Chapter

2-2

C H AP T E R

C H A P T E R 2

2

CONCEPTUAL FRAMEWORK FOR

CONCEPTUAL FRAMEWORK FOR

FINANCIAL REPORTING

FINANCIAL REPORTING

Intermediate Accounting

IFRS Edition

Kieso, Weygandt, and Warfield

3.

Chapter

2-3

Conceptual

Conceptual

Framework

Framework

First Level: Basic

FirstLevel: Basic

Objective

Objective

Second Level:

Second Level:

Fundamental

Fundamental

Concepts

Concepts

Third Level:

Third Level:

Recognition,

Recognition,

Measurement, and

Measurement, and

Disclosure

Disclosure

Concepts

Concepts

Need

Need

Development

Development

Overview

Overview

Qualitative

Qualitative

characteristics

characteristics

Basic elements

Basic elements

Basic assumptions

Basic assumptions

Basic principles

Basic principles

Constraints

Constraints

Summary of the

Summary of the

structure

structure

Conceptual Framework For Financial Reporting

Conceptual Framework For Financial Reporting

4.

Chapter

2-4

Need for aConceptual Framework

Rule-making should build on and relate to an

established body of concepts.

Enables IASB to issue more useful and consistent

pronouncements over time.

Conceptual Framework

Conceptual Framework

LO 1 Describe the usefulness of a conceptual framework.

LO 1 Describe the usefulness of a conceptual framework.

Conceptual Framework

Conceptual Framework establishes the concepts

that underlie financial reporting.

5.

Chapter

2-5

Development of aConceptual Framework

IASB and FASB are working on a joint project to

develop a common conceptual framework

Framework will build on existing IASB and FASB

frameworks.

Project has identified the objective of financial

reporting (Chapter 1) and the qualitative

characteristics of decision-useful financial reporting

information.

Conceptual Framework

Conceptual Framework

LO 2 Describe efforts to construct a conceptual framework.

LO 2 Describe efforts to construct a conceptual framework.

6.

Chapter

2-6

Three levels:

First Level= Basic objective

Second Level = Qualitative characteristics and

elements of financial statements

Third Level = Recognition, measurement, and

disclosure concepts

Conceptual Framework

Conceptual Framework

LO 2 Describe efforts to construct a conceptual framework.

LO 2 Describe efforts to construct a conceptual framework.

Overview of the Conceptual Framework

7.

Chapter

2-7

LO 2 Describeefforts to construct

LO 2 Describe efforts to construct

a conceptual framework.

a conceptual framework.

ASSUMPTIONS

ASSUMPTIONS

1.

1. Economic entity

Economic entity

2.

2. Going concern

Going concern

3.

3. Monetary unit

Monetary unit

4.

4. Periodicity

Periodicity

5.

5. Accrual

Accrual

PRINCIPLES

PRINCIPLES

1.

1. Measurement

Measurement

2.

2. Revenue recognition

Revenue recognition

3.

3. Expense recognition

Expense recognition

4.

4. Full disclosure

Full disclosure

CONSTRAINTS

CONSTRAINTS

1.

1. Cost

Cost

2.

2. Materiality

Materiality

OBJECTIVE

OBJECTIVE

Provide information

Provide information

about the reporting

about the reporting

entity that is useful

entity that is useful

to present and potential

to present and potential

equity investors,

equity investors,

lenders, and other

lenders, and other

creditors in their

creditors in their

capacity as capital

capacity as capital

Providers.

Providers.

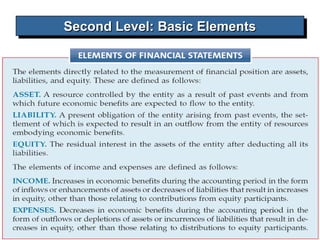

ELEMENTS

ELEMENTS

1.

1. Assets

Assets

2.

2. Liabilities

Liabilities

3.

3. Equity

Equity

4.

4. Income

Income

5.

5. Expenses

Expenses

Illustration 2-7

Framework for Financial

Reporting

First level

Second level

Third

level

QUALITATIVE

QUALITATIVE

CHARACTERISTICS

CHARACTERISTICS

1.

1. Fundamental

Fundamental

qualities

qualities

2.

2. Enhancing

Enhancing

qualities

qualities

8.

Chapter

2-8

“To provide financialinformation about the reporting

entity that is useful to present and potential equity

investors, lenders, and other creditors in making

decisions in their capacity as capital providers.”

First Level: Basic Objective

First Level: Basic Objective

LO 3 Understand the objectives of financial reporting.

LO 3 Understand the objectives of financial reporting.

OBJECTIVE

OBJECTIVE

Provided by issuing general-purpose financial

statements.

Assumption is that users have reasonable knowledge

of business and financial accounting matters to

understand the information.

9.

Chapter

2-9

IASB identified theQualitative Characteristics

of accounting information that distinguish

better (more useful) information from inferior

(less useful) information for decision-making

purposes.

Second Level: Fundamental Concepts

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

LO 4 Identify the qualitative characteristics of accounting information.

Qualitative Characteristics of Accounting

Information

10.

Chapter

2-10

Illustration 2-2

Hierarchy ofAccounting

Qualities

Second Level: Fundamental Concepts

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

LO 4 Identify the qualitative characteristics of accounting information.

11.

Chapter

2-11

Fundamental Quality -Relevance

Relevance is one of the two fundamental qualities that

make accounting information useful for decision-

making.

Second Level: Fundamental Concepts

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

LO 4 Identify the qualitative characteristics of accounting information.

12.

Chapter

2-12

Fundamental Quality –Faithful Representation

Faithful representation means that the numbers and

descriptions match what really existed or happened.

Second Level: Fundamental Concepts

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

LO 4 Identify the qualitative characteristics of accounting information.

13.

Chapter

2-13

Enhancing Qualities

Distinguish more-usefulinformation from less-useful

information.

Second Level: Fundamental Concepts

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

LO 4 Identify the qualitative characteristics of accounting information.

14.

Chapter

2-14

ASSUMPTIONS

ASSUMPTIONS

1.

1. Economic entity

Economicentity

2.

2. Going concern

Going concern

3.

3. Monetary unit

Monetary unit

4.

4. Periodicity

Periodicity

5.

5. Accrual

Accrual

PRINCIPLES

PRINCIPLES

1.

1. Measurement

Measurement

2.

2. Revenue recognition

Revenue recognition

3.

3. Expense recognition

Expense recognition

4.

4. Full disclosure

Full disclosure

CONSTRAINTS

CONSTRAINTS

1.

1. Cost

Cost

2.

2. Materiality

Materiality

OBJECTIVE

OBJECTIVE

Provide information

Provide information

about the reporting

about the reporting

entity that is useful

entity that is useful

to present and potential

to present and potential

equity investors,

equity investors,

lenders, and other

lenders, and other

creditors in their

creditors in their

capacity as capital

capacity as capital

Providers.

Providers.

ELEMENTS

ELEMENTS

1.

1. Assets

Assets

2.

2. Liabilities

Liabilities

3.

3. Equity

Equity

4.

4. Income

Income

5.

5. Expenses

Expenses

Illustration 2-7

Framework for Financial

Reporting

First level

Second level

Third

level

QUALITATIVE

QUALITATIVE

CHARACTERISTICS

CHARACTERISTICS

1.

1. Fundamental

Fundamental

qualities

qualities

2.

2. Enhancing

Enhancing

qualities

qualities

Basic Elements

Basic Elements

LO 4

LO 4

Chapter

2-16

Third Level: Recognition,Measurement, and

Third Level: Recognition, Measurement, and

Disclosure Concepts

Disclosure Concepts

These concepts explain how companies should

recognize, measure, and report financial elements and

events.

ASSUMPTIONS

ASSUMPTIONS

1.

1. Economic entity

Economic entity

2.

2. Going concern

Going concern

3.

3. Monetary unit

Monetary unit

4.

4. Periodicity

Periodicity

5.

5. Accrual

Accrual

PRINCIPLES

PRINCIPLES

1.

1. Measurement

Measurement

2.

2. Revenue recognition

Revenue recognition

3.

3. Expense recognition

Expense recognition

4.

4. Full disclosure

Full disclosure

CONSTRAINTS

CONSTRAINTS

1.

1. Cost

Cost

2.

2. Materiality

Materiality

LO 6 Describe the basic assumptions of accounting.

LO 6 Describe the basic assumptions of accounting.

Recognition, Measurement, and Disclosure Concepts

Illustration 2-7

Framework for

Financial Reporting

17.

Chapter

2-17

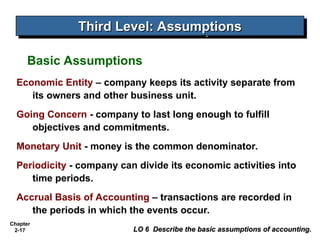

Economic Entity –company keeps its activity separate from

its owners and other business unit.

Going Concern - company to last long enough to fulfill

objectives and commitments.

Monetary Unit - money is the common denominator.

Periodicity - company can divide its economic activities into

time periods.

Accrual Basis of Accounting – transactions are recorded in

the periods in which the events occur.

LO 6 Describe the basic assumptions of accounting.

LO 6 Describe the basic assumptions of accounting.

Third Level: Assumptions

Third Level: Assumptions

Basic Assumptions

18.

Chapter

2-18

Measurement

Cost is generallythought to be a faithful

representation of the amount paid for a given item.

Fair value is “the amount for which an asset could be

exchanged, a liability settled, or an equity instrument

granted could be exchanged, between knowledgeable,

willing parties in an arm’s length transaction.”

IASB has taken the step of giving companies the

option to use fair value as the basis for measurement

of financial assets and financial liabilities.

Third Level: Principles

Third Level: Principles

Principles

19.

Chapter

2-19

Revenue Recognition -revenue is to be recognized when

it is probable that future economic benefits will flow to the

company and reliable measurement of the amount of revenue

is possible.

Third Level: Principles

Third Level: Principles

LO 7 Explain the application of the basic principles of accounting.

LO 7 Explain the application of the basic principles of accounting.

Illustration 2-3

Timing of Revenue Recognition

20.

Chapter

2-20

Expense Recognition -outflows or “using up” of

assets or incurring of liabilities (or a combination of both)

during a period as a result of delivering or producing

goods and/or rendering services.

Third Level: Principles

Third Level: Principles

LO 7 Explain the application of the basic principles of accounting.

LO 7 Explain the application of the basic principles of accounting.

Illustration 2-4

Expense Recognition

“Let the expense follow the revenues.”

21.

Chapter

2-21

Full Disclosure –providing information that is of

sufficient importance to influence the judgment and

decisions of an informed user.

Provided through:

Financial Statements

Notes to the Financial Statements

Supplementary information

Third Level: Principles

Third Level: Principles

LO 7 Explain the application of the basic principles of accounting.

LO 7 Explain the application of the basic principles of accounting.

22.

Chapter

2-22

Cost – thecost of providing the information must be

weighed against the benefits that can be derived

from using it.

Materiality - an item is material if its inclusion or

omission would influence or change the judgment

of a reasonable person.

Third Level: Constraints

Third Level: Constraints

LO 8 Describe the impact that constraints have on

LO 8 Describe the impact that constraints have on

reporting accounting information.

reporting accounting information.

Constraints

Chapter

2-24

The existingconceptual frameworks underlying U.S. GAAP and IFRS

are very similar.

The converged framework should be a single document, unlike the two

conceptual frameworks that presently exist.

Both the IASB and FASB have similar measurement principles, based

on historical cost and fair value. However, U.S. GAAP has a concept

statement to guide estimation of fair values when market-related data is

not available (Statement of Financial Accounting Concepts No. 7,

“Using Cash Flow Information and Present Value in Accounting”). The

IASB is considering a proposal to provide expanded guidance on

estimating fair values.