Downloaded 181 times

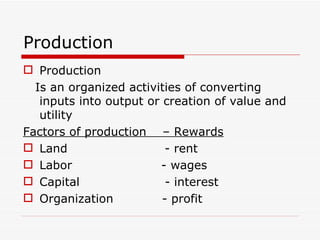

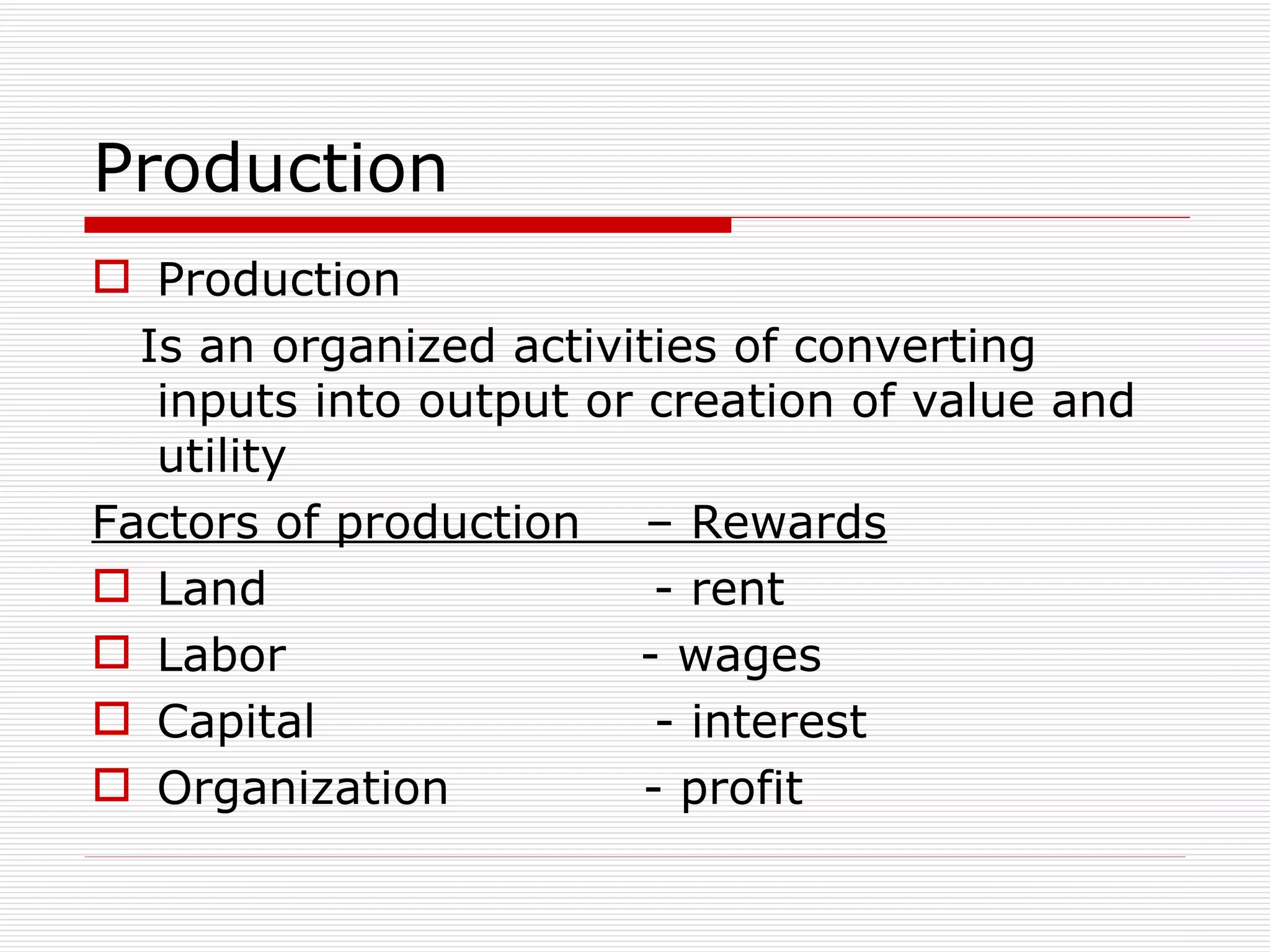

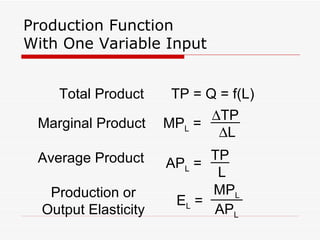

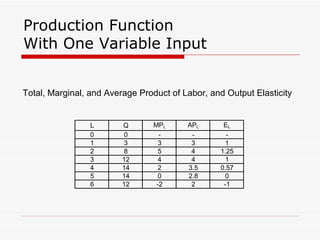

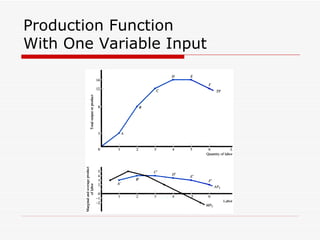

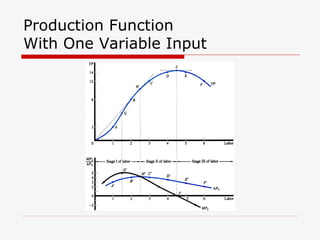

The document discusses various concepts related to production and costs, including: 1. Production involves converting inputs into outputs through organized activities to create value and utility. The main factors of production are land, labor, capital, and organization. 2. Production functions show the relationship between physical inputs and outputs. Total, marginal, and average product are discussed for functions with one variable input like labor. 3. Optimal use of variable inputs occurs when marginal revenue product equals marginal resource cost. Production with two inputs is discussed using isoquants and isocost lines.