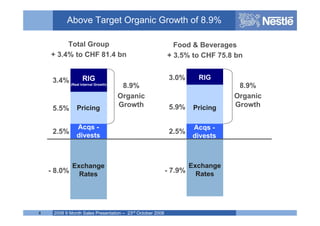

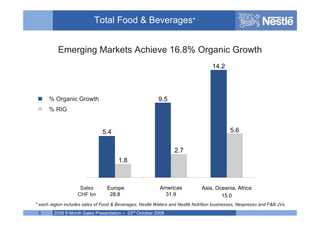

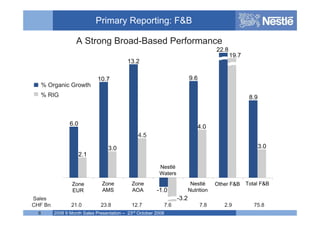

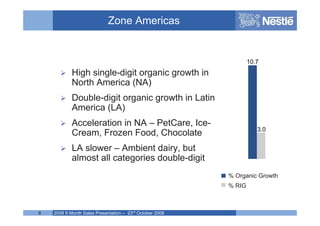

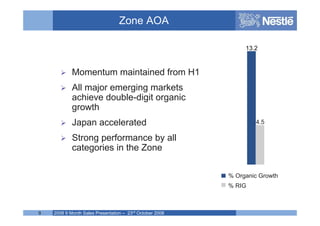

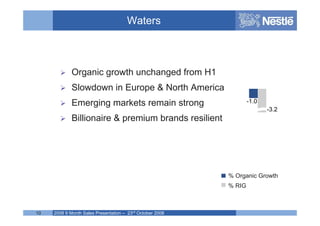

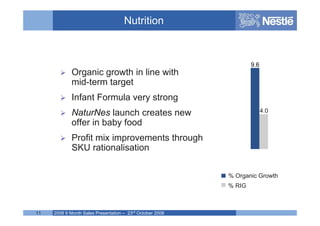

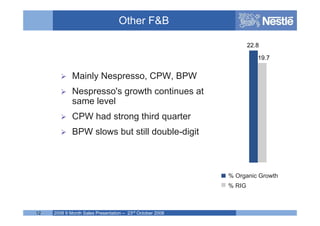

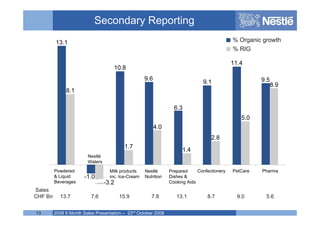

Roddy Child-Villiers, Head of Investor Relations, presented Nestle's 2008 9-month sales results. Key highlights included organic growth of 8.9% for the group and food & beverage division, comfortably above the long-term target. Emerging markets achieved 16.8% organic growth. The financial position remained strong with a high credit rating and predictable cash flows. The outlook for full-year organic growth was improved to around 8%.

![Eletropaulo 1 q10_eng_final [modo de compatibilidade]](https://cdn.slidesharecdn.com/ss_thumbnails/eletropaulo1q10engfinalmododecompatibilidade-100517082821-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![The Evolution of Sales Performance Management [presentation]](https://cdn.slidesharecdn.com/ss_thumbnails/infographic-spm-evolution-presentation-141212095258-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)