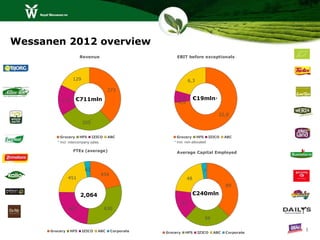

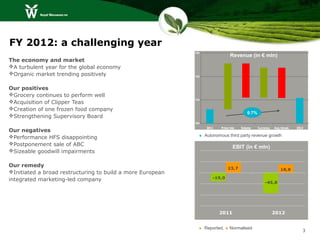

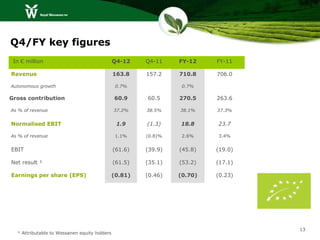

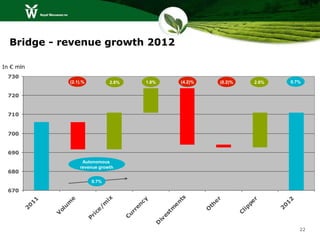

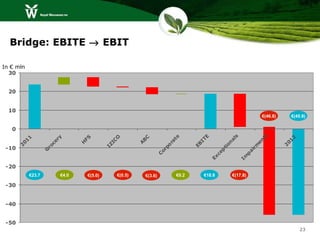

Wessanen reported revenue of €711 million in 2012, a 0.7% increase over 2011. EBIT before exceptionals was €19 million, down from €23.7 million in 2011. The Grocery segment continued to perform well with 4.6% autonomous growth in 2012. However, performance in the Health Food Stores and IZICO segments was disappointing. A broad restructuring was initiated to build a more integrated European company.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)