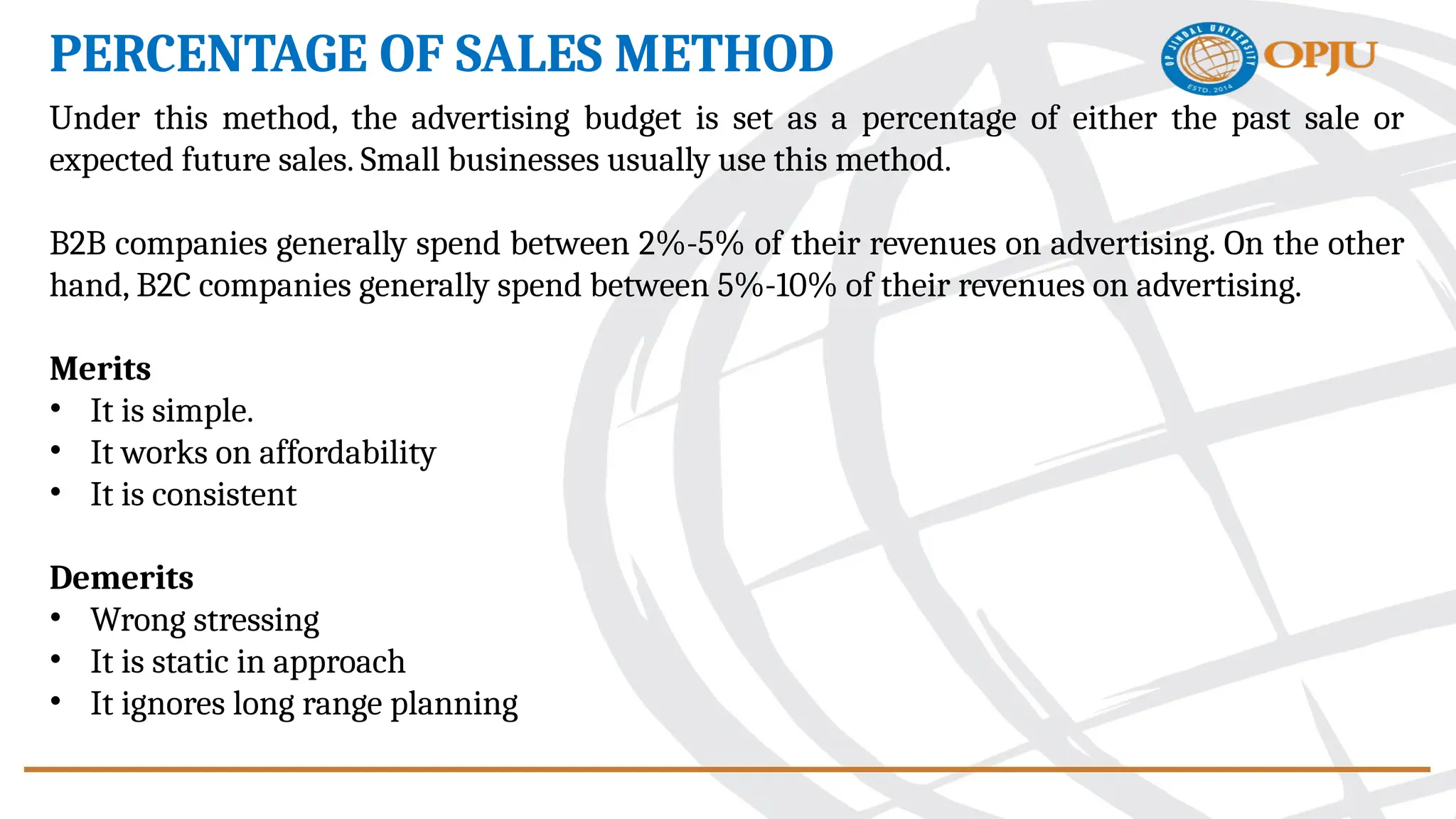

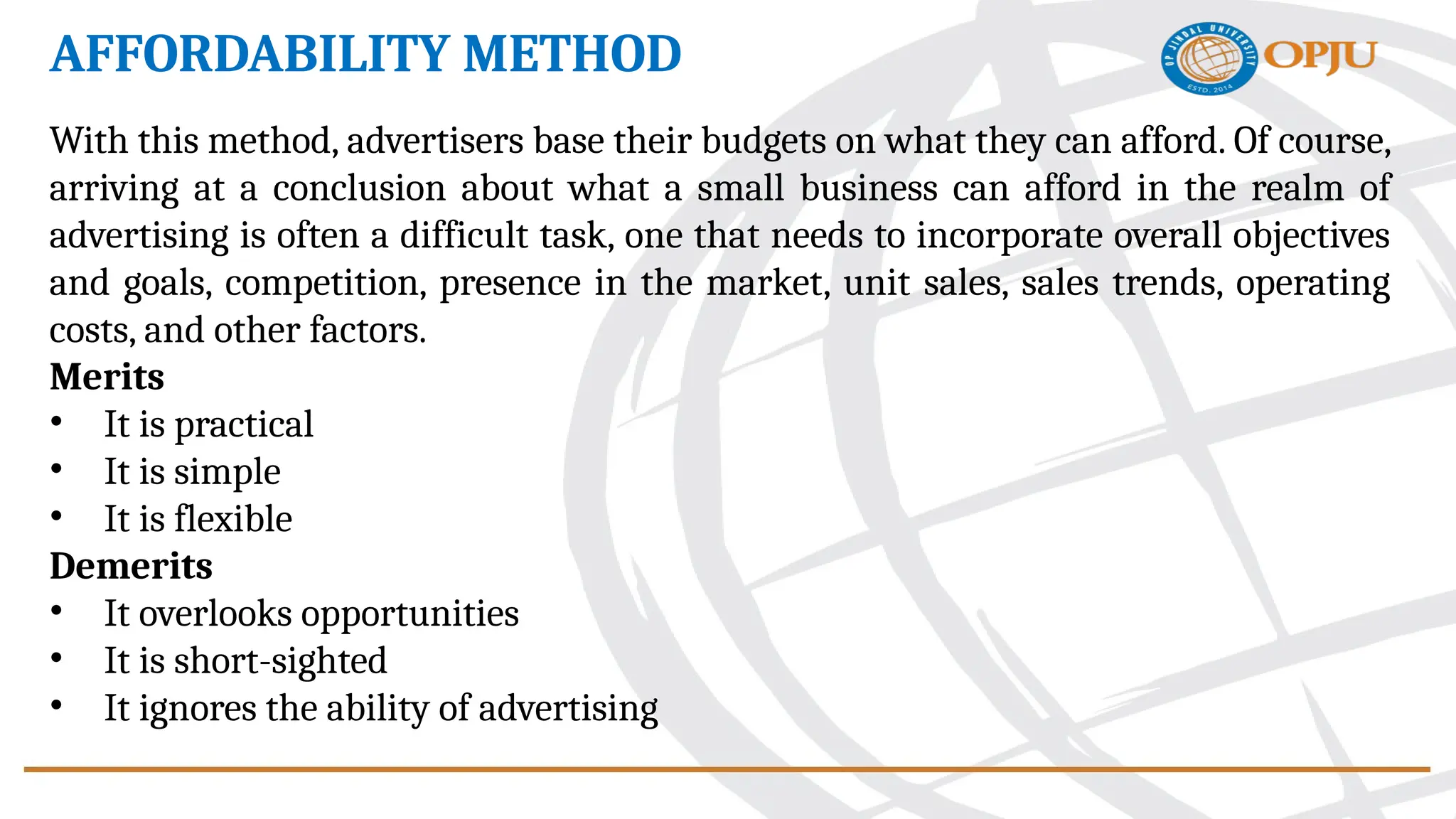

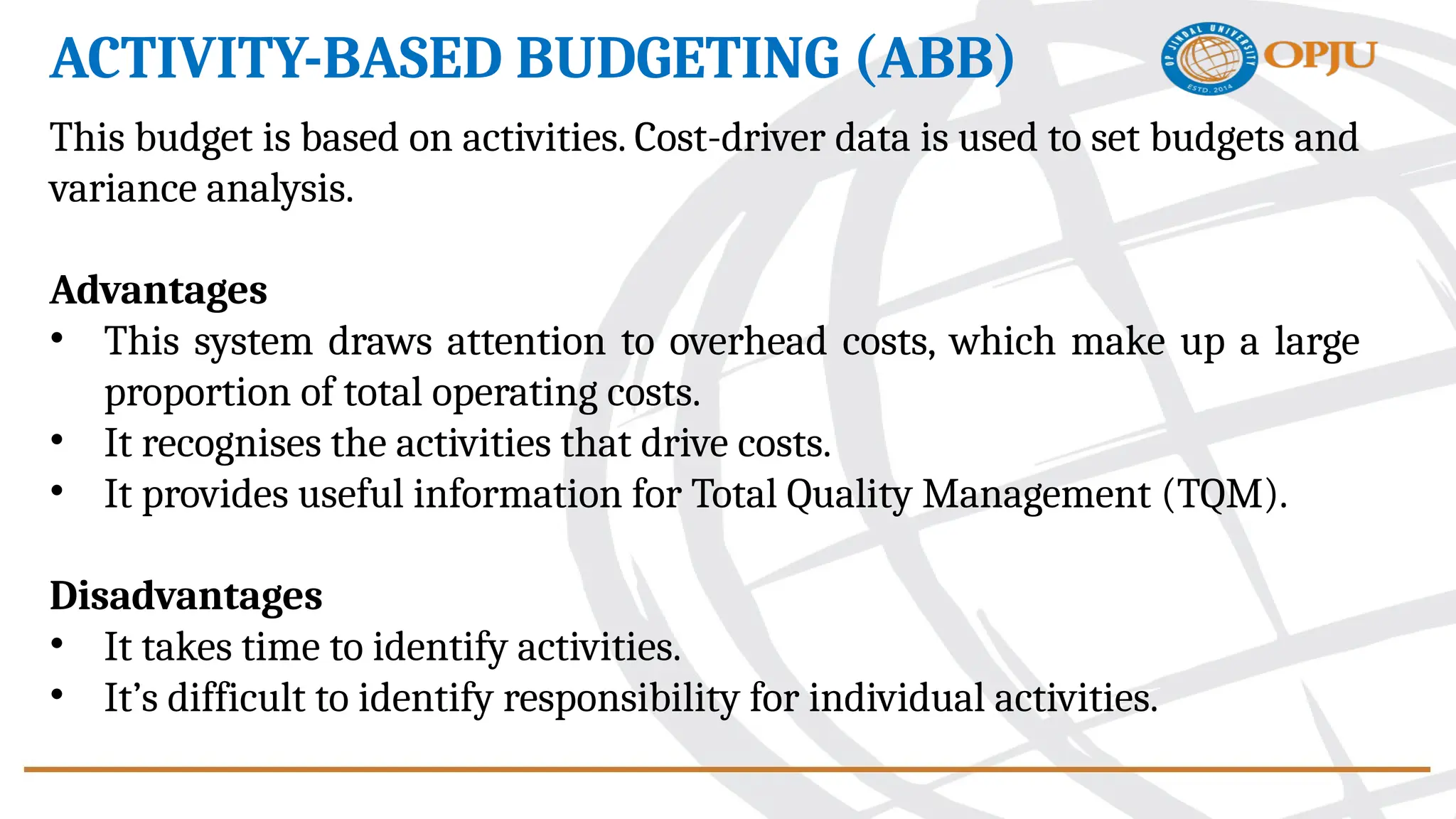

The document provides an overview of advertising budgeting, detailing the significance of an advertising budget as an estimate of promotional expenditures and its relationship with marketing objectives. It discusses various methods for budgeting, including the percentage of sales, objective and task, and competitive parity methods, along with their merits and demerits. Additionally, it covers different budgeting approaches and types, highlighting factors that influence budget size.