Downloaded 54 times

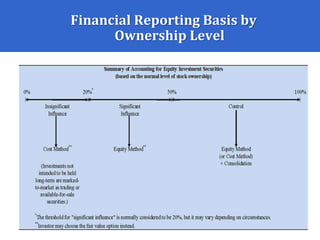

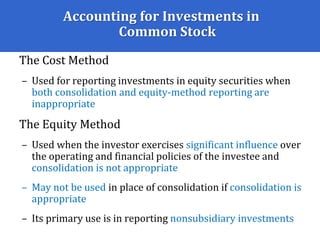

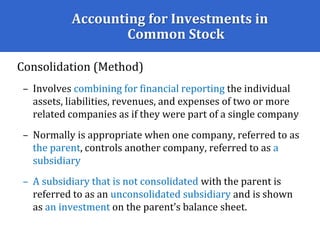

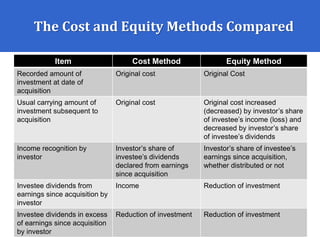

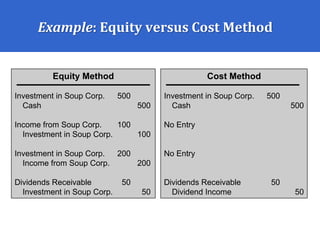

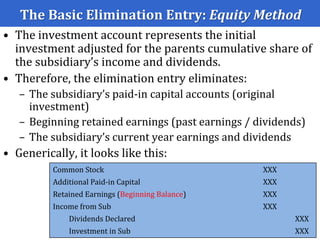

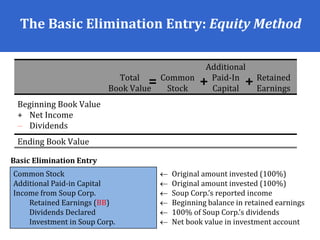

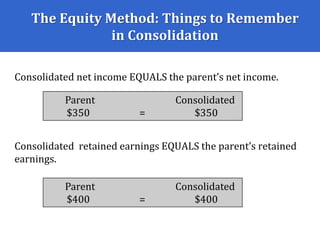

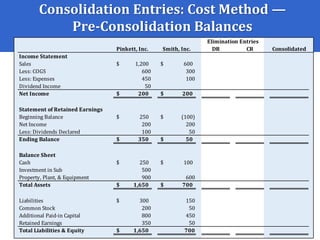

The accounting method used to record investments in common stock depends on the level of influence or control the investor has over the investee. For investments with no significant influence, the cost method is used, where the investment is recorded at cost and income is only recognized through dividends. The equity method is used for investments where significant influence exists, and the investment is adjusted each period for the investor's share of earnings or losses and dividends.