessive, destructive or uncollectible.

• The French paid in 1815 and 1871---”Le

Boche Paiera”

8. The magnitude of reparations

Indemnity Percent Share of

(billions) of One Debt

Year's Service

GDP to GDP

France 1815-1819 FF 1.65 to 18 to 21 1.2 to 1.4

1.95

France 1871 FF 5.0 25 0.7

Germany1923-1931 DM 50 83 2.5

Vichy 1940-44 FF 479 111 2.6

Germany1953-1965 527 US$ 7.7 0.4

Japan 1955-1965 1486 US$ 3.0 0.8

9. Solution---the Dawes Loan 1924

• German Hyperinflation.

• Dawes Loan---begins series of loans---

U.S. provides funds and funds for

investment around the globe.

• New York as central of global finance—not

London

10. Return to Gold Standard

“Status Quo Antebellum”

• No problem for U.S.—huge balance of payments

surpluses and gold

• U.K. deflates and returns to gold in 1925 at old

parity £1 = $4.86. But overvalued. Depressed

economy.

• France with near hyperinflation returns to gold in

1926 at a new parity (old $1= 5FF now $1 = 25.5

FF) Undervalued currency. Booming economy.

• Germany’s hyperinflation---returns to gold at

near purchasing power 1925.

• Major imbalances---brittle equilibrium.

11. Adjustment under restored gold

standard more difficult

• International capital markets are revived---

generally free.

• International labor flows almost eliminated

—immigration restrictions

• Increased protectionism

• Less wage flexibility. Wage now seem

sticky even with high unemployment

12. U.S. Economic Prosperity in 1920s

• No trend inflation

• High productivity growth

• 1922-1929, GNP grew at 4.7%,

• Unemployment averaged 3.7%.

• Fed accommodated seasonal demands

for credit and attempted to smooth

economic fluctuations. (2 brief

recessions)

13. Some basic numbers

• Peak August 1929, Trough May 1933

• Real GDP falls 39%

• Real Consumption falls 29%

• Prices (GDP deflator) falls 23%

• Unemployment Jumps:

– 3.2% in 1929

– 25% in 1933 (21%Darby)

– 17% in 1939 (17% Darby)

• Banking Collapse

– July 1929, 24,504 banks, $49 billion deposits.

– December 1932, 17,802 banks, with $36 billion.

– After Bank Holiday March 1933, 11,878 banks with

$23 billion deposits.

14. Key American Role in World Depression

• Based on

industrial

production

GD starts in

most

countries at

the same

time

• But it is

larger and

longer in the

U.S. Romer

(1993)

15. Worst in the U.S.

• For the U.S.,

Industrial

Production

– Biggest drop in

first year

– Biggest drop

peak to trough

– Biggest drop in

the last year.

• However, turning

points are very

similar

16. Understanding the Great Depression:

Its Evolution by Phases

Real GDP, 1920-1941

1. Booming Strong Economy in 1920s

140

2. Beginning Shocks, 1928-1929

3. Aggravating Shocks, 1930-1933

130

4. Rock Bottom and Recovery, 1933-1936

120

5. The 1937-1938 Recession

110

6. The Recovery, 1939-1941

1929=100

100

90

80

70

60

1920 1921 1922 1923 1924 1925 1926 1927 1928 1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939 1940 1941

17. Understanding the

Great Depression:

Four Basic Questions Real GDP, 1920-1941

140

1. Why it Began?

2. Why so Deep? 130

3. Duration? 120

4. Recovery? 110

1929=100

100

90

80

70

60

1920 1921 1922 1923 1924 1925 1926 1927 1928 1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939 1940 1941

18. Understanding the Great Depression:

Its Evolution by Phases

1. Booming Strong Economy in 1920s…but

a) It’s the Roaring Twenties!

b) No trend inflation

c) High productivity growth

d) 1922-1929, GNP grew at 4.7%,

e) Unemployment averaged 3.7%.

f) Fed accommodated seasonal demands for credit and

attempted to smooth economic fluctuations. (2 brief

recessions)

g) BUT: Weak American Agriculture: low prices, high debt,

weak banks

h) BUT: Weak Europe: reparations, debts to U.S., slow

growth, gold standard fragile (overvalued £, UK slumps)

and (undervalued FF, France booms)

i) BUT: U.S. Stock market boom halts foreign loans to

Germany, Eastern Europe and Latin America

19. Understanding the Great Depression:

Its Evolution by Phases

1. Beginning Shocks, 1928-1929

• Spring 1927 U.S. expansionary monetary policy to ease pressure

on the British balance of payments. Critics assert policy too easy,

and allows stock market boom to ignite

• Fed tightens policy in 1928 (discount rate 3 ½ to 5%, and there is

little increase in total money or credit for 1928-1929.

• U.S. stock market boom begins March 1928.

• Commercial paper market vanishes

• No new lending to Germany, Austria and rest of work in

1928….Germany slides into a recession.

• Fed tries to “jaw-bone” market down. Criticizes brokers loans.

• July 1929 raises discount rate from 5 to 6%.

• But July-August is peak of business cycle. Recession begins

Summer 1929

• October 1929 U.S. Stock market crash: wealth effect—lowers

consumption and investment, credit effect—reduces value of

collateral and hence lending

• Smoot-Hawley tariff 1929 by U.S. induces retaliatory tariffs by

other countries, international trade declines

20. Understanding the Great Depression:

Its Evolution by Phases

1. Aggravating Shocks, 1930-1933

a) Banking Panics, 1930, 1931, 1933

– Failure of the Fed to Pursue Expansionary Policy

– Collapse of Gold Standard: Austria, Germany leave the gold

standard, Britain departs after a run on the pound in September 1931

– U.S. begins losing gold, trade deficits and capital flight.

2. From Rock Bottom to Recovery, 1933-1936

– Bank Holiday March 1933

– U.S. abandons the Gold Standard March 1933

– New Deal Banking and Securities Legislation

– Monetary Expansion

– Minimal Fiscal Policy

– National Industrial Recovery Act (NIRA)

3. The 1937-1938 Recession

a) The Fed Raises Reserve Requirements

4. The Recovery, 1939-1941

a) Monetary Expansion

b) Fiscal Expansion in preparation for war.

21. Four Basic Questions:

1. Why It Began?

2. Why So Deep and 3. So Long?

• Friedman and Schwartz (and others), the

economy is entering a recession in late

1929

• The economy is beginning to recover in

1931 like a normal business cycle

• BUT what makes the recession worse?

• What turns the recession into a

depression?

22. The Worsening Depression

• Slight recovery early 1931,then plunge.

• Why?

• Romer (1993) “The source of the continued

decline in production in the United States was

almost surely a series of banking panics.”

• Friedman and Schwartz (1963) document four

panics

– Fall of 1930

– Spring 1931

– Fall 1931---Britain abandons the Gold Standard

– First Quarter 1933

• 9000 Banks suspend operations. Depositors

and stockholders lose $2.5 billion = 2.4% of

GDP…...not the whole story

24. Why Banking Panics?

• There were no banking panics in Canada.

• Fragmented unit banking system

• Undiversified bank portfolios with high

regional concentration of loans. Large

number of bank closures in the agricultural

states when agricultural prices fall. In

addition, many hold bonds whose value

collapsed.

• Many banks become insolvent

• Fear of insolvency feeds the liquidity

crisespanics.

25. Effects of Banking Panics

• Money Supply Declines and there is a massive

rise in realized real interest rates, over 10%.

• Friedman and Schwartz blame inaction of the

Fed for this decline---and hence for the

depression.

26. How do Friedman and Schwartz

explain why the Fed did not act?

• Up to end of 1930

– What is the Fed concerned

about?

– How does it react to banking

failures?

• Who was Benjamin Strong?

• New York Fed v. Board of

Governors?

• What could the Fed have

done 1930-1931?

• What does Congress do?

27. Why didn’t the Fed act?

• Beginning in 1931, Friedman and Schwartz argue that Fed

could have expanded but chose not to.

• In diary of Charles S. Hamlin member of the FR Board, he

wrote during August 1931 that Open market committee

voted 11 to 1 against $300 million open market purchase

of bonds---reduce it to $120 million.

• Governor Mayer of the Board worried about inflation.

• Members of the regional banks did not grasp the extent of

the crisis.

• Pressure from Congress---open market operations of $1

billion. Until Congress adjourns.

• After Britain leaves gold in September 1931, gold drain

starts. Dollars exchanged for gold---Fed’s reserves fall, it

is afraid that further expansion will lead to greater loss of

gold----constrained by the gold standard. Reserves falling

after UK goes off gold in 1931, must retain high interest

rates.

28. Understanding the Great Depression:

Four Basic Questions

1. Why it Began?

2. Why so Deep?

3. Duration?

4. Recovery?

29. Understanding the Great Depression:

Four Basic Questions

1. Why it Began?

Business Cycle Peak 7/8-1929, Federal

Reserve’s tight policy

2. Why so Deep?

Banking Panics. Inaction of the Federal

Reserve

• Duration?

• Recovery?

30. How is the economy driven into a

severe depression by the declining

money supply?

What is the mechanism of

transmission?

Several Explanations……

31. Romer (1993) basic argument is simple

• Depression is the result of a series of aggregate demand

(monetary) shocks that moved economy down an

upward sloping aggregate supply curve.

Price Price

Level Level

Output Output

32. Romer (1993) basic argument is simple

• Depression is the result of a series of aggregate

demand (monetary) shocks that moved

economy down an upward sloping aggregate

supply curve.

• Result is two problems: (1) unemployment and

(2) deflation.

• Unemployment:

– Key point is the upward sloping supply curve. Wages

and prices not perfectly flexible in 1920s and 1930s.

– Why did they become less flexible? Some studies

point to turn-of-the-century change in labor contracts,

World War I or desire of business to keep demand

strong.

– Wage and price stickiness means that aggregate

demand shocks will have real effects.

34. How did deflationary shocks affect the

economy?

• Conventional 19th century view: fall in wages and

prices raises stimulate investment, countering

shock….but not in sticky price world.

• How did the monetary shocks hurt the

economy?

– Explanation 1: High real interest rate hypothesis:

Deflation affects expectations. Deflation generates

expectations of higher real rate of interest, raising real

rates and driving down investment

– Explanation 2: Debt-Deflation hypothesis:

Unanticipated inflation increased real debt, increasing

defaults and thus depressing supply of credit

35. Rising Real Interest r = i – p(expected)

Rates—Did the Fed

understand?

• Nominal commercial paper

rate 1927.4 to 1928.4 rises

from 4.0% to 5.5% and the

realized real rate from 5.6% to

9.5%.

• Rational expectations

estimates by Romer of the

expected real interest rate are

shown to rise----implying

higher anticipated interest

rates.

• Interest sensitive industries

begin to slow in 1929: building

permits and automobile

registrations.

36. • Sources of the onset—1929-1930/1931 contrasts

previous experience

• The decline in consumer spending and fixed investment

that are the key elements that need to be explained.

39. Debt Deflation

Hypothesis:

Hamilton looks at

the futures

markets for

predictions of

future prices----

errors random until

1930s when

underestimate

deflation

seriously----don’t

believe that crisis

will continue

40. Klug, Landon-Lane and White looked at the forecasts of

Railroad Shippers and found huge cumulating errors in

forecasts of carloadings---businessmen keep thinking that

recovery is around the bend.

20

10

0

p rc n g e r

e e ta e rro

-10

-20

-30

-40

-50

12

98 13

90 13

92 13

94 13

96 13

98 14

90

Y a a dQ a r

e r n u rte

41. Bernanke’s Contribution—a Third Factor

• In addition to monetary collapse, there was a

disruption of intermediation.

• Bernanke (1983): banks play special role for

firms that cannot issue bonds and stocks. When

banks fail the information and relationships are

lost and the cost of credit intermediation rises.

Costs include screening, monitoring, and

accounting costs as well as expected losses

from bad borrowers.

• Major contribution to economic decline 1931 and

1932.

42. Banking crises an

important

determinant of

loans as much as

industrial Panic

production. begins

Liquidation of loans

after stock market

crash

But then credit

declines little even

though IP falls 25%

until banking

crises.

43.

44. Understanding the Great Depression:

Four Basic Questions

1. Why it Began?

Business Cycle Peak 7/8-1929, Federal

Reserve’s tight policy

2. Why so Deep?

Banking Panics. Inaction of the Federal

Reserve—prolonged monetary contraction

• Duration?----Clearly inaction plays a role

—what else?

• Recovery?

45. What about Fiscal Policy—Deficit

Spending?

Price Price

Level Level

Output Output

46. Fiscal Policy?—Deficit Spending?

Federal Deficit as Percentage of GDP

In 2005---it was -2.6%

10

8

6

4

2

Percent

0

1920 1921 1922 1923 1924 1925 1926 1927 1928 1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939

-2

-4

-6

-8

-10

Actual GDP Full Employment GDP

47. Industrial Policy?

• Specific Intervention in industry?

• National Industry Recovery Act (NIRA) of 1933

created the National Recovery Administration

(NRA). (Declared unconstitutional May 1935)

• National Labor Relations Act (1935) that

promoted unions and Fair Labor Standards Act

(1938) that set minimum wages in certain

industries and regulates working conditions.

• NRA established guidelines that raised nominal

wages and prices and encouraged higher levels

of employment by work-sharing reductions in the

length of the work week.

48. Industrial Policy

• Weinstein (1980), using

aggregate monthly data on

hourly earnings in

manufacturing, he found that

the NIRA raised nominal wages

directly and indirectly by raising

prices. Econometric estimates

that average hourly earnings

would have been 35 cents not

60 cents.

• Result----higher wages create

more unemployment and

increase the duration of the

depression because of higher

costs to producers---

counterproductive

• Shift in the Aggregate Supply

Curve

50. Recession of 1937-1938

• Did the Fed learn its lesson?

• Rising excess reserves held by banks—

Fed worries about inflation potential and

wants to induce lending.

• Uses new tool of required reserves.

Required reserve ratio doubled.

• Result? Banks raise their excess reserves

and huge monetary contraction.

51. Understanding the Great Depression:

Four Basic Questions

1. Why it Began?

Business Cycle Peak 7/8-1929, Federal Reserve’s

tight policy

2. Why so Deep?

Banking Panics. Inaction of the Federal Reserve.

Prolonged Monetary Contraction

3. Duration?

Continued Monetary Policy Mistakes, Fiscal Policy

not tried. Industrial Policy makes things worse.

• Recovery? Why?

52. Recovery, 1934-1937….why?

• Real GDP grows at

10% p.a.

1934-1937.

• But real GDP on

reaches 1929 peak

in 1937 and trend

path in 1942.

• What drove the

recovery.

• Friedman and

Schwartz (1963)

and Romer (1992):

huge increases in

the money supply.

55. How was the money supply increased?

• F.D. Roosevelt takes emergency powers granted by

Congress in the 100 days.

• FDR allows the dollar to depreciate—sets new value for

gold in 1934: from $20.36 per ounce to $35 per ounce.

• Huge revaluation of big U.S. gold stocks. Treasury

issues gold certificates equal in value to increase and

deposits them with the Fed. As government spends

them, they enter the monetary base. High powered

money increased 12% between April 1933 and April

1934.

• Devaluation also improved the competitiveness of U.S.

goods—rise in the trade balance.

• Devaluation attracted capital flows from Europe,

especially with Hitler’s rise to power. High powered

money rises 40% from April 1934 to April 1937.

• Result: real interest rates fall and recovery of investment

and consumer durable spending.

58. Understanding the Great Depression:

Four Basic Questions

1. Why it Began?

Business Cycle Peak 7/8-1929, Federal Reserve’s

tight policy

2. Why so Deep?

Banking Panics. Inaction of the Federal Reserve

Prolonged Monetary Contraction.

3. Duration?

Continued Monetary Policy Mistakes, Fiscal Policy

not tried. Industrial Policy makes things worse.

4. Recovery?

Monetary Expansion

59. Some Effects of the Great Depression

1. Activist Monetary Policy

2. Activist Fiscal Policy---idea of cyclically

balanced budget

3. Insurance and Regulation of the Financial

Sector

4. Agricultural Regulation

5. Growth of Government and shift in Federalism

6. Growth of Unions

7. Genesis of Social Security

8. Smoot-Hawley Tariff of 1929 to the WTO

9. The IMF and World Bank