Downloaded 19 times

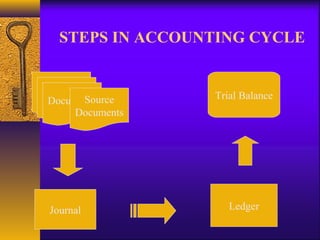

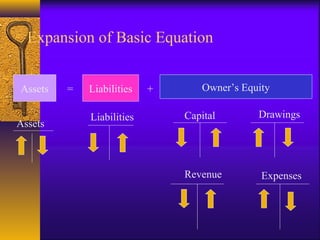

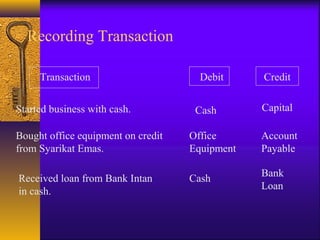

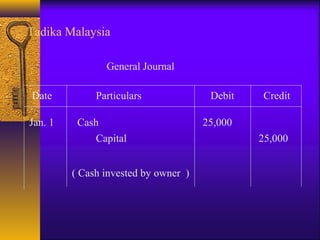

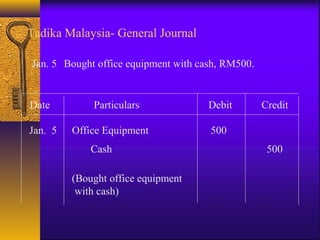

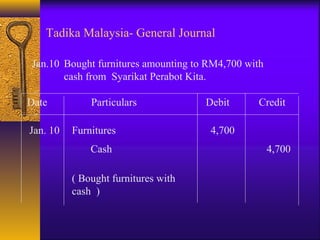

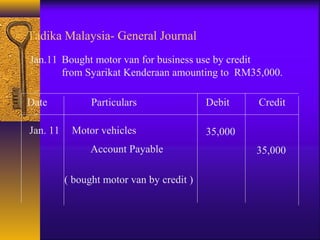

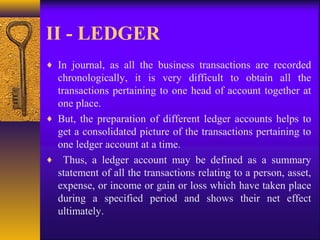

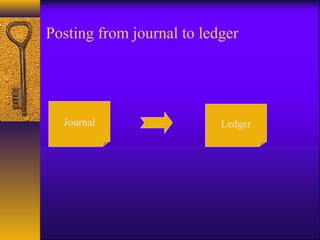

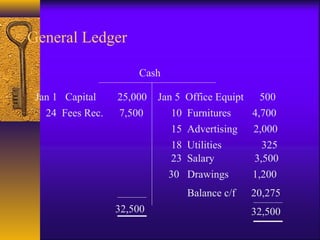

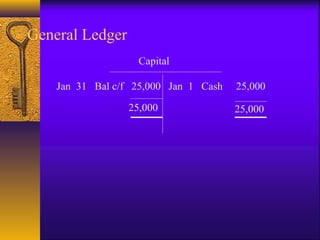

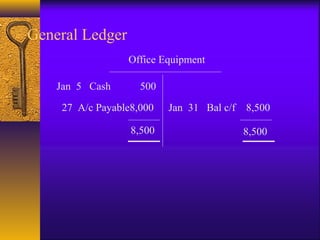

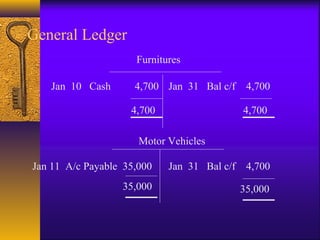

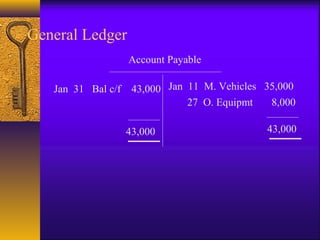

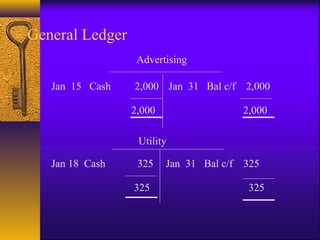

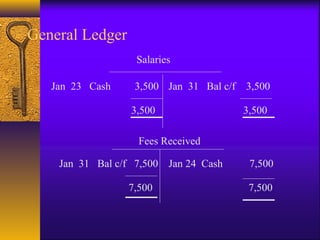

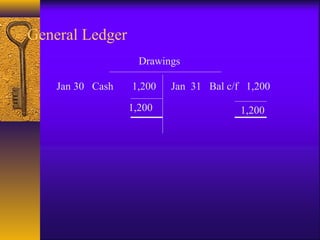

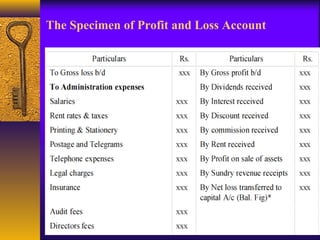

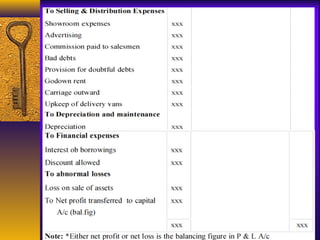

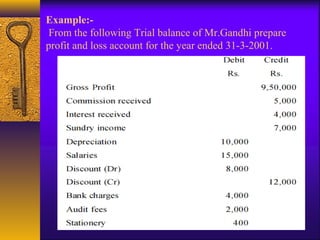

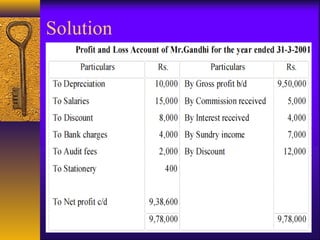

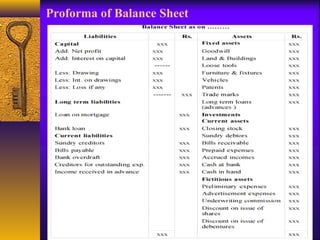

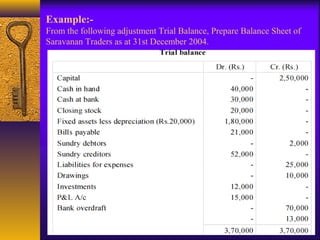

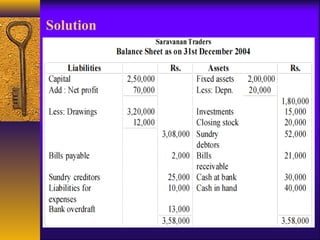

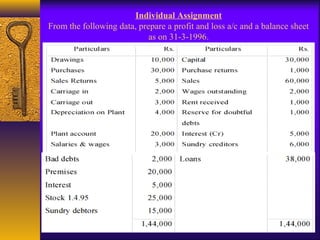

This document discusses key accounting concepts such as bookkeeping, accounting, the accounting cycle, and financial statements. It defines bookkeeping as recording transactions and accounting as analyzing an organization's performance. The accounting cycle involves recording transactions in journals, posting to ledgers, preparing a trial balance, and ultimately financial statements including trading accounts, profit and loss statements, and balance sheets. Trading accounts determine gross profit or loss, profit and loss statements calculate net profit or loss, and balance sheets present the financial position of an organization by listing assets, liabilities, and capital. Examples are provided to illustrate journal entries, ledger accounts, trial balances, and basic financial statements.