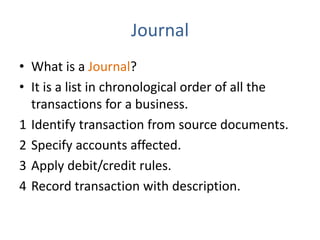

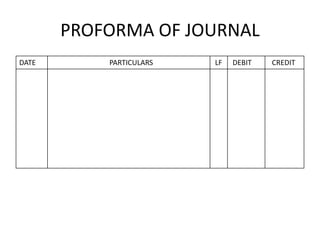

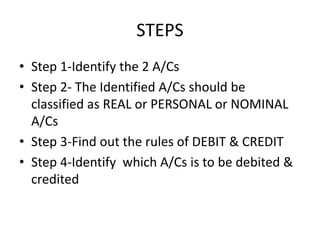

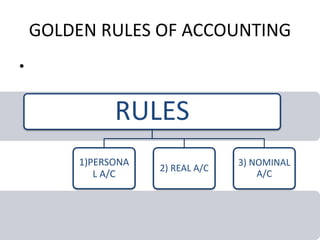

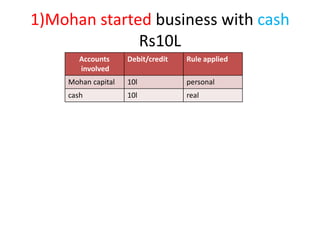

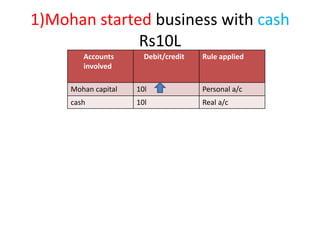

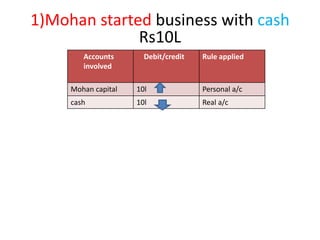

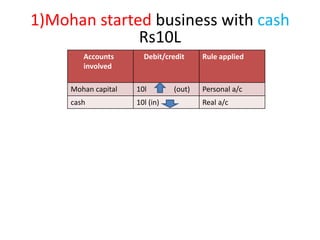

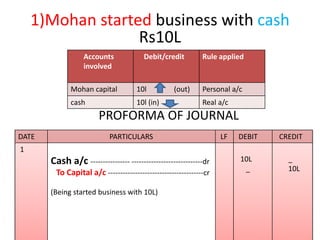

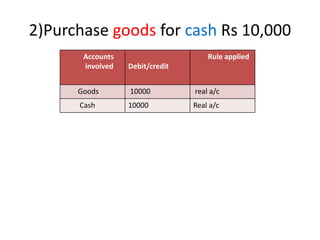

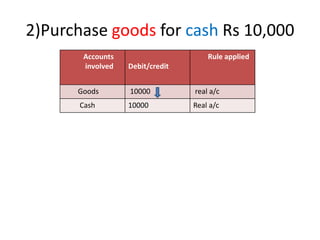

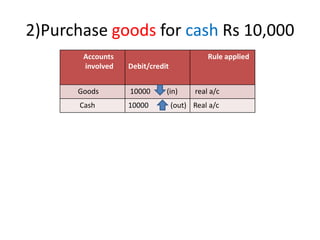

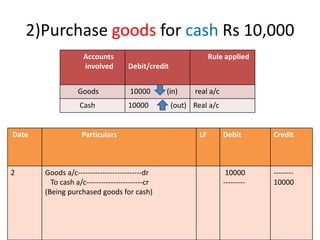

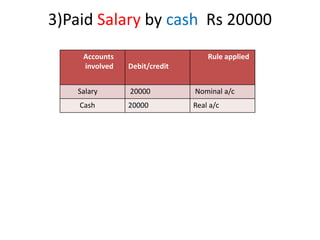

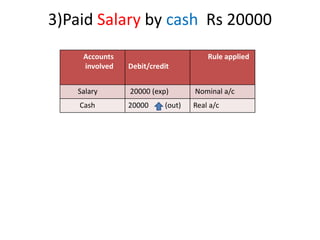

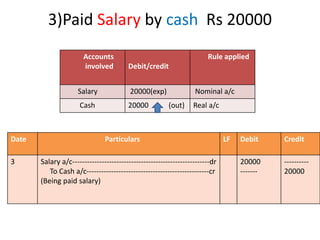

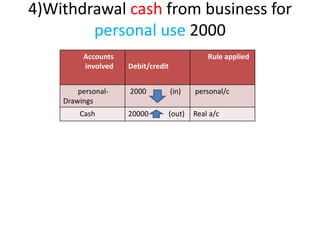

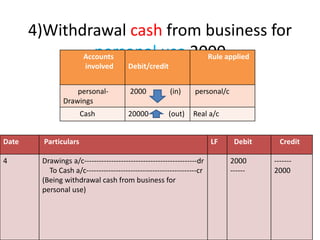

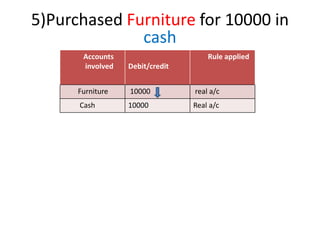

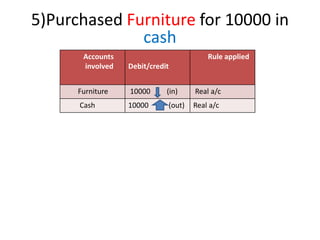

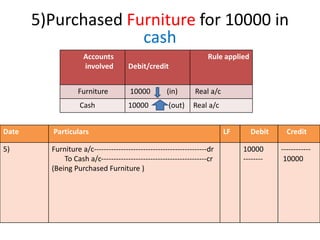

The document discusses journal entries in accounting. It defines a journal as a chronological list of all business transactions that identifies the affected accounts, applies debit and credit rules, and records the transaction description. It provides examples of journal entries for various common transactions like starting a business, purchasing goods or assets, paying expenses, and withdrawing cash. For each transaction, it identifies the involved accounts, classifies them as personal, real or nominal, and applies the relevant debit and credit rules to record the transaction in journal entry format.