Downloaded 1,183 times

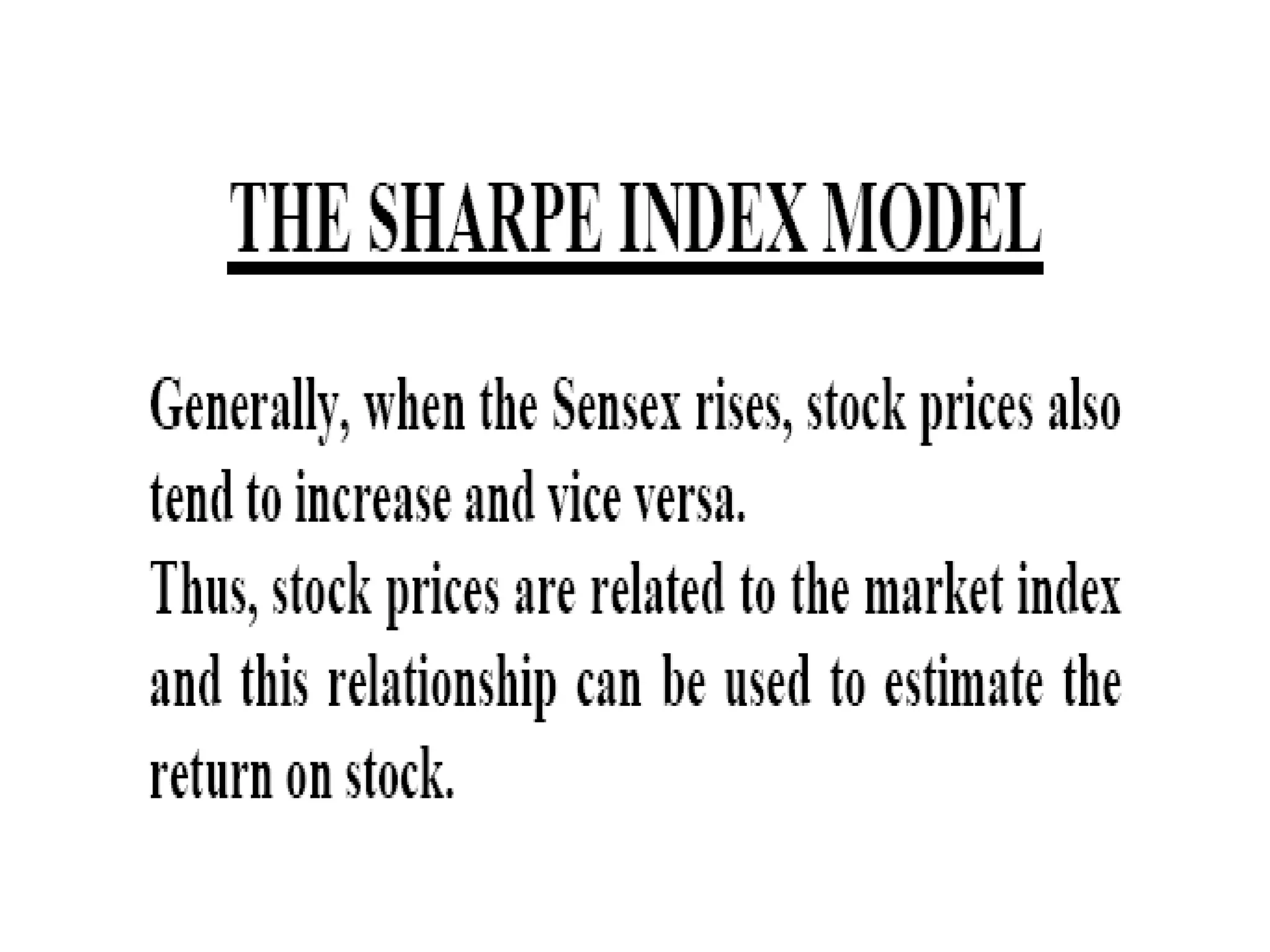

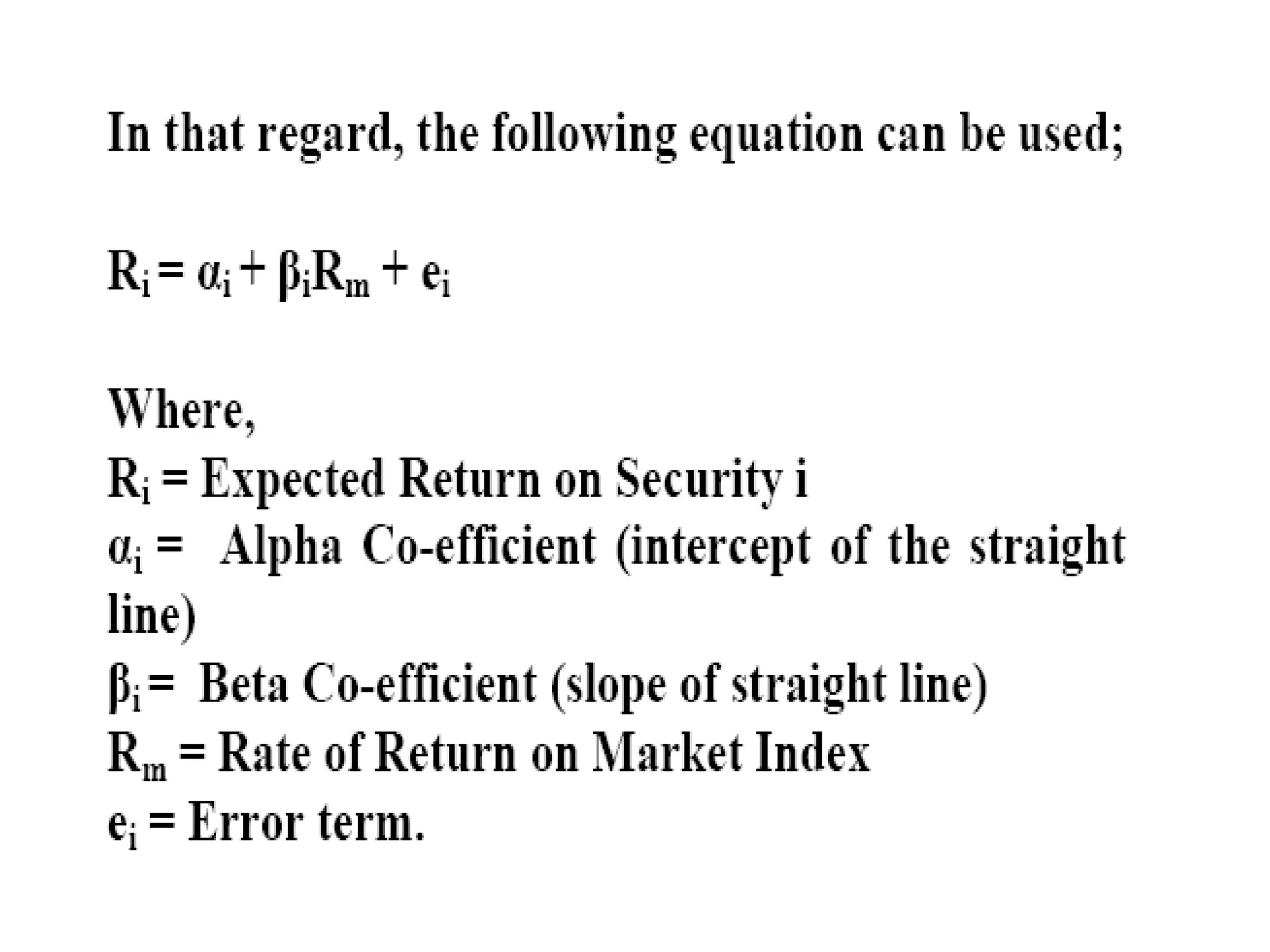

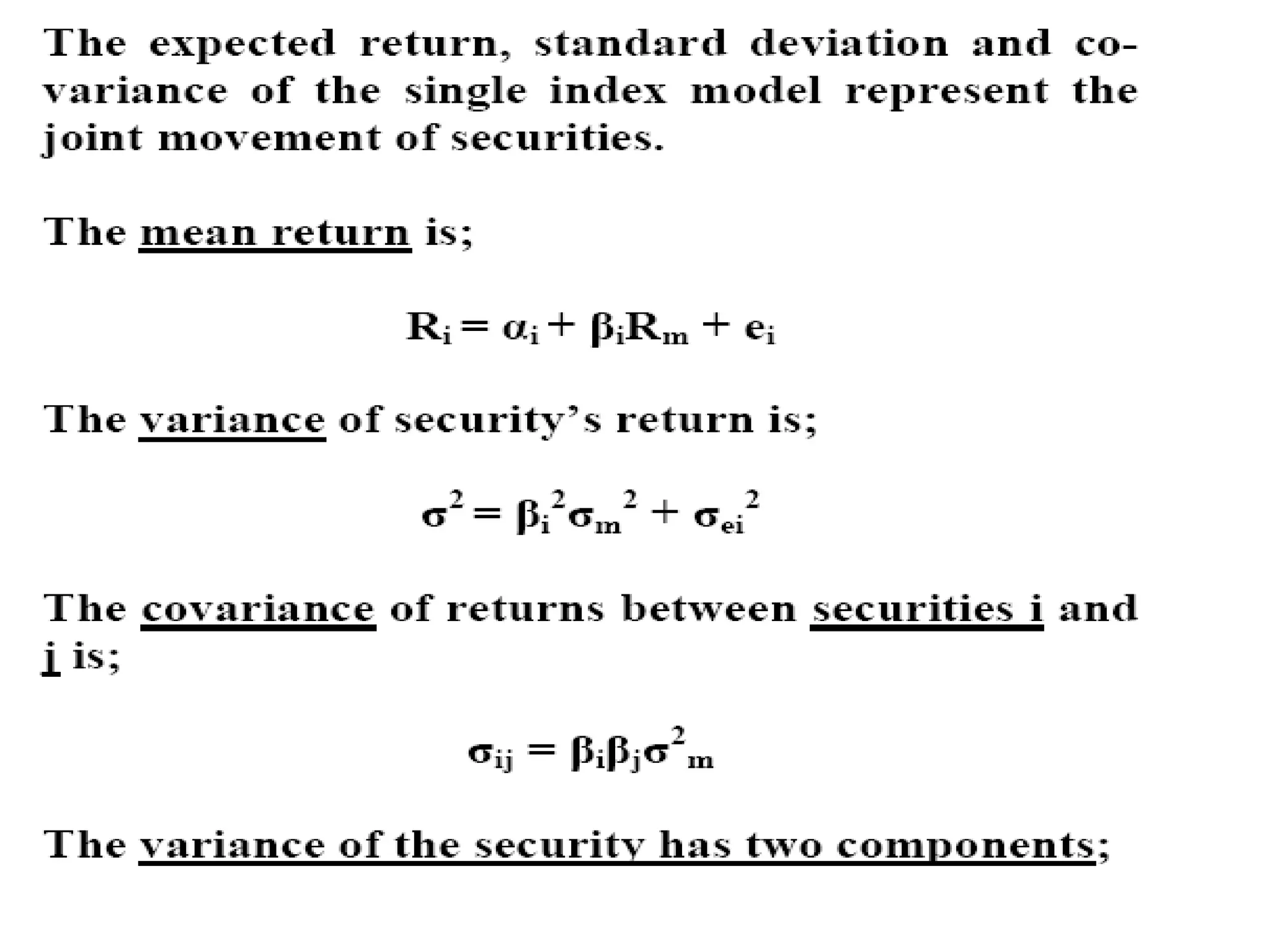

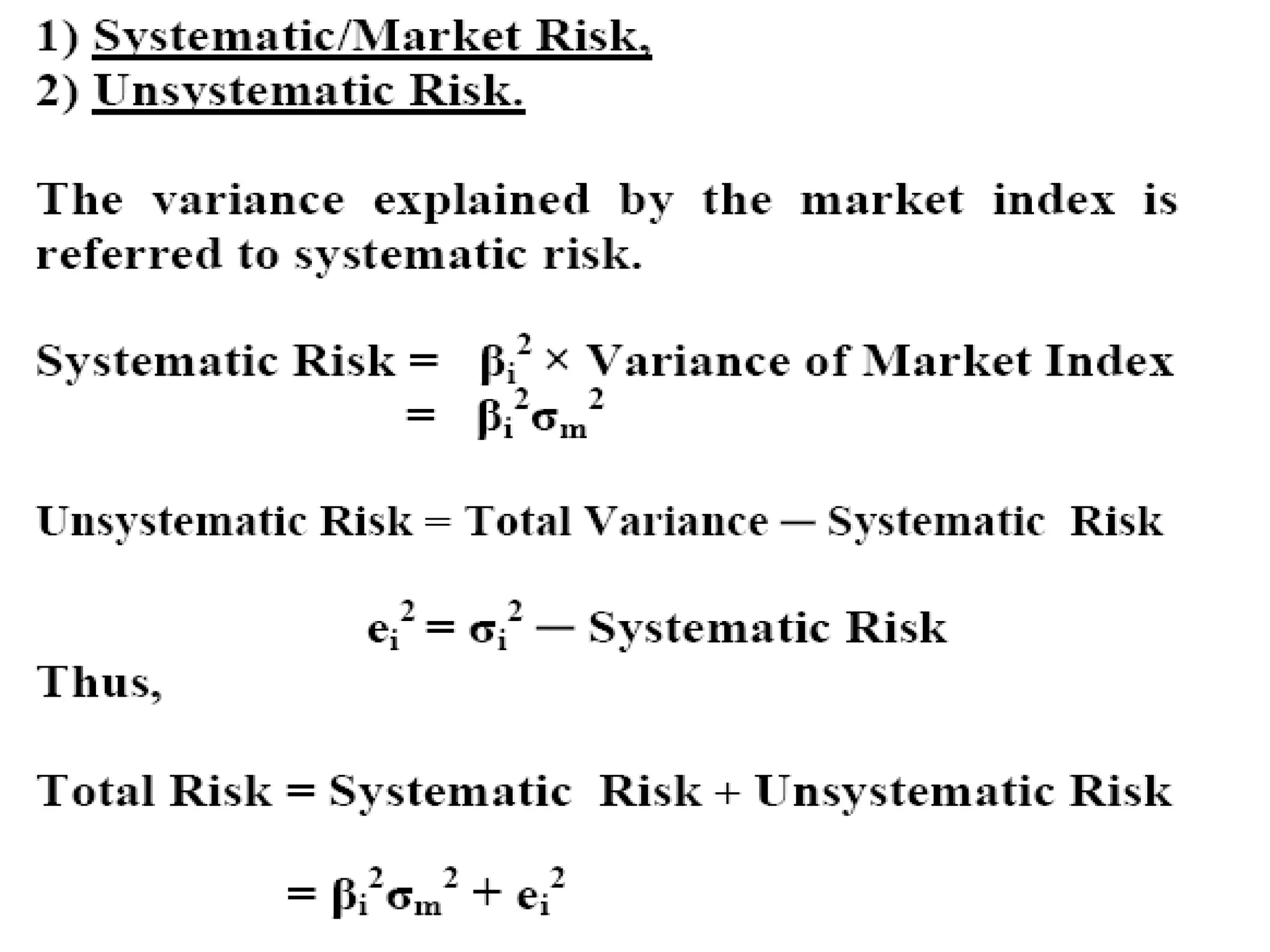

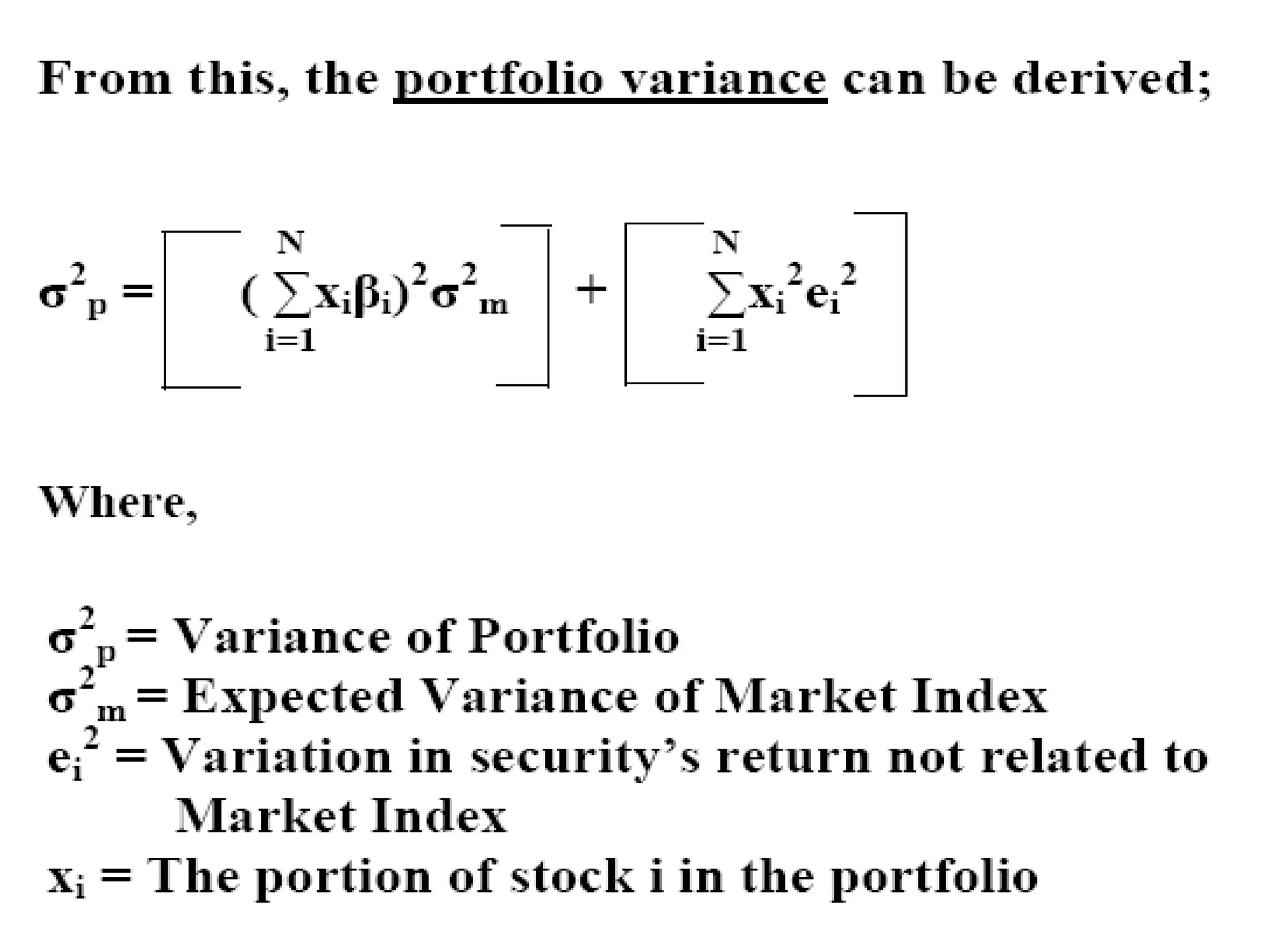

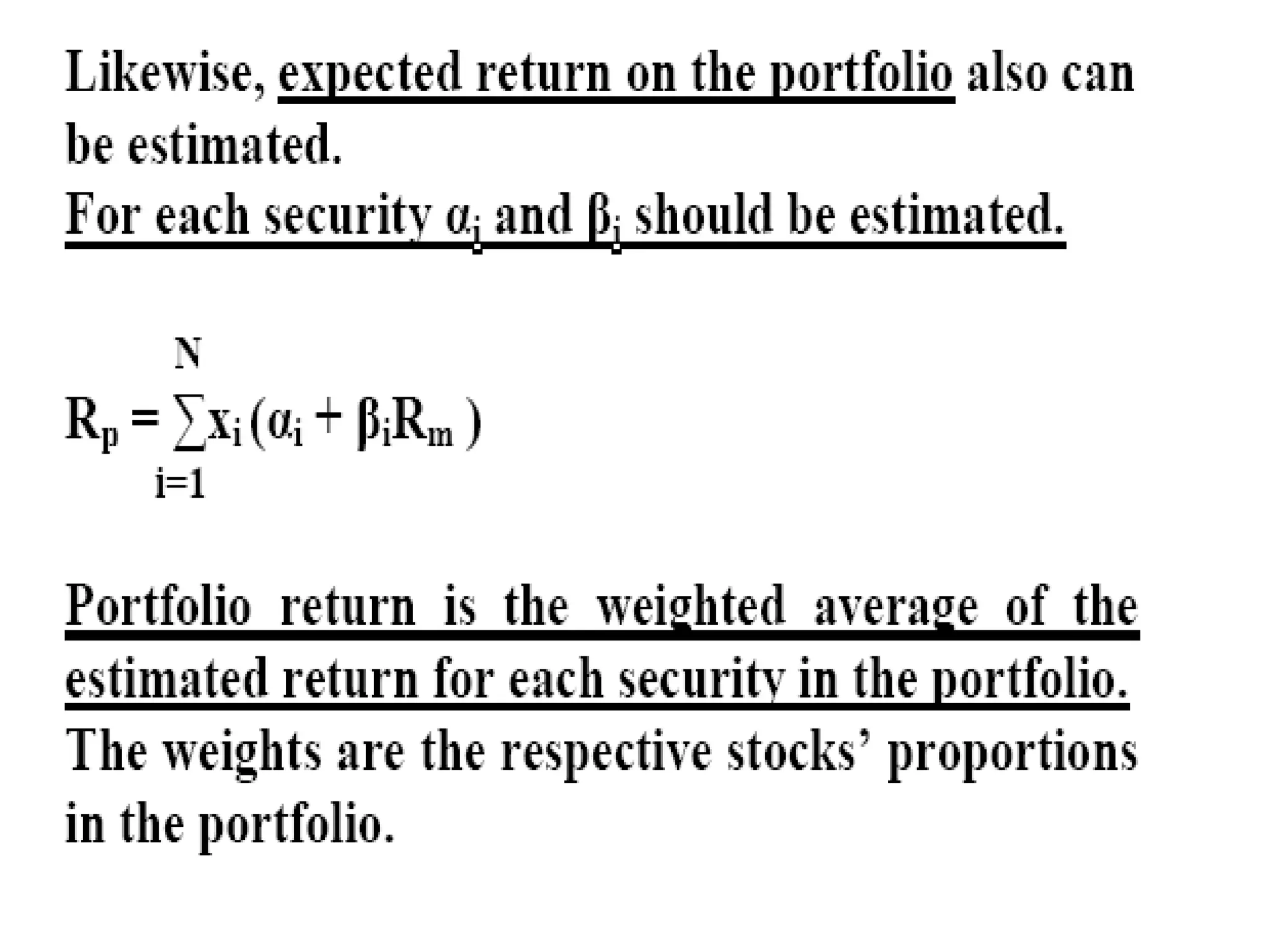

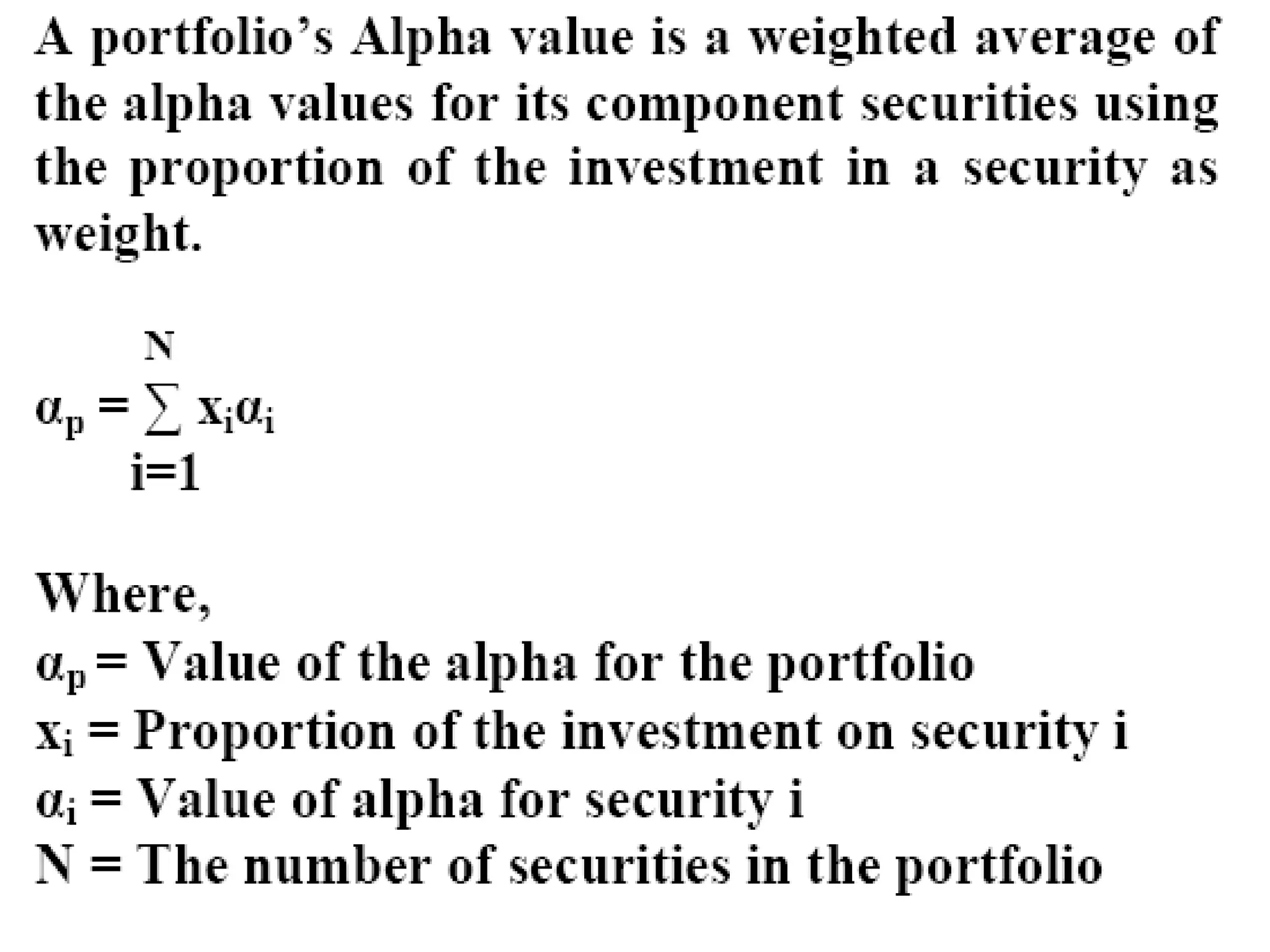

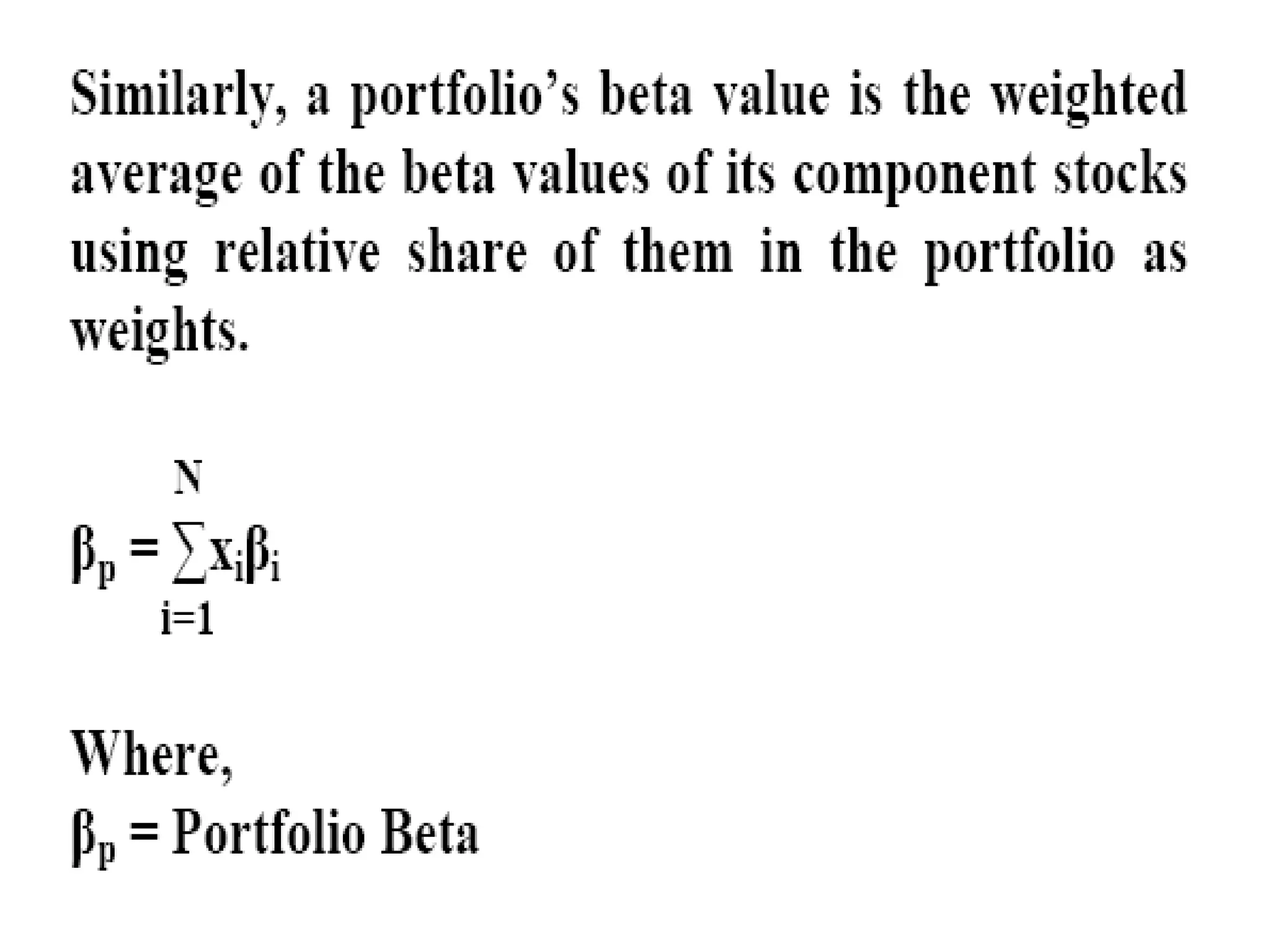

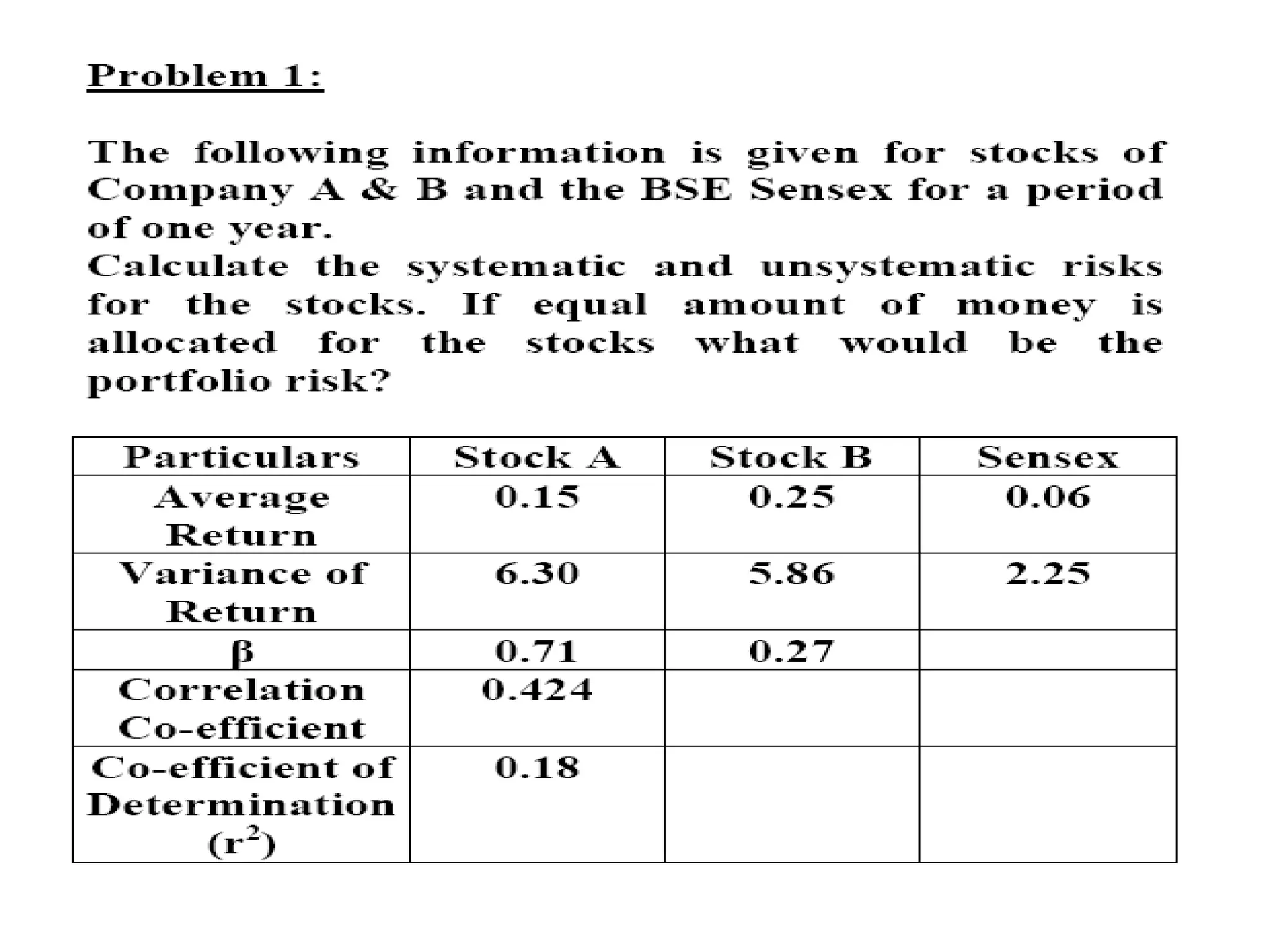

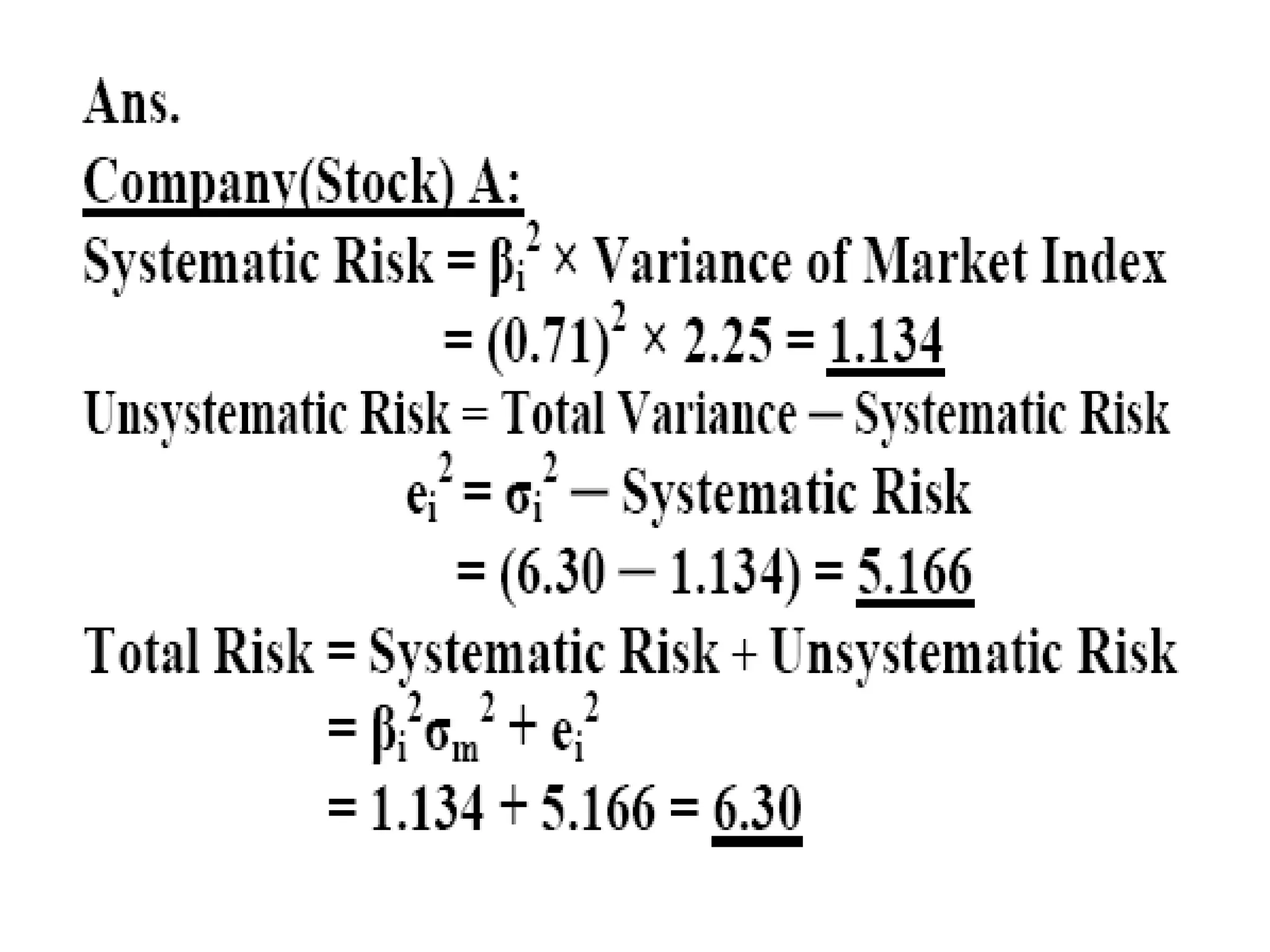

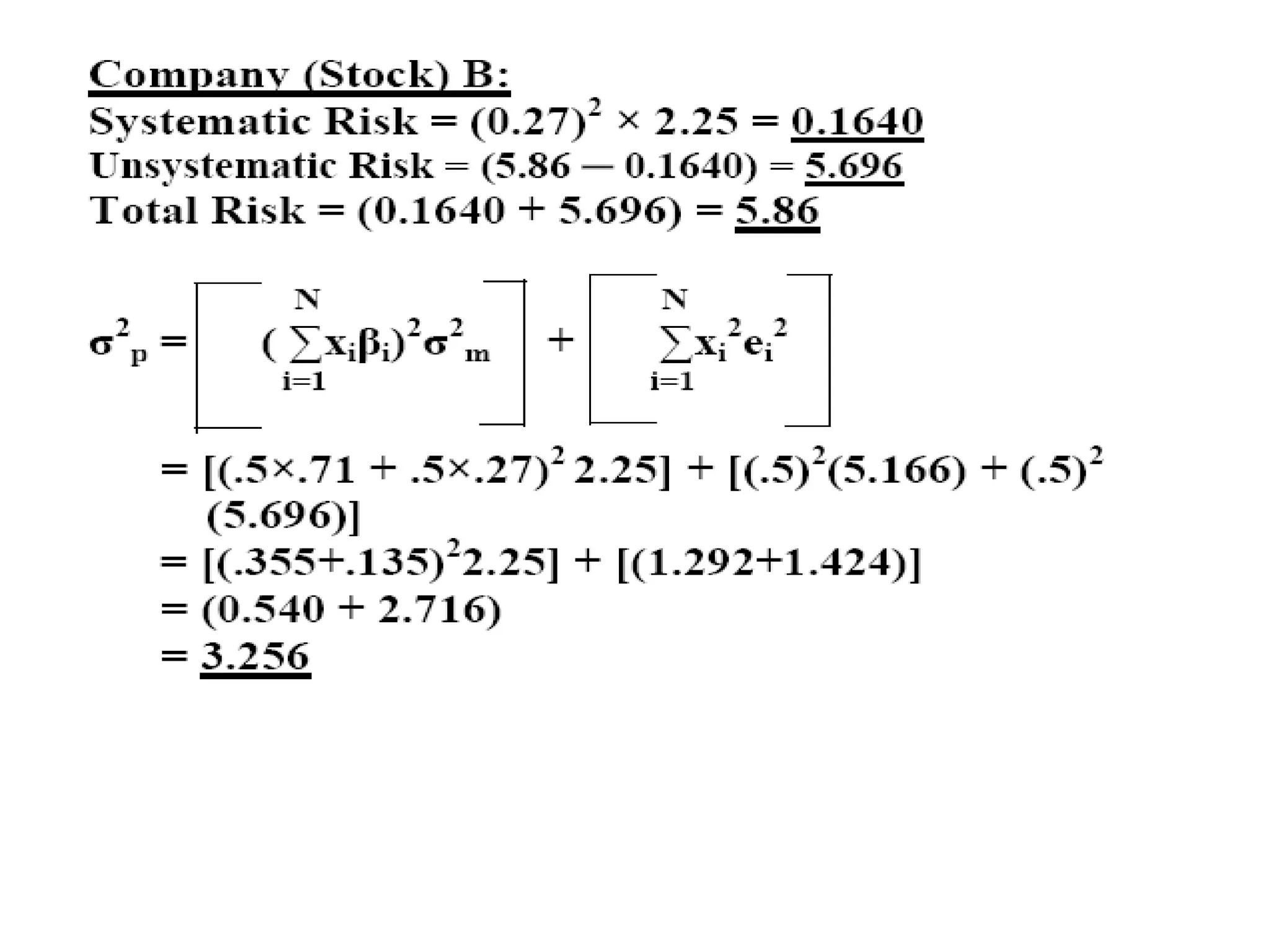

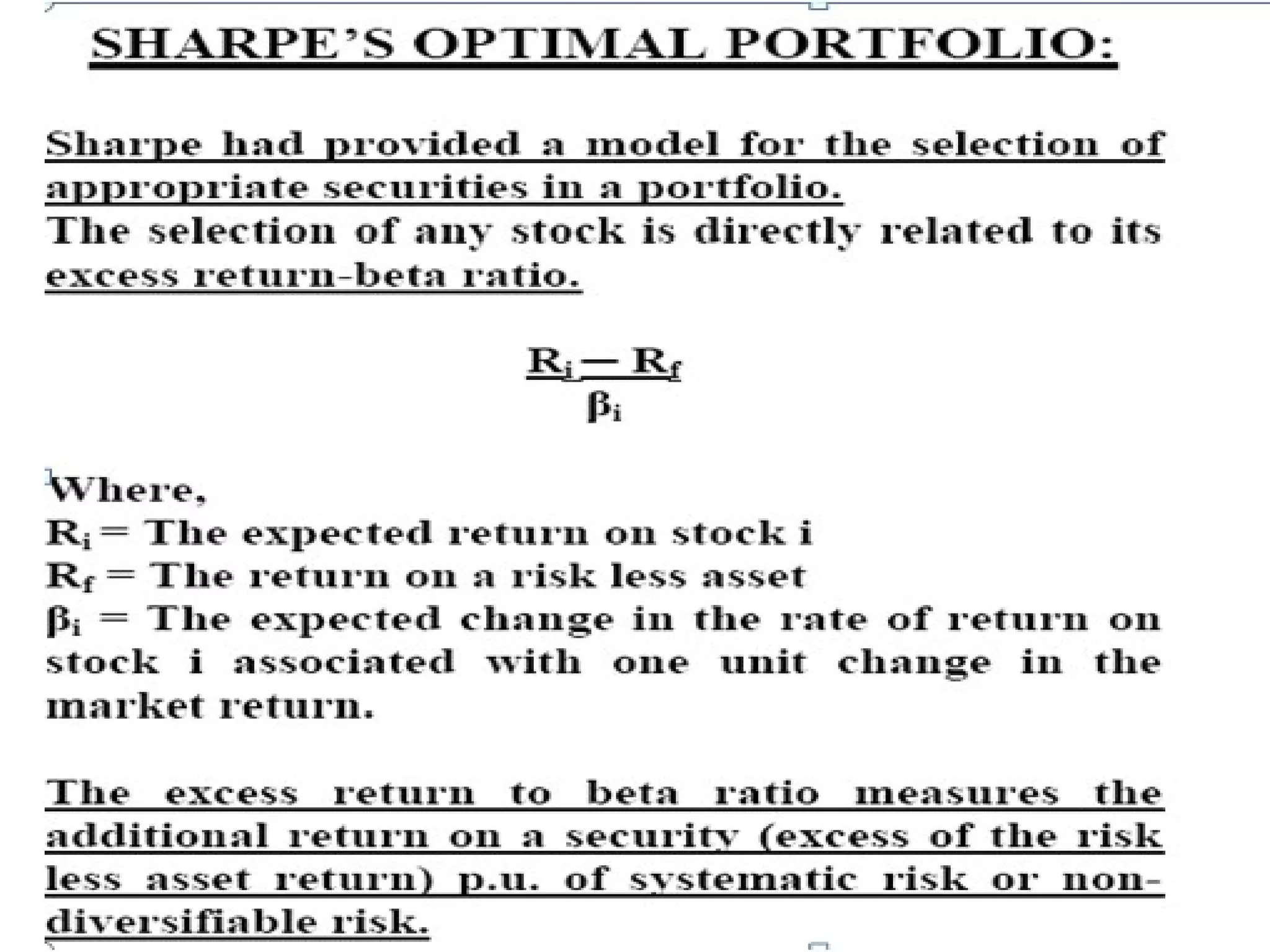

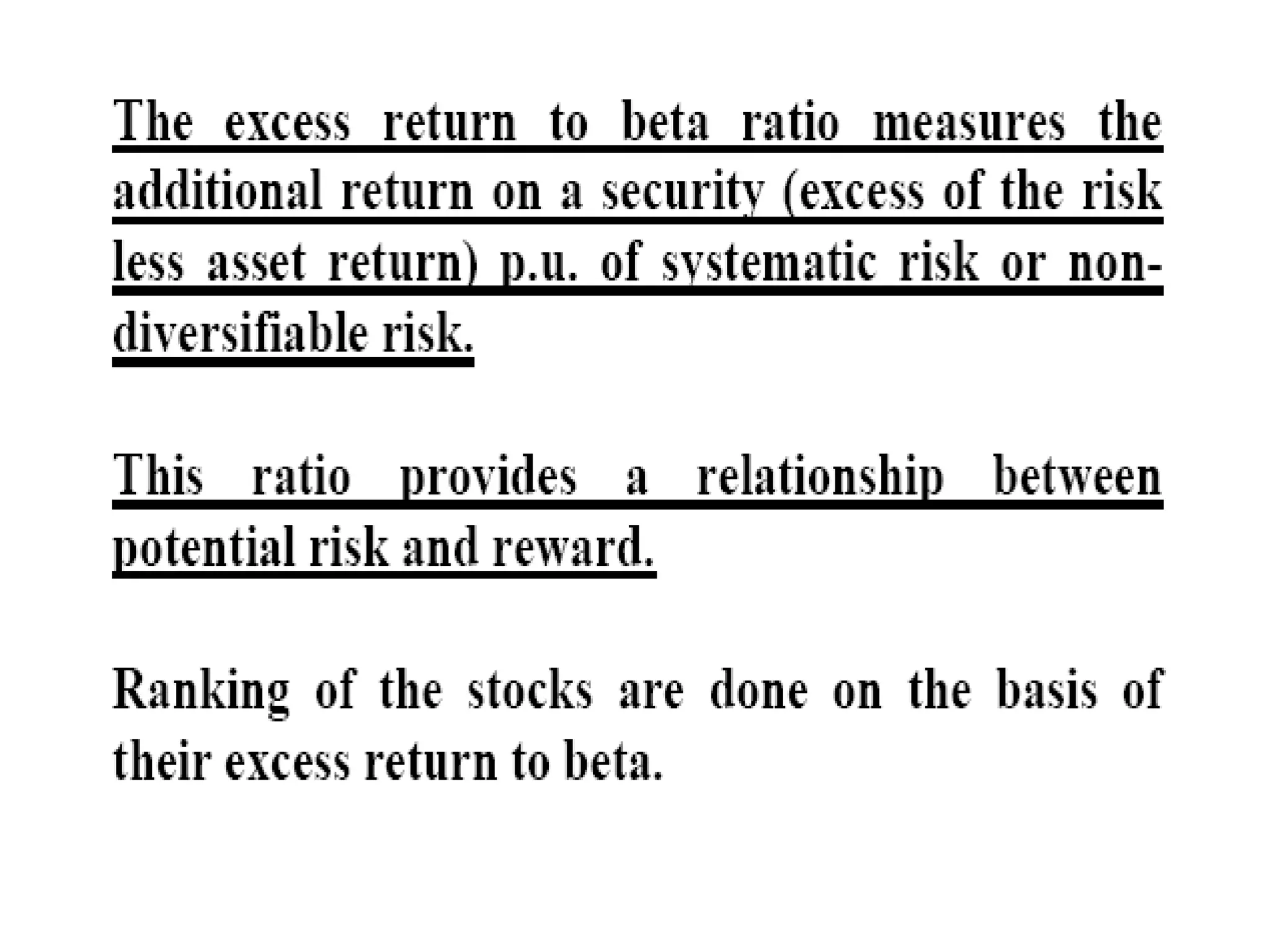

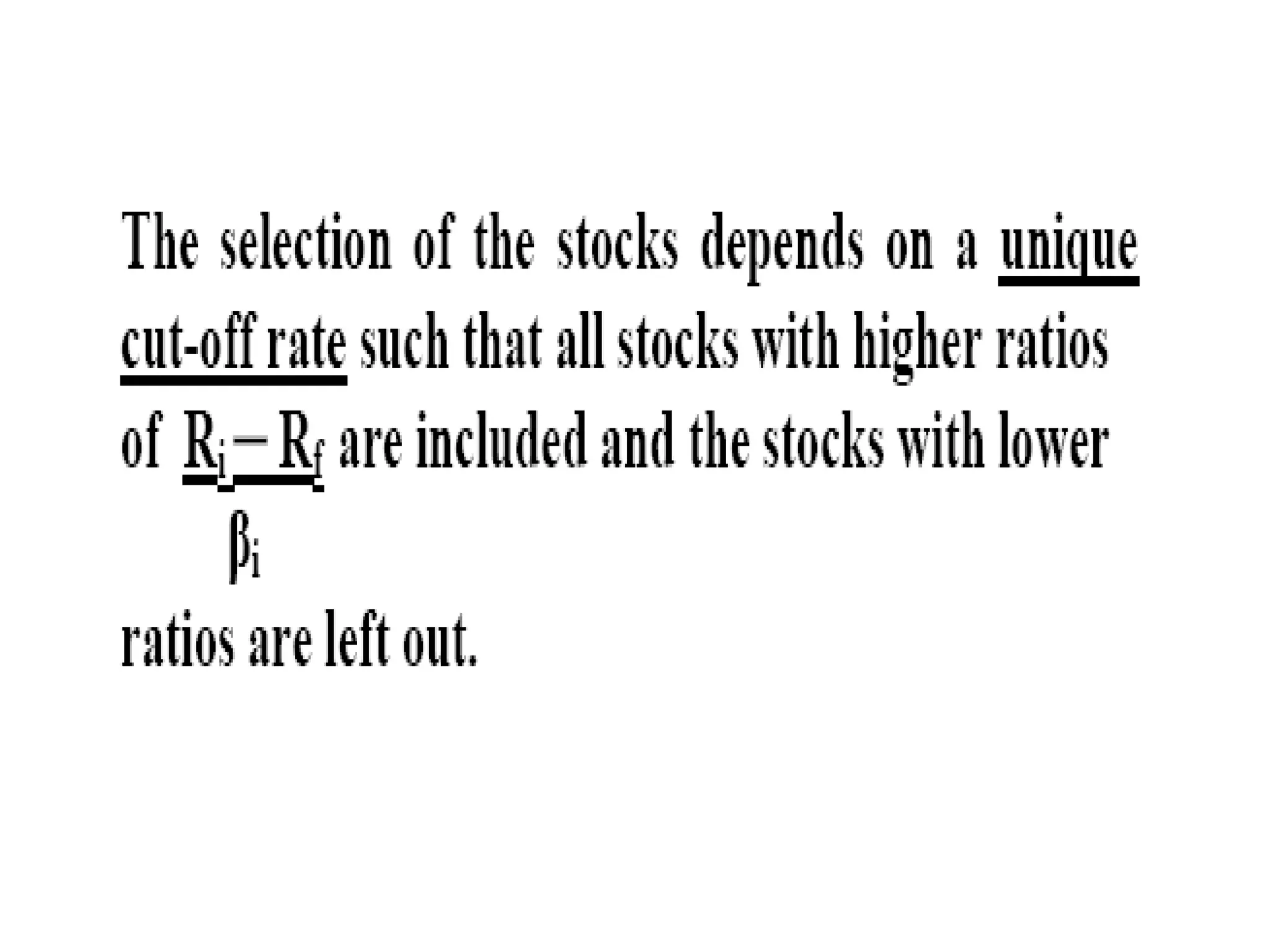

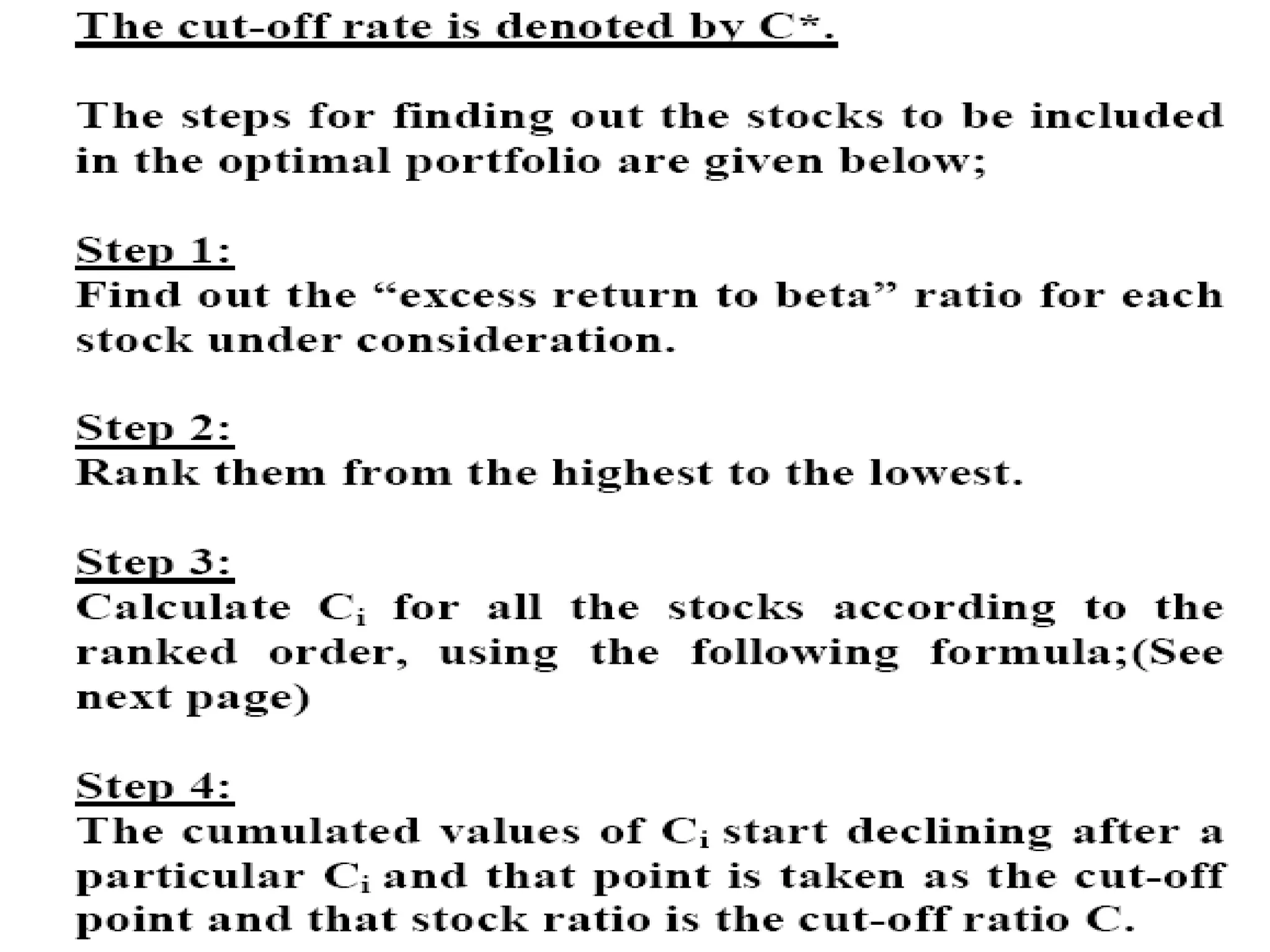

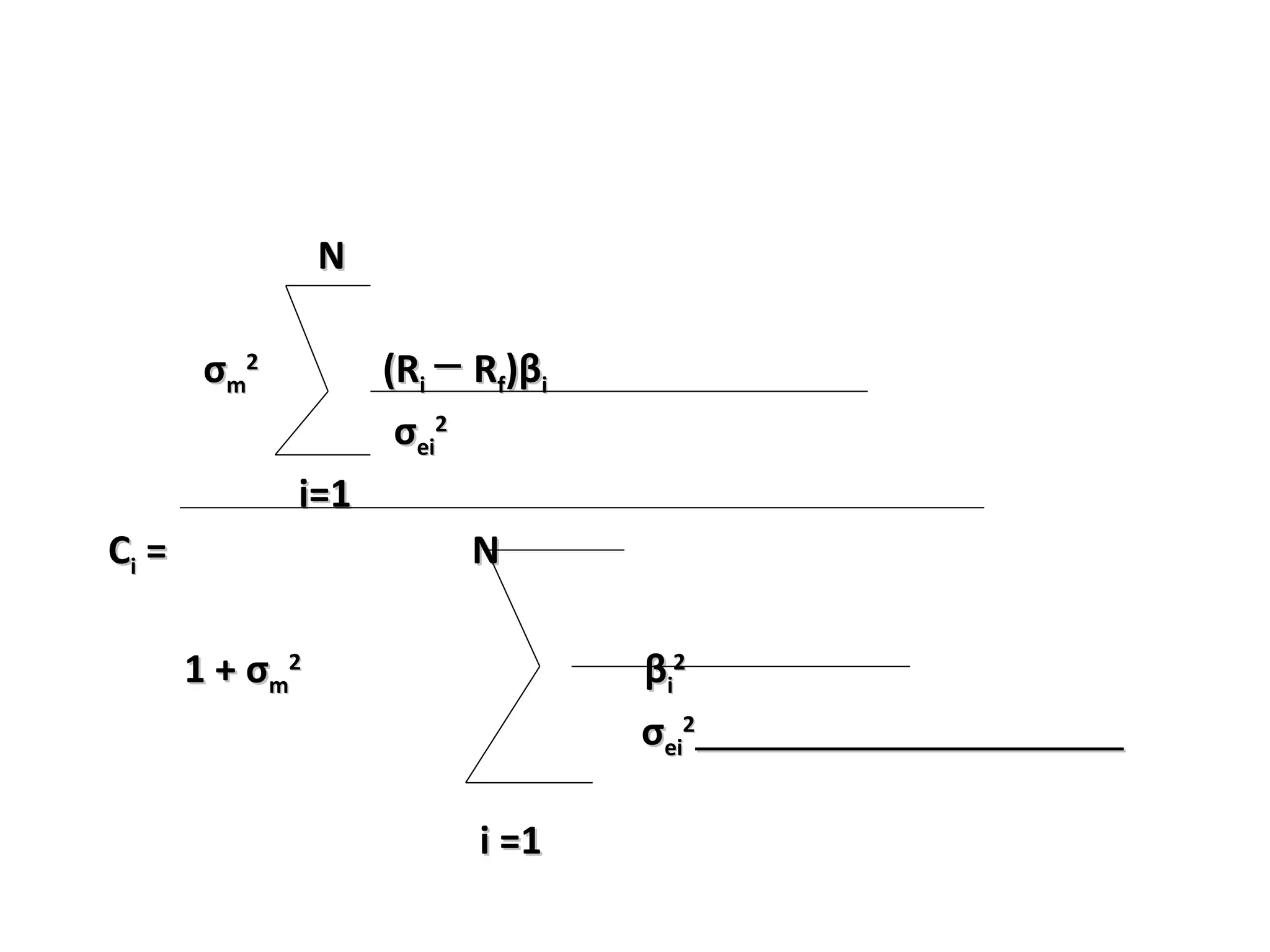

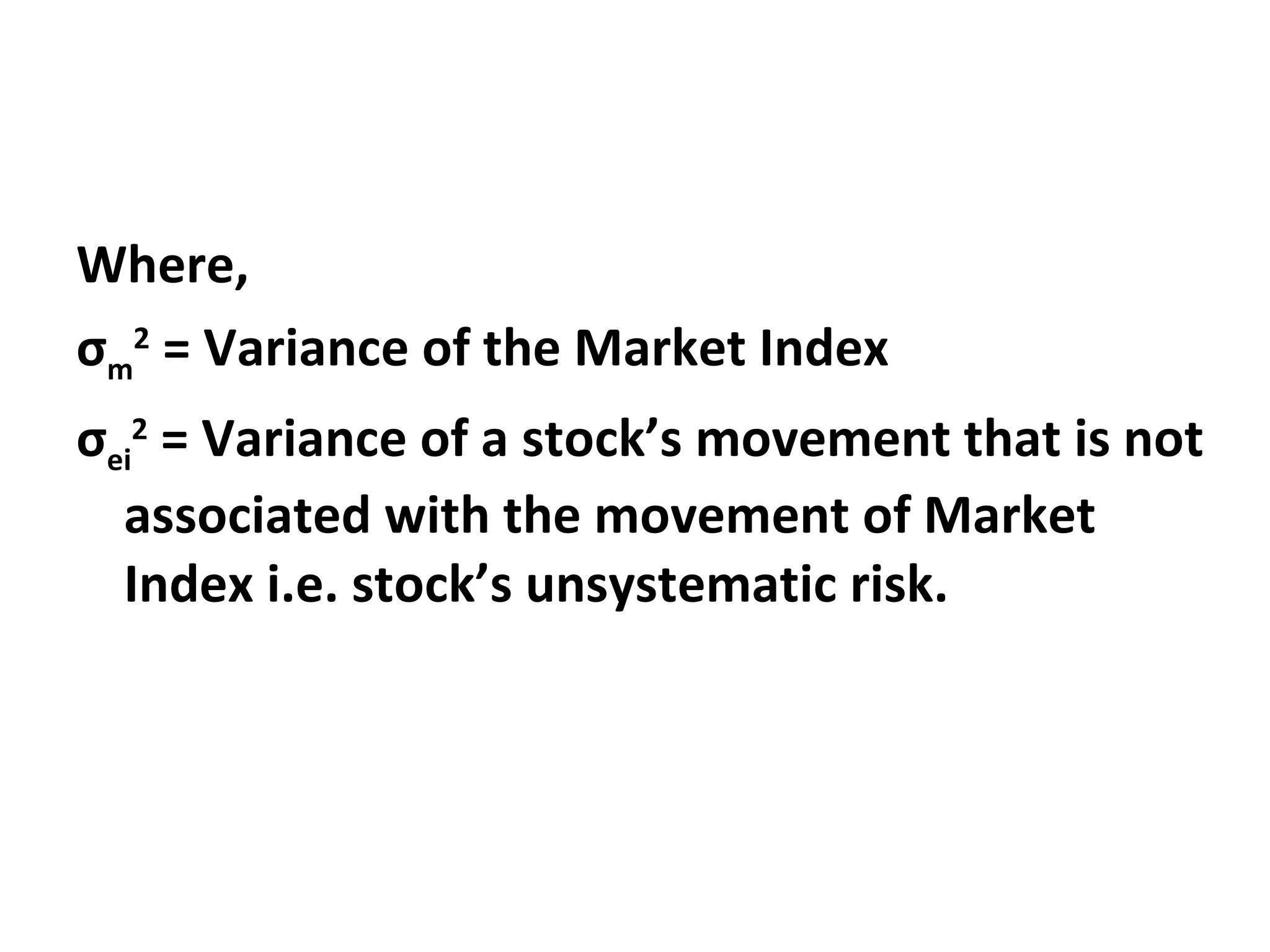

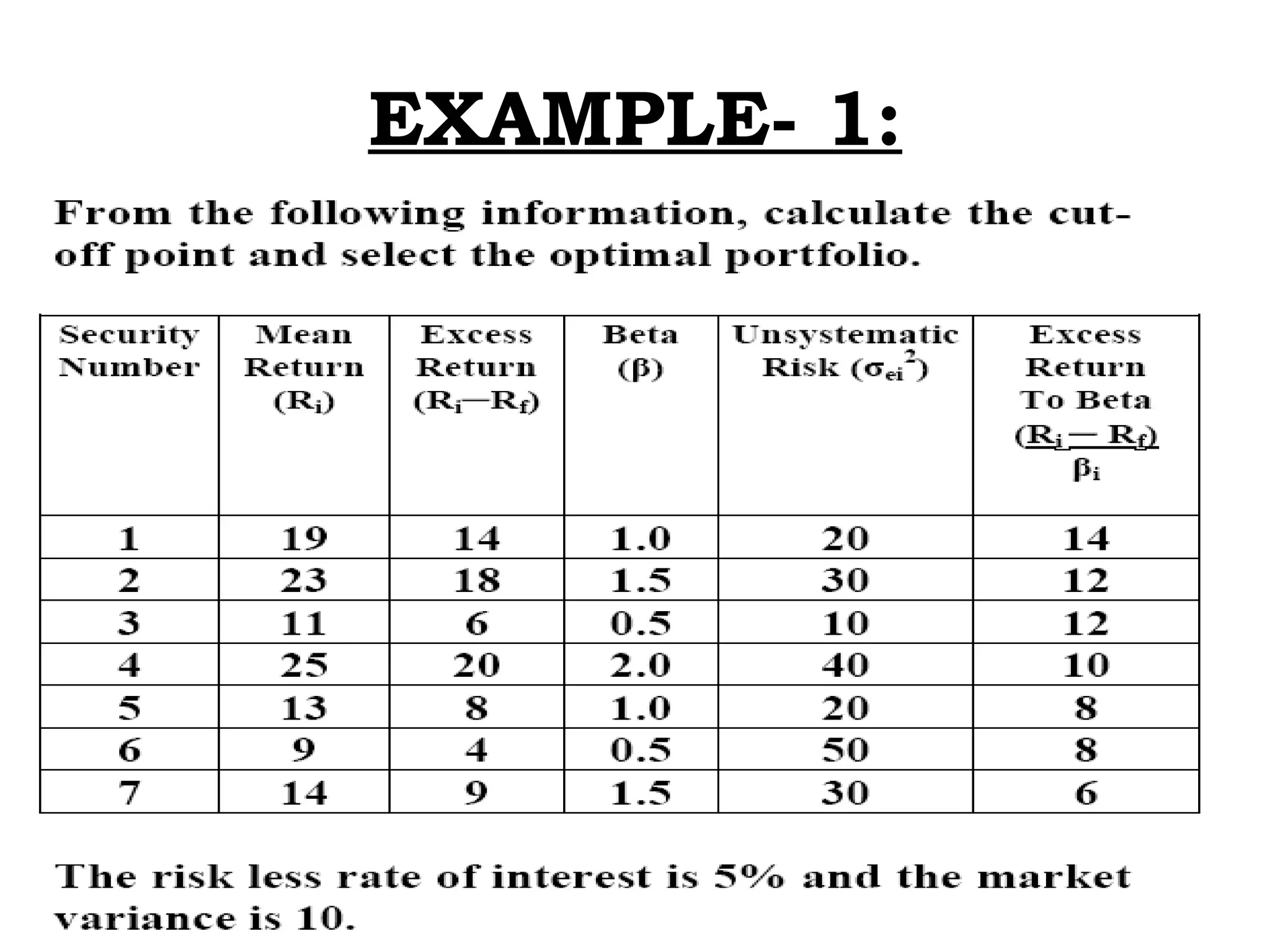

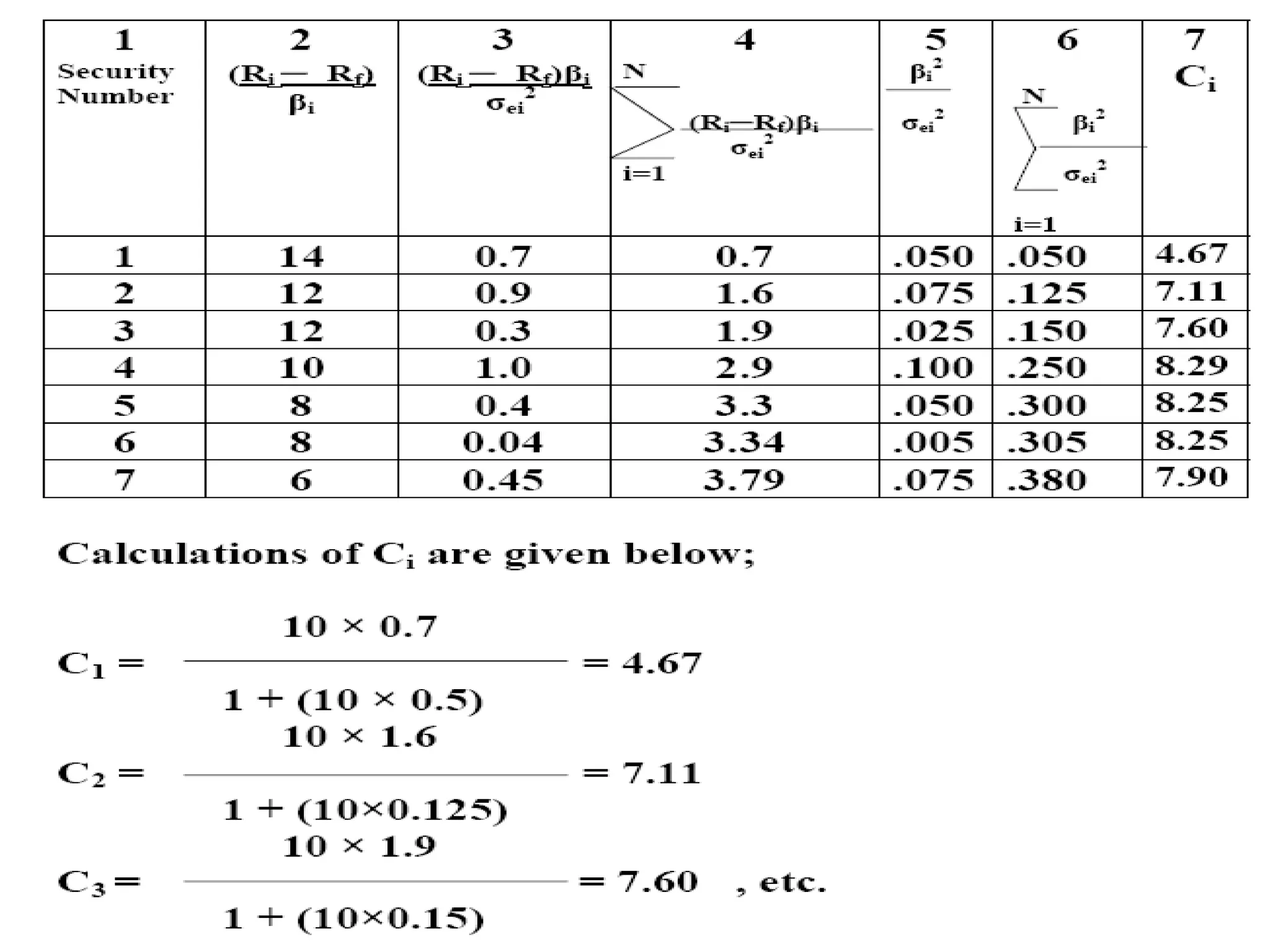

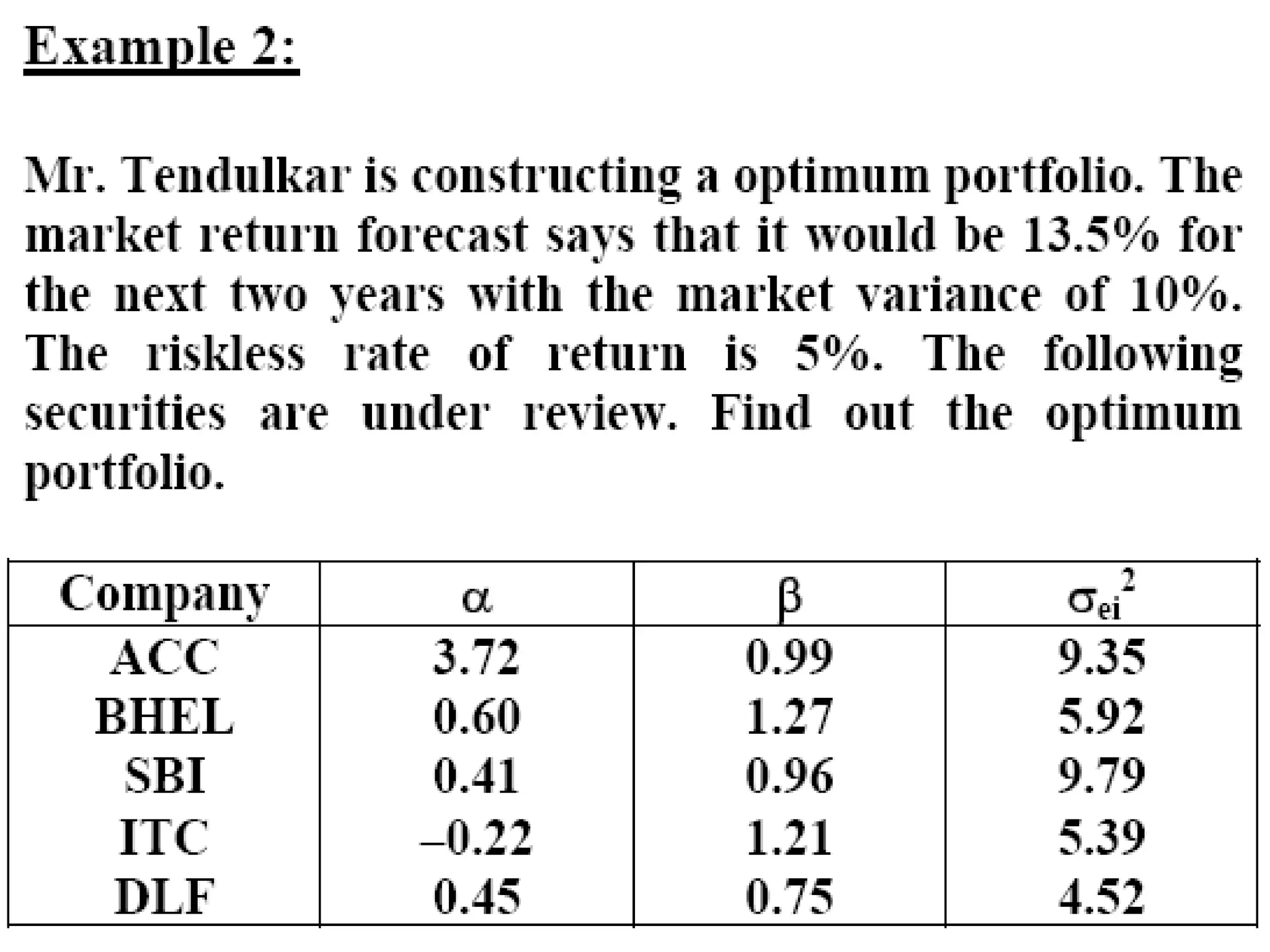

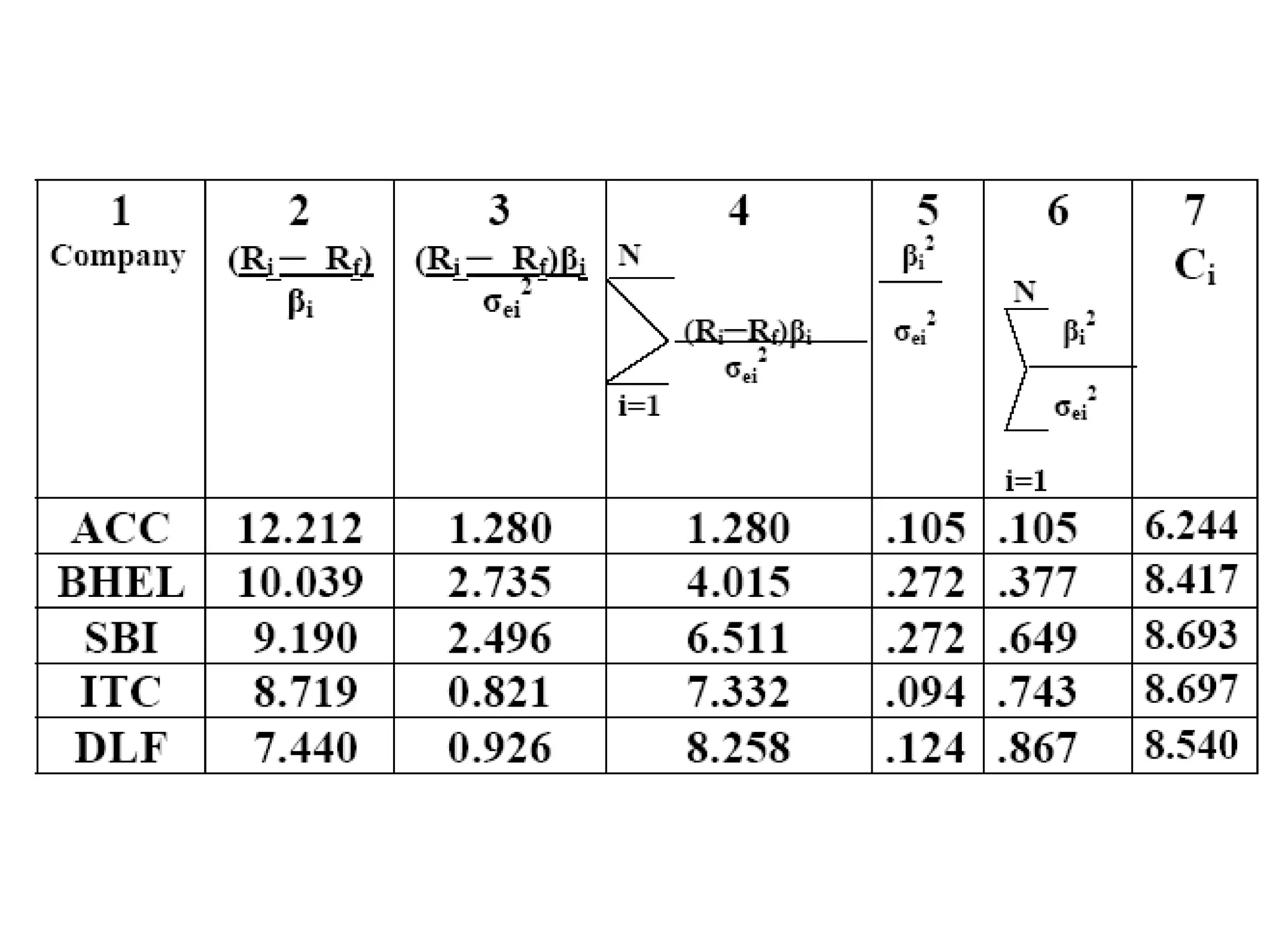

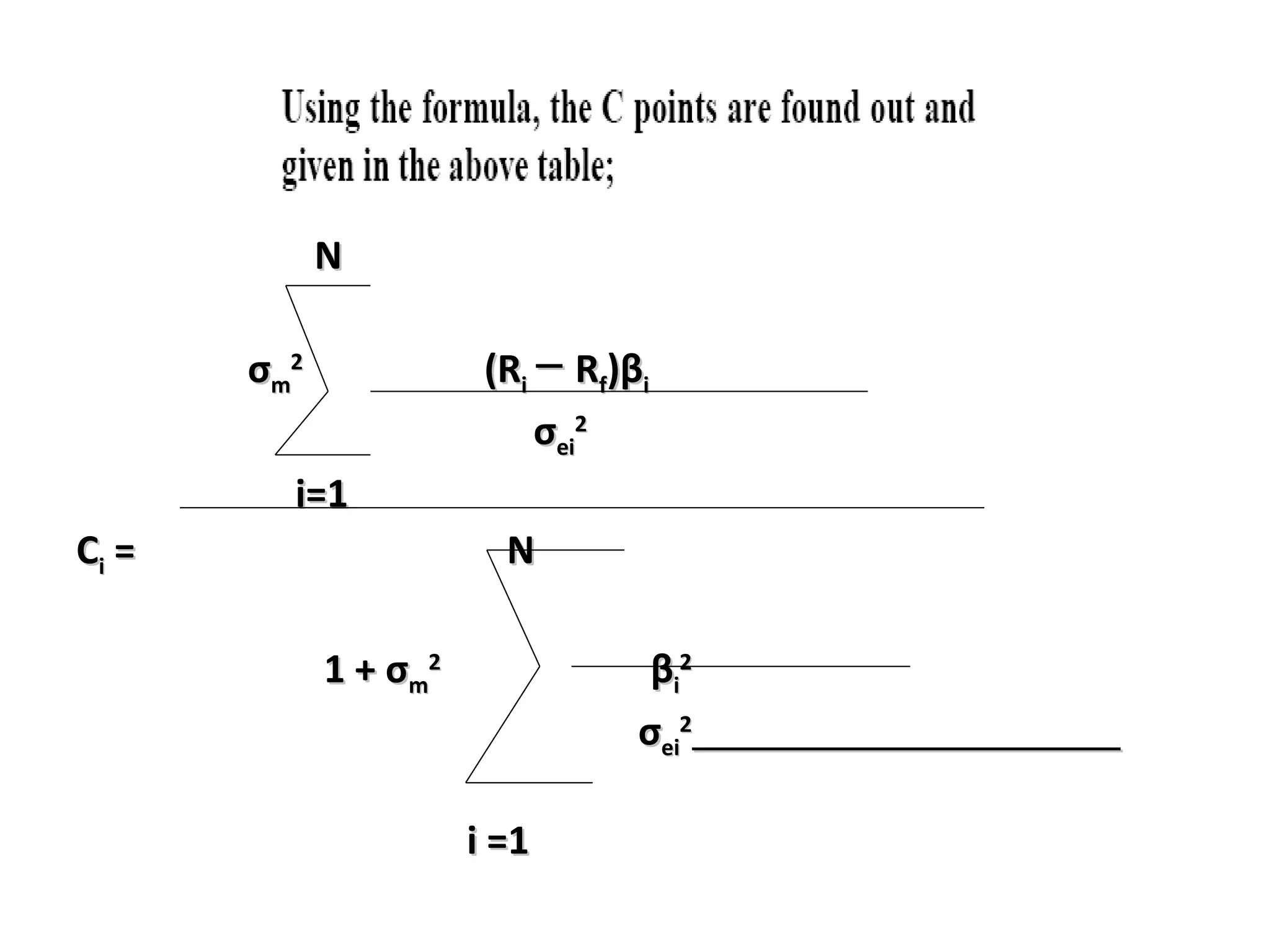

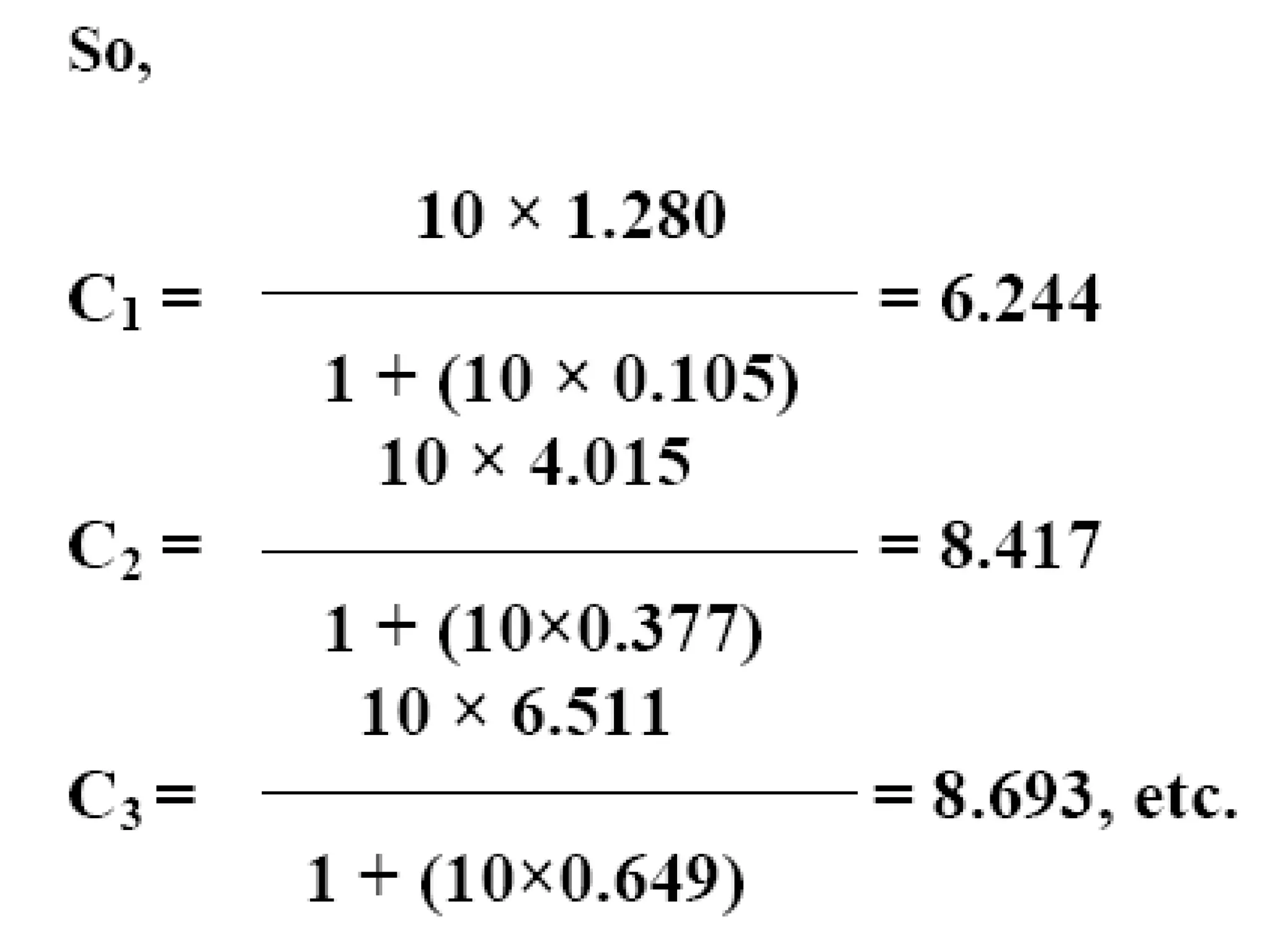

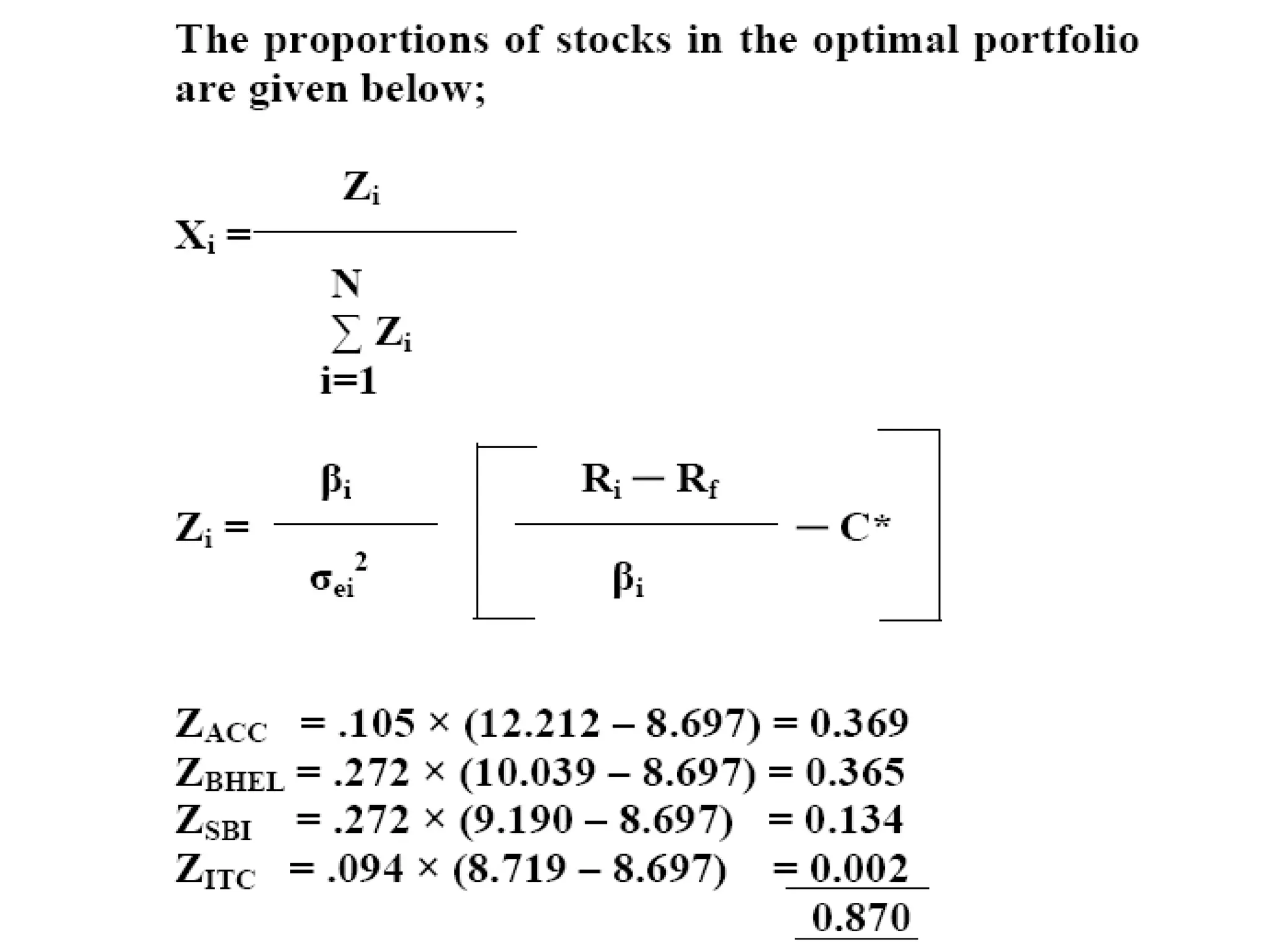

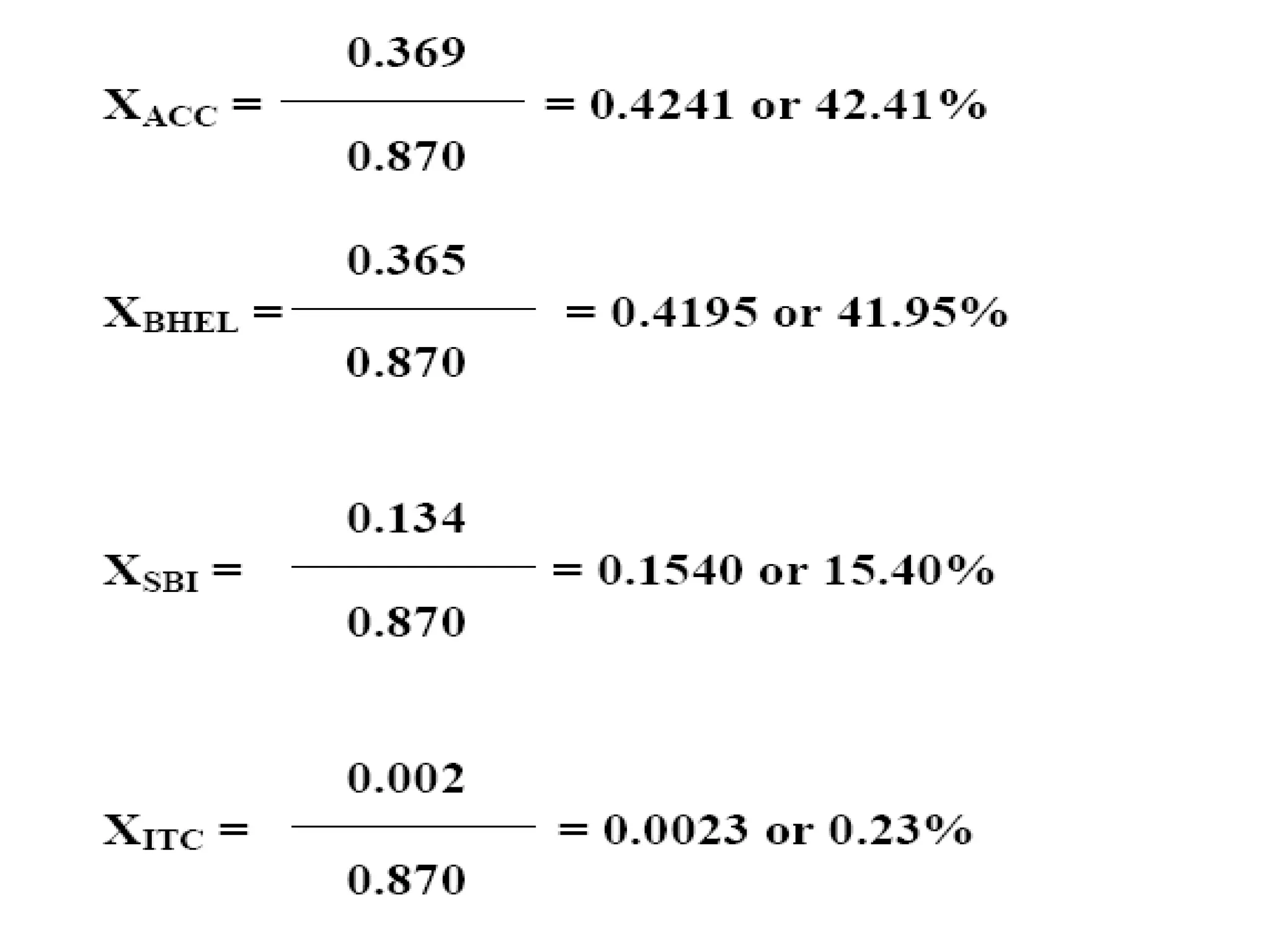

The document discusses the Sharp Index model for calculating the expected return of a portfolio. It provides the formula for calculating the Sharpe ratio which takes into account the variance of the market index, variance of individual stock movements not associated with the market, and the beta of each stock. It also mentions there are examples provided to demonstrate solving the Sharpe ratio formula.