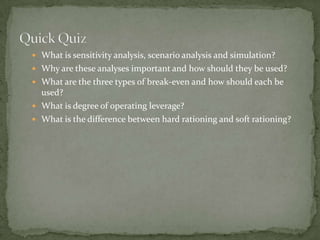

![ What is the operating cash flow at the accounting break-even point

(ignoring taxes)?

OCF = (S – VC – FC - D) + D

OCF = (200*25,000 – 200*15,000 – 1,000,000 -1,000,000) + 1,000,000 =

1,000,000

What is the cash break-even quantity?

OCF = [(P-v)Q – FC – D] + D = (P-v)Q – FC

Q = (OCF + FC) / (P – v)

Q = (0 + 1,000,000) / (25,000 – 15,000) = 100 units](https://image.slidesharecdn.com/presentation1-130306145447-phpapp01/85/Project-Profitability-Analysis-and-Evaluation-19-320.jpg)

This document discusses various techniques for evaluating project profitability, including net present value estimates, scenario analysis, break-even analysis, operating leverage, and capital rationing. It provides examples and explanations of how to conduct sensitivity analysis on variables, analyze best-case and worst-case scenarios, calculate accounting, cash, and financial break-even points, determine degree of operating leverage, and assess capital rationing constraints. The goal is to understand risks and potential outcomes of projects through quantitative analysis before making investment decisions.

![1. Payback Period and Net Present Value[LO1, 2] If a project with .docx](https://cdn.slidesharecdn.com/ss_thumbnails/1-221101035238-1d86b81e-thumbnail.jpg?width=640&height=640&fit=bounds)

![Ent ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/entppt1-190502205922-thumbnail.jpg?width=640&height=640&fit=bounds)

![Ent ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/entppt1-190502210300-thumbnail.jpg?width=640&height=640&fit=bounds)