Downloaded 428 times

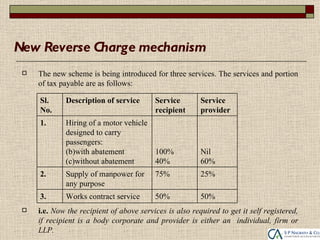

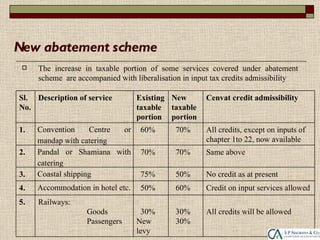

The document summarizes key changes to India's service tax laws effective July 1, 2012. Key points include: 1) The service tax rate increased from 10% to 12% and the system shifted from a positive to a negative list. 2) Many services were exempted from tax and new sections were introduced to define taxable services and the place of provision. 3) A reverse charge mechanism was introduced for three specified services and the abatement scheme was modified. 4) Procedural amendments included changes to invoicing rules, cenvat credit, and limitations periods.