Downloaded 174 times

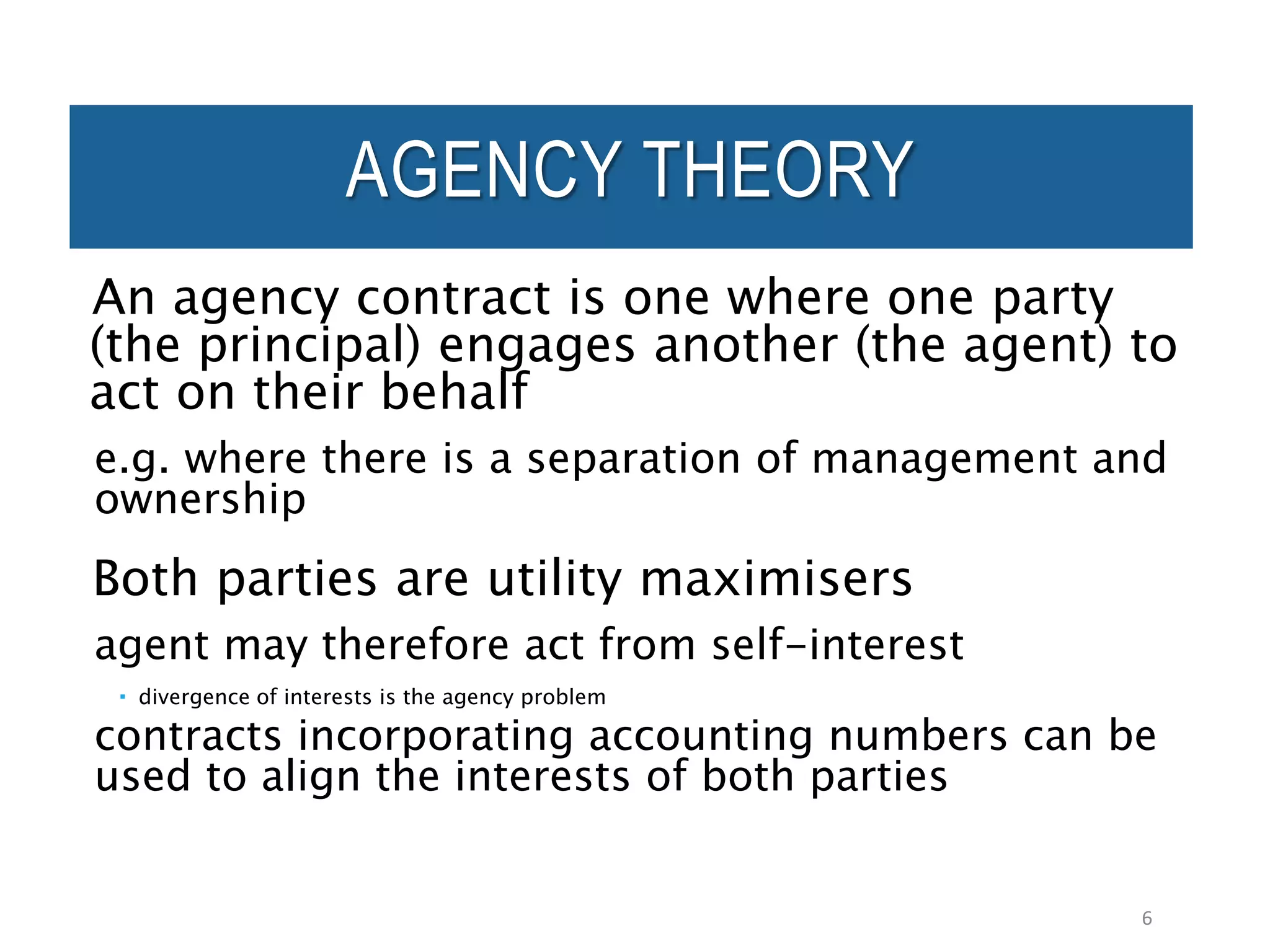

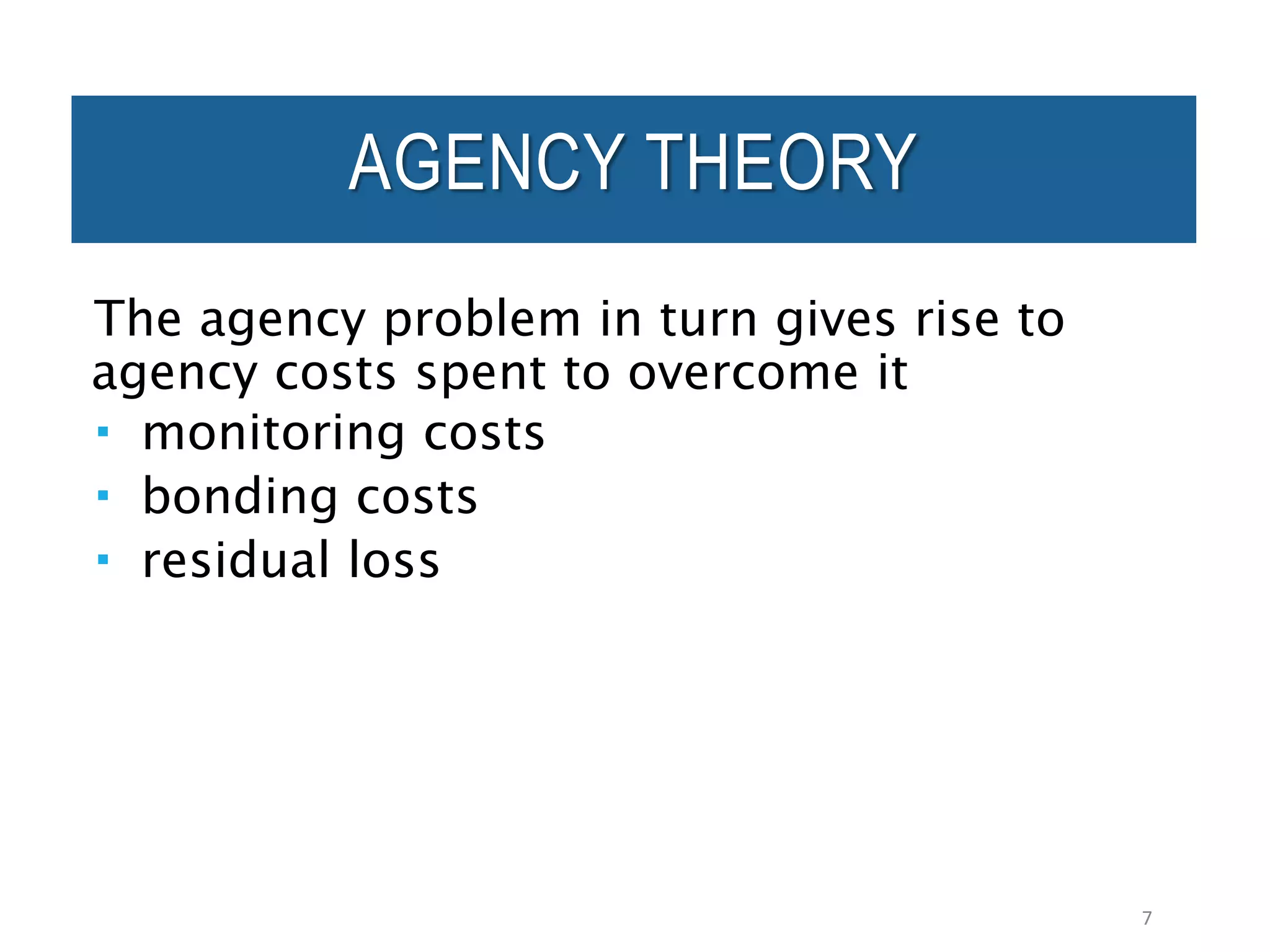

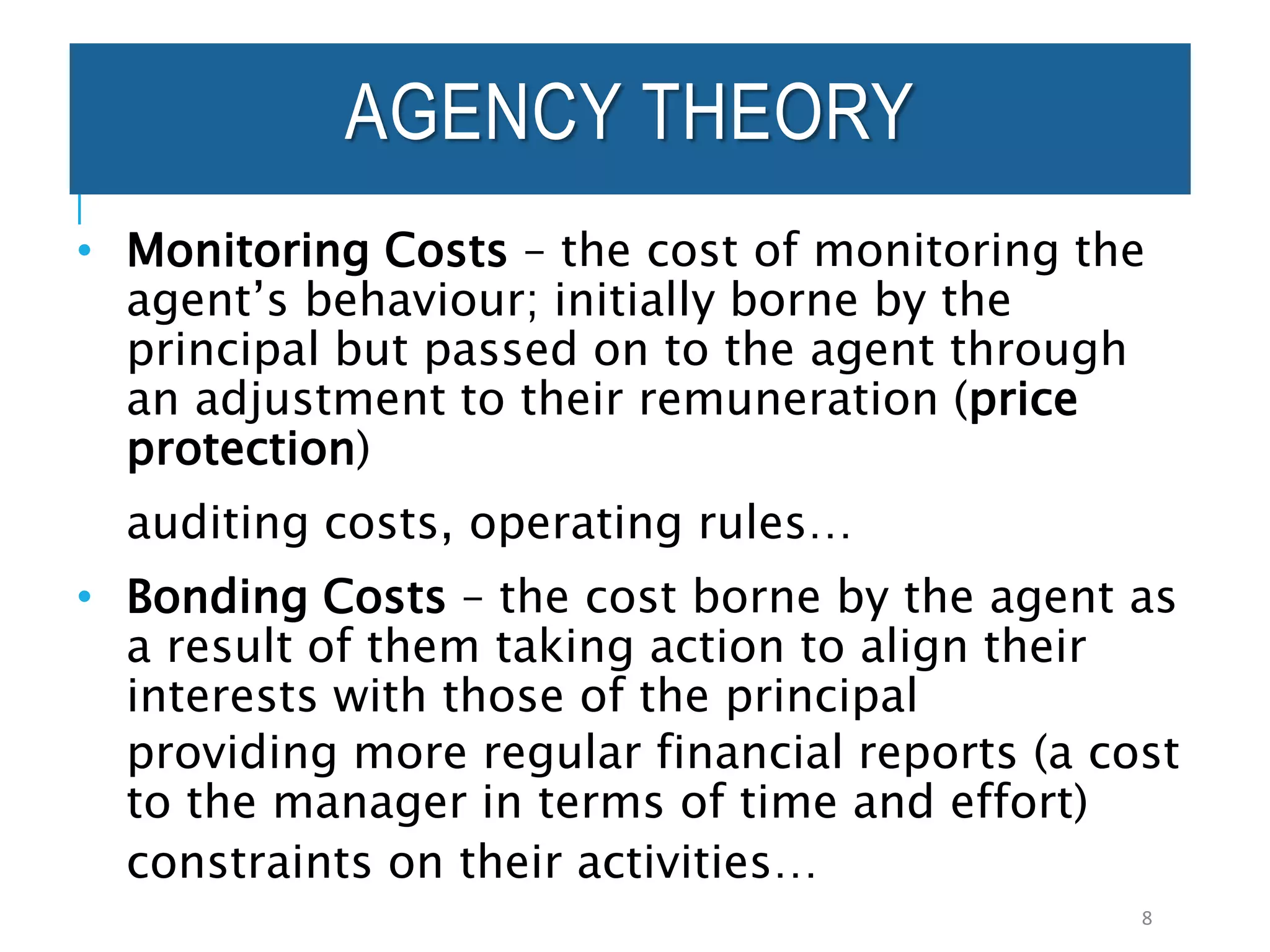

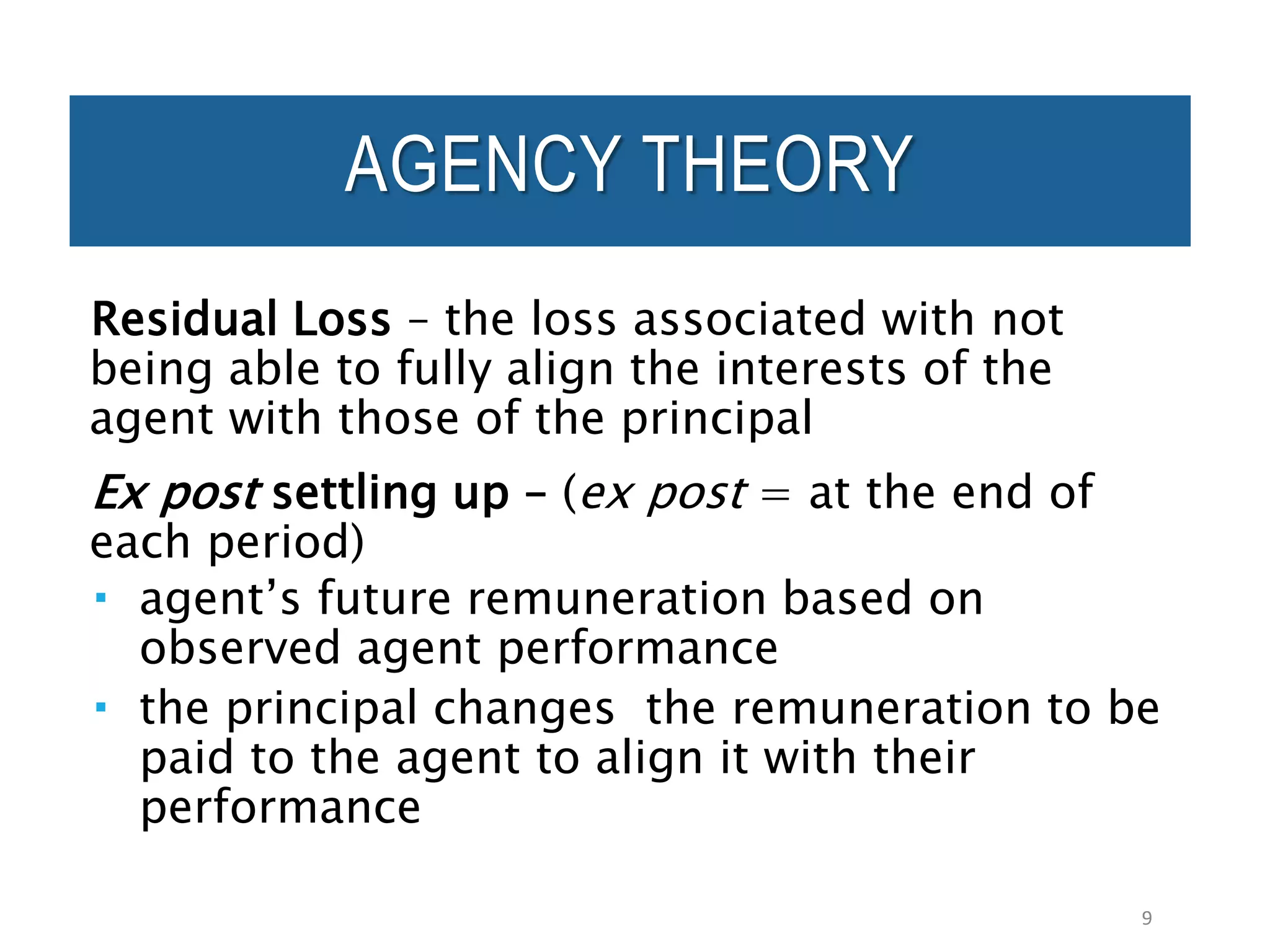

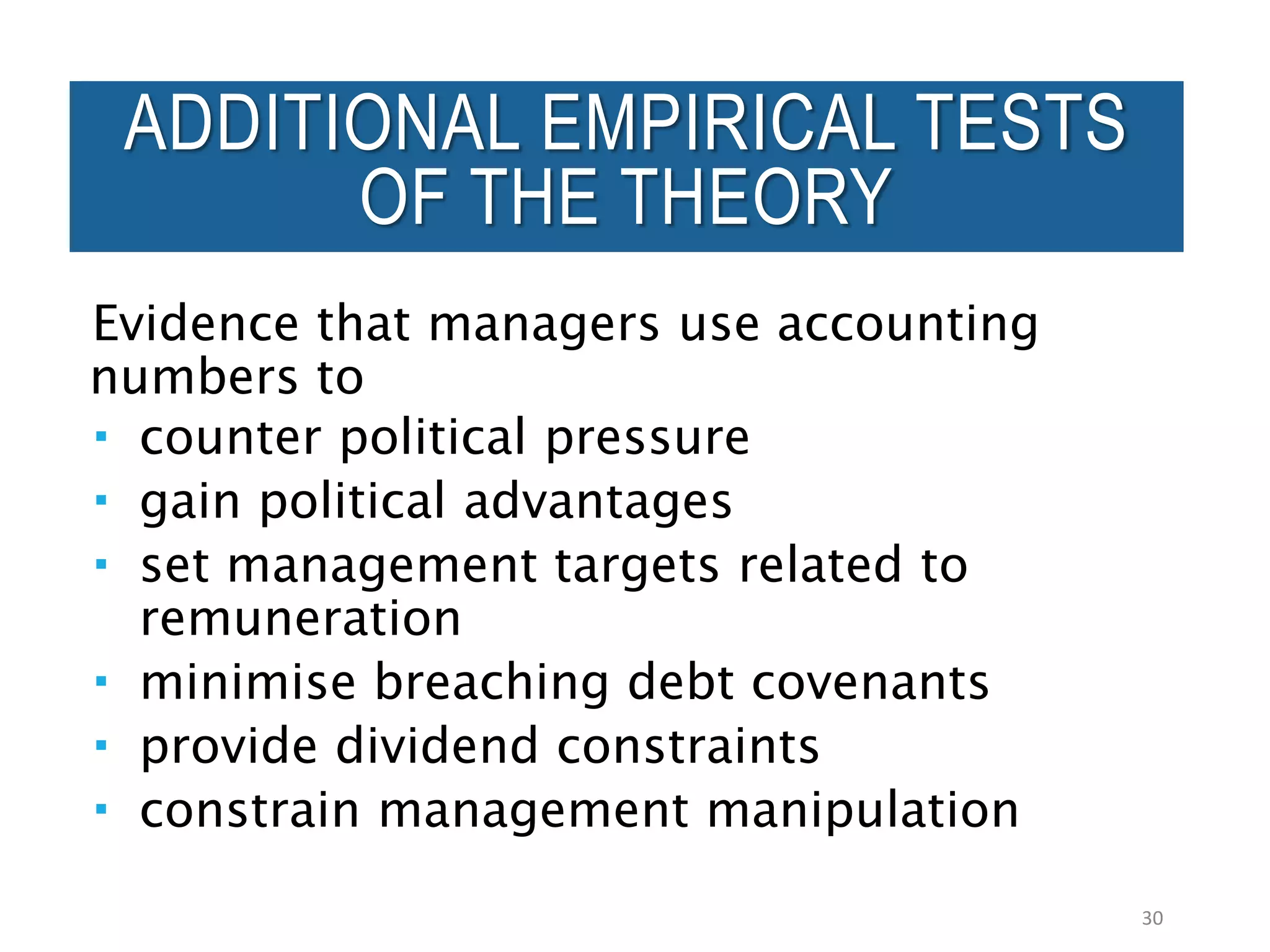

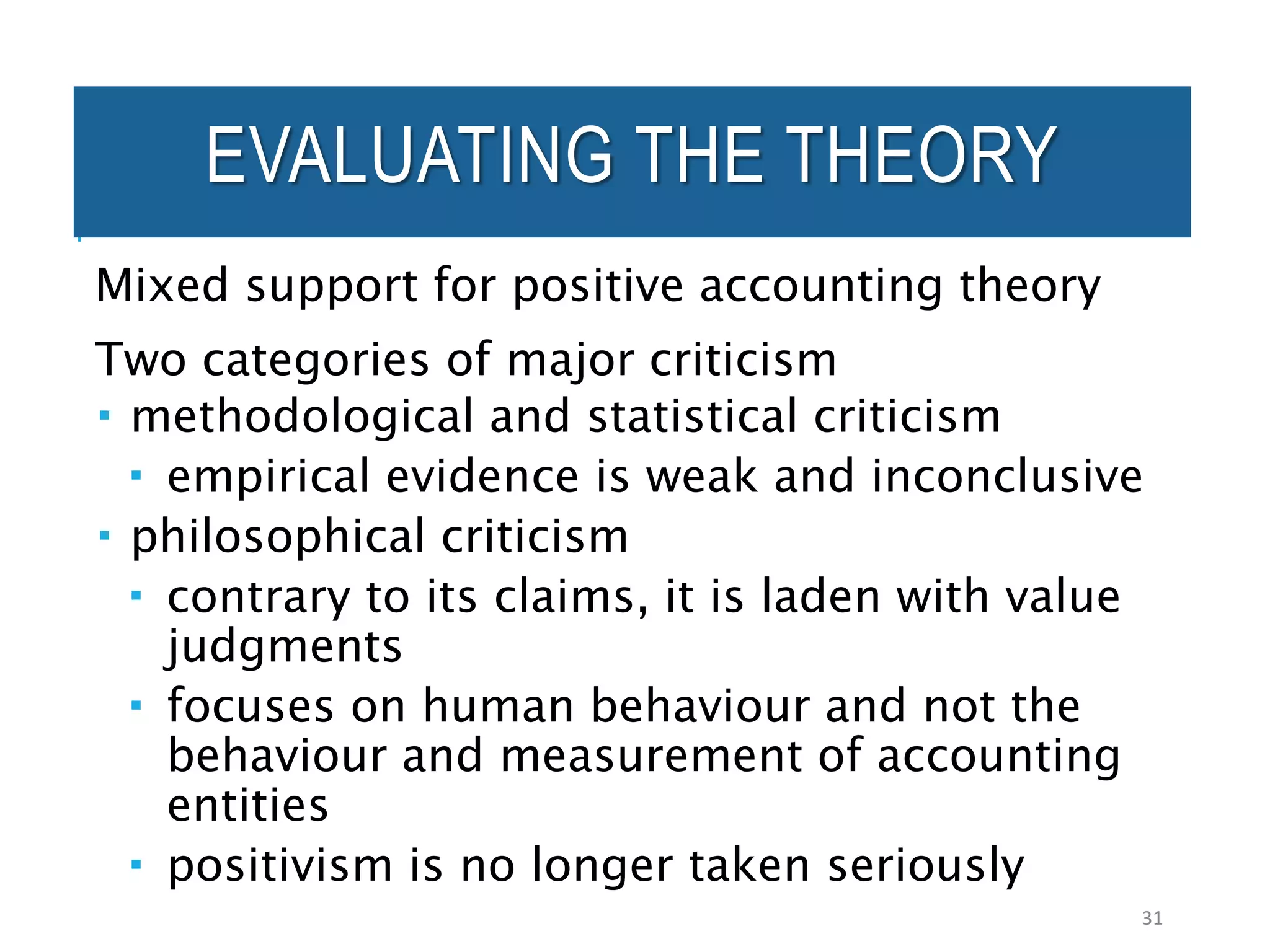

Positive accounting theory sees the firm as a nexus of contracts between shareholders, managers, and debtholders. Agency theory and contracting theory explain how accounting is used to reduce agency costs that arise from the conflicts of interests between these parties. Accounting numbers are incorporated into contracts to monitor managers' behavior and align their interests with shareholders. However, empirical evidence for positive accounting theory has been mixed and inconclusive. It has also been criticized for focusing more on human behavior rather than the measurement of accounting entities.