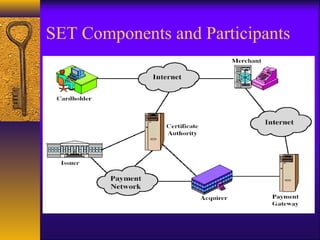

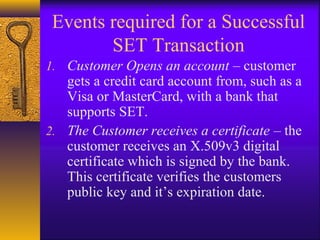

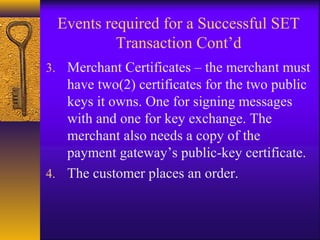

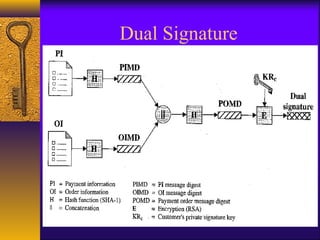

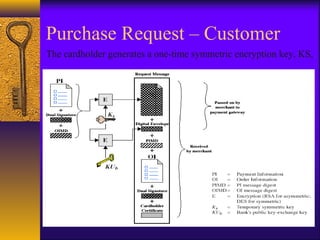

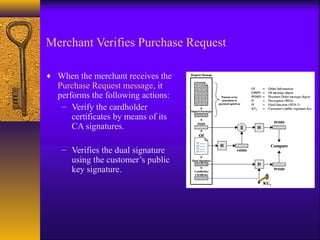

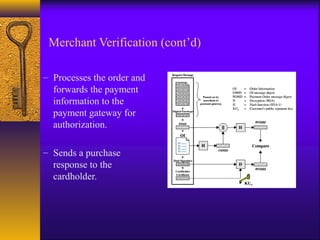

This document provides an overview of Secure Electronic Transaction (SET), which was created by Visa and Mastercard to securely facilitate online credit card transactions. SET uses public key cryptography including digital signatures and certificates to provide confidentiality, integrity, and authentication. It involves cardholders, merchants, issuers, acquirers, payment gateways, and a certification authority. The key steps in a SET transaction include the customer receiving an X.509 certificate, order and payment information being sent with dual signatures to link them, and the merchant requesting payment authorization from the payment gateway.