The document discusses various aspects of the reverse charge mechanism under service tax in India. It defines reverse charge mechanism and explains when it came into effect. It lists 12 services to which reverse charge applies and whether it is full or partial reverse charge. It addresses issues around point of taxation, CENVAT credit, valuation, exemptions and compliance requirements. It provides an example of the accounting treatment and invoice format under reverse charge mechanism.

The presentation contains the history of Reverse charge machainism from the date from which it was inroduced and the subsequent amendments. We have added all the services covered under Reverse Charge Mechainism till date. For ease of understanding, we have presented every service in the form of chart and diagrams.

Meaning of the term "Service" in Service tax as per Finance Act, 1994Abhinav Chhabra

A comprehensive analysis of the definition of the term "Service" as per Finance Act, 1994. This presentation will guide about what all are the services that can be liable to service tax subject to other provisions of the Finance Act, 1994.

The presentation contains the history of Reverse charge machainism from the date from which it was inroduced and the subsequent amendments. We have added all the services covered under Reverse Charge Mechainism till date. For ease of understanding, we have presented every service in the form of chart and diagrams.

Meaning of the term "Service" in Service tax as per Finance Act, 1994Abhinav Chhabra

A comprehensive analysis of the definition of the term "Service" as per Finance Act, 1994. This presentation will guide about what all are the services that can be liable to service tax subject to other provisions of the Finance Act, 1994.

This presentation takes you through the basic provisions of Reverse Charge / Joint Charge mechanism introduced w.e.f 1-7-2012. The provisions have wide ramifications as now very few businesses would be able to avoid taking registration with the service tax department.

There are so many changes done by Finance Bill, 2016 in various Act's. Provisions for service tax has also been amended or proposed to be amended. This budget was much awaited because a massive change is awaiting in the form of GST. Looking, to the large number of changes, we have consolidated changes with respect to Service tax in one presentation. Changes are classified according to subject in order to ensure ease of understanding.

If you have any Query you can contact Us

Mail id:- ca.sanjiv.nanda@gmail.com

Youtube Channel :- https://www.youtube.com/channel/UCmmx2GFXeoF-DNtNjwnpYJA

Website :- http://www.sanjivnanda.com/

Facebook link :- https://www.facebook.com/ca.sanjivnanda919/

Twitter :- https://twitter.com/

Presentation on service tax Act 1994, for undergraduate commerce students of Goa University. Includes historical background, year wise tax collection e for last 20 years and procedural aspect of service tax Act 1994 with latest amendments are covered.

Hello Friends ,

This slides contains

1) Service Tax Amendments Finance Act 2016

2) CENVAT Rules Amendments Fiance Act 2016

3) Case Laws-

a) No Service Tax on FLats where value of land is included.

b) No Service Tax Audit by Departmental Person

Back to Basics: VAT invoicing & the reverse chargeAlex Baulf

In this VAT Club "Back to Basics" presentation, Grant Thornton UK LLP's Hugh Doherty & Arsalan Aslam present on valid VAT invoicing, self-billing and the reverse charge.

This presentation takes you through the basic provisions of Reverse Charge / Joint Charge mechanism introduced w.e.f 1-7-2012. The provisions have wide ramifications as now very few businesses would be able to avoid taking registration with the service tax department.

There are so many changes done by Finance Bill, 2016 in various Act's. Provisions for service tax has also been amended or proposed to be amended. This budget was much awaited because a massive change is awaiting in the form of GST. Looking, to the large number of changes, we have consolidated changes with respect to Service tax in one presentation. Changes are classified according to subject in order to ensure ease of understanding.

If you have any Query you can contact Us

Mail id:- ca.sanjiv.nanda@gmail.com

Youtube Channel :- https://www.youtube.com/channel/UCmmx2GFXeoF-DNtNjwnpYJA

Website :- http://www.sanjivnanda.com/

Facebook link :- https://www.facebook.com/ca.sanjivnanda919/

Twitter :- https://twitter.com/

Presentation on service tax Act 1994, for undergraduate commerce students of Goa University. Includes historical background, year wise tax collection e for last 20 years and procedural aspect of service tax Act 1994 with latest amendments are covered.

Hello Friends ,

This slides contains

1) Service Tax Amendments Finance Act 2016

2) CENVAT Rules Amendments Fiance Act 2016

3) Case Laws-

a) No Service Tax on FLats where value of land is included.

b) No Service Tax Audit by Departmental Person

Back to Basics: VAT invoicing & the reverse chargeAlex Baulf

In this VAT Club "Back to Basics" presentation, Grant Thornton UK LLP's Hugh Doherty & Arsalan Aslam present on valid VAT invoicing, self-billing and the reverse charge.

issue 4/2014 of Indirect Tax News.

This newsletter informs readers about issues of practical importance in the field of VAT and similar indirect taxes, such as GST. Experts from all over the world provide first-hand information on recent developments in legislation, jurisdiction and tax authorities’ opinions and Directives.

Service tax reverse charge w.e.f.1 6-2016Rahul Pansari

Comprehensive presentation on Reverse charge mechanism in Service Tax as amended w.e.f. 1st June 2016 in very effective & user-friendly manner.

For any query, pls feel free to contact on 94135-46230.

The Service Tax was payable on receipt basis i.e. on receipt of amount of the invoice or bill from the customer or receipt of advance, whichever is earlier.

With the introduction of POT Rules, general rule for the time of provision of service would be the earliest of the following dates:

a) Date on which service is provided or to be provided

b) Date of invoice

c) Date of payment

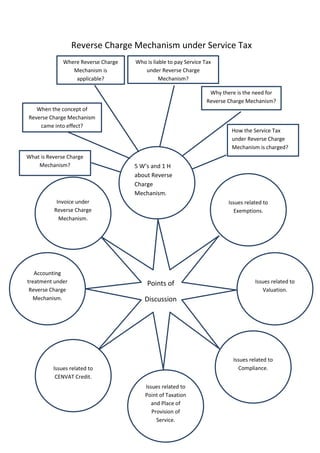

1. Reverse Charge Mechanism under Service Tax

Points of

Discussion

Invoice under

Reverse Charge

Mechanism.

Accounting

treatment under

Reverse Charge

Mechanism.

Issues related to

CENVAT Credit.

Issues related to

Point of Taxation

and Place of

Provision of

Service.

5 W’s and 1 H

about Reverse

Charge

Mechanism.

Issues related to

Compliance.

Issues related to

Valuation.

Issues related to

Exemptions.

Who is liable to pay Service Tax

under Reverse Charge

Mechanism?

How the Service Tax

under Reverse Charge

Mechanism is charged?

What is Reverse Charge

Mechanism?

Why there is the need for

Reverse Charge Mechanism?

Where Reverse Charge

Mechanism is

applicable?

When the concept of

Reverse Charge Mechanism

came into effect?

2. 5 W’s and 1 H about Reverse Charge Mechanism under Service Tax.

What is Reverse Charge Mechanism?

o Generally, service tax is payable by person providing the service [Section 68(1)].

o Section 68(2) of the Finance Act, 1994 makes provision for reverse charge i.e. making

person receiving the service to pay service tax (Tax Shifting).

o Provision can be made that part of the tax will be paid by the service receiver and part by

the service provider i.e. Concept of Partial Reverse Charge.

When the concept of Reverse Charge Mechanism came into effect?

o With effect from July 1, 2012, a new taxation scheme for the service sector came into

effect, which states that both the service provider and service recipient must pay the

requisite service tax. Prior to this, the liability to pay such tax was only born by either the

service provider or the service recipient.

Where Reverse Charge Mechanism is applicable?

o Reverse Charge Mechanism is applicable in case of taxable services that are notified by the

Central Government in the notification no. 30/2012-ST.

o There are 12 services under Reverse Charge Mechanism out of which 4 services are

covered under Partial Reverse Charge Mechanism.

Who is liable to pay Service Tax under Reverse Charge Mechanism?

o Rule 2(1)(d) of the service tax rules, 1994 read with notification no. 30/2012-ST.

o In case of Full Reverse Charge Mechanism, the liability to pay service tax is of the service

recipient, whereas in case of Partial Reverse Charge Mechanism part liability is of service

provider and part is of recipient of service.

o Percentage of service tax payable by service provider and service recipient is different for

different services.

Why there is the need for Reverse Charge Mechanism?

o The only sole reason for Reverse Charge Mechanism is to prevent the revenue loss to the

government as in the notified services it was difficult to trace the service providers.

How the Service Tax under Reverse Charge Mechanism is charged?

o Service tax is levied as per section 66B of the Finance Act, 1994 at the rate 12% of the

value determined u/s 67 read with rules made thereunder.

o Service tax is levied on all services other than those specified in the negative list. (Services

to be provided are also covered un sec. 66B)

o Service tax is an indirect tax levied by service provider on the service recipient. Service

provider collects service tax from service receiver and pays to Govt. itself / himself.

o Under Reverse Charge Mechanism, the position becomes reverse. Instead of tax being

paid by service provider, service receiver has to deposit tax in Govt. account.

3. Various aspects about the services notified in the notification 30/2012-ST dated 20-06-2012.

Sr

No.

Description of

Service

Service

Provider

Service

Recipient

Percentage of

Service Tax payable

by

Effective date and

POPS Rule.

Service

Provider

Service

Recipient

1

Service of Arbitral

Tribunal

Arbitral

Tribunal

Any Business

Entity located in

taxable territory

Nil 100%

Not. No. 25/2012-ST,

dated June 20, 2012.

POPS

Rule 8 if not, Rule 3.

Business Entity [Sec 65B(17)] : Business Entity mean any person ordinarily carrying out any activity relating to

industry, commerce or any other business or profession.

2

Service provided

by the Director of

the company to

the said company

Director Said Company Nil 100%

Effective from

August 7, 2012 thru

Not. No. 45/2012-ST,

POPS

Rule 8 if not, Rule 3.

Service tax is payable in on services provided by non – executive, nominee and independent directors.

Managing director, wholetime director and executive directors are not covered.

3

Support Services

by Government or

local authority

excluding,-

(a) Renting of

Immovable

Property [Rule

2(1)(f) of ST

Rules, 1994]

(b) Services

specified u/s

66d(a)(i),(ii)

and (iii)

Govt .or local

authority

Any Business

Entity located in

taxable territory

Nil 100%

Not. No. 30/2012-ST,

dated June 20, 2012.

POPS

Depends upon type

of services rendered.

(No Specific Rule).

4 Goods Transport

Agency by way of

transport of goods

by road in a goods

carriage.

Goods

Transport

Agency

Where person

liable to pay

freight is-

(a) Registered

factory

(b) Registered

society

(c) Co-op.

Society

established

by or undue

any law

(d) Registered

dealer of

excisable

goods

(e) Body

corporate

Nil 100%

Not. No. 33/2004-ST,

dated January 1,

2005. (Amended by

FA 2012)

POPS

Rule 10

4. established

by or undue

any law

(f) Partnership

firm(includi

ng AOP and

LLP)

And such

person is

located in

taxable

territory.

5

Insurance auxiliary

service

Insurance

Agent

Any person

carrying on

insurance

business

Nil 100%

Not. No. 36/2004-ST,

dated 31.12.2004.

(Amended by FA

2102)

POPS

Rule 9(c).

6

Legal Services

[Rule 2(1)(cca) of

ST rules, 1994.

Individual

advocate or

a firm of

advocate

Any business

entity located in

taxable territory

Nil 100%

Not. No. 25/2012-ST,

dated June 20, 2012.

POPS

Rule 8 if not, Rule 3.

7 Sponsorship

Any person

by way of

Sponsorship

Any body

corporate or

partnership firm

(including LLP)

Nil 100%

Not. No. 30/2012-ST

Amended, dated

June 20, 2012.

POPS

Rule 8 if not, Rule 7 if

not, Rule 6.

8 Security Service

Any

Individual or

HUF or

Partnership

firm

(including

LLP and AOP)

Located in

taxable

territory

A business

entity registered

as body

corporate and

located in

taxable territory

25% 75%

Not. No. 30/2012-ST,

dated June 20,2012

POPS

Rule 8 if not, Rule 3.

9

Supply of

manpower

25% 75%

10

Service portion in

execution of

works contract

50% 50%

11

Renting of a motor

vehicle designed

to carry

passengers -

(i) on abated value

(ii) on non- abated

value

Nil 100%

60% 40%

12 Any Service

Person

located

outside

taxable

territory

Person located

within taxable

territory

Nil 100%

POPS

Rule 8 if not, Rule 3.

5. Issues related to Exemptions/ Valuation

(a) Is Service Recipient liable to pay his share of service tax under reverse charge mechanism when

basic exemption limit of Rs. 10 Lacs is available to service provider under notification no. 33/2012-

ST?

In case the service provider is availing exemption under notification no. 33/2012-ST then he is

not be obliged to pay any tax. However, service recipient shall have to pay service tax to the

extent of his service tax liability under partial reverse charge mechanism.

(b) Whether service receiver can avail SSI exemption limit?

No, the service recipient cannot avail SSI exemption while discharging service tax liability

under reverse charge in terms of notification no. 33/2012-ST.

(c) Service Provider has not availed abatement which is legally available or chooses different valuation

option and prepared the invoice. Can service recipient claim such abatement or chooses different

method of valuation for payment of service tax under reverse charge mechanism?

It is being provided by way of explanation in the notification no. 33/2012-ST that service

provider and service recipient are different and independent of each other. The service

recipient can independently avail or forgo abatement or choose a valuation option, which is

independent of service provider.

Issues related to compliance

(a) A service recipient is liable to pay service tax under reverse charge mechanism. However, he does

not want to get service tax registration and tells his supplier of service to charge service tax and

pay it to the service tax department. Can he do so?

Section 69(2) made it mandatory to get registration.

(b) If a service provider is registered with the service tax department and now is liable to pay service

tax under reverse charge mechanism, is he required to take new existing registration?

No, registration is required to be done only once, but it has to be intimated that the tax is

being paid as service recipient.

Issues related to Point of Taxation

What is the point of taxation for service tax liability under reverse charge mechanism?

Generally as per rule 3 of Point of Taxation Rules, 2011, Point of Taxation for service

provider would be earliest of :- Date of invoice or date of receipt of payment. Incase where

invoice is not issued with 30 days from date of receipt of payment or date of completion of

service, whichever is earlier then point of taxation would be earliest of following i.e. date of

receipt of payment or date of completion of service.

However, in case of Reverse Charge Mechanism, date of payment is the point of taxation.

If payment not made within 6 months of the date of invoice, Point of taxation is determined as

per rule 3.

6. Issues related to CENVAT Credit.

(a) Can CENVAT credit be utilised by service recipient to discharge the liability of service tax under

reverse charge mechanism?

As per Rule 3(4) of CENVAT Credit Rules, 2004, the service recipient cannot use CENVAT credit

balance to pay tax under reverse charge. Such tax is to be paid in cash using GAR-7 challan.

(b) Can CENVAT credit be availed for service tax paid as recipient under reverse charge?

Yes, under reverse charge only payment burden is shifted rest remains the same.

(c) Due to partial reverse charge, a service provider has excess CENVAT credit compared to his

service tax liability. What can service provider do with this credit?

As per rule 5B of the CENVAT Credit Rules, 2004, a service provider notified under section

68(2) of the Finance Act and being unable to utilise the CENVAT Credit availed on inputs and

input services for payment of service tax shall be allowed refund of such unutilised amount.

(d) A portion of the service tax is to be paid by the service provider under reverse charge and the rest

of the service tax is duly charged by the service provider in its invoice. Which is the document on

basis of which CENVAT credit can be taken?

On the basis of invoice for the service provider’s portion and copy of GAR-7 challan for service

recipient’s portion.

Accounting treatment under Reverse Charge Mechanism.

Accounting Entries – Service Receiver Books

(Example. Service Value – Rs.10000 and SP-25% and SR- 75%)

At the time of payment to service provider:

Expenses A/c. Dr.

ST Input Credit (ST)A/c. Dr.

ST Input Credit (Edu.Cess)A/c. Dr.

ST Input Credit (SHEC)A/c. Dr.

ST Deferred Input Credit(ST)A/c. Dr.

ST Deferred Input Credit(Edu.Cess)A/c. Dr.

ST Deferred Input Credit (SHEC)A/c. Dr.

To Bank A/c.

To ST payable(ST)A/c.

To ST payable(Edu.Cess)A/c.

To ST payable(SHEC)A/c.

10000

300

6

3

900

18

9

10309

900

18

9

7. At the time of payment of Service Tax

(a) Service Tax Payment

ST payable(ST)A/c. Dr.

ST payable(Edu.Cess)A/c. Dr.

ST payable(SHEC)A/c Dr.

To Bank

900

18

9

927

(b) Service Tax eligible CENVAT

ST Input Credit(ST)A/c. Dr.

ST Input Credit(Edu.Cess)A/c. Dr.

ST Input Credit(SHEC)A/c. Dr.

To ST Deferred Input Credit(ST)A/c.

To ST Deferred Input Credit(Edu.Cess) A/c.

To ST Deferred Input Credit(SHEC) A/c .

900

18

9

900

18

9

Invoice under Reverse Charge Mechanism

All contains of the Rule 4A of Service Tax Rules, 1994 will remain same except for minor difference in

the manner of presentation of service tax liability.

Following is specimen of invoice under reverse charge.

ABC Ltd

Nagpur – 440001

Service Tax Regn No.: Date:

PAN:

Client Name:

Client Address:

Particulars Amount Amount

Manpower Service

Add: Service Tax @12%

E.Cess @2%

S.H.E.Cess @1%

Total

Total Service Tax Amount

Less: Service provider’s share @25%

Service Receiver’s share @75%

Net Amount Payable

-sd-

(Authorised signatory)

1236.00

309.00

10000.00

1200.00

24.00

12.00

11236.00

-927.00927.00

10309.00

![ 5 W’s and 1 H about Reverse Charge Mechanism under Service Tax.

What is Reverse Charge Mechanism?

o Generally, service tax is payable by person providing the service [Section 68(1)].

o Section 68(2) of the Finance Act, 1994 makes provision for reverse charge i.e. making

person receiving the service to pay service tax (Tax Shifting).

o Provision can be made that part of the tax will be paid by the service receiver and part by

the service provider i.e. Concept of Partial Reverse Charge.

When the concept of Reverse Charge Mechanism came into effect?

o With effect from July 1, 2012, a new taxation scheme for the service sector came into

effect, which states that both the service provider and service recipient must pay the

requisite service tax. Prior to this, the liability to pay such tax was only born by either the

service provider or the service recipient.

Where Reverse Charge Mechanism is applicable?

o Reverse Charge Mechanism is applicable in case of taxable services that are notified by the

Central Government in the notification no. 30/2012-ST.

o There are 12 services under Reverse Charge Mechanism out of which 4 services are

covered under Partial Reverse Charge Mechanism.

Who is liable to pay Service Tax under Reverse Charge Mechanism?

o Rule 2(1)(d) of the service tax rules, 1994 read with notification no. 30/2012-ST.

o In case of Full Reverse Charge Mechanism, the liability to pay service tax is of the service

recipient, whereas in case of Partial Reverse Charge Mechanism part liability is of service

provider and part is of recipient of service.

o Percentage of service tax payable by service provider and service recipient is different for

different services.

Why there is the need for Reverse Charge Mechanism?

o The only sole reason for Reverse Charge Mechanism is to prevent the revenue loss to the

government as in the notified services it was difficult to trace the service providers.

How the Service Tax under Reverse Charge Mechanism is charged?

o Service tax is levied as per section 66B of the Finance Act, 1994 at the rate 12% of the

value determined u/s 67 read with rules made thereunder.

o Service tax is levied on all services other than those specified in the negative list. (Services

to be provided are also covered un sec. 66B)

o Service tax is an indirect tax levied by service provider on the service recipient. Service

provider collects service tax from service receiver and pays to Govt. itself / himself.

o Under Reverse Charge Mechanism, the position becomes reverse. Instead of tax being

paid by service provider, service receiver has to deposit tax in Govt. account.](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)