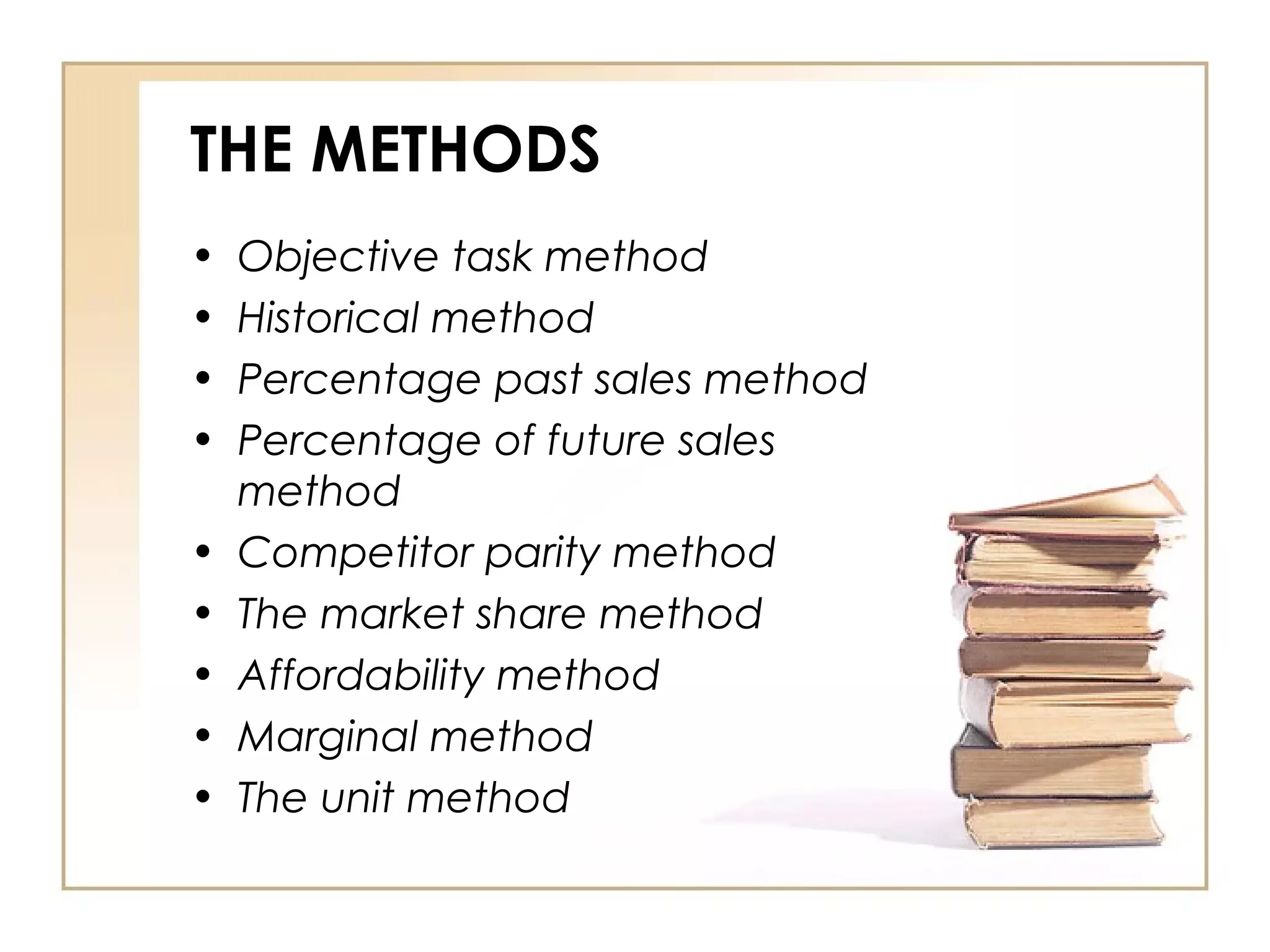

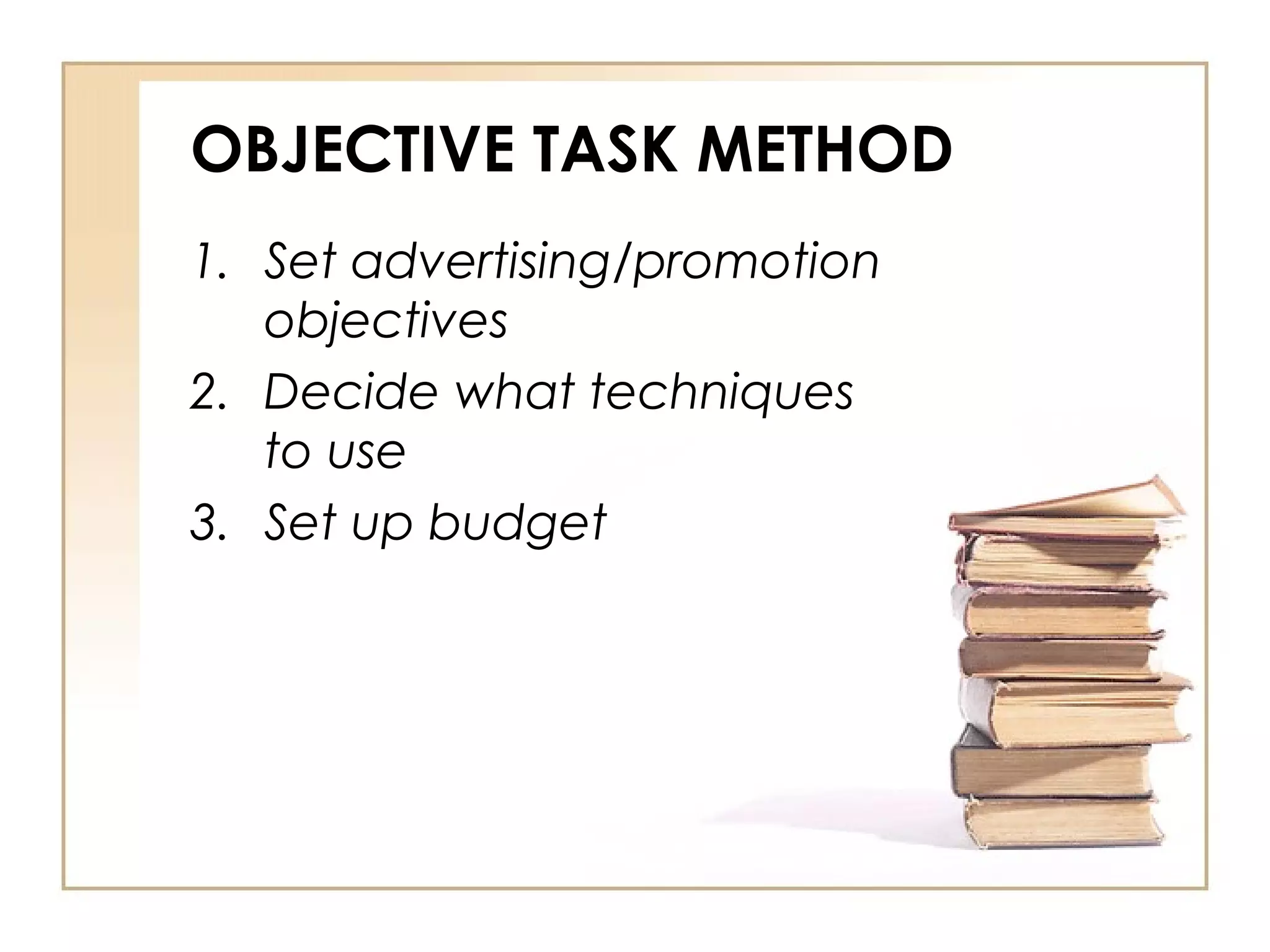

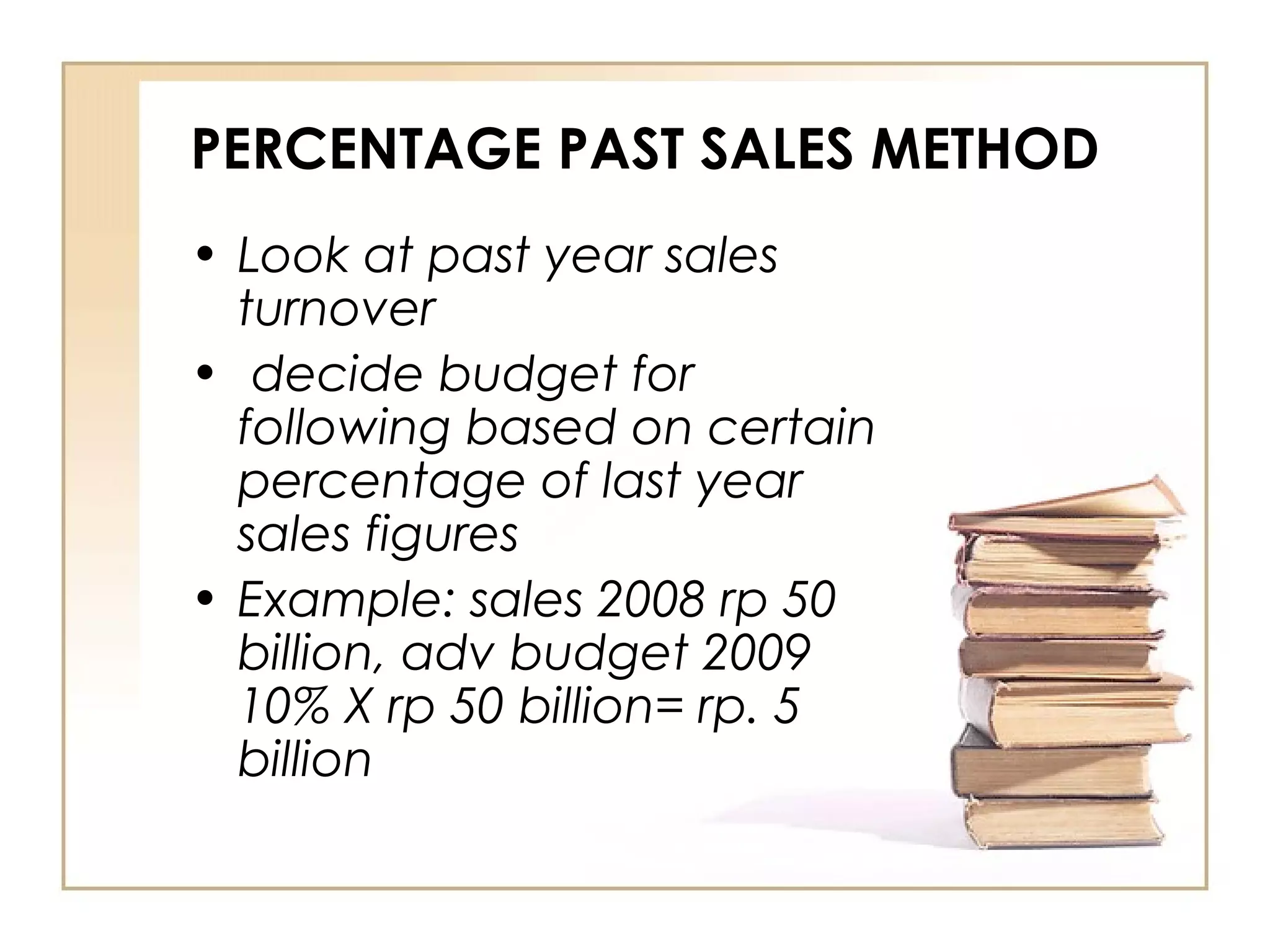

This document outlines 9 different methods for setting advertising budgets: objective task method, historical method, percentage past sales method, percentage of future sales method, competitor parity method, market share method, affordability method, marginal method, and unit method. It provides a brief description of each method, including examples for some. The document concludes by asking which methods might be used by large multinational companies versus local small companies.