Downloaded 503 times

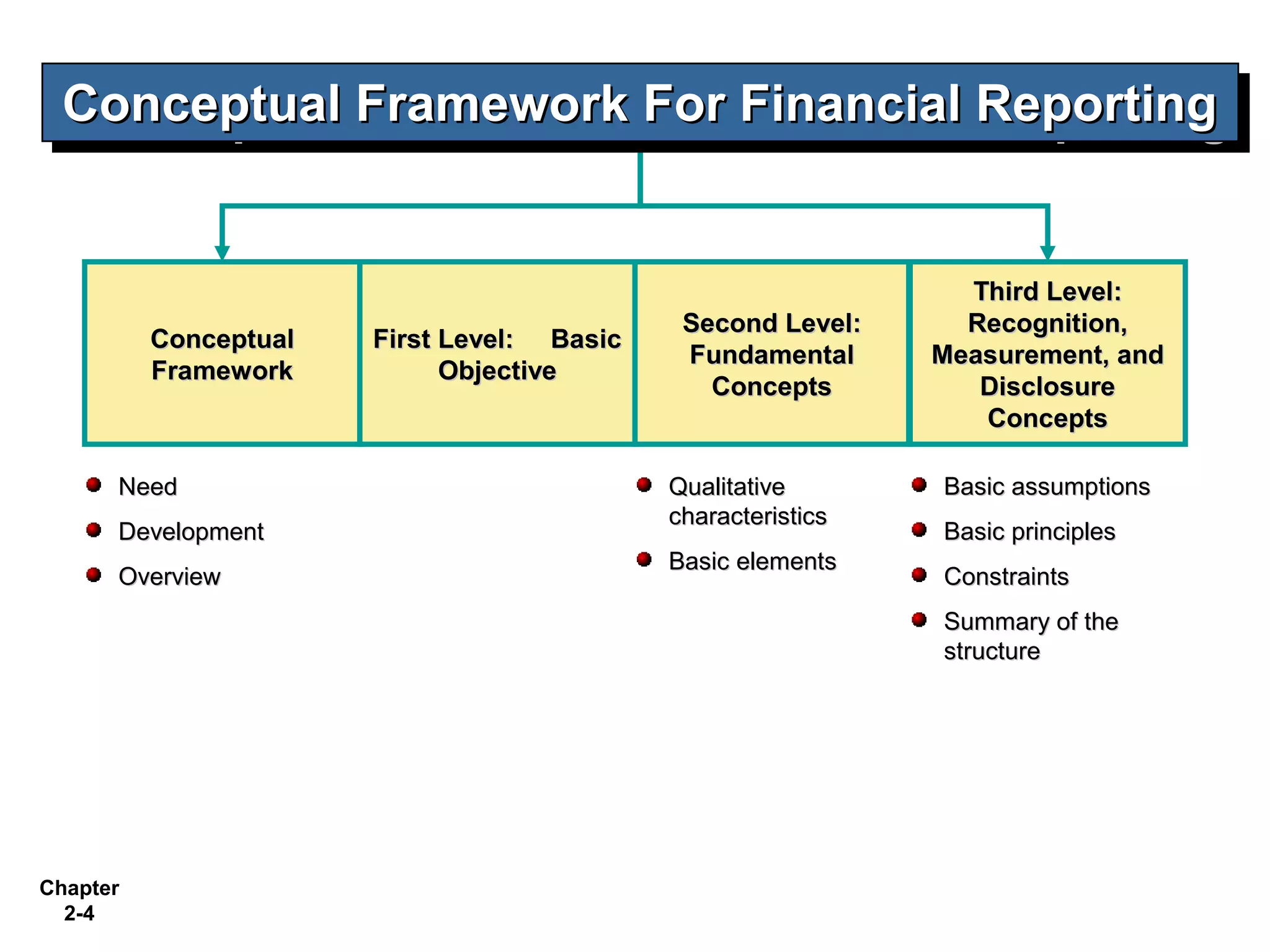

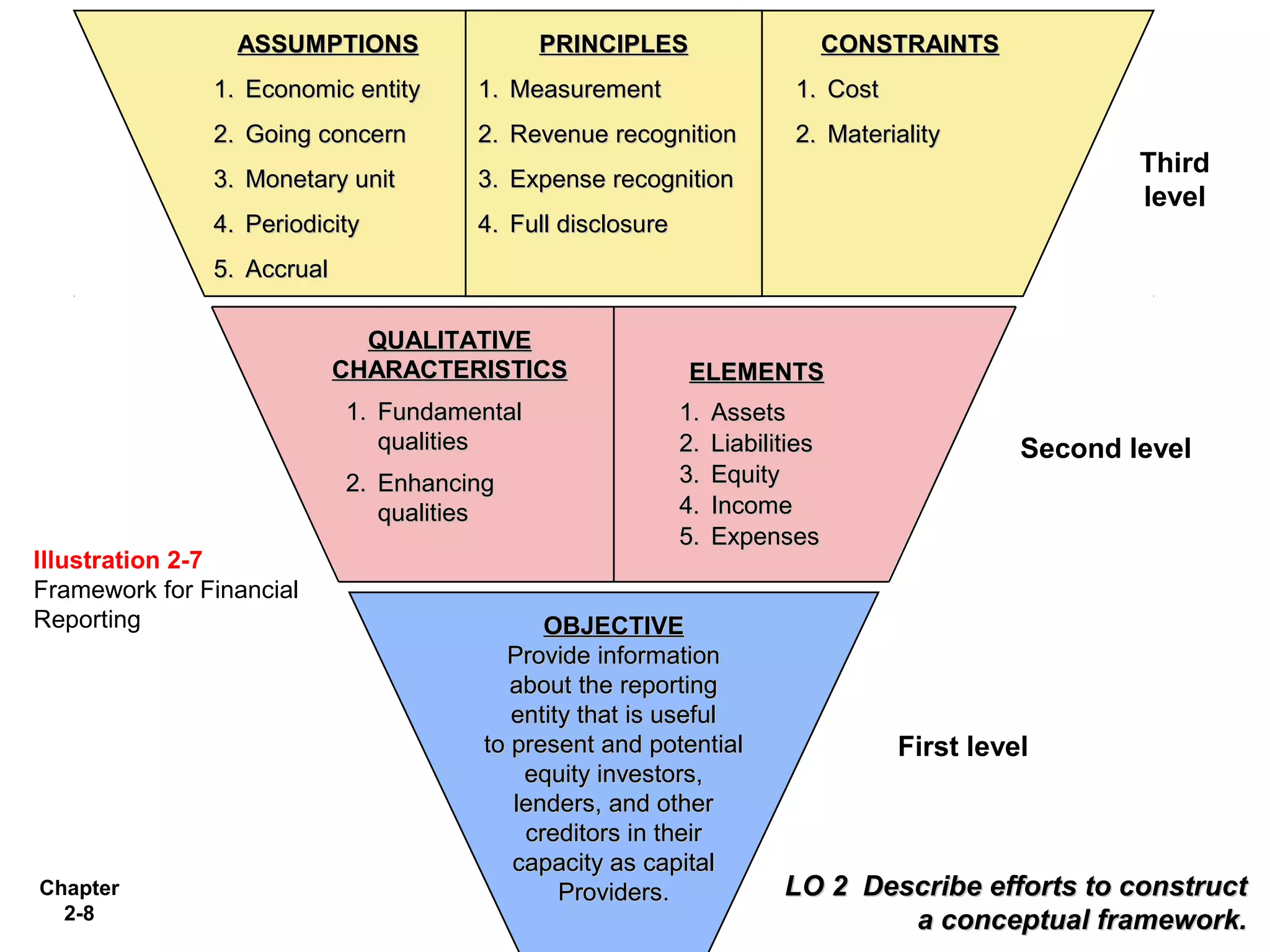

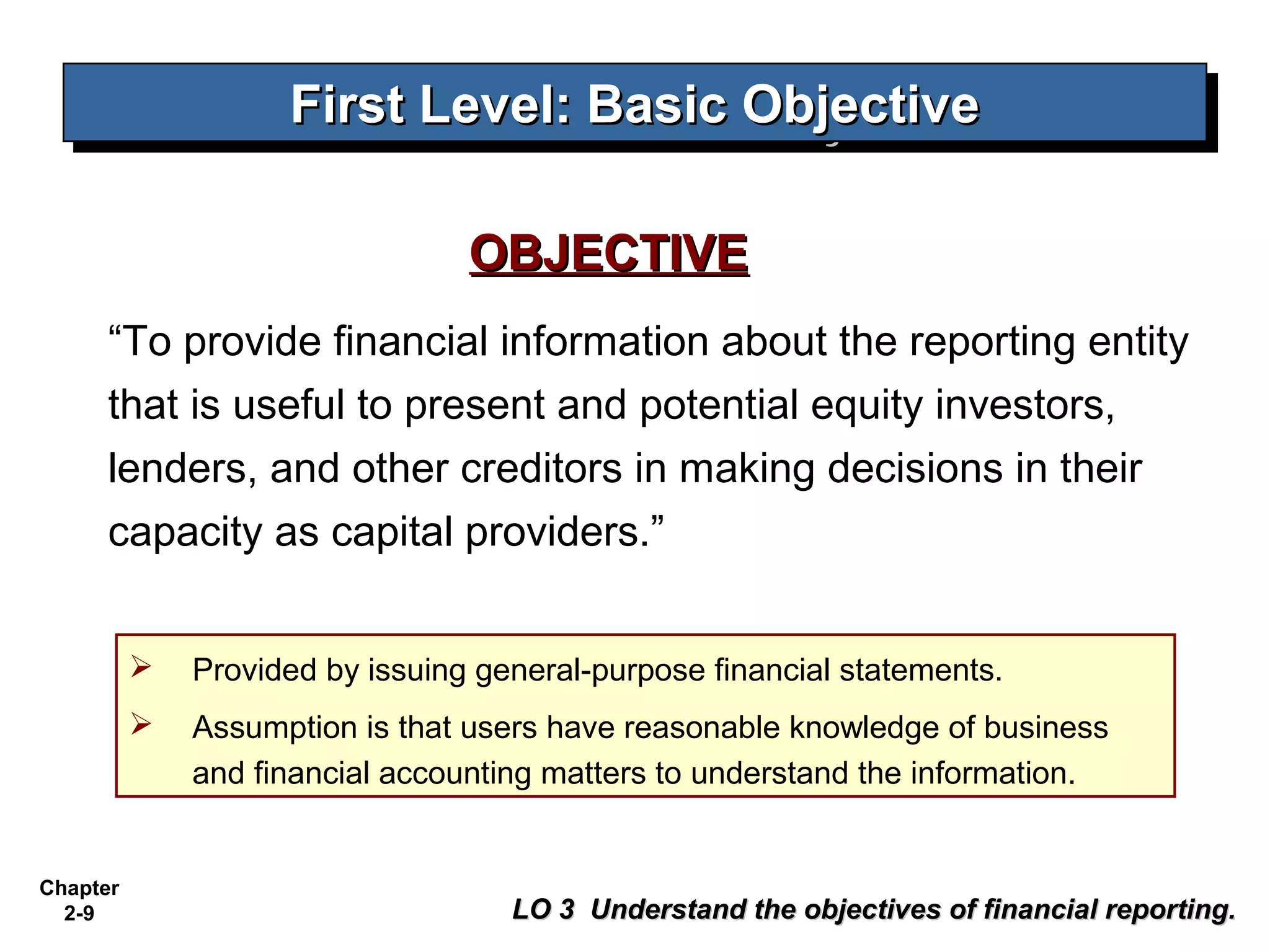

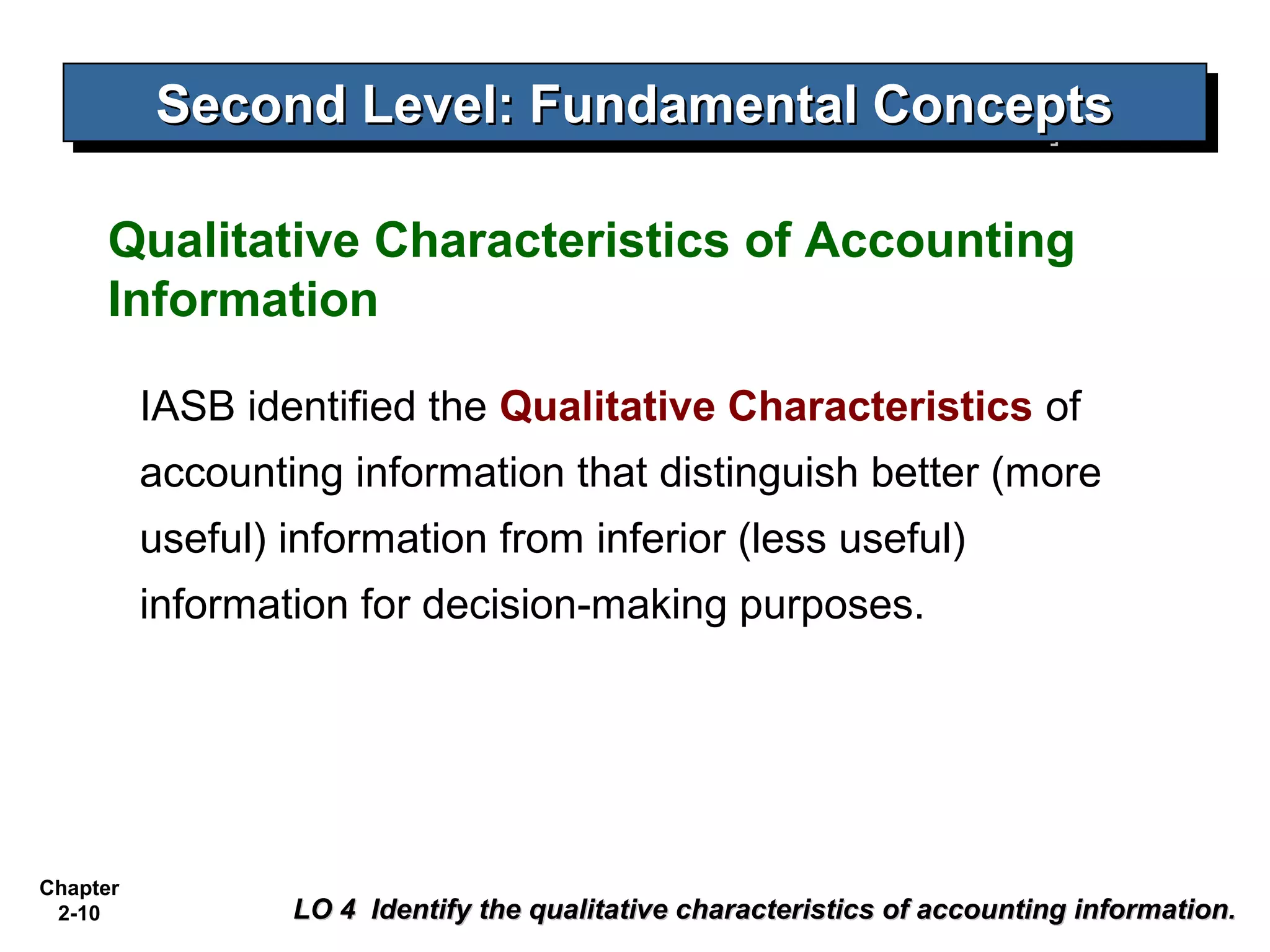

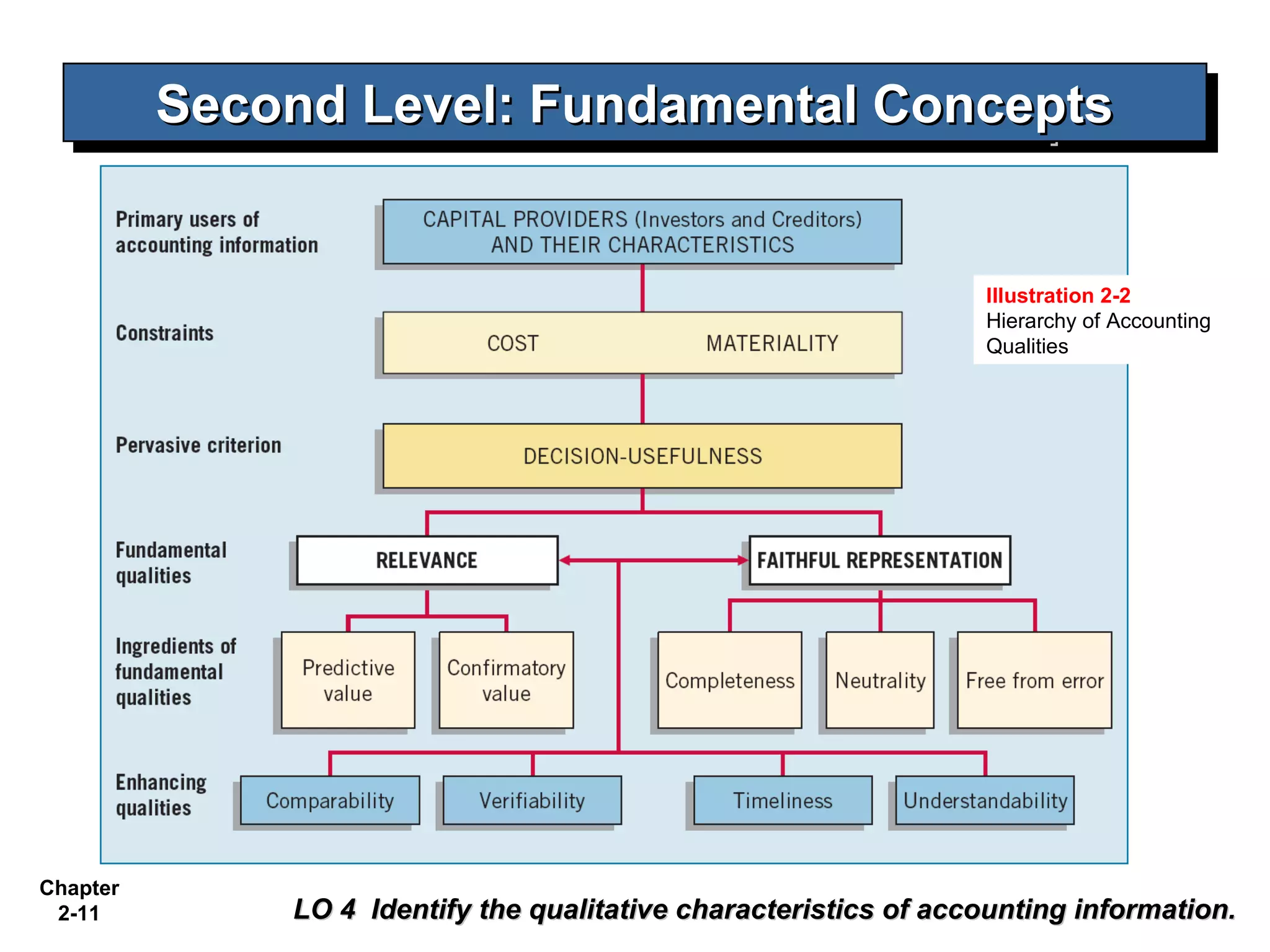

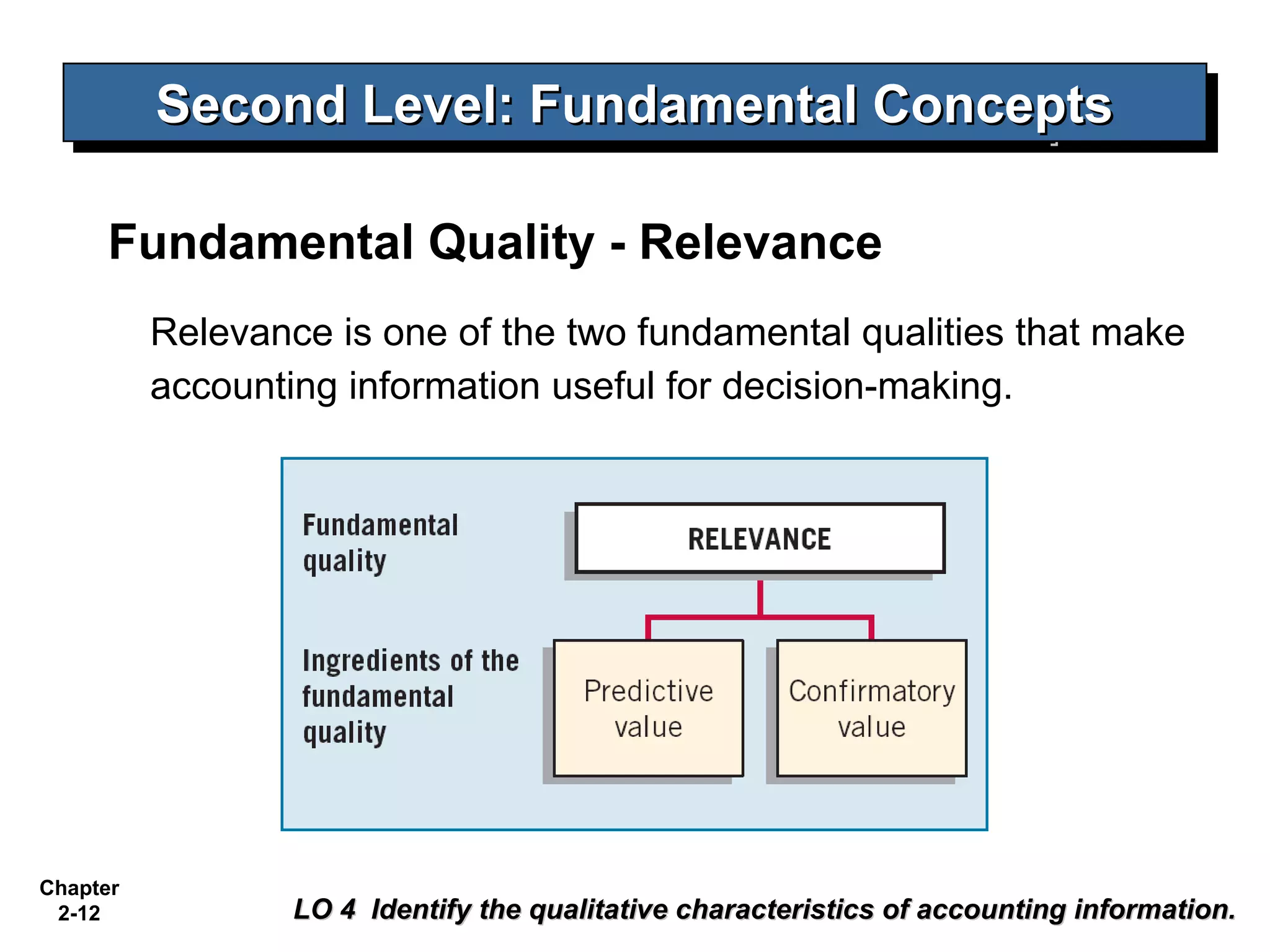

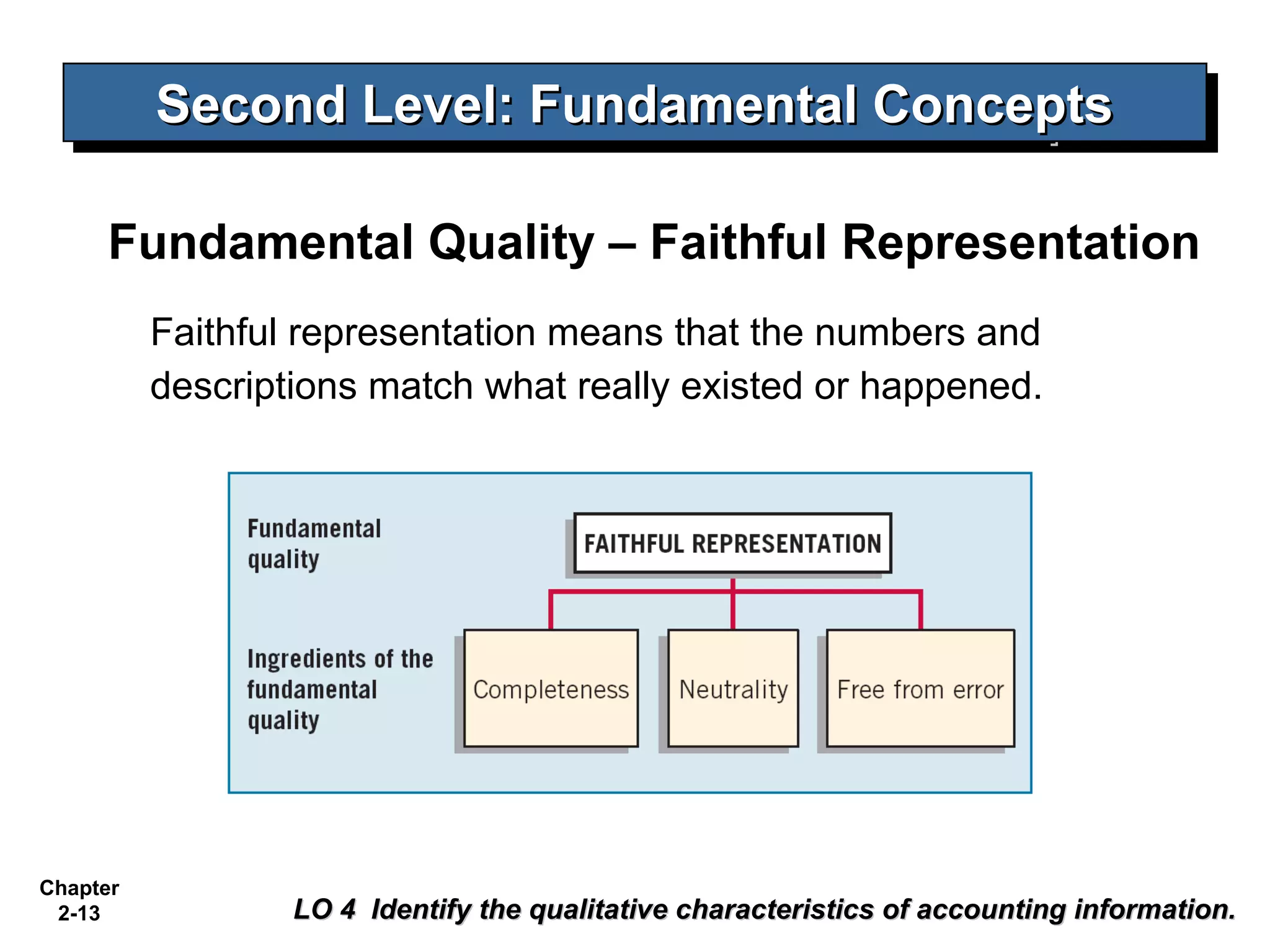

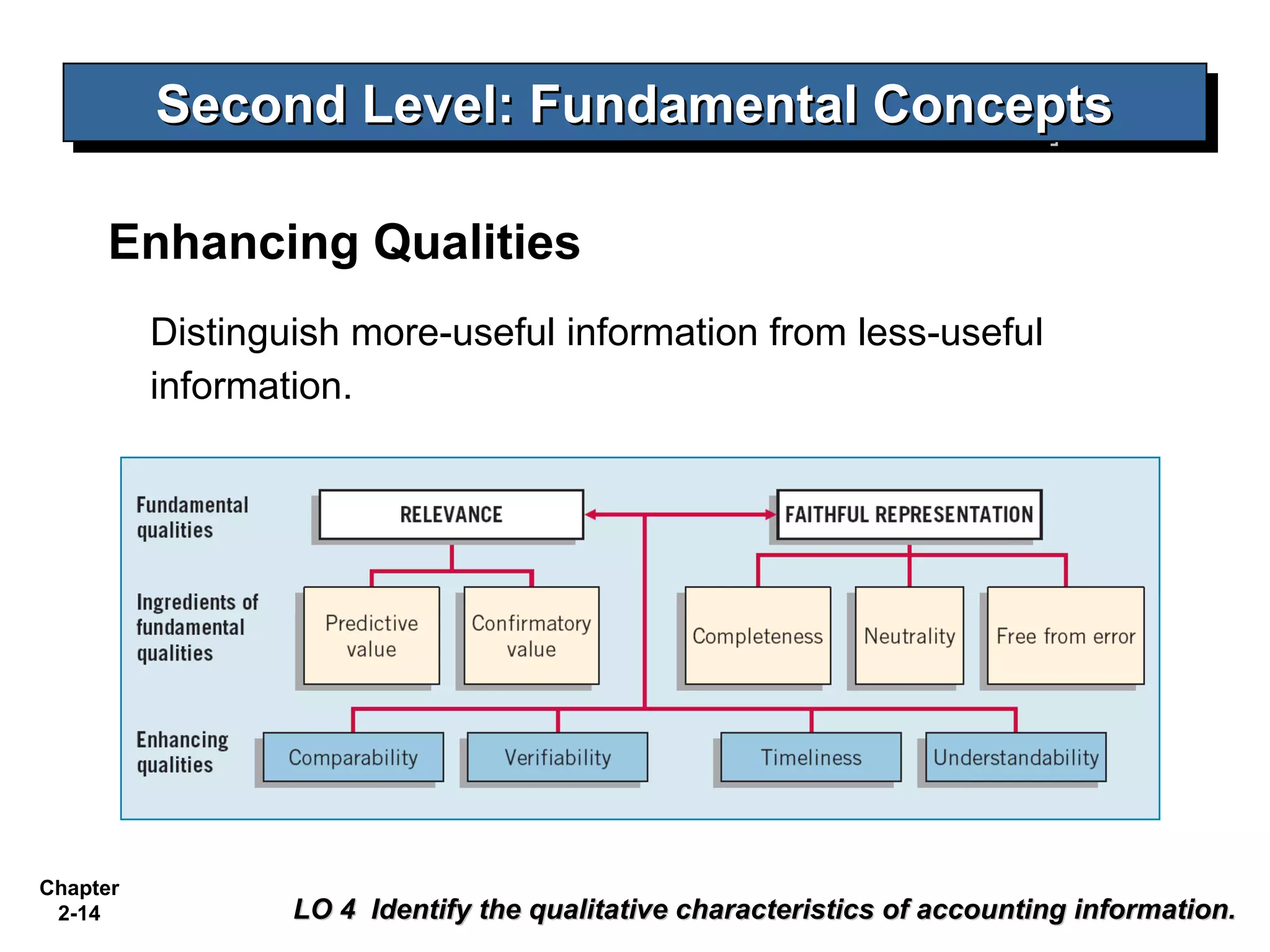

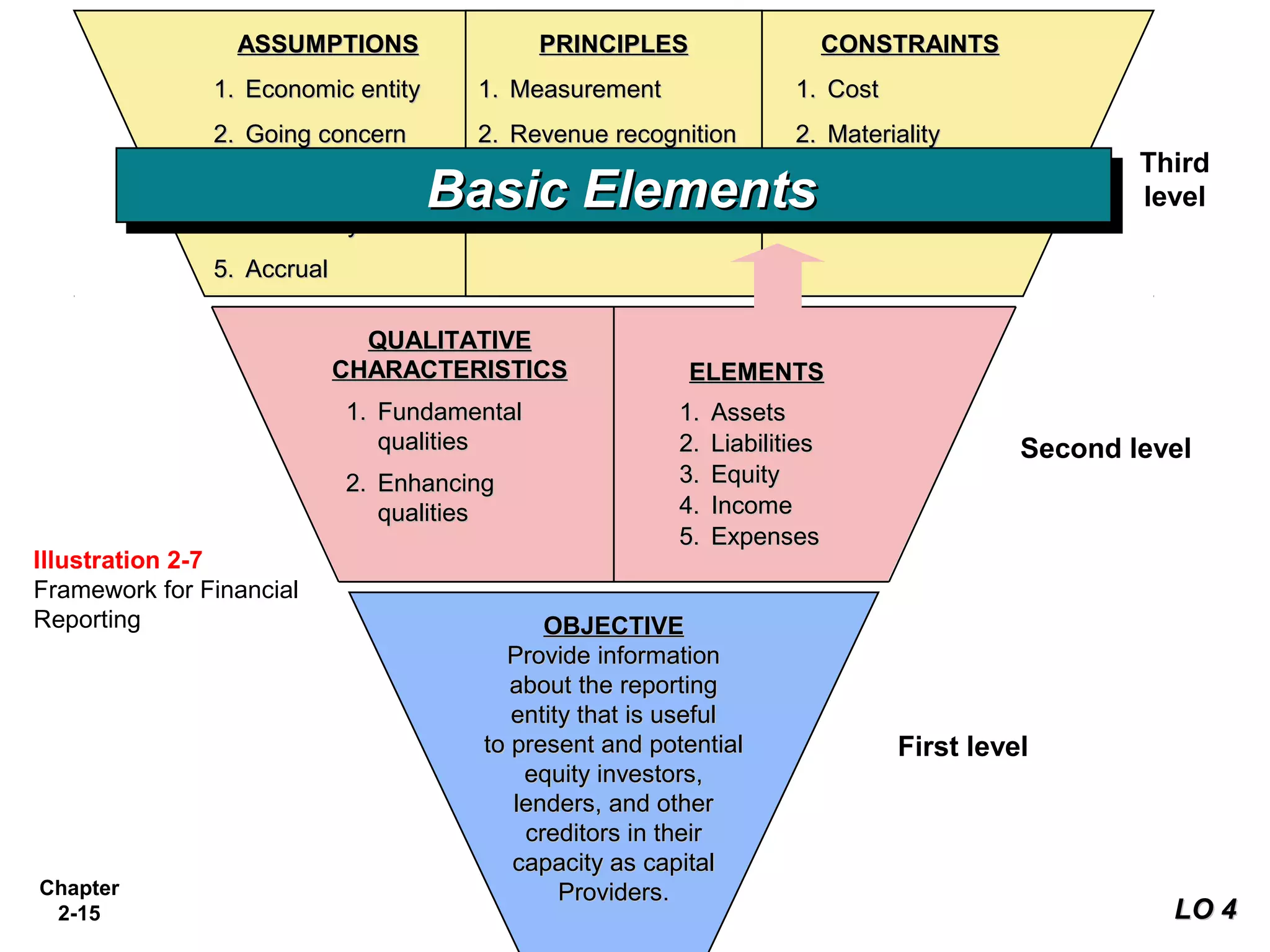

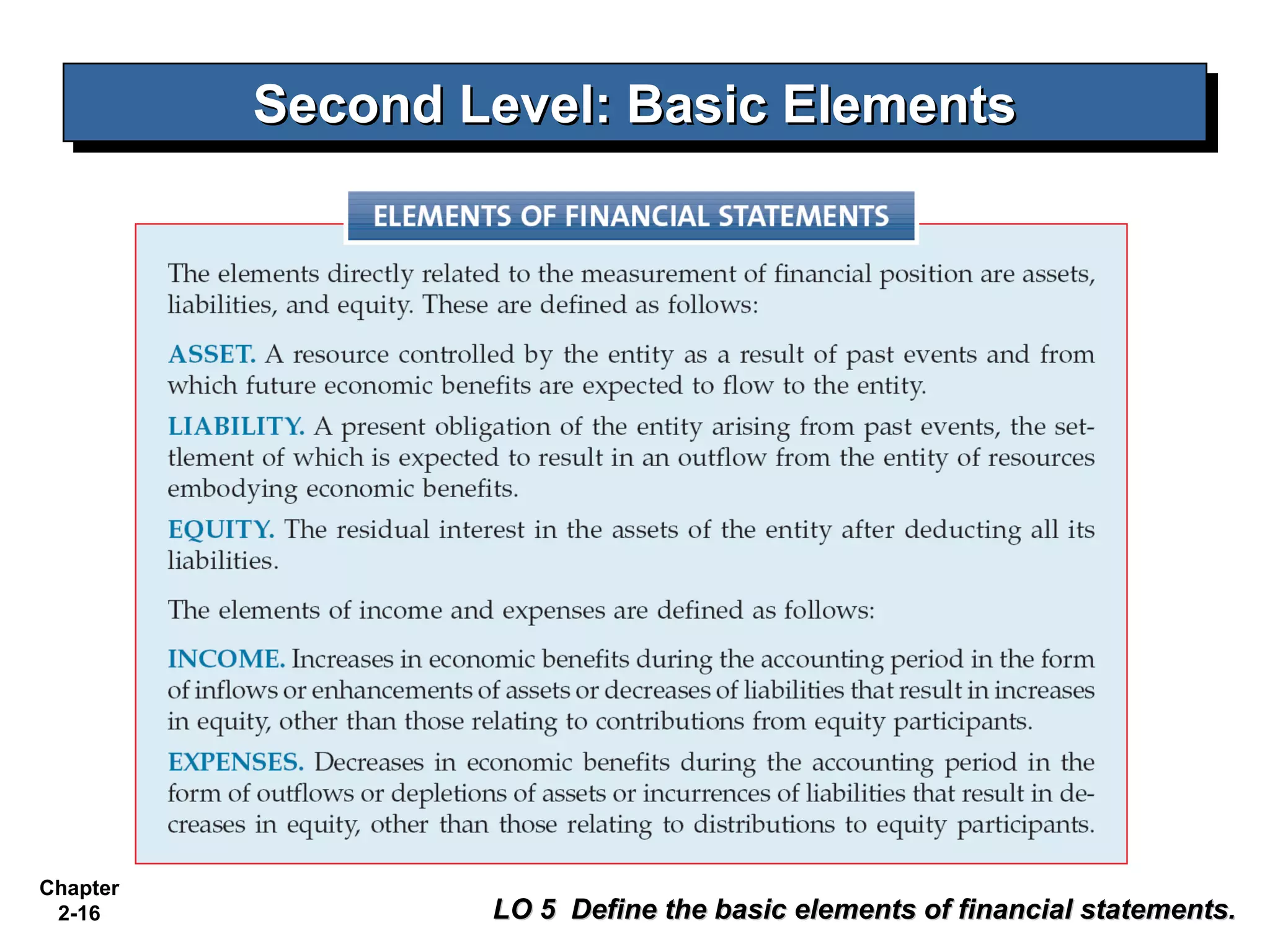

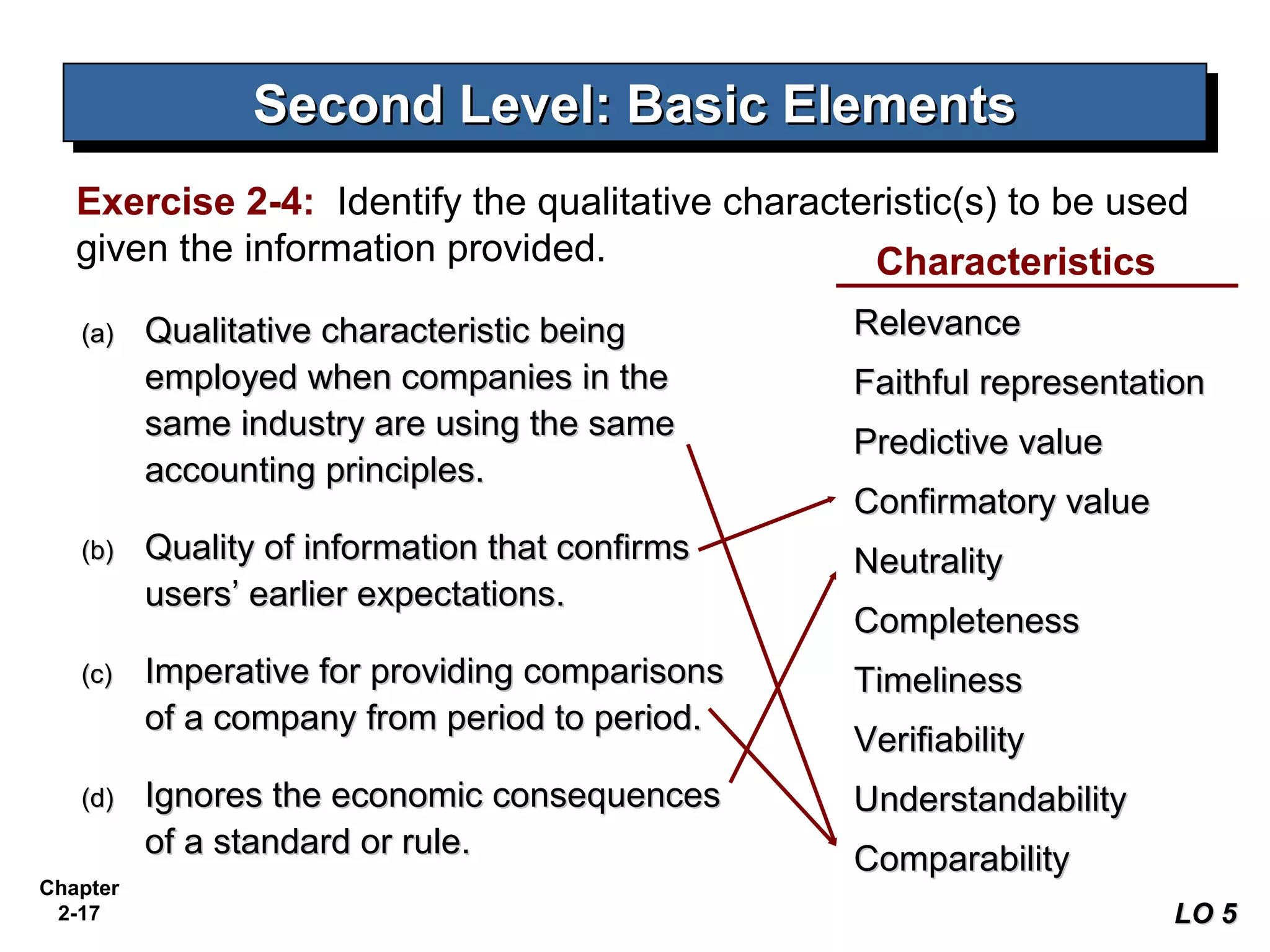

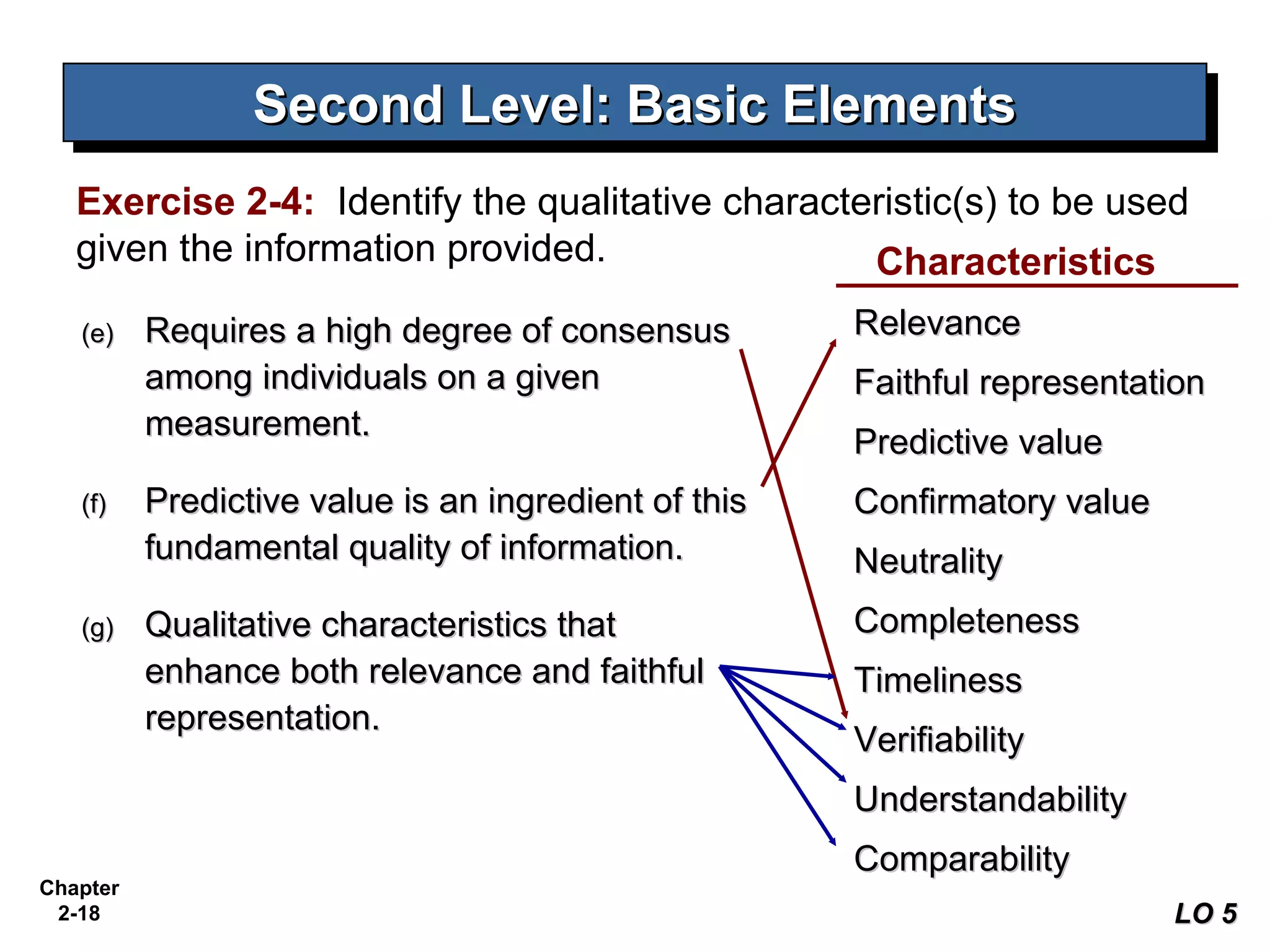

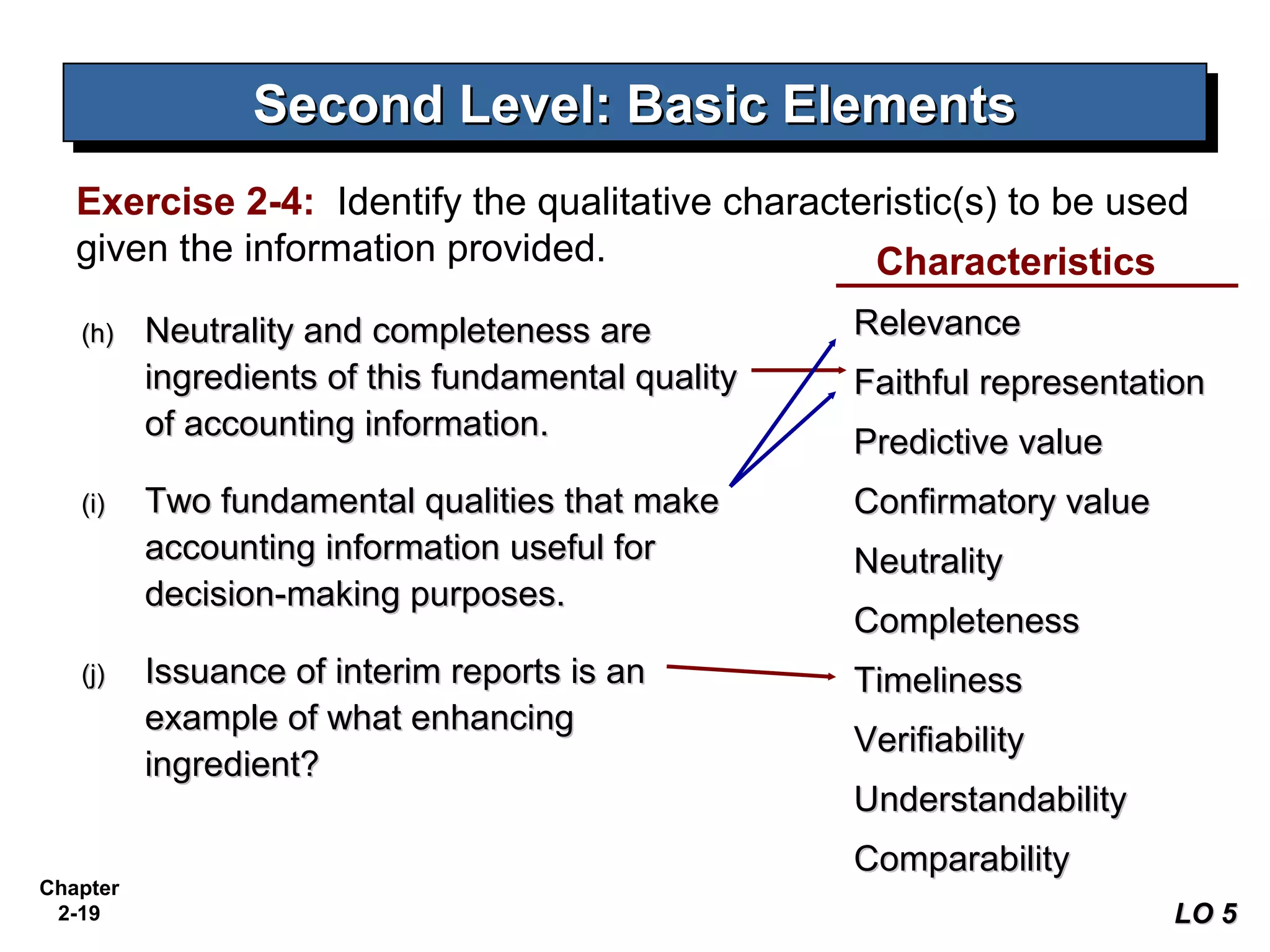

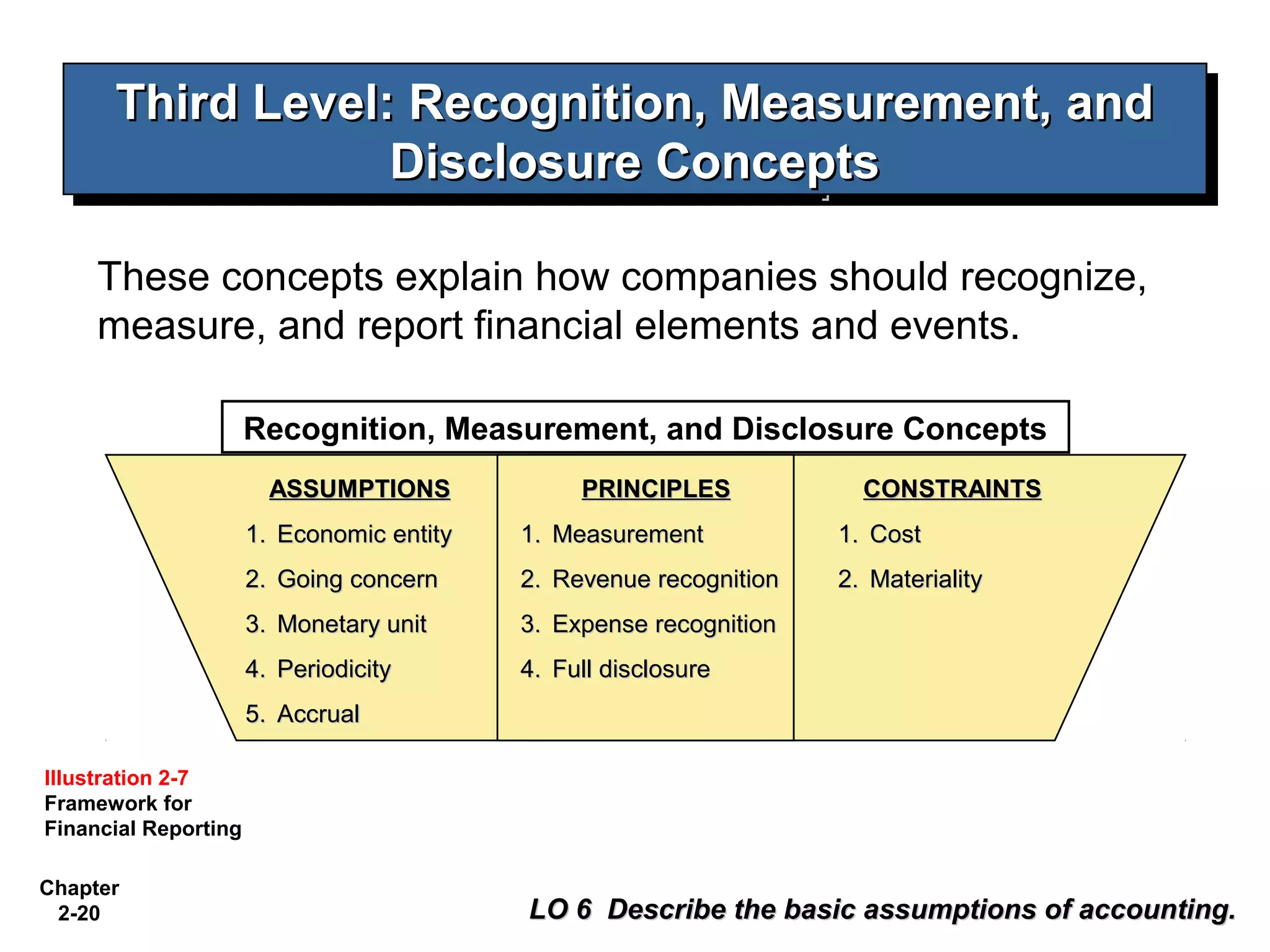

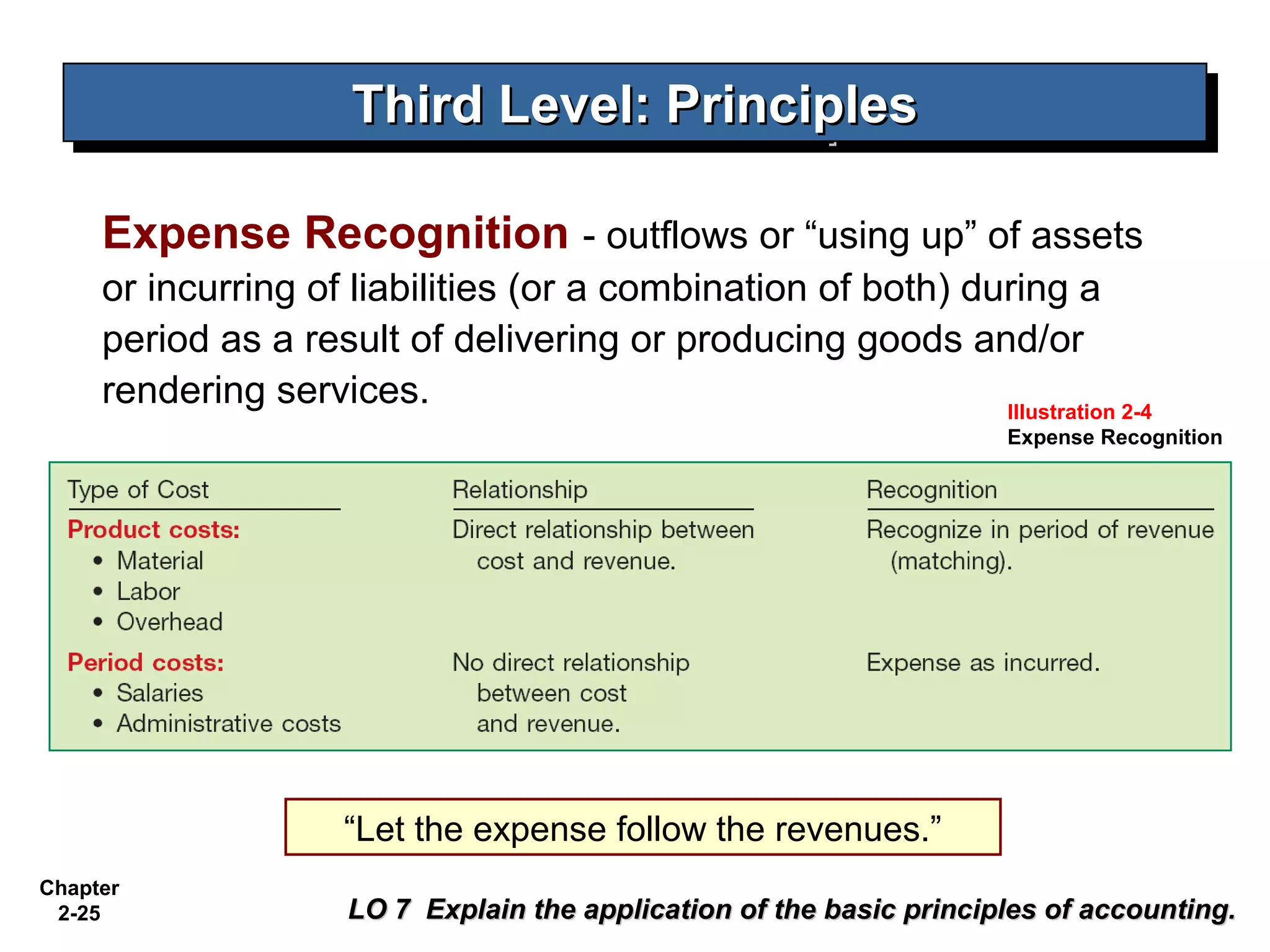

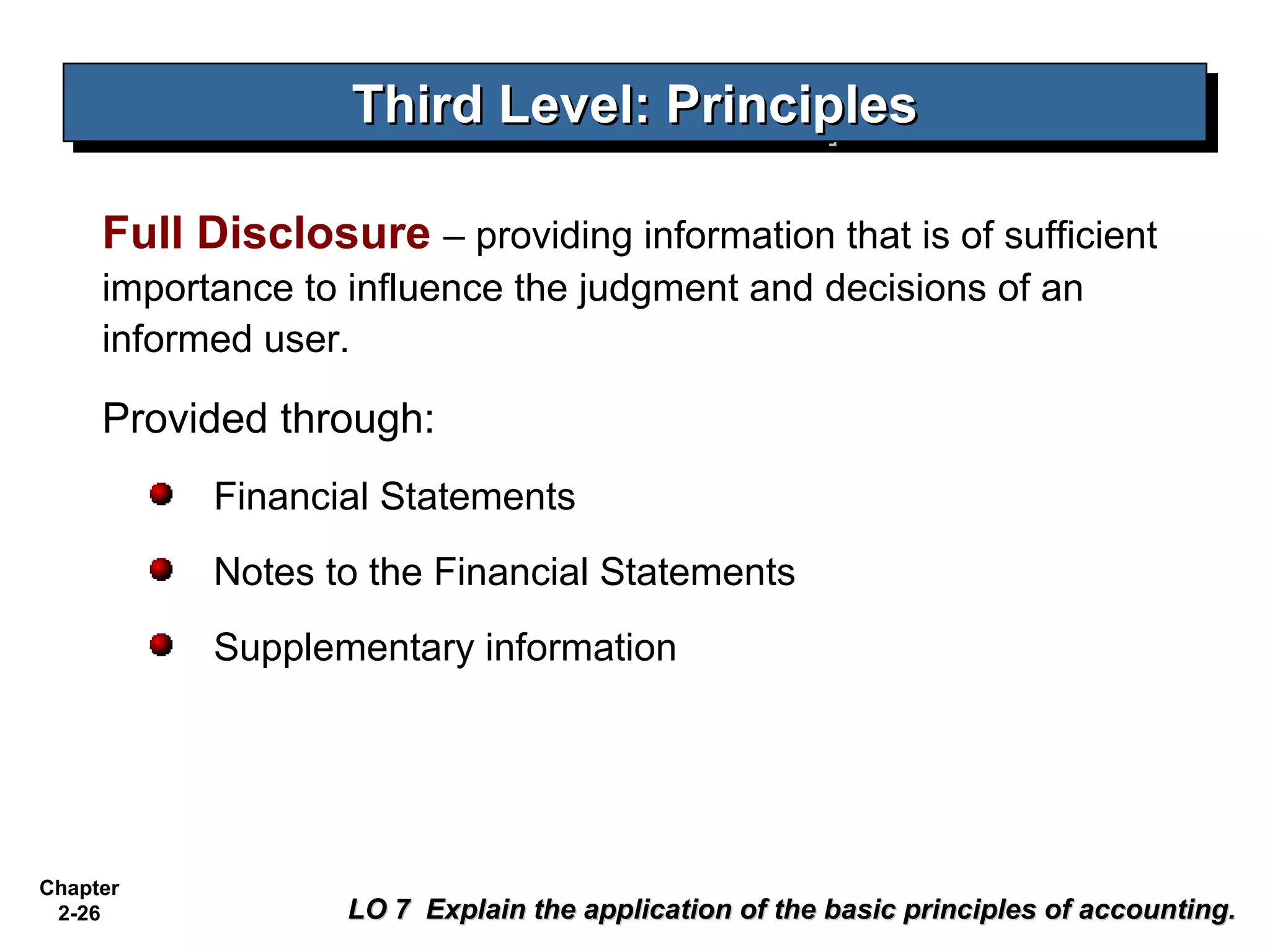

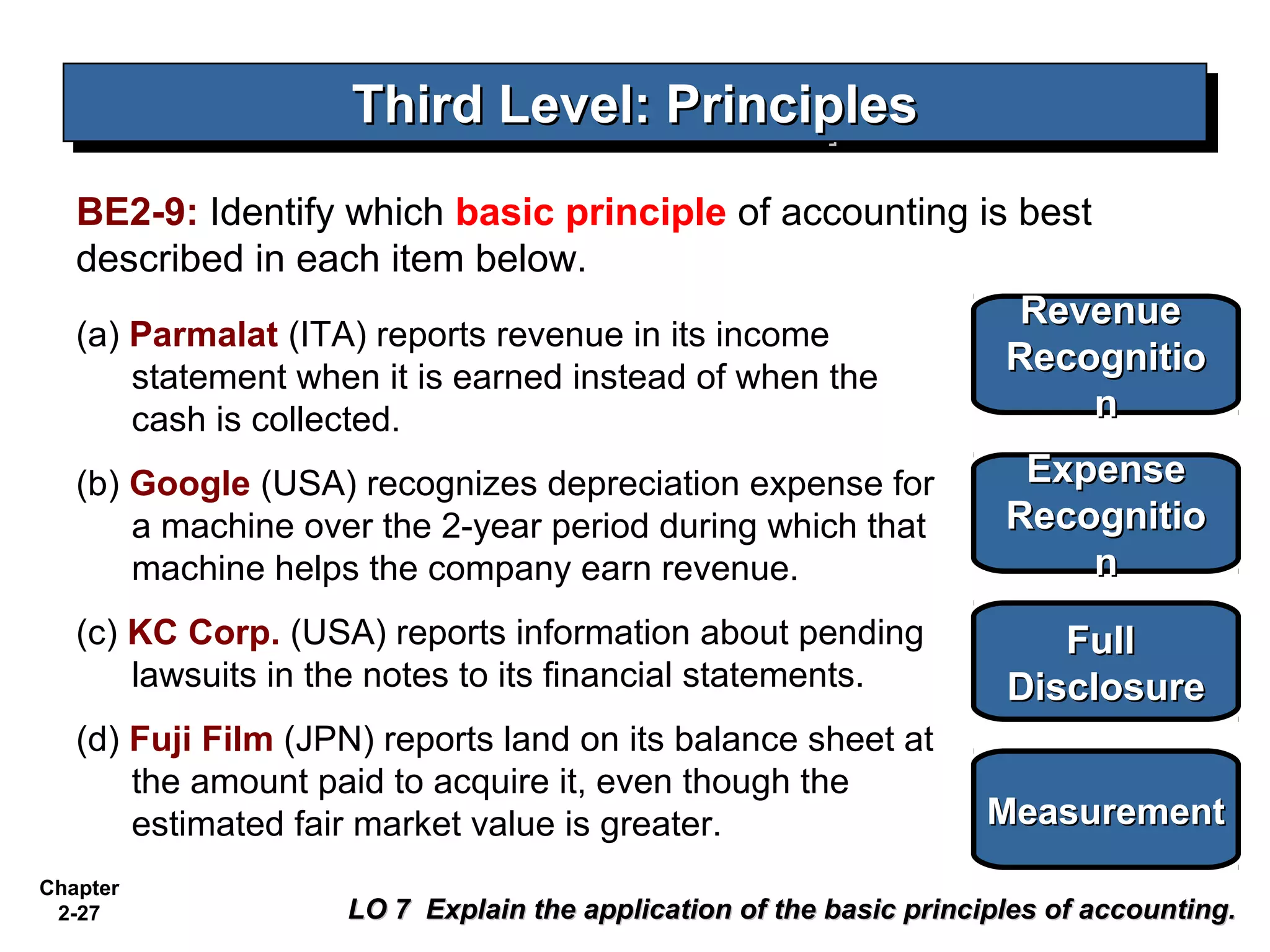

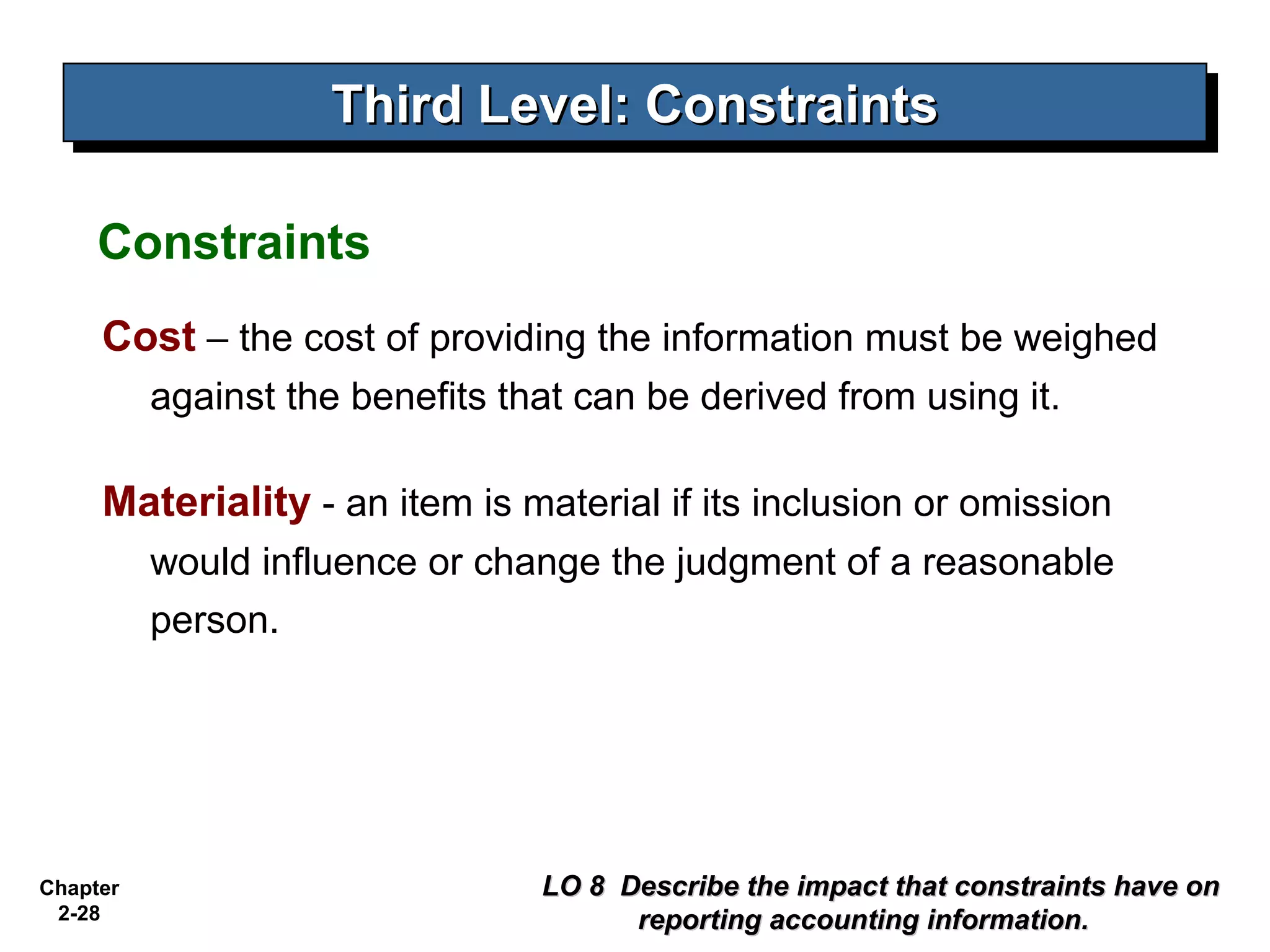

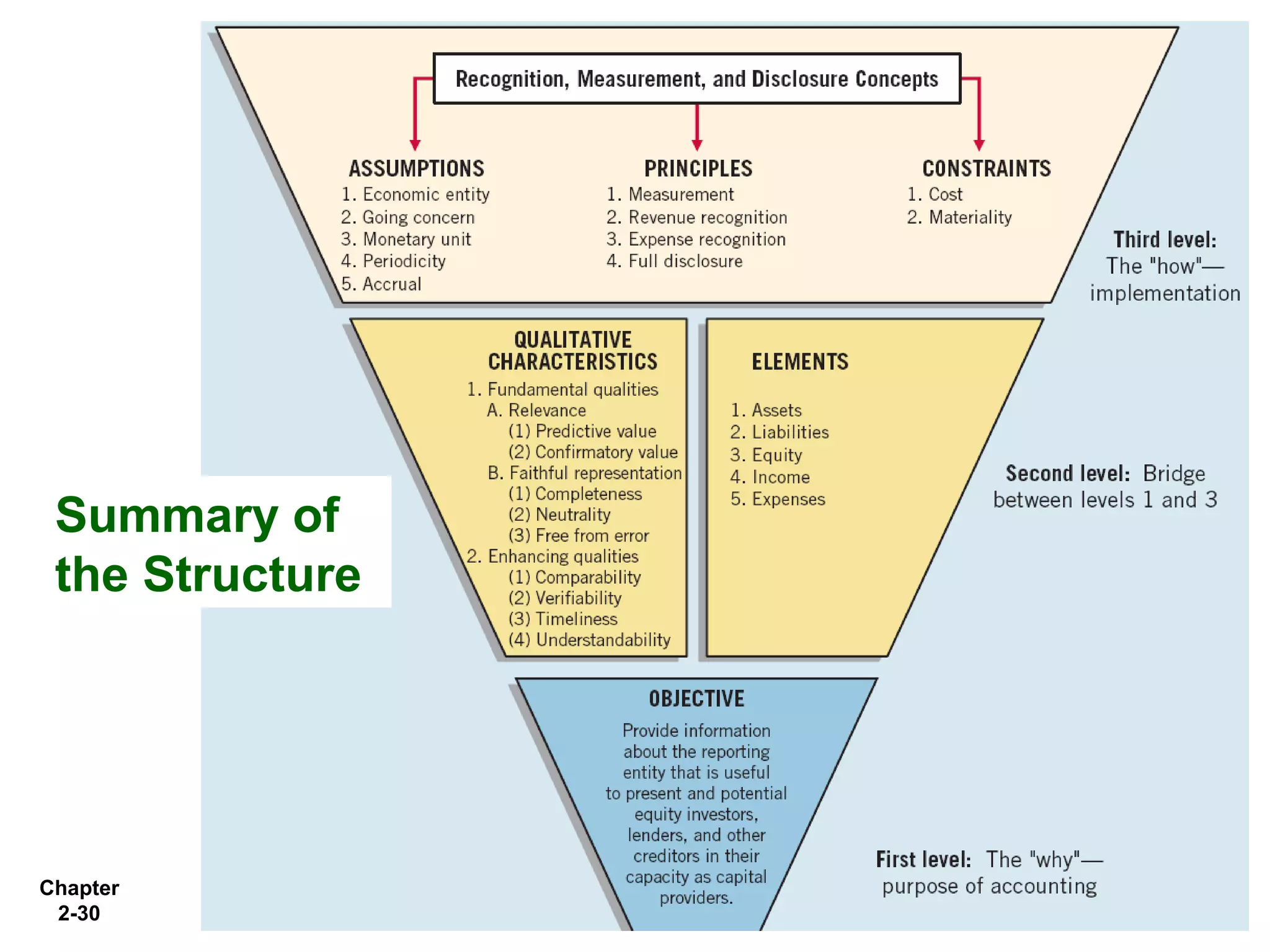

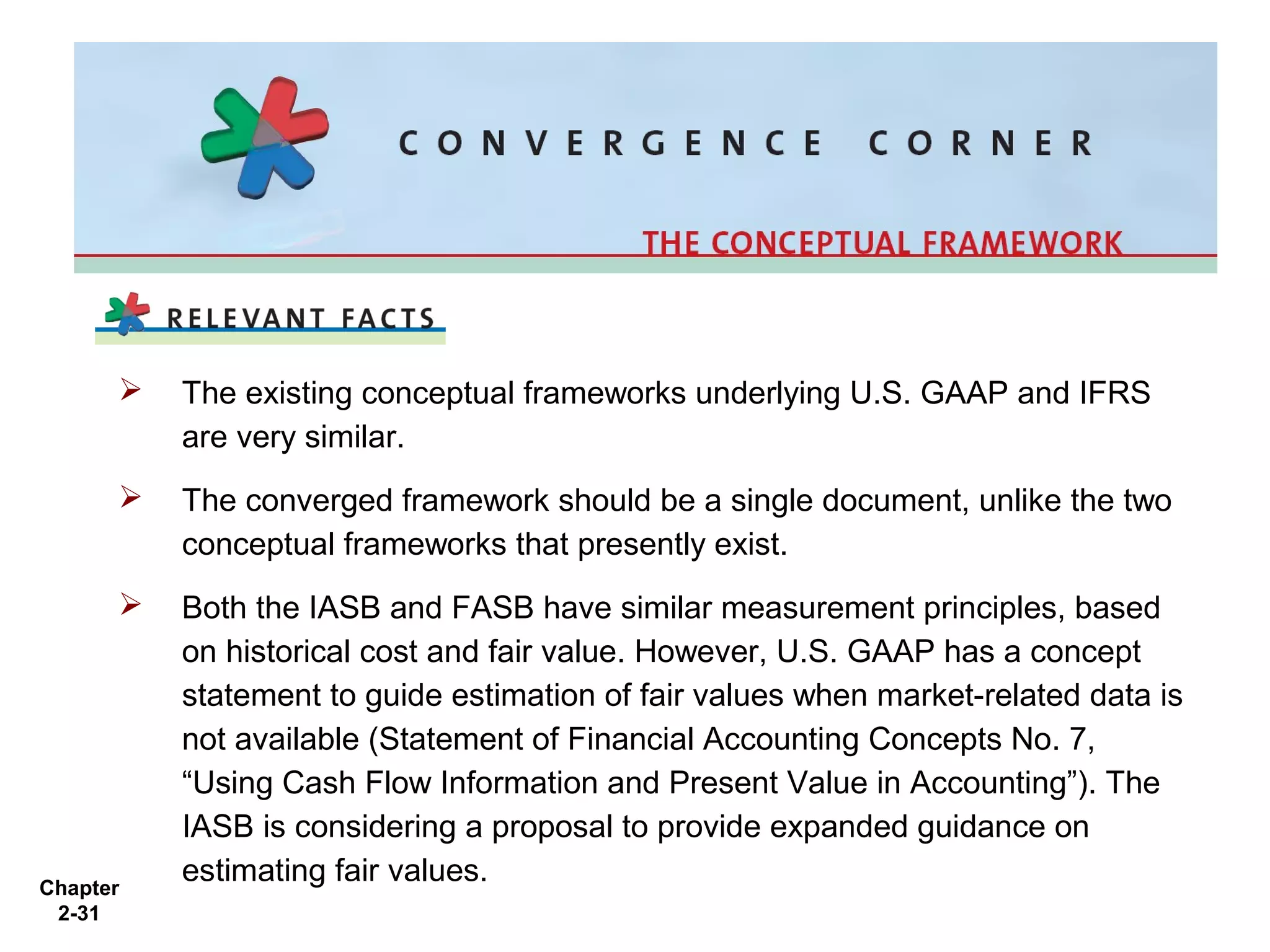

The document provides an overview of the conceptual framework for financial reporting. It discusses the need for a conceptual framework, the efforts to develop one jointly by the IASB and FASB, and the structure and key components of the conceptual framework. The conceptual framework establishes the fundamental concepts that guide financial reporting standards. It includes objectives, qualitative characteristics, elements, assumptions, principles, and constraints of financial reporting.