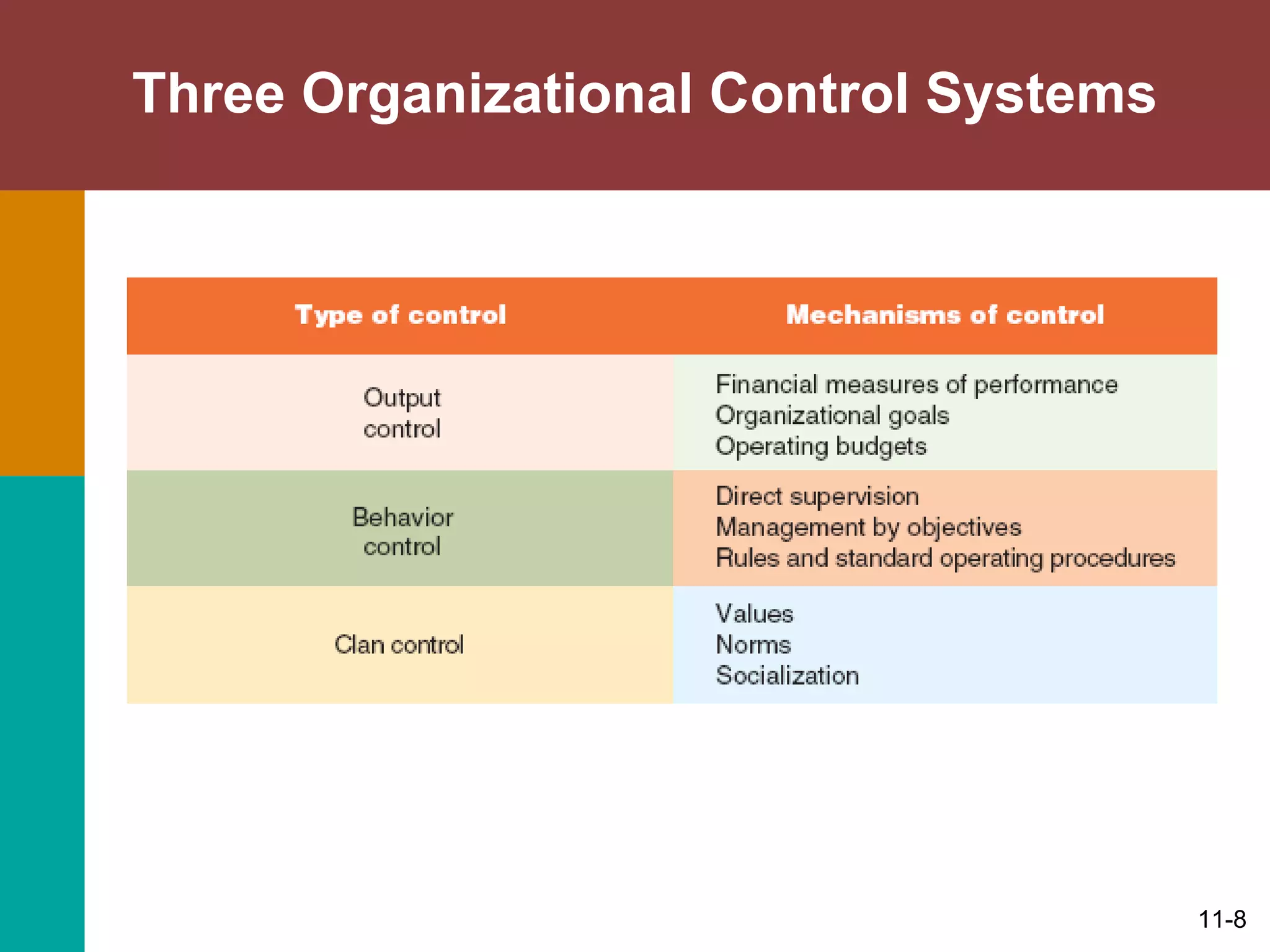

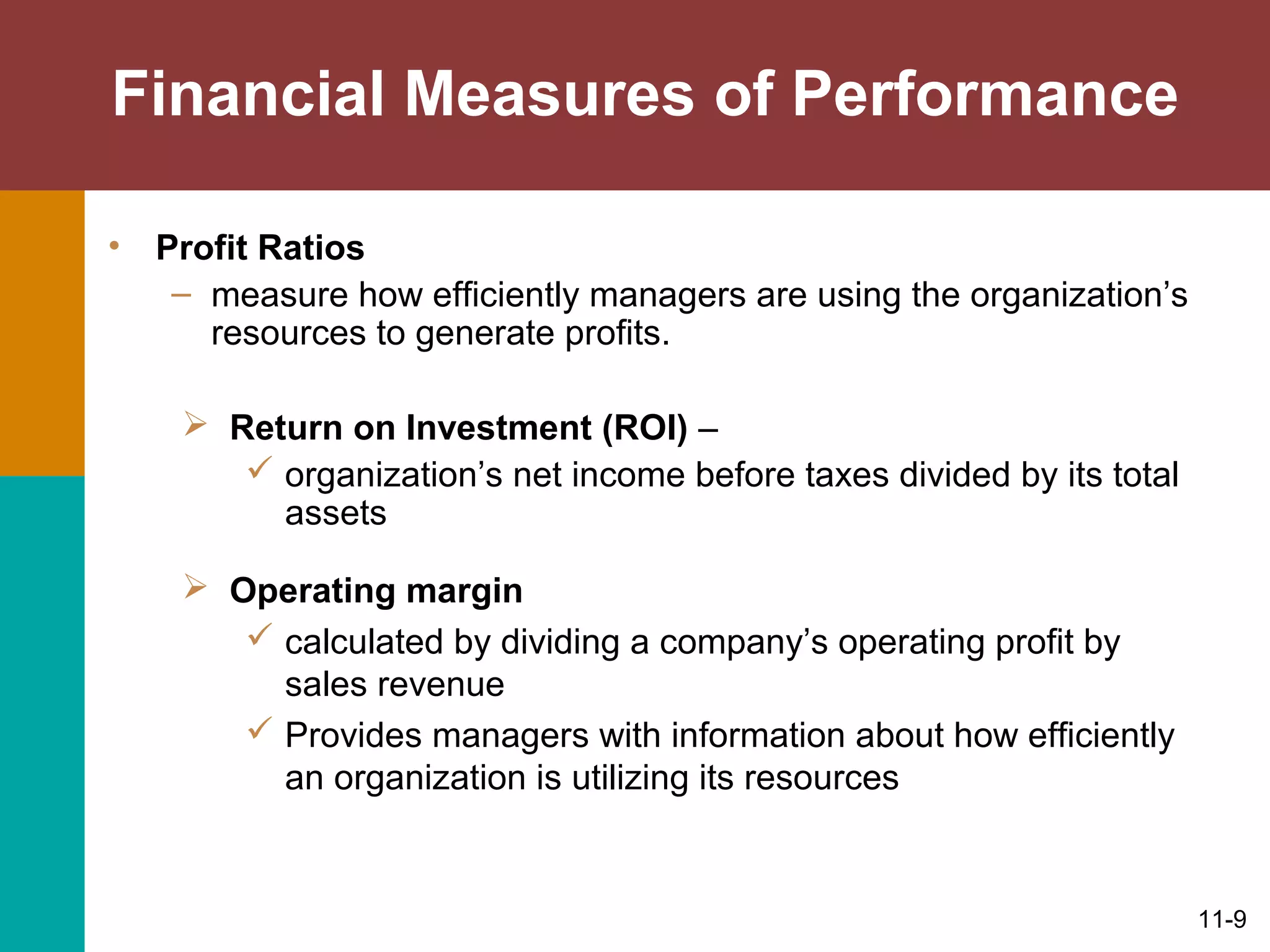

This document discusses organizational control and change. It defines organizational control as how managers monitor performance to achieve goals. There are three types of control systems: feedforward, concurrent, and feedback controls. Managers use output controls like goals and budgets, behavior controls like supervision, and clan controls based on shared values. The document also examines Lewin's force field theory of change and outlines steps to implement and evaluate organizational change.