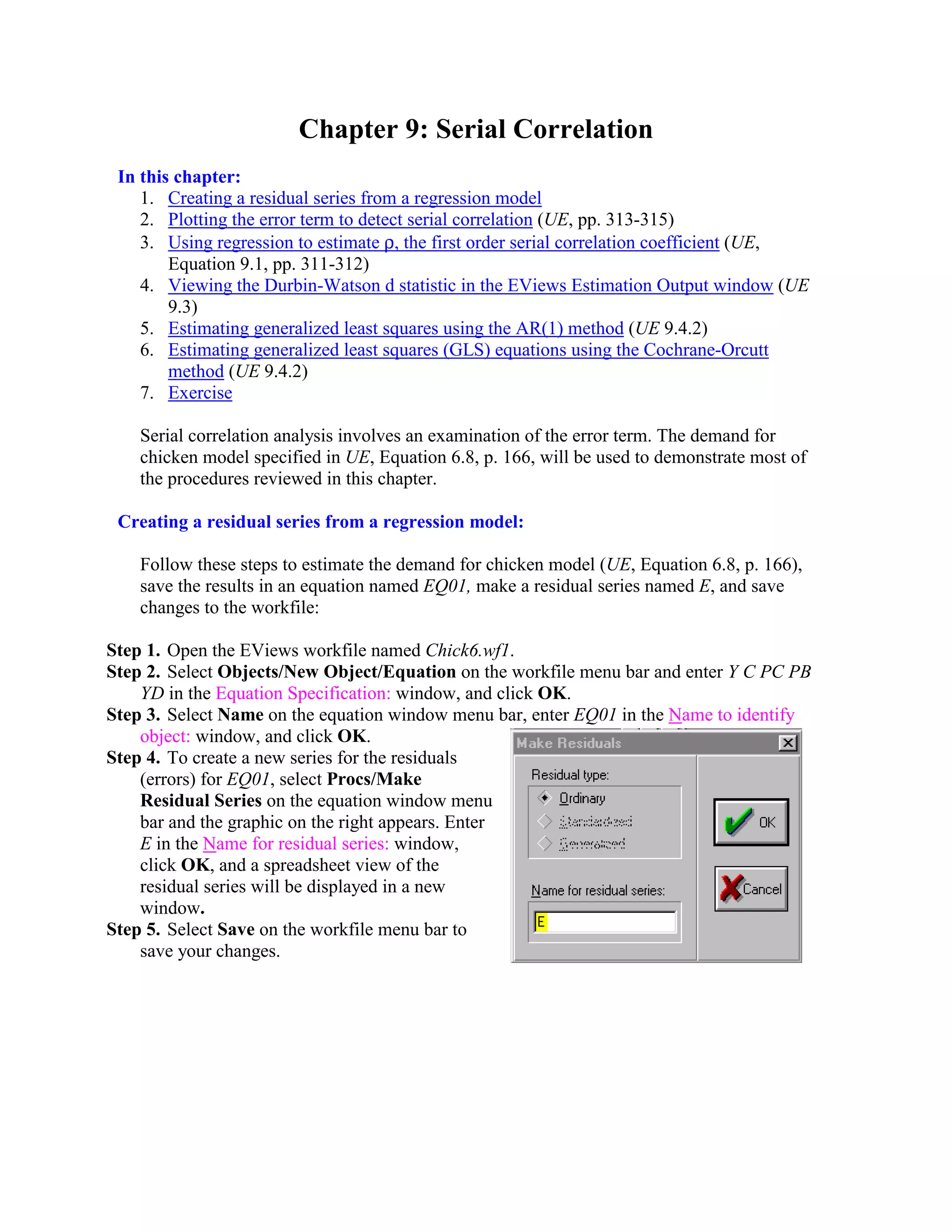

1) The document discusses various techniques for detecting and correcting serial correlation in regression models, including plotting residuals, estimating the serial correlation coefficient ρ, and using the Durbin-Watson statistic.

2) It provides step-by-step instructions for implementing these techniques in EViews, including estimating models with generalized least squares using the AR(1) and Cochrane-Orcutt methods.

3) As an exercise, readers are asked to repeat the Cochrane-Orcutt estimation using a different dependent variable.