The document provides responses to 4 questions regarding adjustments to final accounts for construction projects based on the PAM Contract 2006.

Question 1 summarizes the key elements that must be adjusted in a final account, including variations, remeasurement of provisional quantities, omission of prime costs and provisional sums, addition of NSC and NS final accounts, adjustment of profits and attendance, adjustment of provisional sums based on actual expenditure, and claims for additional expenses and loss.

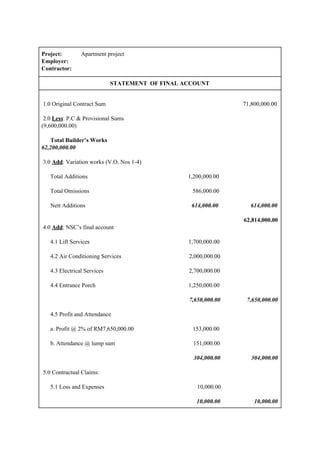

Question 2 discusses the implications of omitting an entrance porch from the tender documents that was later added as a variation, including its treatment as an additional provisional sum and the process for including its cost in interim certificates and adjusting the final contract sum.