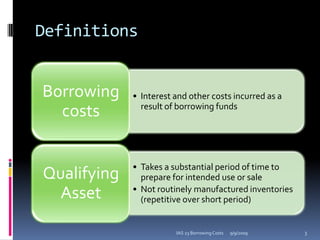

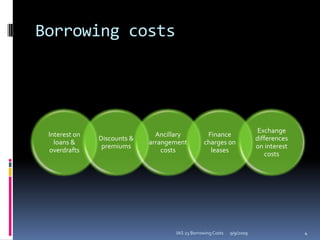

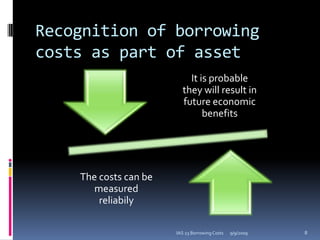

This document discusses IAS 23 Borrowing Costs. It defines borrowing costs and qualifying assets that allow capitalization of borrowing costs. Borrowing costs can be capitalized as part of the cost of a qualifying asset during the period of time required to complete and prepare the asset for its intended use. Capitalization commences when expenditures are incurred on the asset and ceases when the asset is substantially complete. The document also covers suspension of capitalization, disclosure requirements, and transitional provisions related to IAS 23 Borrowing Costs.