Download to read offline

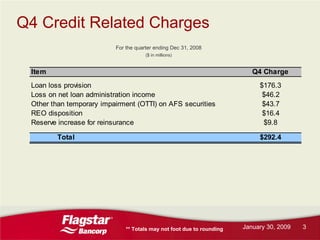

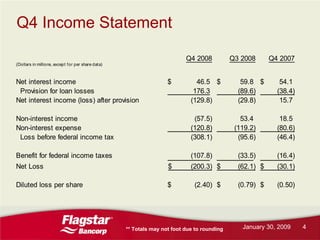

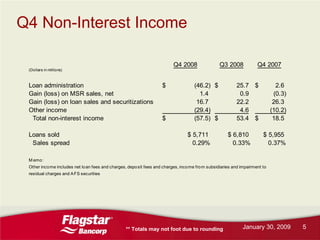

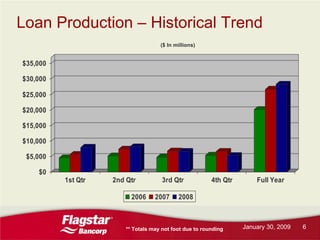

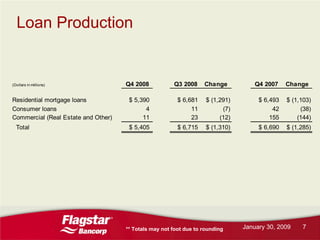

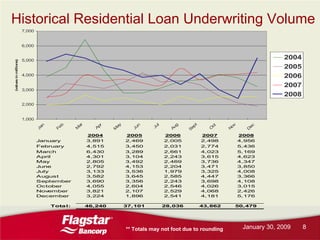

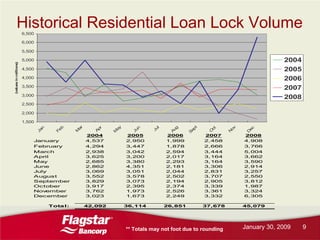

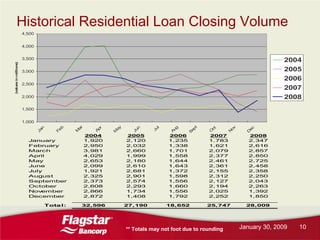

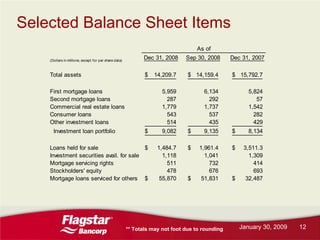

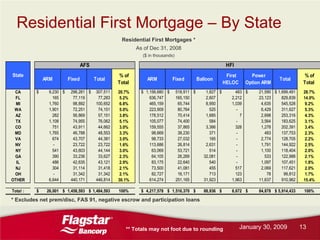

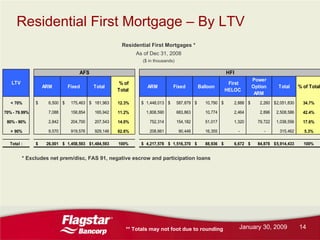

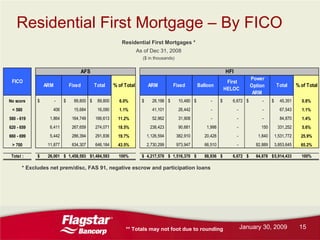

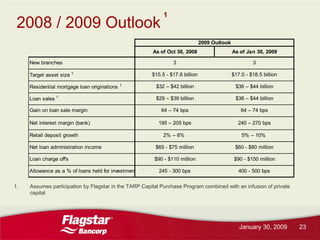

The document provides financial results for Flagstar Bancorp for Q4 2008, including a net loss of $200.3 million compared to a net loss of $62.1 million in Q3 2008. It also discusses factors impacting results such as a $176.3 million provision for loan losses. Additionally, the document reviews historical trends in loan production, underwriting, locks, and closings which have declined significantly from 2007 levels.