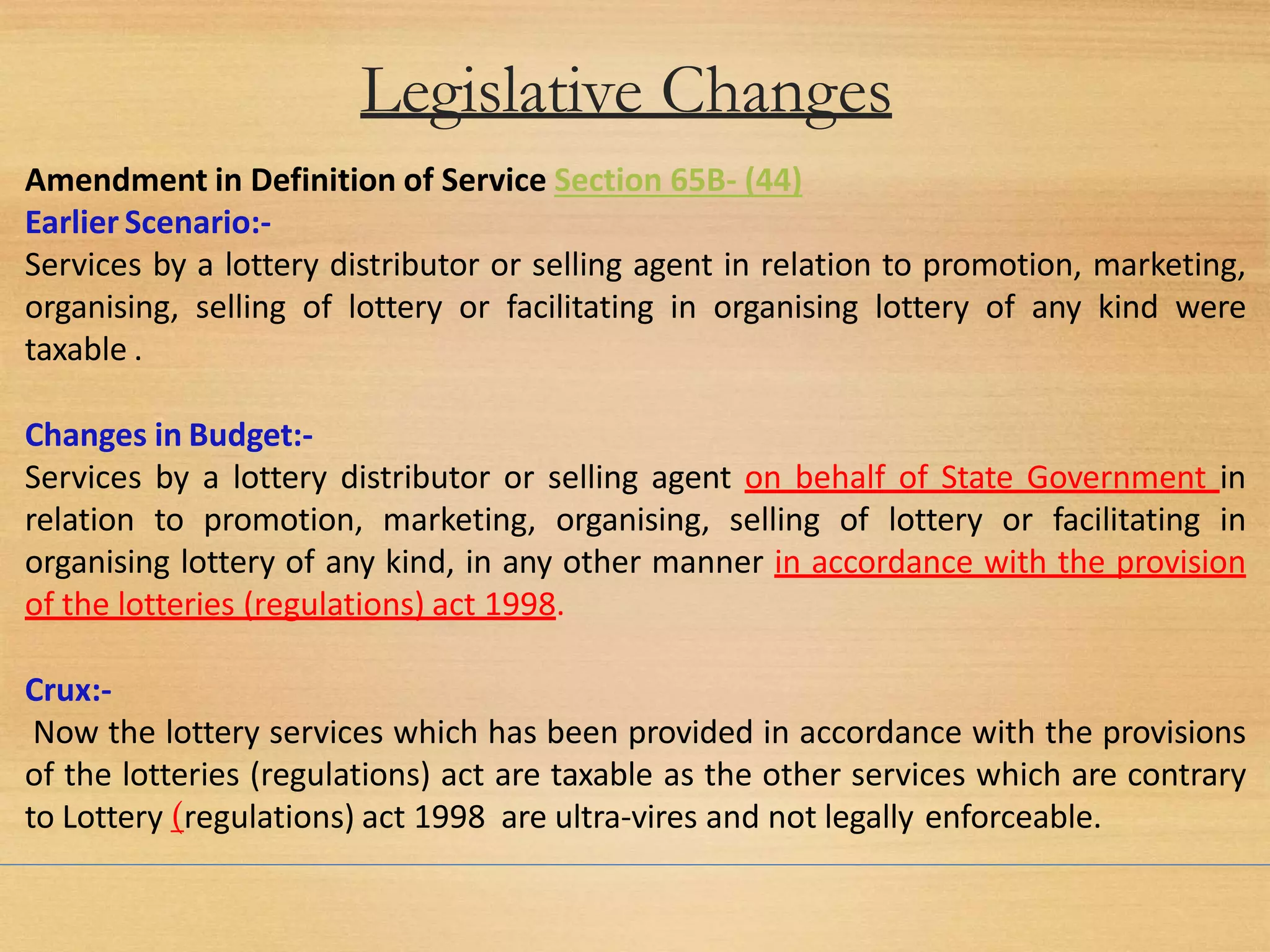

The petitioners challenged the levy of service tax on construction of residential complexes, arguing that it amounts to taxation of immovable property, which is not within the legislative competence of Parliament. The Revenue argued that construction involves various taxable services. The court held that while construction involves both goods and services, the dominant nature is transfer of immovable property and hence service tax cannot be levied. It ruled the levy was beyond Parliament's legislative competence.

![Changes

Section 73-

“Recovery of Service tax not levied or paid or short levied or short paid

or erroneously refunded”

Where any service tax has not been levied or paid or has been short-levied

or short-paid or erroneously refunded, the 4[Central Excise Officer] may,

within ‘eighteen months’ from the relevant date, serve notice on the person

chargeable with the service tax which has not been levied or paid or which

has been short-levied or short-paid or the person to whom such tax refund

has erroneously been made, requiring him to show cause why he should not

pay the amount specified in the notice

Changes in Budget:-

In the 1994 Act, in section 73,––

(i) in sub-sections (1), (1A), (2A) and (3), for the words “eighteen months”,

wherever they occur, the words “thirty months” shall be substituted;

Effect:- The normal period of SCN would be 30 months and the extended period

would continue to be 5years.](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-12-2048.jpg)

![Suresh Kumar Bansal Vs. Union of India & Ors;

Anuj Goyal & Ors Vs. Union of India & Others [2016-TIOL-1077-HC-DEL-ST]

Facts & Ground:-

• Petitioners entered into into a composite contract for purchase of flats with M/s

Sethi Buildwell Pvt. Ltd. In housing project

• Builder recovered Service tax apart from consideration on the services ‘in relation to

construction of complex’ as defined under Section 65(105)(zzzh) of the Finance Act,

1994 (“the Finance Act”)

• Being aggrieved, the Petitioners filed Petitions before the High Court of Delhi.

Petitioners’ contentions:-

• The entries relating to taxation in List I and List II of the Seventh Schedule to the

Constitution of India were mutually exclusive and the Parliament did not have the

power to levy tax on immovable property; thus beyond the legislative competence of

the Parliament;

• Their Agreement is a composite contract and in absence of specific provisions for

ascertaining the service component of the said Agreement, the levy would be beyond

the legislative competence of the Parliament;](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-18-2048.jpg)

![Suresh Kumar Bansal Vs. Union of India & Ors;

Anuj Goyal & Ors Vs. Union of India & Others [2016-TIOL-1077-HC-DEL-ST]

Revenue’s Contention:-

• Development of a project results in the substantial value addition on bare land and

includes various services such as consulting services, engineering services,

management services, architectural services, These services are subsumed in the

taxable service as contemplated under Section 65(105)(zzzh) of the Finance Act.

• Taxable value is only 25% due to abatement available (Nt 1/2006)

Court’s Observation:-

• No impinges on the legislative field reserved for the States under Entry-49 of List-II

of the Seventh Schedule to the Constitution of India The imposition of Service tax

by virtue of the impugned explanation is not a levy on immovable property as

contended.

• While the legislative competence of the Parliament to tax the element of service

involved cannot be disputed but the levy itself would fail, if it does not provide for a

mechanism to ascertain the value of the services component which is the subject of

the levy.](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-19-2048.jpg)

![Suresh Kumar Bansal Vs. Union of India & Ors;

Anuj Goyal & Ors Vs. Union of India & Others [2016-TIOL-1077-HC-DEL-ST]

Court’s Observation continue………

• None of the Rules under the Service Tax (Determination of Value) Rules, 2006 (“the

Service Tax Valuation Rules”), cater to determination of value of services in case of a

composite contract which involves sale of land.

• The abatement to the extent of 75% by a notification or a circular cannot substitute

the lack of statutory machinery provisions to ascertain the value of services involved

in a composite contract.

Comment

• From July 2012, all services except specified in the Negative List, were subjected to

service tax.

• However, the Act and Rules pertaining to service tax do not contain any provision for

exclusion of value of land.

• An abatement is provided vide a Notification and, therefore, the legal situation from

July 2012 till date is exactly same as was there in the above judgment.](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-20-2048.jpg)

![Insertions

Section 67A-

67A. The rate of service tax, value of a taxable service and rate of exchange,

if any, shall be the rate of service tax or value of a taxable service or rate

of exchange, as the case may be, in force or as applicable at the time

when the taxable service has been provided or agreed to be provided.

Changes in Budget:-

In the 1994 Act, in section 67A, the [existing section] shall be renumbered as

sub-section (1)

and after sub-section (1), the following sub-section shall be inserted,

“(2) The time or the point in time with respect to the rate of service tax shall

be such as may be prescribed.”.

(Point of time with respect to the rate is prescribed in Point of Taxation

Rules,2011)

Effect:- To decide about the applicability of service tax rate, POTR has to be

referred and apparent contradiction b/w Sec. 67A and POTR has been

removed.](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-26-2048.jpg)

![Section 78A-

“Where a company has committed any of the [given] contraventions

then any director, manager, secretary or other officer of such company,

who at the time of such contravention was in charge of, and was

responsible to, the company for the conduct of business of such

company and was knowingly concerned with such contravention, shall

be liable to a penalty which may extend to one lakh rupees:—”

Changes in Budget:-

In the 1994 Act, in section 78A, the following Explanation shall be

inserted, namely:––

“Explanation.–– It is proposed that penalty proceedings under

section 78A shall be deemed to be closed in case where the main

demand and the penalty proceedings have been closed u/s 76 or 78.](https://image.slidesharecdn.com/servicetaxcavijaymaheshwari-160623160002/75/Recent-Amendments-in-Service-Tax-27-2048.jpg)