Downloaded 277 times

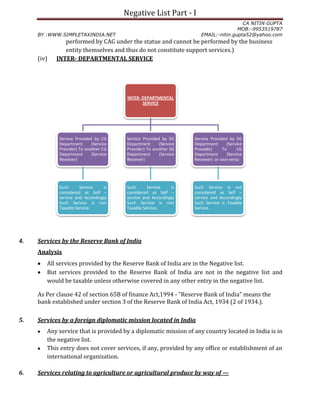

1. The document discusses India's negative list of services that are exempted from service tax. It covers 17 categories of services exempted, including services provided by the government, Reserve Bank of India, agricultural services, trading of goods, manufacturing processes, and more. 2. Key points covered include the definition of government and local authority in the context of the exemption, analysis of specific services covered/not covered under various exemptions, and treatment of bundled services and advertisement agency services for taxability. 3. Printing and publishing of yellow pages and business directories is liable to service tax since it is not considered sale of advertising space exempted under the negative list.