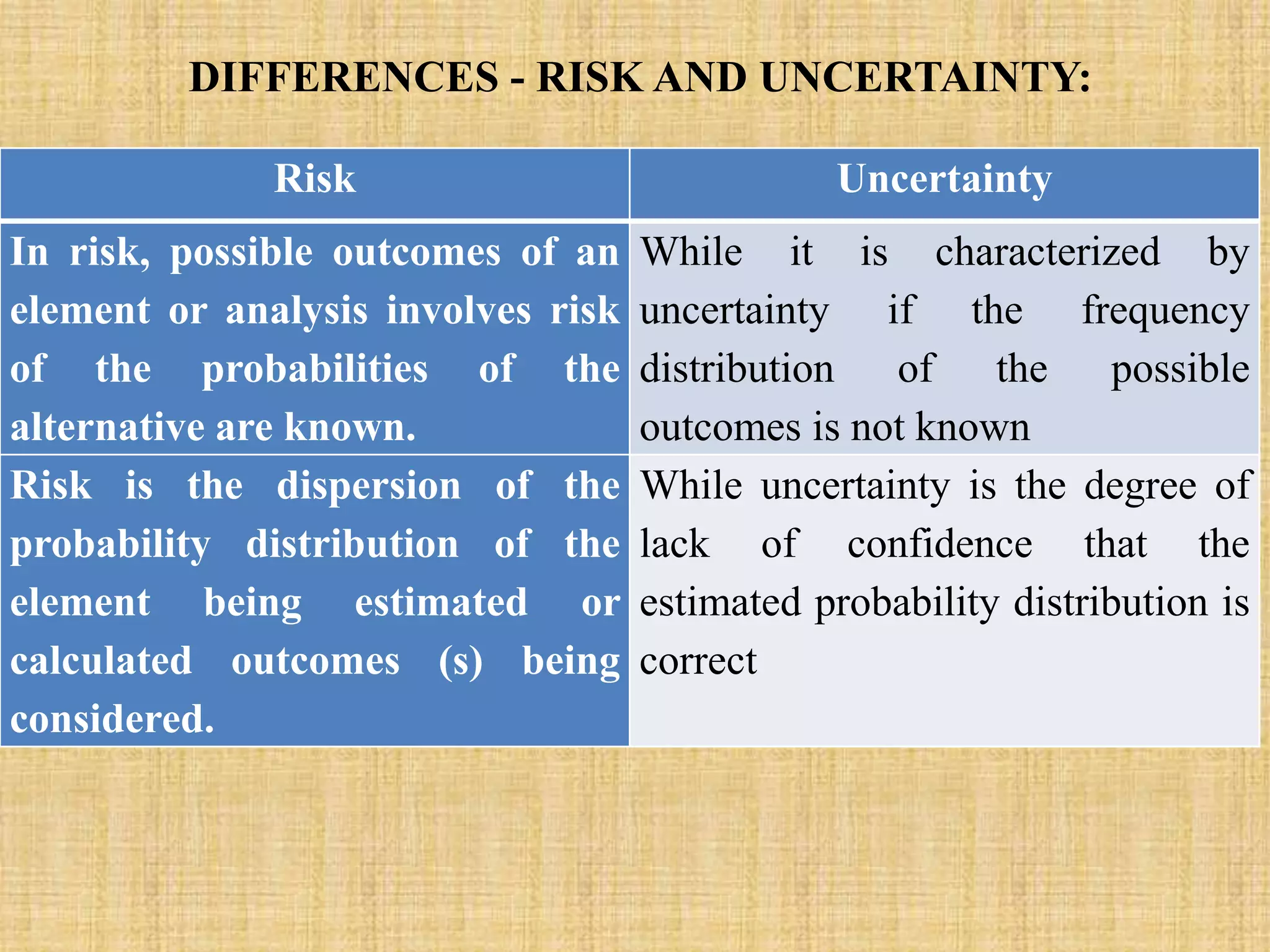

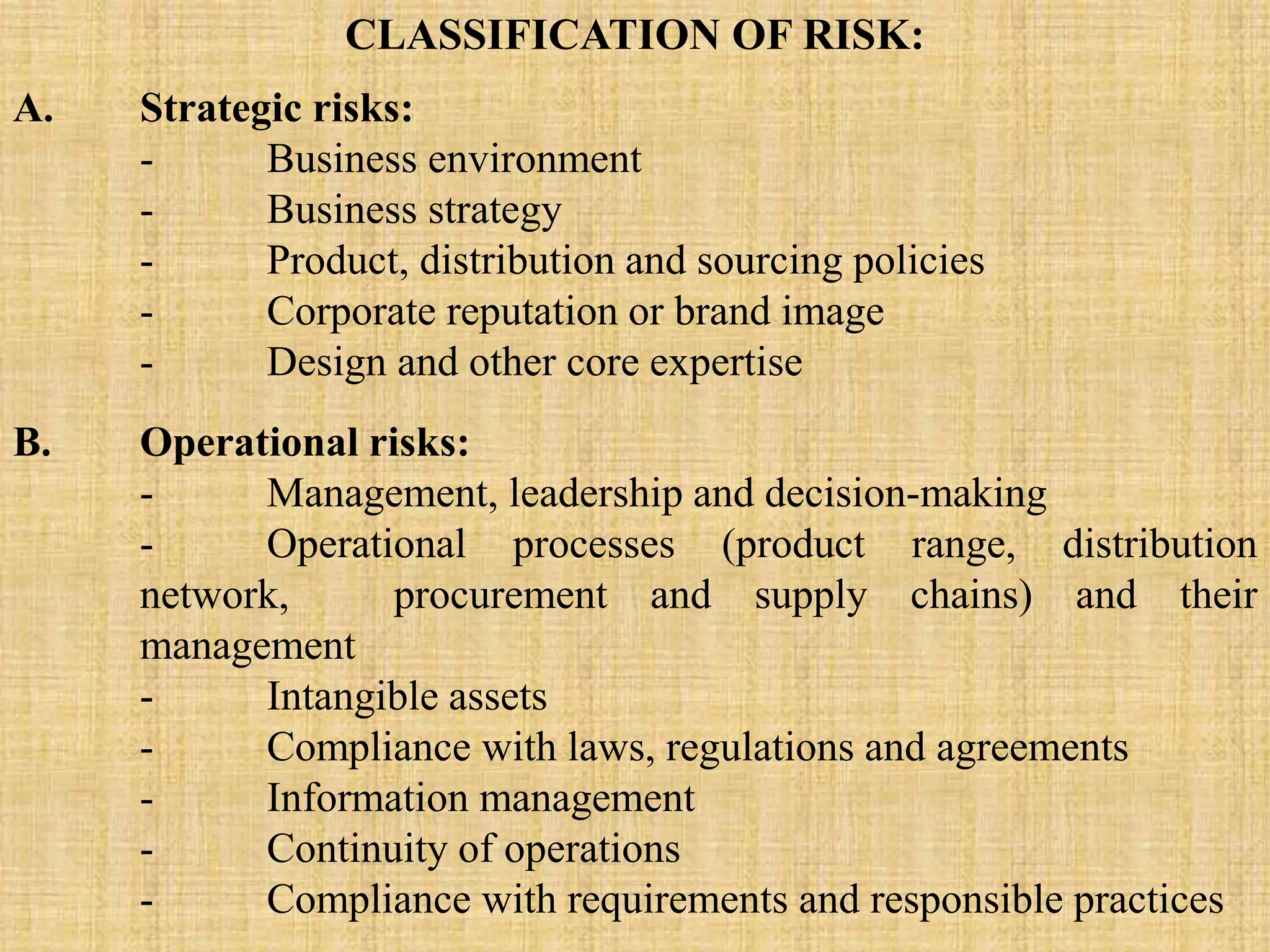

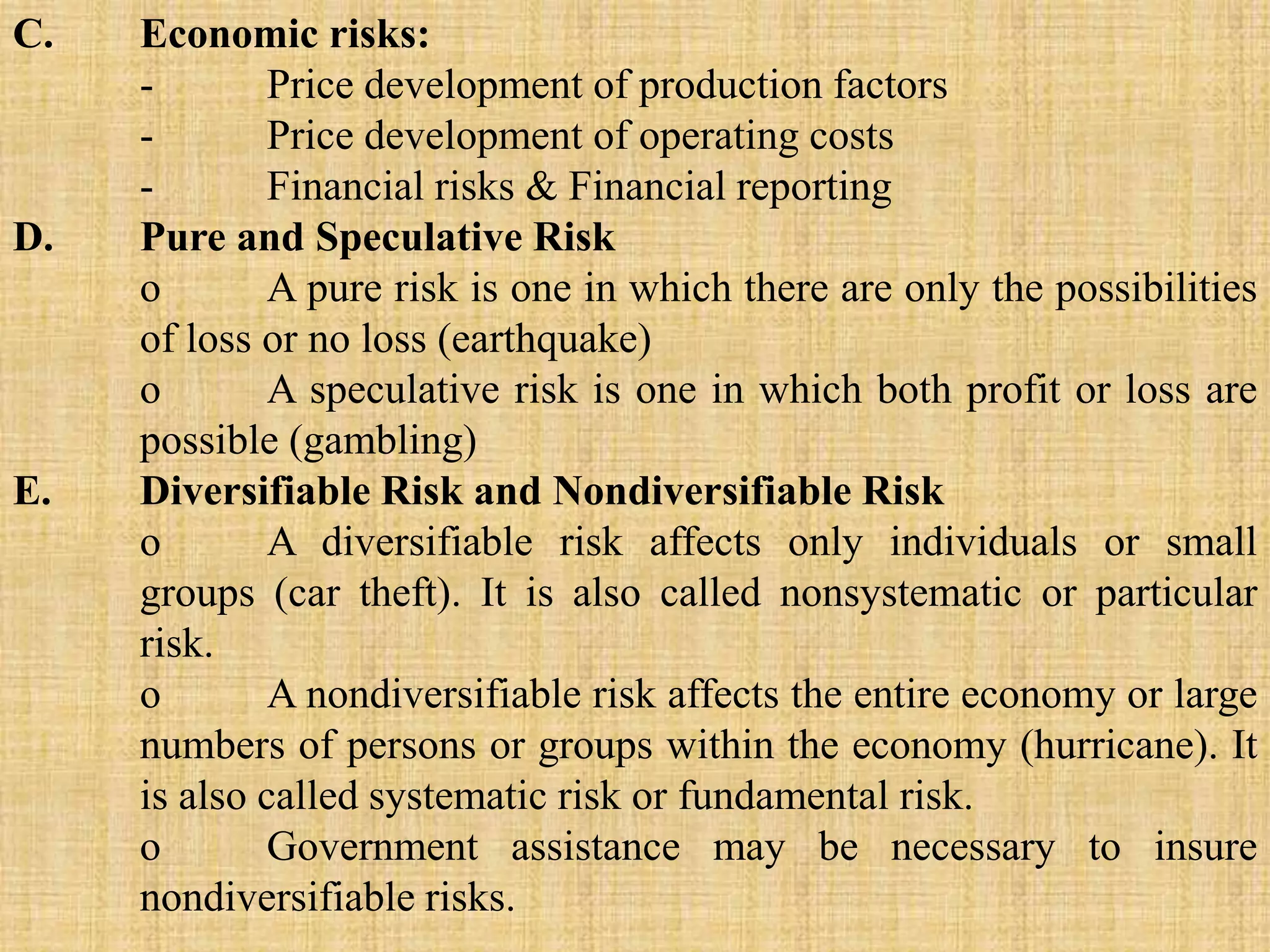

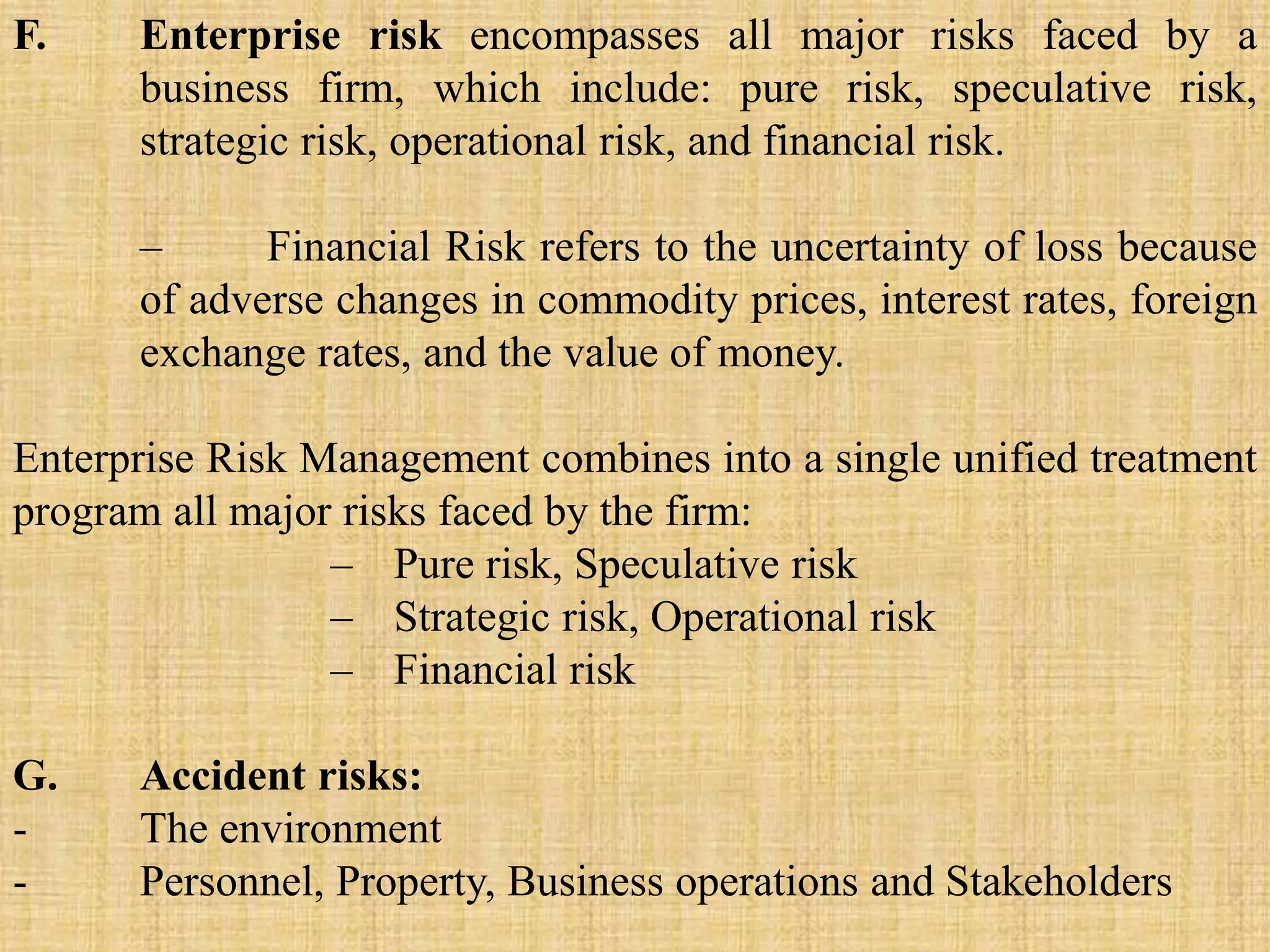

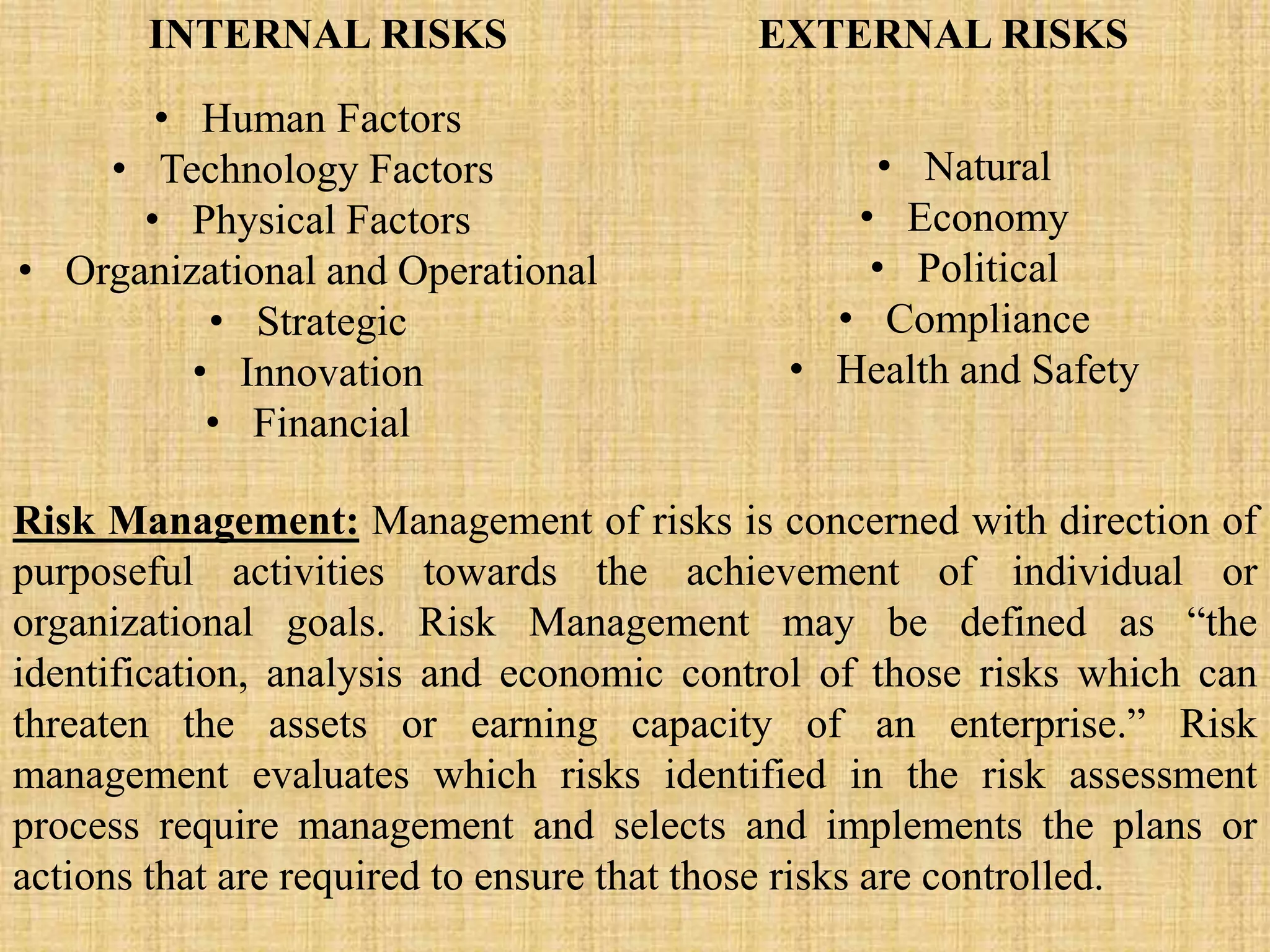

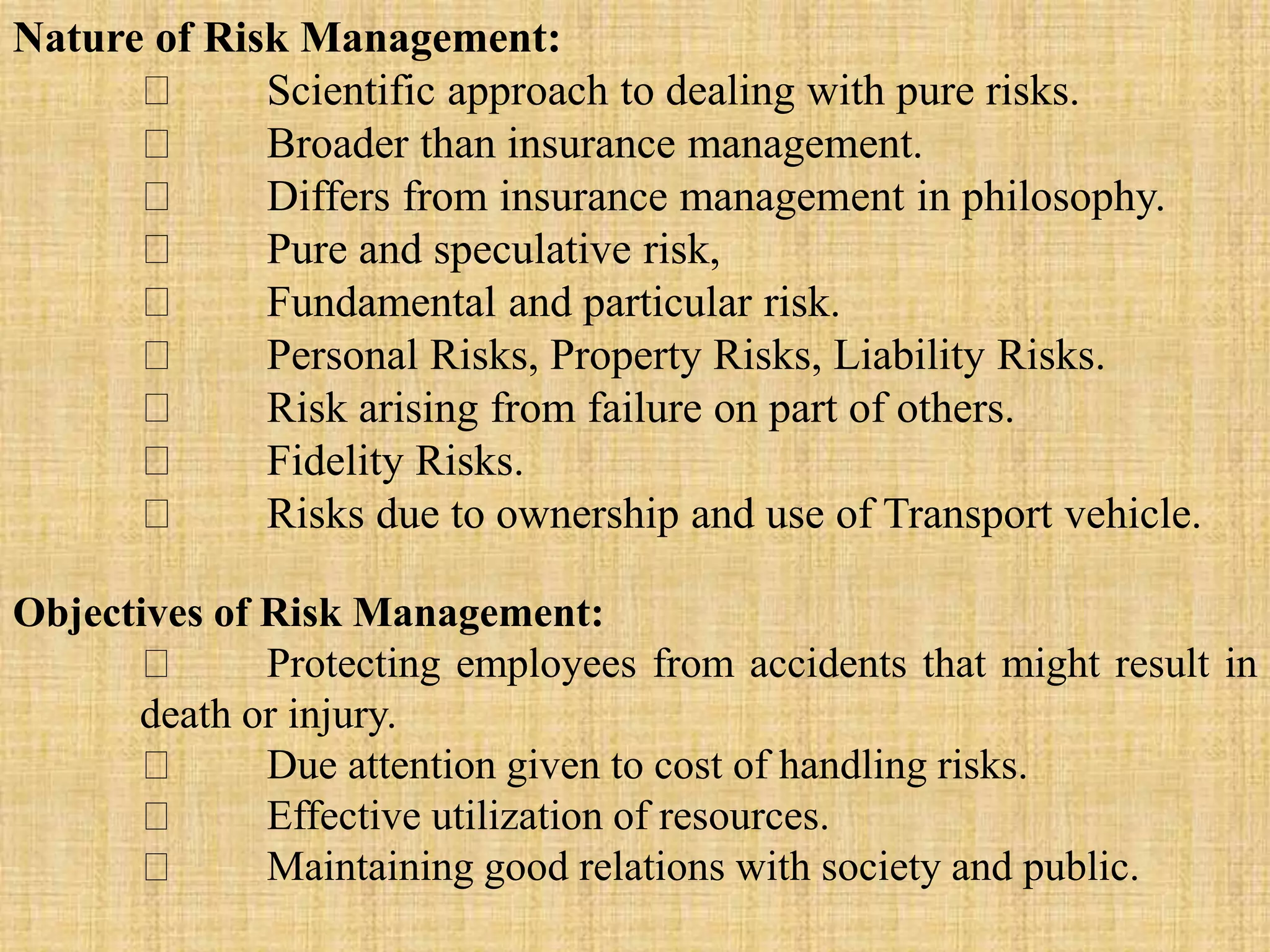

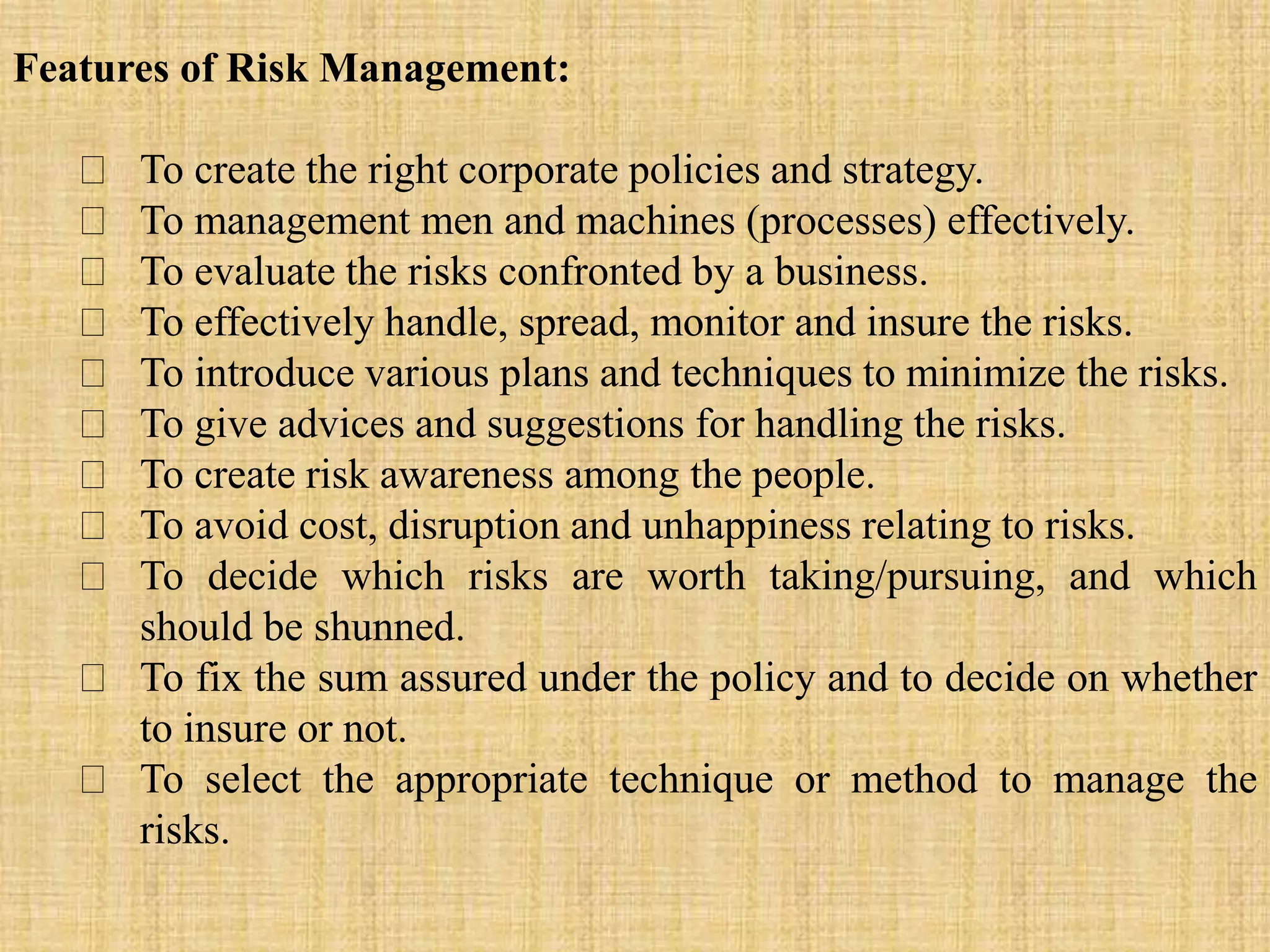

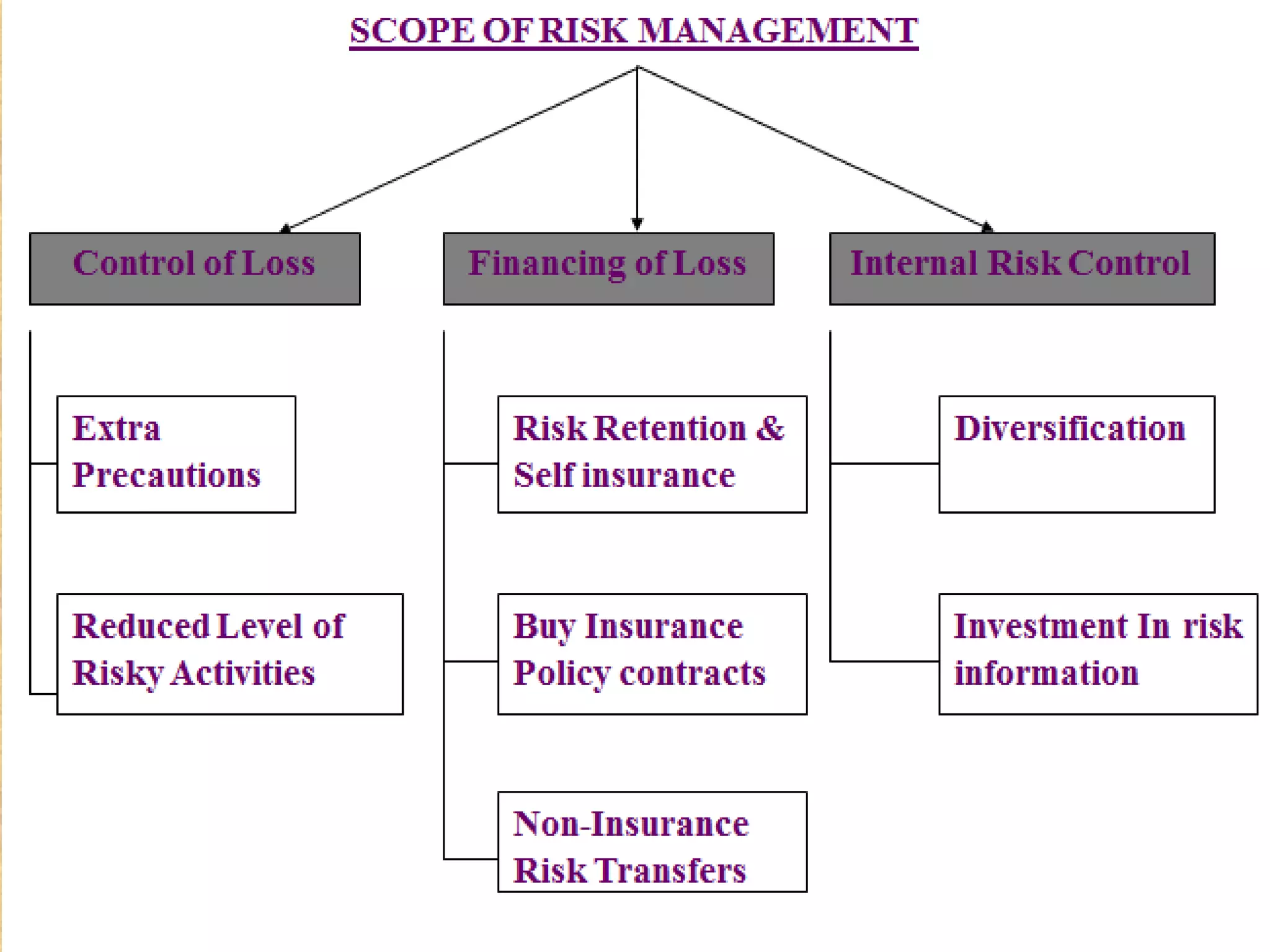

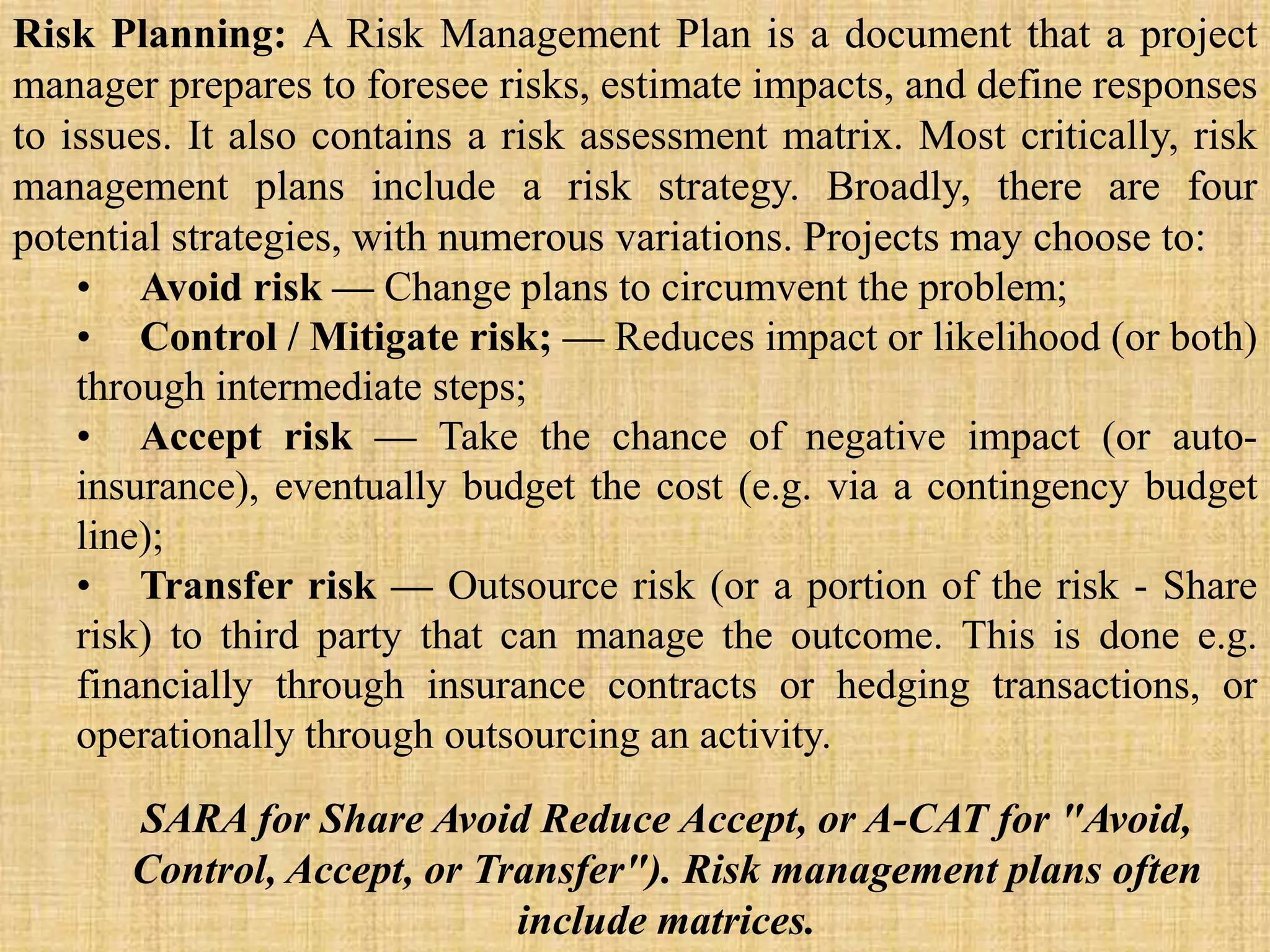

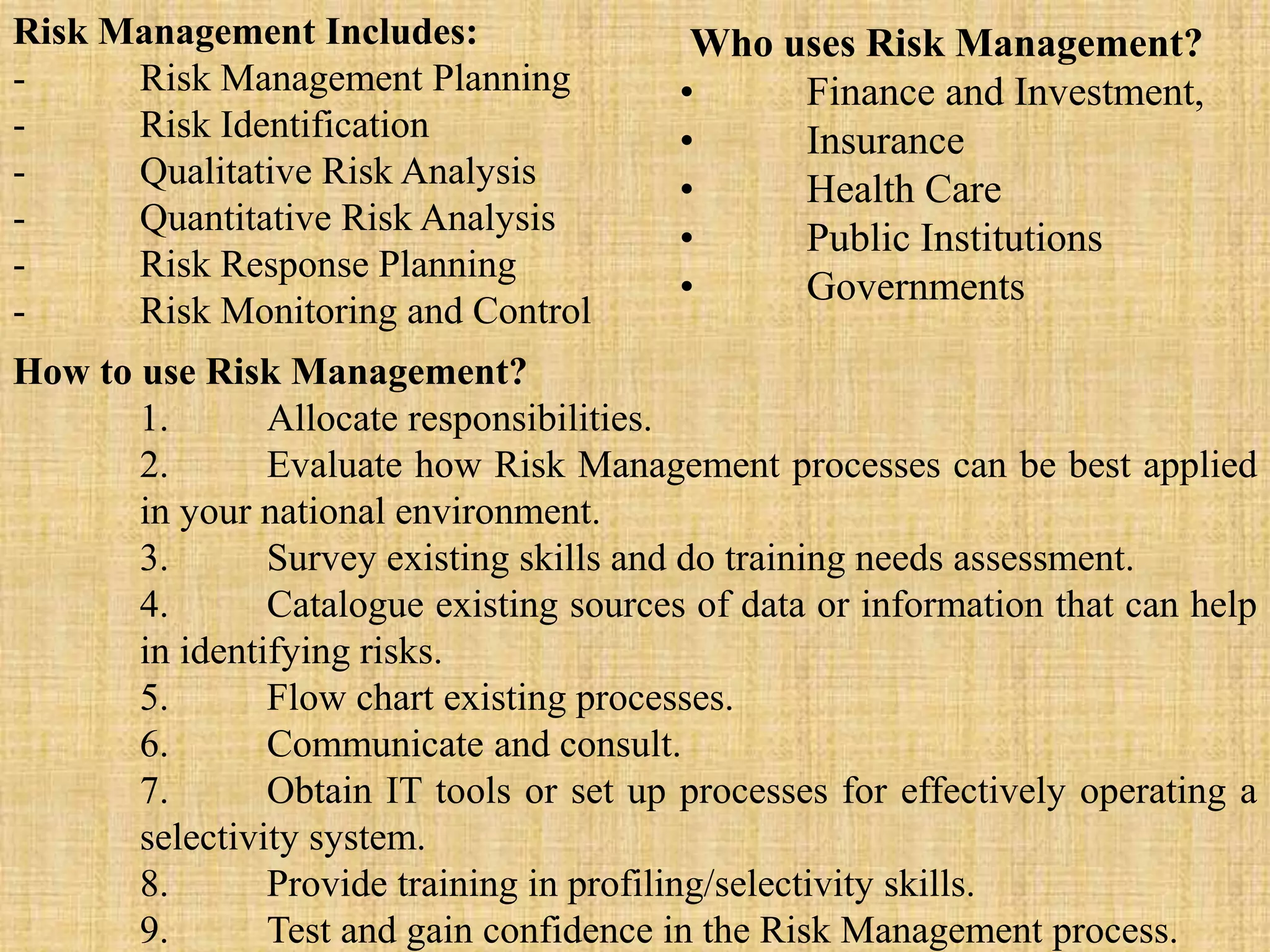

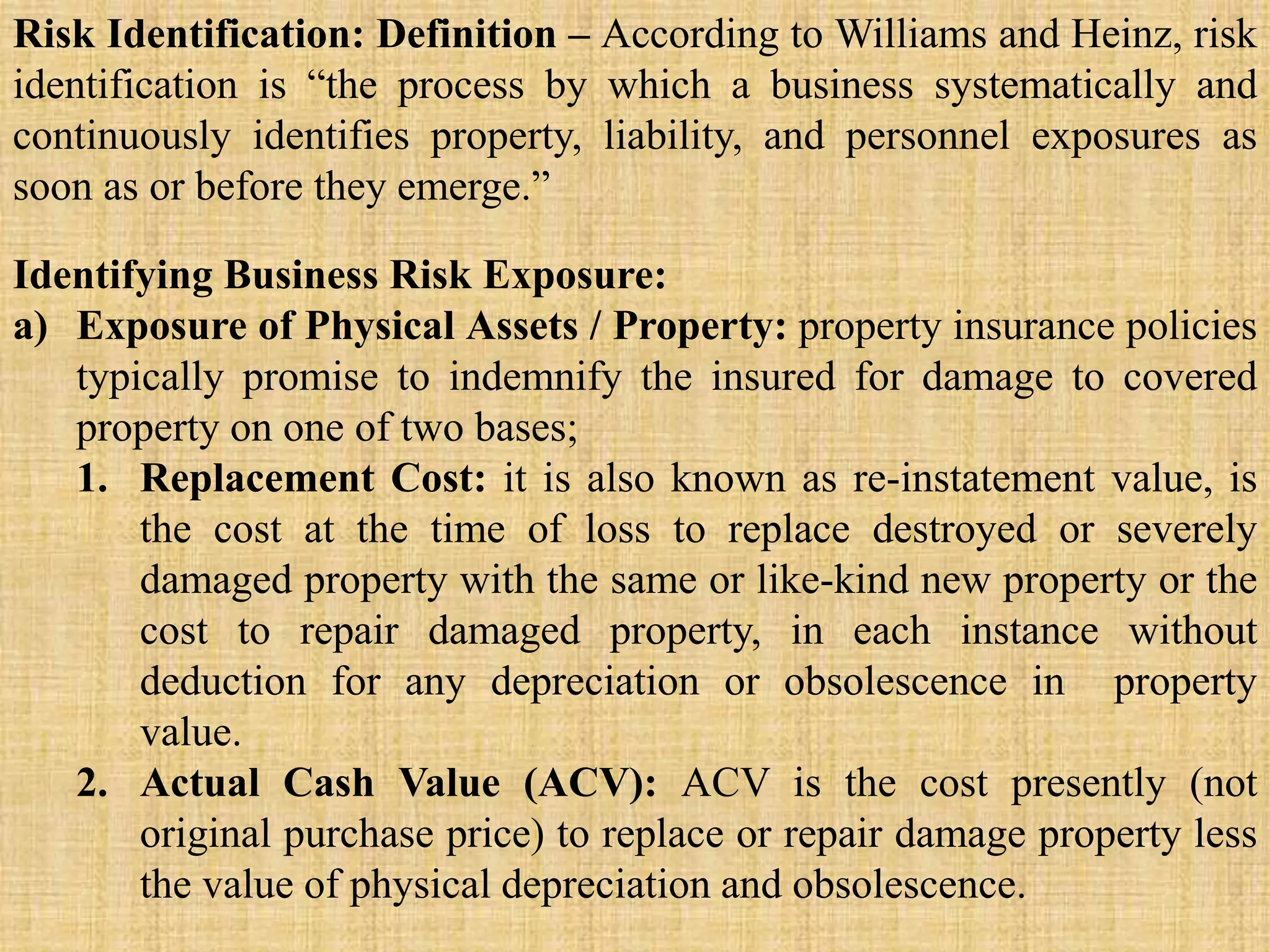

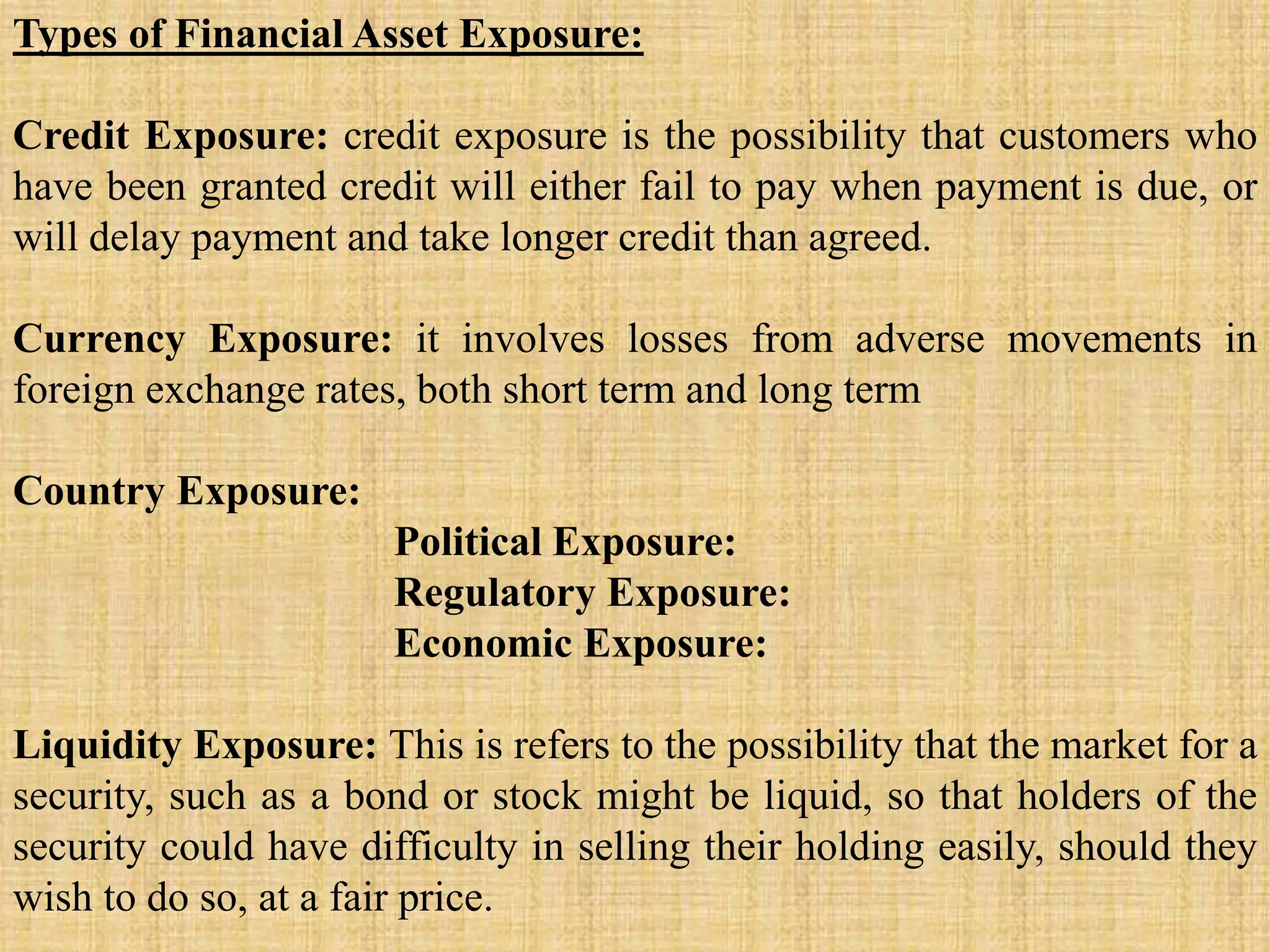

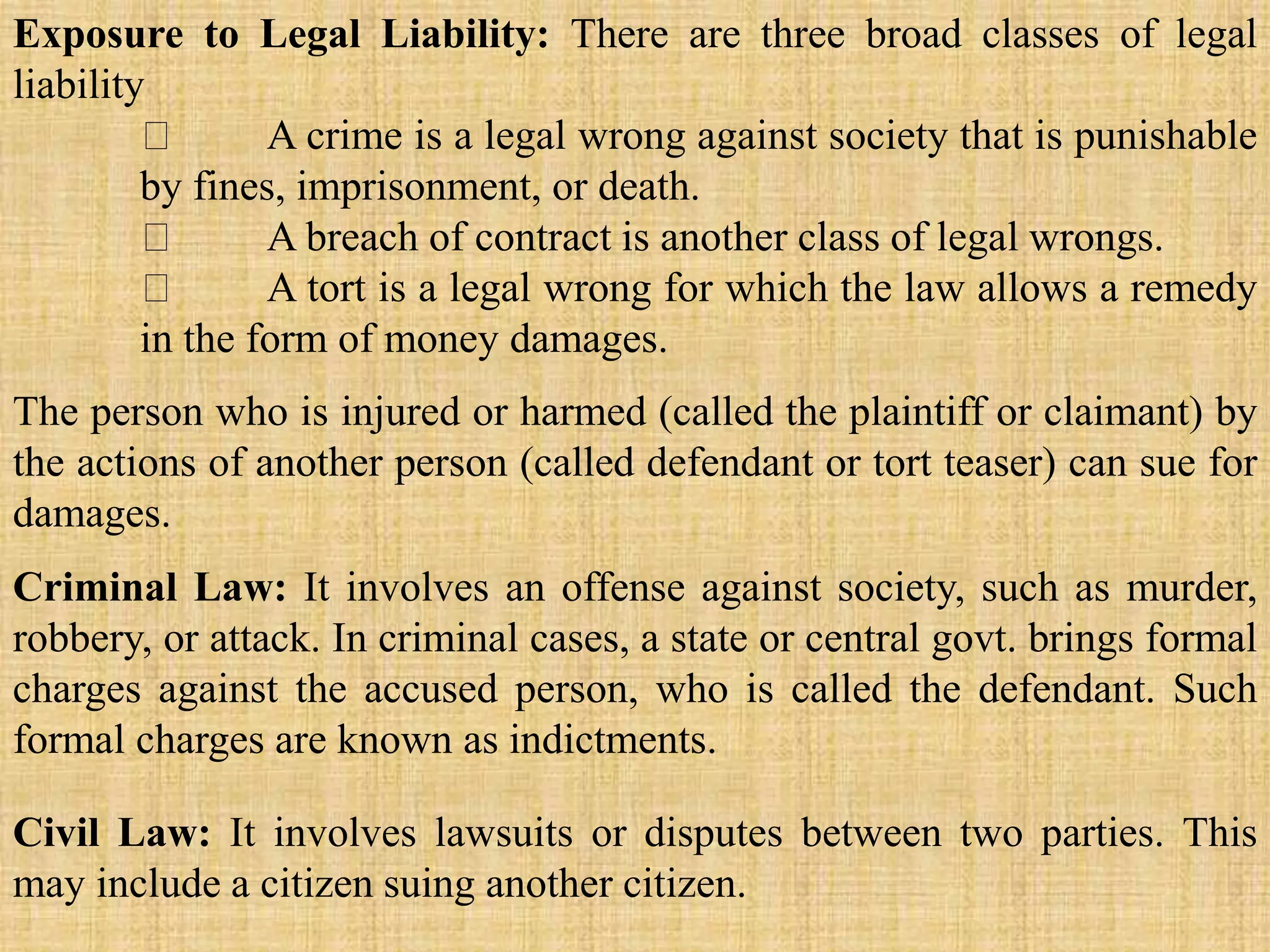

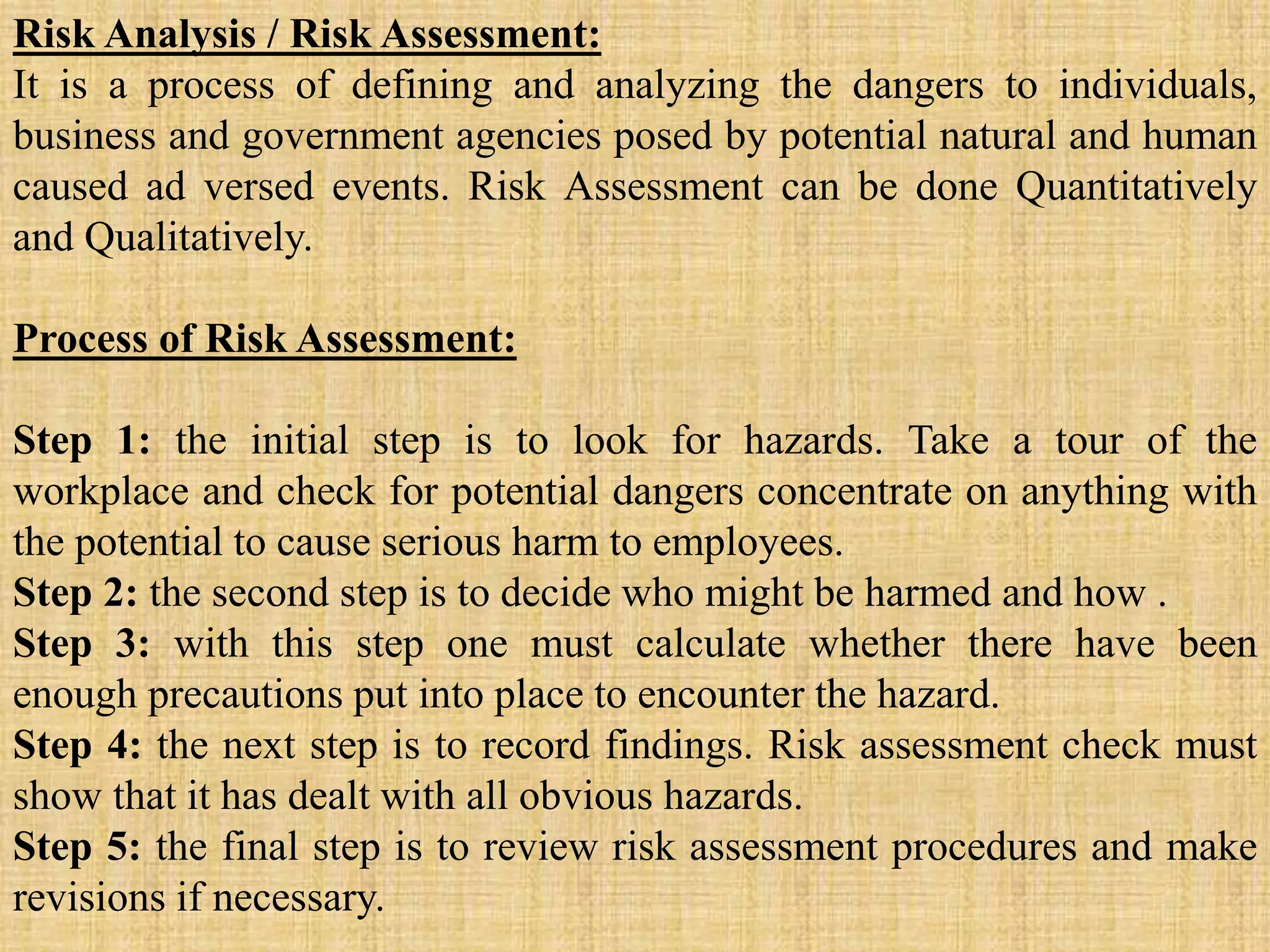

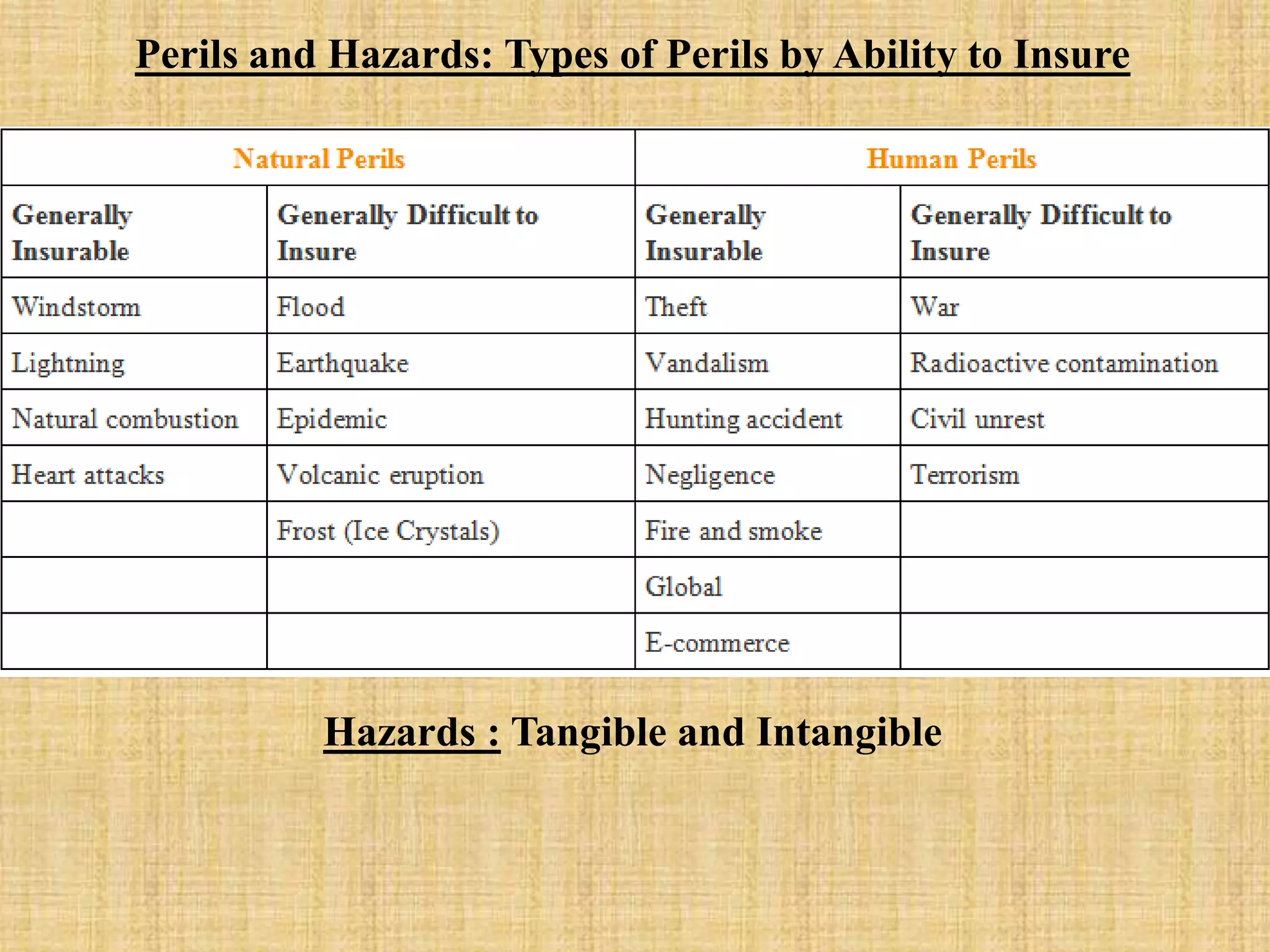

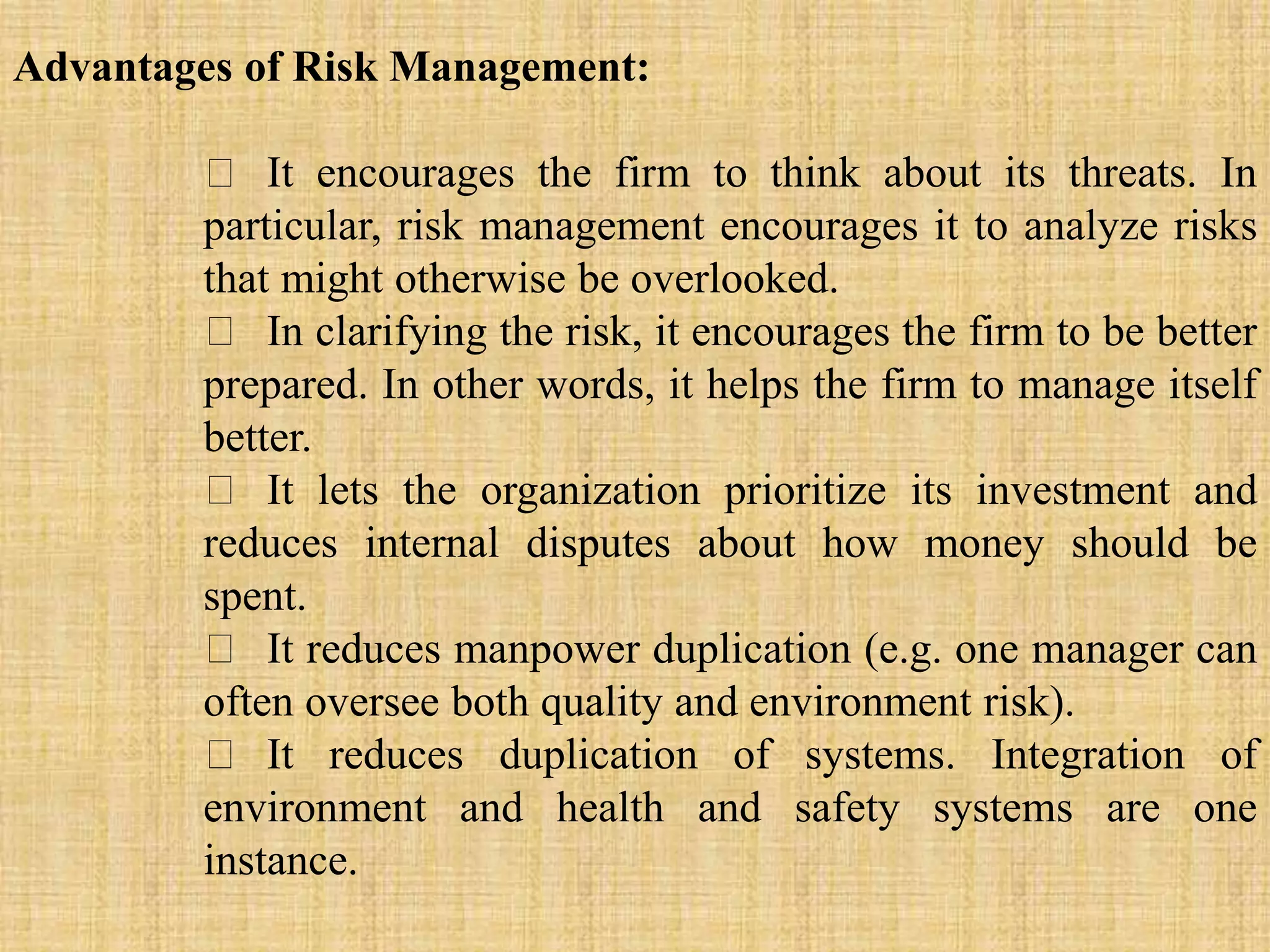

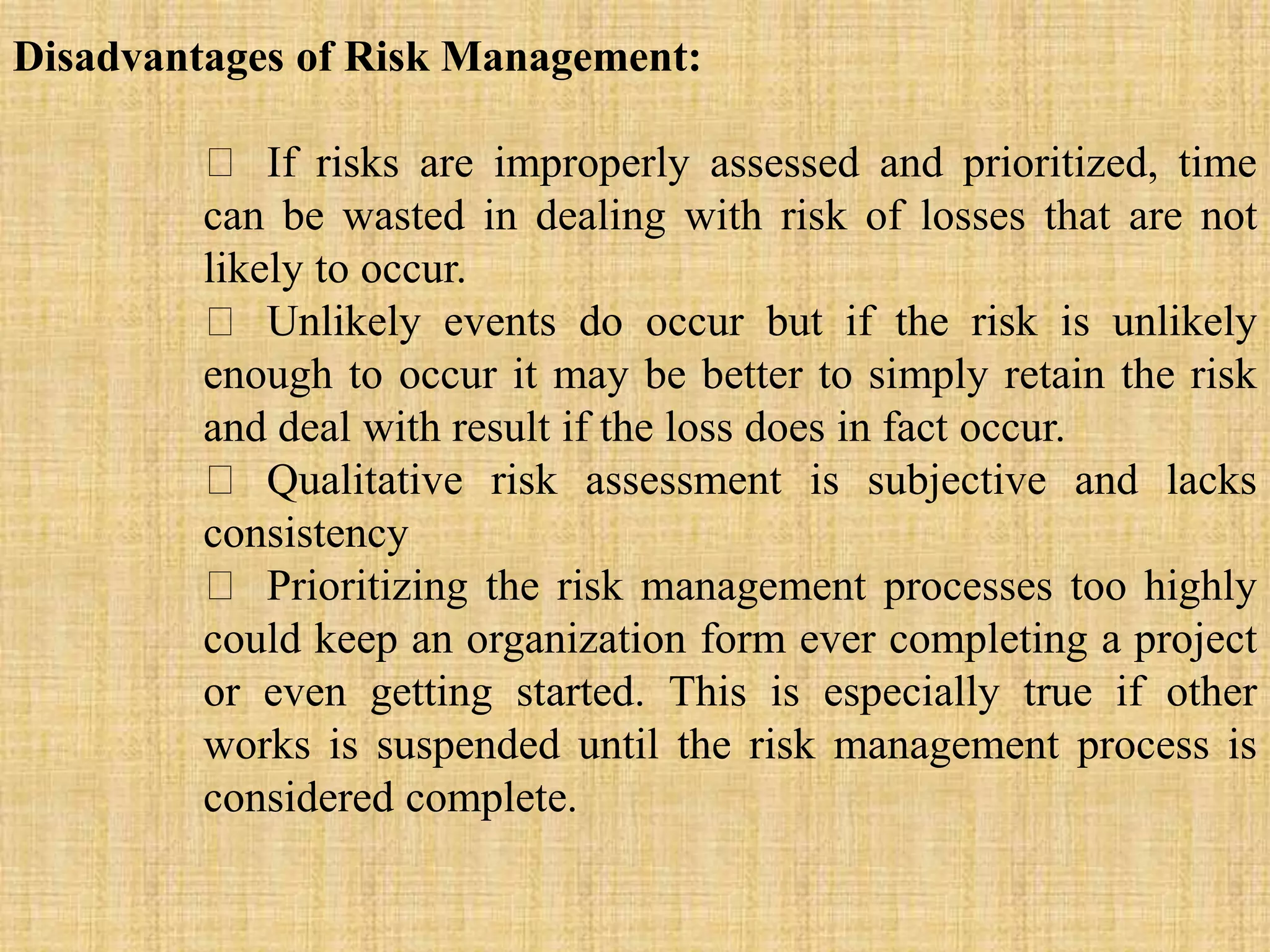

The document provides a comprehensive overview of risk management, defining key concepts such as risk, uncertainty, and various types of risks including strategic, operational, and economic risks. It outlines the processes involved in risk management, including risk identification, analysis, and response planning, emphasizing the importance of preparation and awareness in mitigating potential losses. Additionally, the document discusses different risk management methods and their advantages and disadvantages within organizational contexts.