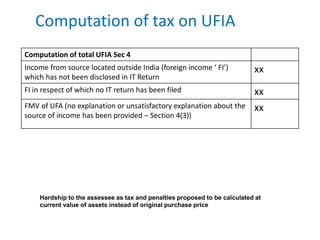

Downloaded 139 times

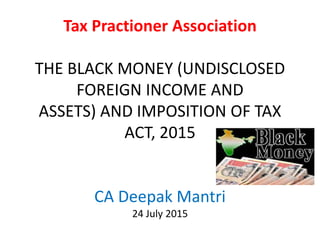

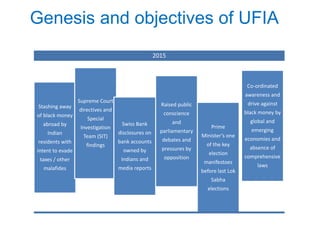

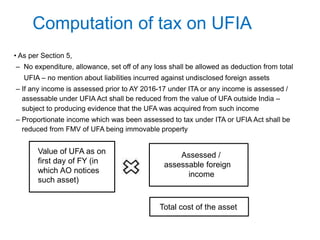

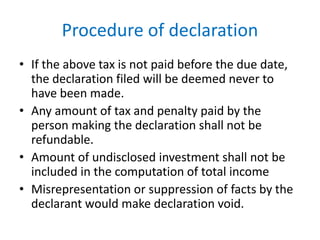

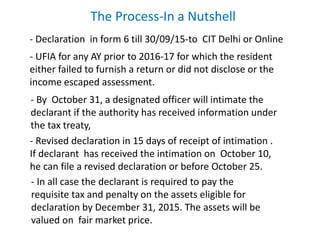

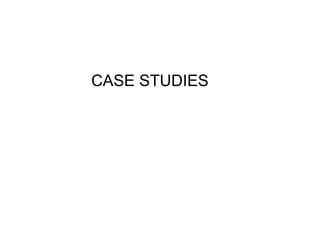

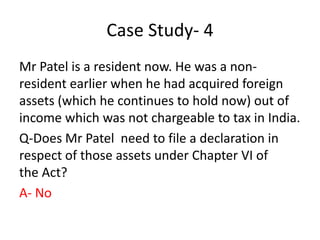

![Undisclosed foreign income and assets

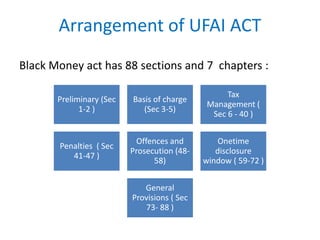

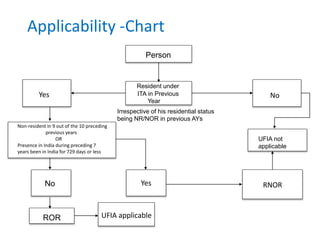

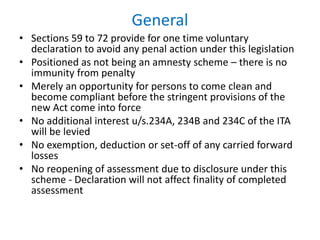

Section 2(11), 2(12) and 4

Undisclosed Foreign Income and Asset

(UFIA) [Section 2(12)]

• Total amount of undisclosed income from

source located outside India [as referred in

Section 4(1)], and

• Value of UFA located outside India

• UFIA shall be

– Income from a source located outside India

which has not been disclosed in the Return

of Income filed under the ITA

– Income from sources, in respect of which

return is not filed under the ITA and

– Value of undisclosed foreign asset (UFA)

located outside India

(fair market value in the previous year in

which AO notices UFA- method of valuation

prescribed by rules)

• Computation of UFIA laid down under section 5

of the Bill

Undisclosed Asset located outside India

(UFA) [Section 2(11)]

• An asset (including financial interest in any

entity) located outside India

• Asset can be held by the assessee in his name

or in respect of which he is a beneficial owner,

and

• Assessee has no explanation about the

source of investment in such asset or the

explanation given by him is the opinion of

the Assessing Officer is unsatisfactory

Test of undisclosed foreign asset is to

explain the source of investment

Asset not taxable as UFA if its source is

explained (even though it is not declared

in the return of income)](https://image.slidesharecdn.com/blackmoney-copy-150806172211-lva1-app6892/85/Black-money-14-320.jpg)

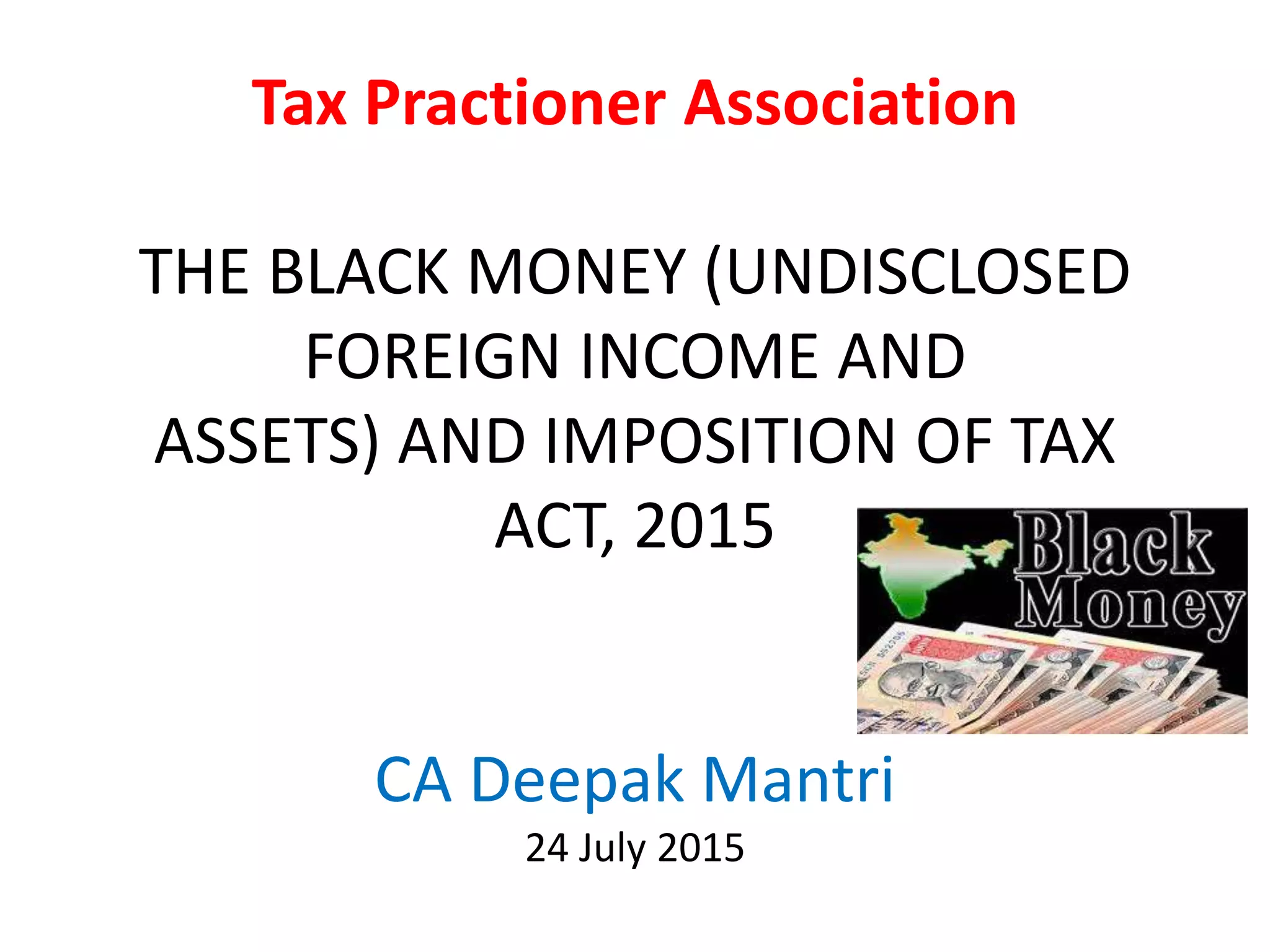

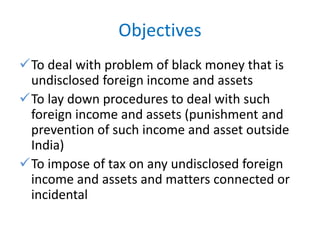

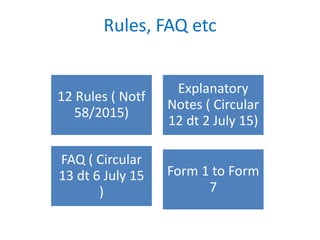

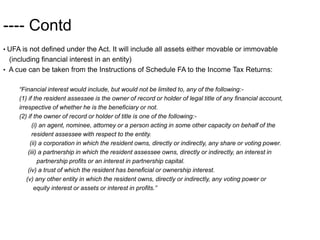

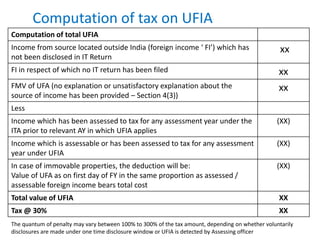

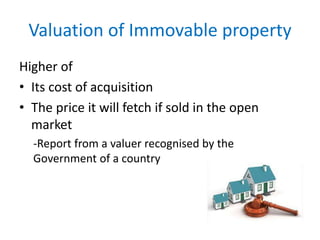

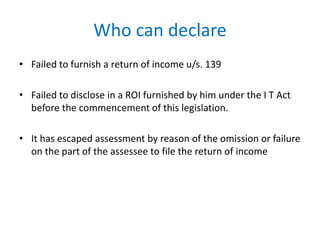

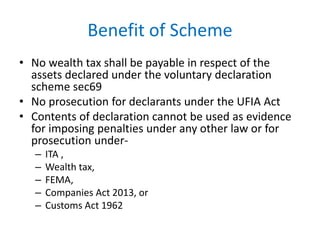

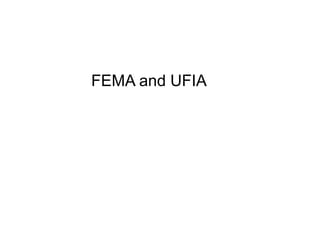

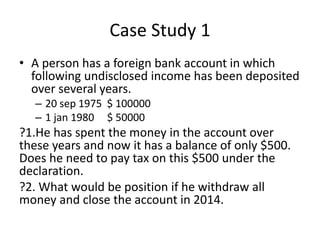

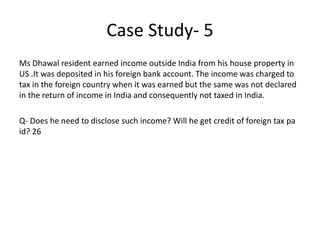

![Illustration

• Mr. A acquired foreign asset (immovable property) in the AY 2010-11 for

Rs.60 lacs. Out of the total investment, Rs.40 lacs was assessed to tax in an

earlier year.

• In AY 17-18, AO identified the value of such undisclosed asset as Rs.2 crore

for which no explanation was provided.

Computation of total UFIA Rs. (in crores)

FMV of UFA (no explanation provided

or explanation not satisfactory) 2.00

Less

Income which has been assessed to tax for any (1.33)

assessment year under the ITA prior to relevant AY in which

the Black Money Act [Rs.2crore -(Rs.2crore X 0.40 lacs / 0.60lacs)]

Amount chargeable to tax under Black Money Act 0.67](https://image.slidesharecdn.com/blackmoney-copy-150806172211-lva1-app6892/85/Black-money-20-320.jpg)

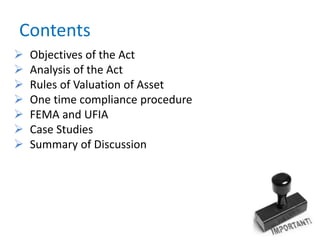

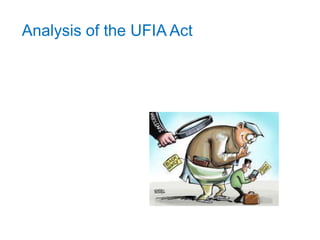

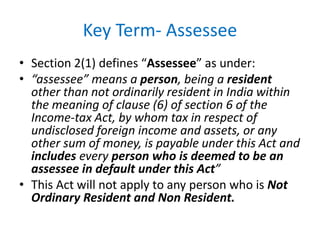

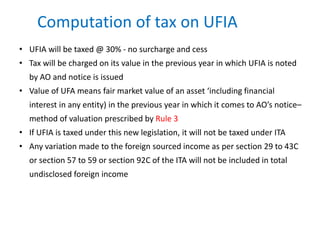

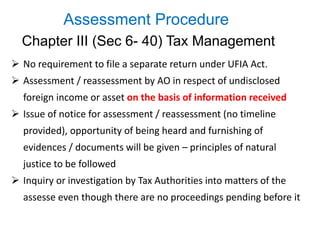

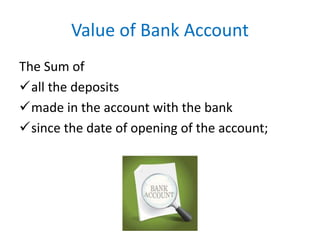

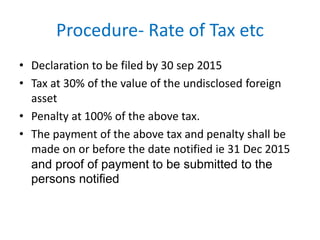

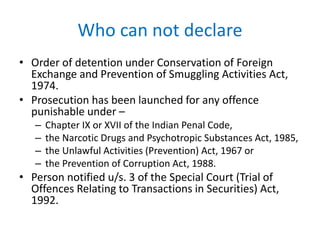

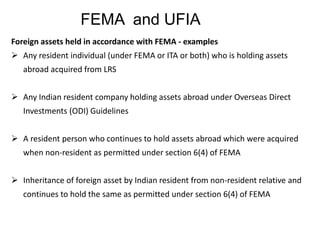

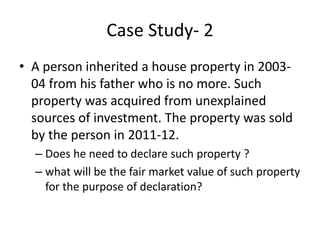

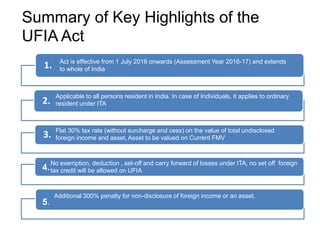

![Penalty Contd…

Nature of default Penalty

Failure to furnish documents before tax authority [Section 45]

If any person fails to:

a) answer any question asked by tax authority

b) sign a statement which he is legally bound to do so

c) attend or to give evidence or produce books of account

Rs.0.5 Lakhs to

Rs.2

Lakhs

Punishment for second and subsequent offences [Section 58]

If a person, who has been convicted for an offence as mentioned above,

is again convicted for an offence under this Bill

Rs. 5 lakhs to Rs.

1

Crore](https://image.slidesharecdn.com/blackmoney-copy-150806172211-lva1-app6892/85/Black-money-25-320.jpg)

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 aims to address the issue of undisclosed foreign income and assets held by Indian residents, imposing penalties and taxes on individuals who fail to disclose such assets. The act outlines procedures for compliance, valuation of assets, and enforcement mechanisms, and includes a one-time compliance window allowing individuals to declare undeclared foreign assets to avoid penalties. International cooperation has increased with agreements for information exchange, further enforcing the fight against black money stashed abroad.